I’ve had a few emails asking me this very question: “Do I need to own a house to retire early?”

Sometimes in Australia it’s just assumed that everybody aspires (or should aspire) to own a home.

But there are plenty of folks who are happy renting and they have no interest in owning property, for a variety of reasons.

Some don’t care either way, but simply prefer owning investments like shares, rather than the roof over their head.

But is that a problem when it comes to early retirement? Are you on rocky ground if you plan to rent forever? That’s what we’ll get into today.

It’s an interesting topic with emotions involved and many aspects to discuss. As always, there are benefits on each side. So we’ll run through those and I’ll also share what we’re doing and our future plans.

In the blue corner, we have home ownership. Here are the points that come to mind in favour of owning your own place if you want to retire early…

You won’t be forced to move by a landlord who wants to move in, renovate, or sell the property. This offers huge peace of mind in retirement and is hard to put a price on.

This means you can decorate however you want, dig up concrete to put in a veggie patch, install solar panels, etc.

You’ll pay no capital gains tax (CGT) when you sell your home – even for a large profit.

Also, the value of your residence is not included in the ‘assets test’ for the pension or unemployment benefits. This is a huge benefit later in life and as a backup plan, but it also may not stay this way forever.

This can be used as an emergency fund/buffer or for investment opportunities. Banks will lend large amounts at relatively cheap interest rates against residential property.

This leverage can be used to increase your investments, or be more fully invested and have less cash laying around, since there is easy access to a cheap emergency fund via a line of credit or similar.

Let’s say half your spending is for housing and the other half for other living costs. In this case, half becomes locked in and paid for.

So this means less reliance on investments to cover your annual spending. As we know, returns from shares (including dividends) , can vary from year to year and are not ‘locked in’.

I see this as a large psychological benefit. Having less money leaving the bank account every month is arguably a more enjoyable situation for your finances in retirement.

Plus, if your investments are going through a rough patch, it’s much easier to plug the gap with part-time work. Compare that to renting and relying 100% on investments (see above), where a downturn can have more of an effect and create a bigger ‘gap’ to cover.

In the red corner, we have renting. Let’s run through some of the upsides to retiring early while not owning your own place.

With a rental, you can switch locations, move interstate, or pack-up and go travelling with none of the major costs or complexity involved with owning.

Moving house while owning is going to cost an absolute fortune in stamp duty and agents fees alone – often 5-8% of the property value. This would be $30k-$50k for a $600k property. Painful!

Let’s say your situation has changed. Your investments aren’t going as well as expected, or you have a large unexpected expense. When renting, you can easily trade your current place to a lower cost home when the lease expires.

On the other hand, if things are going well and you find yourself with extra income and wealth in retirement, trading up and renting a swanky beachside or city residence is equally simple. This way, you get to have fun experimenting with different locations, property types and lifestyles to see which you like best.

Not owning a house means all your cash can be tucked away in investments which should provide higher returns over time. This may or may not be important to you in retirement.

Sure, owning saves you rent, but comes with tons of other costs. Plus, long term performance of the sharemarket is driven by company profits, which are likely to grow faster than rents over time.

Owning a home means having a massive amount of savings tied up in one asset, in one location. This concerns some people, who would prefer to spread their money across a large number of assets.

Having 100% investments allows you to control exactly where those dollars are sitting. Aussie and international shares. Local or global real estate investment trusts. Emerging markets. Individual companies. Your local fish ‘n’ chip shop?

For similar properties in most cities renting is still the cheaper option Even a paid-off house comes with the following ongoing expenses: Council rates. Water rates. Insurance. Strata fees. Maintenance. Upgrades over time. Huge moving costs.

Renting comes with a clear monthly cost, with no hidden surprises. The hidden costs of owning are massively under-counted most of the time (more below). This difference often means that in Australia, less wealth is needed to retire in the first place.

Owning property means everyone has their hand out. Governments and councils are seemingly always looking for ways to increase revenue, by hiking taxes/charges to property owners.

