Well, it’s been a long time between drinks as far as portfolio updates go. In fact, the last one was back in September 2017!

Not for any special reason, other than it slipped my mind and there was plenty of other stuff to write about. But in the interest of transparency and also entertainment, I’ll aim to post a portfolio update at least twice a year.

This way you can see where our cash is going, and maybe even cheer from the sidelines at (hopefully) the progress.

As I’ve said before, the idea isn’t to copy this yourself, because what feels right for me, may not be right for you. It’s about sharing and following along. So let’s get started…

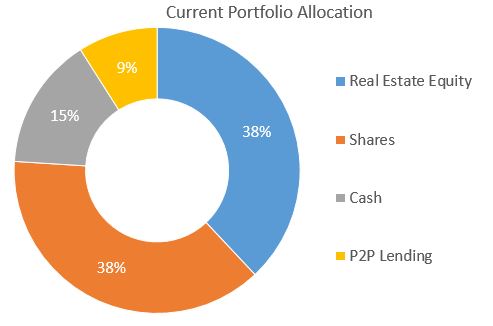

Here’s a breakdown of where our money is invested right now. These figures are excluding Super and are percentages rather than numbers, for privacy reasons.

Regular readers will know we hit Financial Independence with our savings mostly in property, along with some shares. While the shares provide income, the property doesn’t. In fact, they cost us a bit in negative cashflow.

So to create the income stream we need to live on, we’re slowly selling these off and investing the proceeds in cash producing investments. A couple have been sold so far and here we are!

The end goal is a portfolio that generates a solid level of cashflow which covers our household spending. That portfolio will be mostly shares, with some smaller investments in peer-to-peer lending and real estate investment trusts (REITs) – which are still technically shares.

A fair question. And we thought about that. But we decided against it for the following reasons…

— The tax on our capital gains would be much higher if we sold multiple properties in the same year.

— We wanted the option to decide when to sell, to optimise the outcome a bit and try to avoid selling during property market weakness.

— We were (and still are) learning more about shares and designing our portfolio, so we didn’t feel comfortable having to invest such a large sum all at once. Essentially, it’s less stressful this way because of our initial lower experience with the asset class.

— We wanted to dollar cost average into shares over time as we transition, in case the market fell and we missed the opportunity to buy more at lower prices.

While all this is hardly ideal and a bit messy, our monthly cashflow works like this…

We have a decent sized lump in the bank which is used to cover personal and property expenses. Investment income and any part-time work income rolls into the bank and can be used for this also. And from the balance, we invest each month (usually $2-3k) into shares.

The cash balance declines over time, until every few years we need to sell another property and continue the process.

After 10 years (say), we’ll then have zero properties and a decent sized share portfolio which produces income higher than our spending.

Got a headache yet?

There’s a reason I say just to focus solely on building dividend income quickly from shares. Rather than trying to build equity, either through growth shares or leveraged property and then switching strategy later to focus on cashflow.

Everyone’s different, but that’s what I’d do starting from scratch today. With a strong savings rate, you don’t need high growth or leverage!

Well, by my estimates, in the last few years our Perth properties have actually gone down by almost $200k. So on that front, not great!

But luckily, we left work with more equity than we needed, due to my partner’s home equity when we met. There’s less cushion than before, but things are still on track.

If there’s a positive, we have no vacant properties, most loans are now fixed at decent rates and setup as Principal & Interest. That wasn’t our initial plan, but the rates on variable interest only loans were becoming extortionate!

While it means cash is going towards paying down debt instead of shares, at least there’s hopefully some equity building and we’ll get that cash back eventually when we sell.

Our peer-to-peer lending with Ratesetter keeps delivering a very reliable source of relatively high yield monthly income with no hiccups thus far. This suits us nicely being in a very low tax situation. Hopefully the loans, defaults and provision fund continue to be well managed into the future.

As for shares, the portfolio value bounces around as usual. Well, I assume it does (we have two accounts so I rarely bother adding them up to find the total ‘value’).

Importantly, we’ve had another year of dividend increases across most of our holdings. Of course, regular top ups mean the income we’re paid continues to grow regardless.