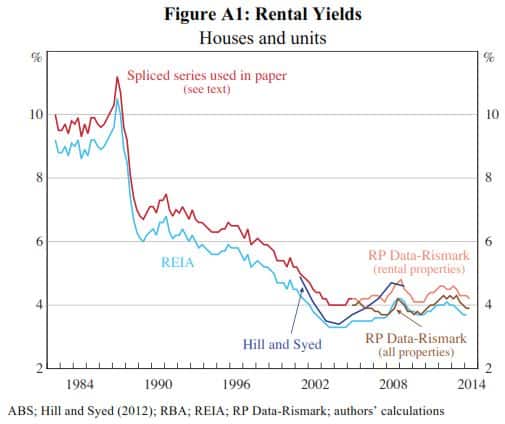

Stamp duty has kept increasing over decades (even faster than home prices). And home prices have continued growing faster than rents (evident from rental yields declining over decades).

Not to mention council rates, insurance and strata fees rarely seem to fall, even if house prices and rents do. In fact, they often still rise. Trust me, I’m a Perth property owner with first-hand experience here 😉

Rents rise over time too, of course. But relentlessly rising stamp duty and ownership costs disproportionately hurt owners and very much favours renting.

There’s only one hand out – the landlord’s – and it’s very clear how much we’re paying them. Not so with owning, once everything is accounted for.

For those who don’t know, here’s the story. Mrs SMA and I met, and I moved in with her. We stayed in this owner-occupied home for the entirety of our FI journey.

After leaving work, we could essentially live anywhere. So we decided to move further out of Perth, for more space, more nature and more peacefulness.

Because it’s INSANE to sell-up and move without knowing whether you’ll like the new place and enjoy living there for at least 10 years, we decided to rent. That was 3 years ago now and we’re still happily renting. Our old place is now one of our investment properties.

Down the track, we’ll sell these properties and eventually just have a share portfolio. We’re doing this slowly over time as mentioned on the blog several times.

Despite enjoying renting, we’ll almost certainly buy a place later, if we’re happy committing to the location. For the following reasons…

1 — Mrs SMA can turn as much space as she wants into veggie patches and plant her fruit trees which are currently in big pots.

2 — We can install a shitload of solar panels and hopefully run entirely on clean energy. And we may also install a water tank and look at various ways to recycle what we use.

3 — It dramatically lowers our annual living costs permanently, which gets me very irrationally excited.

4 — We’ll have access to cheap debt, should we want to put our lazy equity to use, or just have a convenient and efficient emergency fund. Then, any cash can be stored in an offset account rather than a savings account.

5 — We won’t have to move for any reason unless we feel like it. Flexibility is probably not as important to us as certainty.

You can notice a theme among the two comparisons. The benefits of home ownership skew towards security. While the positives for renting centre around freedom. I find that interesting.

There are clearly benefits to both options, and each can work well. Once again, it comes down to what suits the individual.

So, while there are benefits to doing so, you do NOT need to own a house to retire early. Despite what some may say, you are not insane if you want to keep renting!

If you value security, control, settling in, access to cheap debt, or the structural advantages of buying, then maybe owning a house in retirement is the best move for you.

But if you value freedom, flexibility, having more investments/diversification, the ability to retire a bit sooner, working your money harder or to avoid holding the cookie jar that everyone dips into, then maybe renting in retirement is a better fit.

Will you own a home when you reach Financial Independence? Or are you happy renting? Let me know what you think in the comments below…

Why deliberate spending is my favourite money management style. What it really means and how you can use it as your situation and priorities change over time.

My thoughts on ‘The Great Taking’. An idea that the masses will lose untold amounts of wealth in the next financial crash, due to a deliberate plan by mysterious figures.

Get my latest content and thoughts straight to your inbox.

A fresh dose of financial motivation to power your journey.

Great article!

I always see people talk about rent money is ‘dead money’ but right now for many of us it is as you’ve said ‘freedom money’

Also loved the sneak peak if the podcast. You are both look so happy! I can’t wait to listen ????

Thanks Miss B! Yeah we’ve been having fun recording, but still very new to it all 🙂

Cheers for another great article Dave

Its rare to see someone point out the positive and negatives as you do. As you know usually people are firmly in the ‘Red’ or ‘Blue’ corner on this issue.

Once expense you forgot to mention for owning a house however is the seemingly endless amount of money (and time) spent at Bunnings!

Spot on!!!

Haha yes that’s a good point, home ownership lends itself towards all sorts of furnishing/decorating/improving that you wouldn’t do with a rental. Another under-counted cost no doubt! 😉

Time spent gardening is another one… if you have a nice house like I do, you feel compelled to keep it that way. I lose one day a month at least just trimming the hedges and all the other miscellaneous stuff I never worried about while I was renting.