In addition, we recently received a decent special dividend from BKI which was nice, with both BKI and Milton suggesting there may be another special dividend later in the year.

We’ve done enough shuffling (with our portfolio) in the last 12 months to make Pat the Shuffler look like a couch potato!

Well, maybe not that much, but there have been some changes.

One idea that kept slamming me in the face until I could no longer ignore it, was that of simplicity. The benefits of simplicity are many and this deserves its own post!

For some reason, I have this weird tendency to over-complicate things. Not because I think it’s better, but maybe I just get so enthusiastic with what I’m doing that I inadvertently create more work for myself.

Anyway, that’s what I did with our share portfolio. But I’ve since realised that while I love dividend focused investing, I don’t want to spend tons of time on it, especially if there’s no value added for the extra time spent.

Instead, I’ve decided I’d rather spend that time on other fun stuff – like helping in the garden, reading books, playing with the dog or writing blog posts for you!

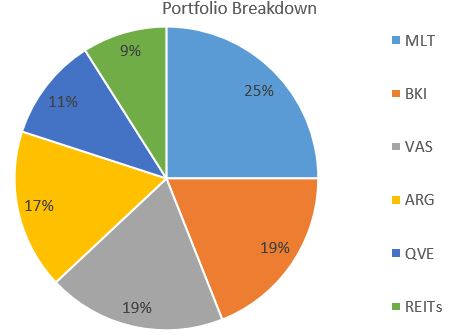

After building a big messy portfolio of individual dividend stocks and LICs, I’ve since sold and re-bought the individual stocks into our super fund accounts, as part of an ongoing stock-picking experiment (mixed results so far, in case you were wondering).

As for the LICs, we’ve reduced these down to 3 main LICs (Argo, Milton and BKI), and one smaller holding which focuses on mid-sized and small companies (QVE for those playing at home).

So we’ve been mostly topping up these core holdings over the last 12 months. And I have to say, the smaller portfolio is heavenly. I joked recently that I’m enjoying simplicity so much that soon there’ll be no holdings left!

We also added the Vanguard Australian shares (VAS) index fund to our portfolio late last year, as mentioned a few times on this blog.

My feelings towards the index have changed in the last couple of years, for a few reasons which I’ll get to in another post (very soon I promise!).

One big reason I decided to add VAS to our portfolio is to add greater opportunity to buy shares when the market is down.

Wait, can’t you do this with LICs too? Well, yes and no.

You may remember the market falling towards the end of last year. As I was licking my lips and looking to put some money to work, I noticed that AFIC and some other funds hadn’t moved much at all, while the index was down around 10%.

Certainly not ideal when you’re looking to buy. So by buying the index instead, I was able to take full advantage of the market drop, buying more shares at lower prices. Yippee!

This is normal by the way, it happens quite often. But it also occurs when the market goes back up. Like recently, the market has rebounded a good 10% and many LICs again haven’t moved quite as much, so they’re currently trading at discounts to NTA.

LIC share prices are generally less volatile and slow moving, causing them to regularly trade at premiums and discounts.

Firstly, I don’t like the following holdings any less than before. But for the sake of simplicity we had to choose something!

Here’s how it went down.

AFIC. Late last year when the market was down, AFIC was trading at around a 7% premium. At the time, our cash balance had taken a hit due to some property expenses, and since I wanted more simplicity, I decided to sell AFIC and use the cash to top up some other holdings that were more attractively priced.

AUI. Australian United Investment Company has a fantastic dividend history, but one of its negatives is low liquidity. This means when putting in a buy order you could be waiting quite a long while for it to fill, a day or more. Not a big deal, but still a little annoying.

Soul Pattinson. Not a traditional LIC. More like an investment conglomerate – owning large stakes in a handful of businesses, along with a small property and share portfolio. An incredible company with a great history. But after purchasing around 18 months ago, it returned around 100% on my investment (for valid reasons, but still unusual for a reliable investment company), so the desire for simplicity and being able to sell tax-free were the main reasons for its removal.

Just to be clear, I could also argue to keep these and get rid of our other holdings, so don’t read too much into this. After all, these three companies have all had stable and increasing dividends for the last 19+ years!