I find that time spent gardening is time well spent. Doesn’t matter if it’s your own place or a rental. There’s something rewarding about gardening. It’s not very Rock ‘n Roll, but I like it… ????

That’s true. But on the other hand, that could be seen as a benefit as something enjoyable and healthy to do with spare time. Whereas with a rental you’re forced to maintain someone else’s yard, so it doesn’t feel the same lol.

Interesting read. I am in red camp.

My understanding from your other reads is rent is generally cheaper than buying.

Just wondering, purely from financial point of view which option is better over period of time say for 5,10,20 & 30years. Does it change over period of time.

Thanks

Purely financial, renting tends to win out in many cases, but only if you’re investing the difference. The RBA did a study on this a few years back from memory. Yes it would definitely change depending on rental yields, mortgage rates and other costs, so there’s no hard law that one is better than the other. And of course it varies wildly by location and property type too.

A happy renter here. Renting a lovely home with pool and backing onto a golf course, at less than half the cost of a mortgage to buy an equivalent property. I’m very thankful to my landlord for subsidising my housing costs!

Haha good stuff John – sounds great!

Thanks Dave for another great well balanced article. I look forward to them each week and I can’t wait for the podcast.

Thanks for reading Shane 🙂

Thanks for the post, at 30 and single i’m most definitely in the red camp. As a dual citizen i’d like to spend a portion of the year abroad and then a portion back home, so the flexibility is paramount but I’m open to changing perspectives as I get older.

Also, sorry if I missed it in the article..

When you plan to eventually purchase a house, would you be selling a large amount of your share portfolio to purchase without a mortgage or would you use a deposit from the sale of shares for a mortgage and just use a portion of the income from the share portfolio to pay down the repayments?

I was just curious… as I imagine an outright purchase would significantly diminish the passive income generated from the portfolio.

Interesting Scott, thanks for sharing.

Um, it really depends. If we sell multiple properties at once and find ourselves with enough cash from property sales to buy outright, or serviceability to get a loan, then we won’t touch our shares. But if it doesn’t work out like that, then we’ll have to sell some shares to do so. But I’ll probably look at ideally pulling some of that equity back out to put into shares.

As you say, doing that would decrease passive income, but having no mortgage/rent also reduces our annual costs quite a bit, so kind of evens out anyway if it comes to that. Hope that makes sense.

Yeah, perfect sense.

Thanks.

A good clear comparison of the two Dave. Thanks.

It’s a question I’m pondering myself for what to do next as I properly start down the road of building investments (I finally cleared all of my debts last week – Yay!).

I’m 45 (next week) and with 2 small children I’m coming down on the Blue side at the moment – so that I can give the kids a stable family home that we can do whatever we want to for the next 10 or 15 years.

It’s nice to see the two options discussed impartially as you’ve done.

Very much looking forward to your joint podcast with Pat.

Cheers!

Congrats on being debt free!

Thanks for your support, I hope you like the pod. Dunno about Pat, but I’m a bit nervous now – don’t want to disappoint anyone lol.

Cheers Dave!

Being debt free is a good feeling.

I also have about $30k in cash, peer-to-peer lending, index funds, and a couple of other small and varied stocks/investments. I had no real strategy previously.

I am currently drawing it all in together as best I can, though it will take a few months to a few years depending on the time it takes to draw down the peer-to-peer investing. And then I’ll either go all in with it to buy a house and pay that off as fast as I can. Or I’ll commit to renting and invest it all for the long term in one or two ETF index funds.

Either way, it’s nice to feel that I am now free to make that choice and commit to it with few other ties.

With your podcast – remember that Nervous = Excited!

Just be yourself. It’s worked so far 🙂

Andrew

Nice Post.

I saved up 20% for a deposit about 3 years ago and started putting the rest into shares while figured out where wanted to buy. After so many years I have realised that I don’t have much desire to buy a house. I feel I might make the purchase later on in life but not until I actually feel like it. In the mean time I will continue investing instead.

If you were to buy later in life (10-20years) would you just take it out of shares that have compounded?

Great to see this thinking here – realising that buying doesn’t seem like the right fit for you now. So many people just do it because it’s what is assumed as the best choice in all cases.