After mulling this over for a while, I’ve decided to share my portfolio breakdown as well.

That way you can follow along as I build this income focused portfolio and continue to evolve my thinking on the topic. At this rate of sharing, soon you’ll know what colour undies I wear too!

There it is. What a number of you have been wondering for ages! Pretty basic and unscientific, right?

That’s partly the idea. 80% of the holdings are relatively boring, diversified and low cost. And the portfolio has a clear focus on reliable income streams.

The portfolio will very likely change over time, as most people’s do. But I’m happy with it at the moment.

Depending on who you are, you’ll either think this portfolio is borderline loopy or perfectly reasonable. That’s okay. We each have to invest according to what feels right for us and our own situation.

Our own goal is dependable and steadily growing dividends. Speaking of which…

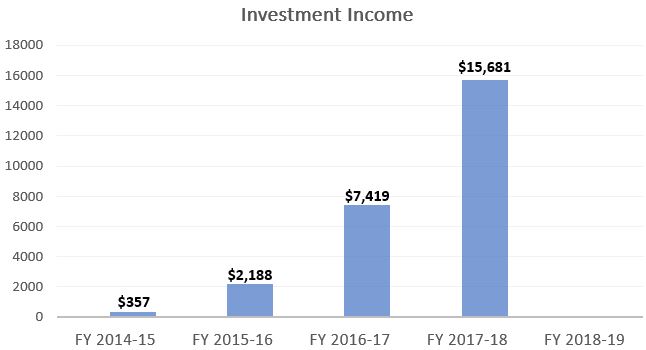

As you probably know, I enjoy tracking our annual dividend income. It’s the key measure of progress in my eyes.

Here’s how our portfolio income has grown over the last few years since we started investing in shares.

This is including franking credits. As I’ve written about before, the real progress is made through regular investing, not high investment returns.

I’m looking forward to plugging in this year’s total, which so far looks to be a decent bit higher than last year.

After that, income growth will be slower because we did invest some small lump sums (from our cash balance) during the last two years which probably won’t be repeated.

It’s very satisfying to keep score this way. Honestly, I can’t even remember what the market did during this time. Up, down and sideways, most likely.

For dividend investors, I think it’s also useful to regularly compare your annual dividend income, with your household spending.

What you’re looking for here, is your coverage ratio.

Which means, how much of your spending is covered by your investment income?

Let’s say you spend $40,000 per year, and your annual dividends are $2,000. Your coverage ratio is 5%. So at this moment, you’re 5% of the way to being financially independent.

But as you continue purchasing shares regularly, reinvesting your dividends, and your holdings increase their dividends, your income and therefore your ‘coverage ratio’ will grow quite quickly.

Just a few years down the track, your annual dividend income is likely closer to $10,000. Now your coverage ratio is 25%.

Use this as your yardstick to measure progress. Forget fluctuating market prices!

As you can see, last financial year, our investment income was around $15,000. Our spending in 2018 was around $45,000. So a third (33%) of our spending was covered by investments. This year, it’ll be well over 40%. And as we proceed to slowly move our savings from property to shares, our coverage ratio will keep increasing.

At this point it’s pretty much steady as she goes.

Our plan is to continue to walk the talk. That is, maintain our moderate spending, and keep adding to our portfolio regularly, regardless of what the market does.

We’ve also started the process to sell the next property, so we’ll see how that goes.

Hopefully you got something out of this post, or at the very least, it satisfied some curiosity. While it might not be the cleanest of FI situations, we’re making it work!

How’s your portfolio going? Let me know in the comments!

Why deliberate spending is my favourite money management style. What it really means and how you can use it as your situation and priorities change over time.

My thoughts on ‘The Great Taking’. An idea that the masses will lose untold amounts of wealth in the next financial crash, due to a deliberate plan by mysterious figures.

Get my latest content and thoughts straight to your inbox.

A fresh dose of financial motivation to power your journey.

Aargh NO! You have simplified your portfolio faster than I could do mine! Another great post, thank you for sharing. Fantastic progress by the way. I’m especially proud of the pie charts and graph! I’m a little surprised you have cut out AUI (oh well, no one is perfect). ;o)

Haha! Thanks for your support mate, thought you might like the charts 🙂

I like the idea of some amount of exposure to small-caps. However, often to do this via an LIC you have to pay a reasonably high MER. I took a look at QVE and seems on the high side. Have you considered something like VSO?

Hi Luke, it’s true the fee is higher than an indexed option but I believe in the manager (IML) and their approach fits our own. The fee is actually lower than many other actively managers in the mid/small area. They tend to dislike the volatility of resources generally and select a basket of value stocks with more reliable earnings and dividend streams. VSO tends to have quite a bit of resources companies, some of which are smaller and more speculative in nature. I understand why people might prefer the index, but in the small end it’s just not for me. The risk is obviously that QVE will underperform over the long term, which is something I accept.

Hi, I’m thinking of getting started in the share market and have been following your blog for some time. I’ve found it informative and helpful.

When you talk about LICs you mention that they charge a MER. This may seem a silly question but is the MER deducted from the dividend, or do investors have to pay for this separately?

That’s great, thanks for reading. There’s no silly questions around here Don 🙂

The fees/MER comes out of the earnings of the company before they pay you a dividend, so it’s all done behind the scenes. Same goes for an index fund – all automatically deducted from the fund.

I think your portfolio is very sensible, after more than 20 years investing in shares with a dividend focus I’ve come to a similar conclusion.

I’ve slowly trimmed my portfolio down to AFI,BKI,MLT,VAS and a local mutual fund that I invested in 20 years ago – mainly international in which I intend to keep while the original Owner/Manager is running the fund.

It’s great to get some perspective from someone who’s been investing for decades.

I only just started investing earlier this year and i’m holding a similar portfolio: AFI, BKI, MLT and VGS. I might still add VAS later on but it’s re-assuring that i’m probably on the right track. There’s a temptation to add more, especially as I get more comfortable with investing.. but I also see the strong value in keeping it simple.

I think your mix is good. I have the same as you minus VAS which I shall buy sooner than later and a few other individual stocks which I am happy with.

Thanks for the feedback Brett and for sharing your own portfolio 🙂

Brett, any reason you prefer VAS over A200? Cheers

Thank you for this post – it satisfies all my graphing and curiosity needs in one place! 🙂 I still think it would be better with numbers, but understand your need to retain some mystery.

That must be a tricky exercise to work though, psychologically, a multi-year trading out of property into shares, in large lumps at least on the sell side. However, it’s an amazing position to be in at your age. Can I ask – are you essentially estimating a 4-5% level of income from the final portfolio when it’s all transferred into LICs/ETFs? How much of a margin over what you need do you think you’ll have when you’re all done with the portfolio switch?

Agree on the coverage ratio – it’s one of the most satisfying metrics to track – I think that’s why the book Your Money or Your Life was so inspiring to so many . I sometimes think of it as almost a discount at the cash register arising from past dividends.

I still haven’t read that book, it’s been on the list for a while, maybe I should bump it up!

Yes that’s correct, I’m roughly expecting around 4-5% income from the final portfolio (not including franking). Very hard to estimate how much margin of safety there will be at the end of the transition, could be quite a bit, could even be negative. Impossible to know right now since it depends what happens to property prices over the next 5-10 years, as well as franking credits and dividend levels! How’s your crystal ball? 😉

One other good thing about Your Money or Your Life (of many, many good things) is the exercise where you work out your net worth then divide that by the number of hours you’ve worked in your life. When you realise that your life so far has been worth 45c an hour or something, you realise that to get to a million dollars either you need to live to be 2 million, or something drastic has to change about the way you spend your income.

Probably not ground breaking for an experienced hand like you SMA, but earth shattering for newbies like I was when I picked it up. And to this day I still think about “how much life energy does X cost?” and refuse purchases when I realise it costs me 3 hours at the office or whatever to buy it.

Great example, and scary eye-opening stuff – I’m sure even savers would be disappointed at how much of their time went into saving X number of dollars! Sounds like a fantastic motivator, maybe after I’ve read the book I’ll paint some examples of that in action. Thanks Chris.