Well, there’s two options. Sell down shares later to pay for a house with cash. Or get a mortgage and keep the shares. Both are valid approaches that have their own pros and cons. Selling the shares to buy with cash is the more conservative approach, so it largely depends on the individual. I’m not 100% sure what we’d do to be honest!

We just bought our first home, after renting for 12 years. From share houses, to apartments, units, townhouses. Will see how it goes. Thanks for all the great info as always. Put the podcast release date on the calendar!

Hi Lachlan,

I’m curious: What was your motivation for moving from renting to owning?

And did you wait to buy in cash, or to have a minimum deposit before buying, etc?

Cheers,

Andrew

Thanks for the support and congrats on the house 🙂

Hi Dave

Great article. Having already fired without house, I’m very comfortable renting for the foreseeable future as described in your article, I have the freedom to move where I like and change location as my needs change. Once in my 60’s things may change, the lifestyle will slow down, home security will likely become more important, so dumping part of the portfolio , purchasing a house and getting a part pension maybe a strategy worth considering later down the track.

cheers,

Daniel

Very nice Daniel. Always good to see a happy long term renter to balance out the viewpoints!

Yep, that sounds like a totally sensible plan to me. Some people fear ‘renting forever’ but as you say, buying is always an option later.

If the global pandemic has taught me one thing… security of my lifestyle is paramount. No matter what the markets are doing or what is happening in the world, you can’t put a price on coming home to something that is yours and which no one can take away from you.

And yep…. podcast looks great!

That’s a very fair point to make in what are pretty uncertain times. There’s a psychological benefit to owning that can’t really be measured 🙂

Enjoyed reading your good balanced article. I am a firm believer in home ownership. Hate periodic housing inspections, hate needing to ask for permission to fix things, hate being asked to move if landlord needs house back. Hate having to move house, removalists, resettle. As one gets older, certainty is priceless. Especially with the recent stock market drop, my own house has done a lot better over the my stocks portfolio. The house has almost doubled in value over the past six years whereas my LICs and ETFs have regressed back to where they were a few years ago.

Haha I can tell you’re passionate about this topic Ken – thanks for sharing! The inspections do get a bit annoying, that’s for sure 😉

At 57 I have done it all, owned apartments, townhouses and houses but sold up about 8 years ago to rent and have been very happy. My portfolio has increased tremendously since freeing up the equity locked in bricks and mortar and I also get to spend half the year travelling and half the year in Australia. I house sit while in Oz and last year saved about $20k on living expenses. I’m now viewing apartments with a view to buy one in Perth CBD and rent out through Airbnb once covid has passed. Just before ‘retiring’ (I was FI at 41 but love my job selling swimming pools and thankfully it is seasonal) I will buy a house again and get a part pension, but for now happy renting and house sitting.

Wow this is interesting! Not very common to see someone owning for ages and then later in life switching to renting (at least for a while) – great to have this example.

House-sitting looks like a fantastic option, which website/platform do you use for that? I don’t know much about it but find it intriguing.

Sounds like you’re super flexible, some people are either one or the other and then never budge from that!

Hi Dave, there are a few housesitting websites: aussiehousesitters.com.au and mindahome.com.au are the two main ones I use, also go direct with an agency in Perth. Things obviously slowed down during covid, but I moved into the apartment I bought to use as an Airbnb on Mounts Bay Rd and rented it out each time I get a housesit position.

This is something I’ve thought a lot about lately. I’m 28 and a semi retired solo investor with 6 properties generating about 95k in rental income.

I’ve been renting for the last 3 with my partner and it suits us just fine for the moment but I think ideally if we have kids down the track and for long term security I would like to own a place of our own even if it was rented out for some time before we moved in. The issue is that “entry level” houses in our current desired area are 1.2-1.3m which is a huge sum of money and a huge amount of debt to get in when we can rent a house in the area for $550-$650 a week.

I personally feel if I was going to spend a million bucks plus I would rather spread it across multiple properties and shares to keep increasing my passive income so I can keep travelling and stay self/semi employed.

Thought provoking article and points Dave- a lot to consider, I change my opinion on this almost weekly though, ha.

Damn that’s incredible, nice work!

That’s the thing – fancier locations tend to be extortionate to buy or incredibly cheap to rent on a yield basis. I had a good example of that in this article, where a young couple bought one of our investment properties and with mortgage and other costs it would be costing them literally double what they’d have to pay in rent!

It’s not an easy choice to make, so flip-flopping is understandable lol.

Nice article, Dave, and I look forward to the podcast with Pat – that hammock looks pretty comfy, by the way!

Cheers! Haha yes, it sure is. If you’re gonna retire, you gotta live up to the stereotype 😉

I have come across some quite academic articles that crunch the numbers and they come down on the side of renting for sheer cash flow and net worth over time scales of 40 years. However, the improvement in finances with renting assumes discipline and continued investing in the share market. There are obvious emotional factors when it comes to renting vs owning, thus making comparisons difficult.

Spot on Jeff! In theory renting wins. In practice, people suck at saving, so you could say owning wins. Without the forced saving of a mortgage, how much wealth/security would the average Aussie create? I wonder, would we even have a middle class?

I think this is one of those situations where the maths doesn’t matter as much as your own priorities.

We own our home, and it basically came down to stability and security. Having lived in a bunch of shoebox sized apartments in London and Hong Kong we wanted to know that we had a place that we could call our own and was designed the way we wanted it.

The fact that we’ve got two young kids was a big factor, we wanted to make sure that they had the stability of living in the same place for their childhood.

Other people have different priorities so it makes more sense for them to rent, and if that’s what works for them then great!

Yep, totally agree mate – it’s largely a lifestyle/mindset thing more than numbers for most people.

Haha I can understand the desire for security, besides you guys can comfortably afford it. And some space for the kids can’t hurt compared to the shoeboxes lol 😉

Hi Dave, cheers as always for the fantastic content.

We have a few IPs that we bought before we stumbled aross fire and passive investing. With current situation in the world i am becoming worried about the IPs. Generally speaking, is now a bad time for people to exit IPs and should they just ride out the coming loses in value or get out if/while they can?

Thanks again.

Hey Joel. Man, really hard to say. I’m not sure I’d say “coming losses in value” are locked in. Some are saying housing will recover quite well due to insanely cheap mortgage rates (cheap credit fuels property), the coming economic re-opening, China growing again, and massive stimulus spending.

So I think that for now, things are still soft, so we wouldn’t look to sell personally. I’m not expecting any of the doomsday theories to play out (huge collapses in prices). But if it’s causing you lots of stress and you think it’s going to get a whole lot worse, then that’s a different story and you have to do what makes sense to you.

It sounds like you may use debt to finance a potential PPOR, do you foresee issues securing finance with your working situation?

Hey Naj. It’s a long way off, but we’d consider borrowing to buy. This is after we’ve sold our other properties of course. There’s zero chance we could get a mortgage right now, and even if we had zero debt, it would be difficult due to our income being dividends, a part time job, and the small income from this blog. If there’s an issue financing, then we’ll probably sell down shares/use cash to buy.

OMG that FI/RE and Chill Podcast intro ????????????

I loved the subtle pause, looks up at the camera and smile ????

I can’t wait!

Haha! Thanks for your support brother 😉

I’m firmly on the side of owning – it worked out brilliantly for me.

I bought a house, paid it off over 17 years, then sold it 3 years later and relocated 16kms away to a cheaper (and better) place. That freed up an enormous amount of equity that, even with the current downturn, will save me having to work a decade sooner than I otherwise would have.

My children had a secure upbringing in the old place, while in the new place I’m making sure that it’ll be ‘retirement ready’ for Old Lady Frogdancer Jones and the dogs. My living costs when retired will be minimal, which is an important thing for me. I too like my veggie patches and fruit trees. 🙂

I’m in my 8th week of lockdown and loving it here. For me, the ‘crazy’ decision of buying a house in an area I’ve never lived in was the right one.

Security for the win!

Thanks for sharing. That turned into a great thing for you in lots of ways! Love the sound of the fruit + veg by the way 😀

I’m firmly in the owning a house camp. As an older single woman (fastest growing category to be homeless) with no one to depend on, security trumps freedom. No one can kick me out. When I paid off the loan and the unit was truly mine, it was liberating. I am free to do whatever I like with my money now that I know I will always have a roof over my head. Plus the unit is phase 3 of my retirement plan – to be activated when I need to move into aged care in my dotage

Same for me, Latestarterfire – when you’ve got no one to look after you in your old age, security is essential. Those aged care facilities will bleed you dry! But they are easier to get into if you can pay. When my sister and I had to find somewhere for our dad (who had zero assets and almost zero money), we ended up going through a broker and even with that professional help, we only managed to get a spot literally as we were moving him out of the unit he was staying in (he’d been asked to leave because his dementia-related behaviour was freaking out the other unit occupants). While all aged care places are required to provide a certain percentage of beds for government funded residents, they are often loath to say they have a place available if there’s a paying customer also applying.