You sold SOL! I nearly fell over reading that today after our emails about it last September about whether or not to ditch it considering the highs it had reached and continues to hold. You were quite keen to stay with it because of the strong track record and growing dividend income stream, but I do understand the attraction to simplifying a portfolio. Mine is too complicated as well. I notice that you said your sale will not attract any tax — presumably because your marginal tax rate is below 30% — and that likely played a key factor for the sale. That would not be the case for me because I’m still working full time.

One other question, and feel free to say no. I was interested in what sort of cost base you have locked in for something like MLT. I ask because I know you add cash most months regardless of price. I’d be interested to know what sort of cost base has resulted for you. For example, I’m currently at $4.32. I wanted to throw much more at it in late December when it dipped below that but I failed to have my SelfWealth account loaded and missed the chance (BTW, do you keep SelfWealth loaded with something just in case? I do now).

Great post! Scott

SOL is a major holding of MLT and effectively run by the same mob. Not quite as convinced about SOLs latest thrust into fund Mgrs. But to date a loooonnnggg history of outperformance and magnificent dividend history.

One Millner holding is enough for me and like Dave I choose MLT (minus BKI) with its greater diversification and the desire to keep it simple.

Nodrog

Nodrog — thanks for the reminder re MLT’s holding of SOL. Currently it’s at 8.4%. I unfortunately got stung by RFG. I think if it totally collapses — which looks more and more likely — I’ll sell SOL and take a zero CGT hit in the process. Like Dave, I’m up about 100% on SOL.

Haha I know! Wasn’t an easy choice at all. I probably wouldn’t have sold if I had to pay 30% tax to be honest. From memory I put most of the cash into Milton, and as Nodrog points out, Milton has a big holding in Soul Patts. Also still have Soul Patts in our super account.

I’m not too sure of cost base as I don’t really look at it (we have 2 accounts which would make it tricky to figure out as well), and it’s kind of irrelevant I think. All we should be deciding is whether something is attractively priced today compared to the future. Anchoring on past prices probably isn’t a great idea.

Note – I just looked and average price is $4.50ish. That, and other cost bases, don’t tell me anything except what tax might be owing if sold. Say I bought 20 years ago and price was $1, does that mean I shouldn’t top up because it’ll increase my cost base? I think that’s madness 🙂

Juyst curious on your thoughts why SOL came down so quick after hitting around $30.00 as a high? PPL buying as it went up must have got burnt badly. Wonder if it will reach those highs again. That would have been the time to sell…..

Hmm I dunno really. It looks like I timed it well, completely by accident! Possibly because its portfolio (NTA) was not worth $30, so it was a little overpriced at that point. Also I think some of SOL holding fell in value (New Hope comes to mind), which would have contributed too. Long term I think SOL should do fine, based on savvy management and extremely long term track record (40 years), so in 20 years could price may look like a bargain. Time will tell.

That’s a good insight, it’s given me something to think about going forward. I might have to go into a couple more LICs.

I have three investment funds: 40% Argo, 40% VDHG through Vanguard and 20% ROBO ETF. The ROBO was a risky one for me based on a hunch about robotic processes becoming mainstream around 2025, so I put a set amount in and am not putting anymore into it. The percentage decreases over time as I pump savings into Argo and VDHG. The VDHG is growing really well right now, and the Argo is paying good dividends so I’m covered on both sides. Like yourself, I’m a fan of simplicity!

Thanks Luke!

If you like keeping it simple, you don’t have to add anything 🙂

Sounds like a decent plan to me, especially not having too much in the ROBO fund!

Thanks

Another great post

I think that VAS is a great ideal during market dips

Please tell me more about your 9% REITS

Regards Len

Cheers Len, thanks for reading!

They’re nothing special, just a few property trusts I bought that looked attractively priced. Would rather not get into stock picking specifics as it’s not really necessary and might give people the wrong idea, but if you really want to look at them they’re CMA, AQR, AVN. I find them interesting, somewhat easy to understand and considering we’re on zero tax rates the higher yield is handy. Not recommendations or advice, invest at your own risk 🙂

Ive just signed up for P2P. I didn’t know about this. I am new to investing and very late in life! I’m 60 this year. I have followed your P2P link for more information. I am not sure if the $100 offer is still active. I can also get $75 if I sign up a friend.