Hello Fire for one, interested in your comment about a broker finding a place for your father. I’m in the same situation looking for a place for my parents, who still rent, have no assets and no savings. They live in regional NSW and I’m in Sydney so a broker would be helpful.

My take on the rent/buy scenario, after seeing my elderly parents forced to move house every couple of years, I think the security and stability of owning your own place outweighs the costs of home ownership.

Yes that’s a huge win, and great to hear! Never heard anyone say they regret living in their own paid-off house. Do you think the psychological benefits of ownership and security are even more important/beneficial for women? Obviously I have no clue, but it sounds like that may be the case.

Hi Dave, I feel it’s true that for most women security of home ownership is very important. My husband and I have separate finances but we own our home jointly. When the mortgage was paid off a couple of years ago, it was such a weight lifted off my shoulders. Even though I still have debt on my investment property and business I feel completely different. Even with the downturn in my turnover due to coronavirus, I’m relaxed and just know if all fails, there is still a roof over my head which no one can take away.

Great article by the way, looking forward to your podcast.

Interesting – thanks for sharing that Leanne, and well done on your overall situation too!

So much of this boils down to preference of lifestyle and risk. I’ve always been in the “own my own home” camp but understand the value that those who prefer to rent are taking advantage of.

My husband and I retired early but then sold our home and took of to explore the world with our backpacks. After a few years we decided to “settle down” just a little and purchased a converted bus to travel in. So we now own our own “home” although for all financial arguments it is still a vehicle and a depreciating asset. Still it gives us the freedom to keep exploring.

Eventually we will most likely buy an actual home attached to the ground for many of the reasons you listed under why to own.

Wow that’s pretty cool, thanks for sharing your thoughts Bonnie! I would expect there’s much less cash tied up in your current ‘home’ versus a regular one, so it’s a lot more efficient than placing it in the ‘vehicle’ category.

Thanks Dave this is really an interesting topic, having moved to Perth late 2017 from London we bought our house in May 2018 (No going back now) with the thought of equity in mind. Typically owning a house in London we noticed that its was primed for equity, however looking into property in Perth don’t tend to see that upward trajectory, don’t get me wrong totally understand there are other factors that come into play, but one of the factors for us owning was 10, 15, 20+ years down the road we’d know our house is worth much more than what we initially paid for it, looking into some of the numbers (at least for the area we are in) not seeing the increases that we (naively) hoped for. Plus renting is not an option for the Mrs 🙂

Thanks for reading. What matters most I think is that it suits people’s lifestyle/psychological preferences, rather than making money from it. Most cities here, including Perth will likely have higher house prices in the future, but it definitely doesn’t happen year after year. Besides, money can and should be channelled into other investments too.

Home ownership for security is my choice. Have friends in their mid 50s who had a cheap stable rental for about 20 years, so thought they were cruising. Then the owner died and the children sold the house within 8 weeks. They had to pay $150 more per week to find a decent rental and move about 5 suburbs away i.e. to far for the “drop in” friends anymore. Now in their 3rd rental in 4 years and the banks won’t lend them money as they are “too old”. Can’t imagine being at the mercy of a landlord when in my 70s.

Jacael’s story of her friends is a perfect example of the need for long-term renters to invest in income-producing shares. A quick whirl on the Moneysmart Compound Interest calculator tells me that a regular deposit of $150 per week (the excess rent the friends are now paying) for 20 years (their period of having a cheap stable rental) and returning sharemarket-like returns of 8.0%, compounded annually, results in almost $360,000…. If they keep going for another 10 years, they’ll be hitting $1M… The moral is; Yes, you can rent ‘forever’ but you MUST invest in income-producing shares during this time in order to have some form of financial security. Oh, and money sitting in a bank account won’t cut it…Invest in the sharemarket!!

Thanks for sharing. That’s quite a sad story. I think this highlights the big advantage of owning – forced saving. Most people are just going to spend whatever is in their account, regardless of the amount. A home loan at least forces you to pay a little bit of principal over time and build up equity. As you’ve pointed out, without that, many without good financial habits and some discipline will end up with very little.