Hi Lilypilly. First, great job getting started investing, that’s wonderful! Second, the Ratesetter signup bonus is available only for new investors, if you already have an account with them unfortunately you won’t get it. Did you sign up through my link or elsewhere? The bonus is definitely still active through my link once the criteria is met – investing $1000 into the 3 or 5 year market. More details on this page, and if you need any help, just send me an email here.

Thanks for the reply. I followed the link on your site and it was a very easy process. I did chose the 3 year option. After some more research I do believe I get the $100 bonus after a month. I will keep you informed.

UPDATE: I have just received the $100. ( @2weeks wait ) Its been the quickest and easiest 100 I have ever made. thank you .

Good stuff – glad to hear you didn’t have to wait too long.

Nah, not what I’d call a sensible low risk portfolio. Where’s the Bitcoin?

I was too embarrassed to list it. Truth is I took out a line of credit and ploughed in at the peak – I thought I was gonna be a billionaire. New blog post – how to reach FI in 3 months with Bitcoin 😉

Thanks for sharing your portfolio SMA. What made you decide to start simplifying your portfolio?

I’m thinking about doing the same with ours. We have a few index funds, a few LICs, and a handful of individual picks back when FireDad started dabbling in stocks. They’re not at the stage where I’d say they’re annoying to manage at tax return time, but the idea of simplicity keeps nagging at me in the back of my mind.

Also what do you think of WAX or WAM? They’ve both returned over 8% dividends in the last 5 years (and around 11% if we go back 10 years) which would fit with your dividend focus. Granted the fees are much higher than ARG or BKI but their past performance is hard to argue with.

Thanks Ms FireMum 🙂

Main reasons – making it more complicated does not add extra return, in fact it can be the opposite, so a realisation of ‘why bother?’. Wanting my partner to feel more comfortable with what we’re doing and how it all works, that’s much easier if it’s a simpler portfolio. And simply wanting less admin and stuff to read/follow gives me more time for other things.

Thanks for sharing your approach – I can’t tell you what to do, but I can only share that the simplicity is great and I wouldn’t go back to a large portfolio again 🙂

I wrote about WAM/WAX in a recent post here, which hopefully answers your question. Good manager and great track record but I’ve come to prefer the older LICs.

Another great post!

We are on our way to FI via purchasing shares to create a dividend income. Whilst I understand the attraction of LICs and ETFs I am finding it difficult to overlook banking shares and some other individual stocks which are paying nearly double the yield. Currently NAB is yielding just under 8% not taking into account franking credits (I think we can kiss these goodbye either next election or in future elections).

Obviously individual stocks will fluctuate a lot more…. but that dividend yeild would have to decrease significantly to drop below a suitable earn (4 to 5 percent). Do you ever consider holding a portion of your portfolio in individual stocks given their obvious high yield?

Thanks again from another WA couple chasing our goal of owning less and living more.

Hey there, thanks OLLM!

I had considered this in the past and used to own a number of stocks, many with higher yields. But I suppose I decided that since our porfolio was going to be entirely Oz focused, which will already mean a large exposure to banks, I didn’t think it was a great idea to pump more into banks by buying them separately. Unless the stock picks are going to be large holdings, they aren’t really going to juice the yield on the portfolio by all that much.

And more important than yield is making sure our income grows over time, with inflation or preferably faster. So to do this, we need to own a decent amount of lower yield high growth companies too. If holding only high yield companies, the risk is that dividends won’t keep up with inflation over time. I realised a balance is a good idea, the older LICs tend to do this exactly – hold a spread of high yield low growth companies, and low yield higher growth companies, offering a decent income which should grow nicely over time. So they fit nicely with our goals and makes sense to outsource the effort/management. Same goes for the index of course, which includes tons of both growth and income focused companies.