Edit: What Jeff said 🙂

This is because they didn’t have enough any buffer and not because they were renting. The same could happen with a PPOR if expenses changed they could be forced to sell and move to a cheaper location. Sure they will likely be forced to move a few times when renting but with a buffer they should be able to live in a similar property in a similar location

Hi Dave, I am a 56 year old female and don’t own a home. I am renting at the moment. I am so terrified of being homeless later in life. I don’t know if I should save a deposit as quickly as I can and try to buy or if I have left it too late and that horse has bolted. If I don’t buy do I just put everything I can into my super. I have no idea about investing but know my time to secure a reasonable retirement is running out. Any suggestions would be greatly appreciated.

Hey Colleen. I would probably save as much as possible and try to buy a very modest place to live. It may be difficult to get a mortgage though since it’s highly unlikely you continue working full time for another 20-30 years. In this case, I’d try to convince them I will use super to help pay it off if possible. If that doesn’t work out, I’d simply keep my spending modest and save as much as possible into super which can supplement the pension. Hope that’s useful, and all the best.

Thanks Dave. I am managing to save around $2500 – $3000 per month so hopefully I will be able to buy something small and then start putting as much into super as I can. Your advice is very much appreciated.

Hi Colleen. It was Socrates who said; ‘wise is the man (or woman!) who knows nothing’. You admit to knowing nothing about investing; so start learning. Make your first ‘investment’ in your self-education; it’s never too late to learn. There are lots of books on investing and wealth accumulation. There are books by Australian authors such as Scott Pape, Michael Kemp, Pete Wargent, and Canna Campbell that you should definitely look up. For a more US-centric view; check out authors such as; JL Collins, John C Bogle, and Vicki Robin. The Richest Man in Babylon by George S Clason is a personal favourite of mine. You can also get financial advice from your Super Fund. Often their general advice is free of charge to members but then you can pay a fee-for-service for more personalised advice. Good luck and keep learning!

Not sure if anyone has mentioned this or not in the comments, but there is also the very flexible, tax-friendly option of salary sacrifice into super, which I started doing a little while back.

As a recently separated dad with an 8-year old, and no property of my own, I found this article helpful and a little more encouraging. Thank you.

Thanks for the comment Tristan, glad you enjoyed the article!

I’m 63 and retired. I’m selling my one bedroom unit that I’ve only owned for 3 years (no mortgage) as I sorely miss having a garden and now there is now going to be a development next door which will block my views and sunlight. I’m very wary of buying again as it’s a massive financial outlay and I can’t see the benefit in buying another tiny place when I can rent something with a small garden and second bedroom further out of the city. I have previously owned a house which had big maintenance issues and was glad to sell up and move interstate. I was very happy renting in the interim. My current home (the one bedroom unit) was a “sensible” buy but very restrictive. I put the difference in price between selling and buying into my Super as a one off contribution just within the three year cap. I prefer the freedom of renting and figure I can pay many years of rent for the price of a place. I can also rent a place that I couldn’t afford to buy. I’m very disciplined with money and my Super balance is very healthy thanks to voluntary contributions whenever I could and the investment strategy devised by the adviser at my super fund. I’m pretty sure I’ll rent long term and live off my super pension whilst drawing down a modest amount (usually works out around $500 a month) to help cover my rent and other expenses. I’m not at all cluey about investing but find Scott Pape’s Barefoot Investor invaluable for good commonsense advice. Given that term deposits are paying negligible interest, where can I park my house money? I’m of two minds if I’ll buy again down the track but you never know. I would love to do some more travelling before I get too old. Nothing fancy. I’m a solo traveller who prefers local transport and cheap accommodation. However I read so many horror stories of single older women ending up in penury. I would appreciate your advice.

Thanks for the article. It made sense to me from the point of looking at just my personal finances and retirement. What do you think if we add to the equation the goal of leaving equity to kids? I want kids to own my property when I die so that they have less financial pressure

Thanks

I’m assuming you mean leaving your kids a property, which is a fine approach. However, there’s nothing magical about leaving them a property specifically. You can leave them an equal amount of ‘equity’ in shares, which they can sell and buy the property they want. Both work.

I think the most important thing is for parents to teach kids about money and investing. Then they won’t actually need an inheritance because they’ll be building their own wealth from a young age, which is more valuable than handing them money.