Hi Dave,

Any insights on why you decided to stick to OZ shares? I have had about 20% of my holdings in IOO for a while and was thinking that if Australia went through a recession or a market correction for reasons that didn’t have to do with th the global market, I could always sell US/International stocks and buy back into oz shares.

I know it sounds a bit like market timing but I’m mainly thinking about scenarios where the A200 was to drop a solid 30-40% over an economic cycle, otherwise, I probably wouldn’t bother and would just ride it out.

I was also thinking the same logic about playing with major currency changes (over a decade or two, not short term forex trading). I was sitting on a bunch of money around 2012-2013 (before I started investing) and can’t help but think that it would have made a lot of sense back then to buy US shares when the AUD was an all-time high…

Hey Vincent. My main reason is my preference is to simply live off the dividend stream from Aussie shares in retirement. I don’t want to have to deal with market prices and sell shares to create income – just a psychological preference I have. I wrote a bit on the Oz-only dividend approach here here and here if you haven’t seen.

Given the strong income, franking credits, plus income reliability from LICs which I invest in alongside VAS, this suits my approach. Our super is 100% international shares which I see as essentially a backup plan for later on. Also we’re both earning some income in retirement so not really worried about dividends collapsing or needing to use backup plan.

You’re right that if Oz crashes and nowhere else did, your US shares would provide a great rebalancing opportunity to buy Oz shares at much lower prices. You’d have to keep tax in mind and could also simply invest with monthly savings. And yes US shares were a great buy with a high AUD around 7 years ago, so currency moves can work in your favour at times and offer opportunities. Everything is obvious in hindsight lol. Hope that helps!

Great to see that dividend income continuing to increase Dave, no doubt it’ll be a bit of a relief when your coverage ratio gets over 100%.

My portfolio has been doing pretty well these last few months, I should really follow your fine example though and streamline things. I’ve got 13 different share holdings across 2 different countries with bank accounts in 3 countries and 7 different investment structures! Some of that has to stay the way it is but depending on the election results and subsequent legislatio I may have an impetus to sell down and hopefully then simplify things greatly when I buy.

Thanks very much, it’s definitely cool watching it climb 🙂

Whoa, that’s some next level complexity there mate, but thanks for sharing! Great to hear your portfolio is doing well.

There’s even people out there who have just 2 holdings – one local index fund and one international – and I hear they manage just fine, they’d look at us and shake their heads lol.

That’s another goal, to eventually get our loans and bank accounts down to perhaps 1 each – that’d be lovely!

I would love to be able to get it down to just two holdings and even better two accounts but for a whole bunch of reasons that isn’t really possible at the moment unfortunately. Still, if I manage to get the Aussie holdings consolidated a fair bit then that will take care of most of the complexity issue for me at least.

Totally understand that – two holdings seems quite extreme for most of us. Sounds like you’re on top of it anyway and at least you can rest easy knowing it will only simplify from here.

Hi Dave, nice article. I am a newbie in this space and have one question regarding qve. I was looking into it and its relatively new lic (4 years old ?) with high mer (0.9 ?). So, this breaks both the standard rules of Peter Thornhill to invest in old lic with small mer. So why qve ?

Cheers for reading PM. First, I don’t follow Peter’s rules religiously, everyone has to make their own decisions. It’s true, QVE is new, but the manager (IML) has been around for just over 20 years now and has a great track record with managed funds – their website here.

Basically, I believe in the manager and their philosophy. They are a conservative value focused manager which focus on companies with reliable earnings and growing dividend streams, and tend to dislike resources for their volatile earnings and unpredictability. As soon as you venture away from very large old LICs into the small/mid cap area, fees are usually much higher (many over 1% plus performance fees), so QVE is better than most in the space.

I expect it to provide a sustainable and growing dividend over the long term. But is it necessary to have? Absolutely not. Would my portfolio be fine without it? Yes. But I like QVE and want to own it as a small part of the portfolio.

Hey mate, great article, thanks! You wrote:

“As you can see, last financial year, our investment income was around $15,000. Our spending in 2018 was around $45,000. So a third (33%) of our spending was covered by investments.”

Sorry for the dumb question, but doesn’t that mean that you’re not really financially independent until you get 100% coverage? Genuine question, no sarcasm.

Does that mean when you originally left full time work it was with the desire of living life on your terms, knowing that you were losing money while still building towards the 100%? I know you both do some part-time work, but I thought that was more for enjoyment, rather than necessity.

Hey Nick, thanks for reading!

Good question. Well I guess some could argue that we’re not FI, but I think that’d be a rubbish argument. Our net worth is enough to create the income, we just haven’t converted all our property to shares yet – whether we do it in 1 year or 10 years, either way we’re living off the portfolio so I don’t see much difference. Not much different to someone selling off shares to live on from their portfolio – we’re selling off properties, living off that, while buying shares at the same time. I guess it’s up to you how you perceive that.

It’s true, the work isn’t necessary because of our net worth – we both really enjoy what we’re doing. Actually, part of me wanted us to never work again to prove this point, but that’s kind of a stupid idea lol. I guess us earning some cash now weakens our ‘proof’ of FI, but there’s not much I can do about that 🙂

You’re probably familiar with the idea that it’s almost inevitable for younger people to continue being productive and earning money after hitting FI because they have heaps of energy and get to choose what to do. Am I FI or fraud? That’s up to you (and everyone) I guess!

Love it, makes total sense, thanks for clarifying. You’re right, there’s not a lot of difference between selling properties and selling shares, both of which result in living off the cash. The point is, you are living life without compulsory work. Also, there’s no need to prove anything, really. 🙂

Thanks for the share and transparency with what you do. I also bought into too many different LICS when starting and even before reading this I was thinking of dropping AFI and WMI and buying more into MLT while its reasonably low, or finally moving into the index (out of my super that is). I do still like to have a couple of individual stocks that pay higher yields even if they are more risky. Like you said what feels right for you 🙂 Look forward to the next post.

Thanks for sharing your own experience Ben. Seems a lot of us get too enthusiastic and buy too many holdings 🙂

Lots of investing lessons to be learned along the way, hopefully I’ll pick up some more and will be sure to share them here!

Hi Ben & Dave,

We’re just starting out on this FI journey and have bought a couple of LICs already. Our next two purchases will be another LIC and an Australian index fund. We honestly, truly intend to never sell anything – just keep investing with our savings and reinvest the dividends from each as they arrive until we need the income to pay the bills.

I’m curious as to what you mean by “too many different LICs/holdings”? How many is too many? What are the downsides of having 5+ LICs? I figure they’re all similar, but also all different, with different managers, styles, focuses, number of holdings, and will perform better at different times, so why not have a slice of all of them (particularly the older, low cost ones)?

I know you keep talking about tax time, but my dividends and franking credits from IAG pre-filled into my tax return this year, so I don’t see what’s so hard?

Can you give more information about the downside to having “too many holdings” (before I make the same mistake and then have to sell!)? Keen to learn from those who have gone before! Thanks 🙂

There’s nothing inherently wrong with it; it just means you’ll have to pay brokerage for each separate holding should you decide to buy more of it.

Also, Dave is a lover of simplicity overall, so I suppose the fewer different holdings you have, the simpler it is, there’s less overall to keep track of. Considering a lot of the LICs have very similar holdings anyway, that’s a reason to possibly avoid some of the double-up.

Well, there’s little to no benefit to having so many. So it’s unnecessary complexity. There’s no set number that is too many. It’s just that it becomes pointless to keep adding similar exposure via a new holding. But if you prefer spreading it around more, that’s okay too. Your dividends will not be pre-filled for all holdings – you’ll have to input a few.

I’ve come to appreciate the joy of simplicity – in life and in investing. It’s just something I like, so I’m trying to practice it a little more with each year that goes by 🙂

Thanks for the response. I guess it’s just FOMO that I want to invest in them all 🙂

To be honest, AFI is our least favourite of the big ones, but we do like ARG and MLT. We’d probably end up buying some AFI anyway eventually – because FOMO and everyone else seems to buy it (not a great reason, I know!) But it will probably be our last LIC addition if we do.

We did buy some BKI, but if I was intending to restrict my portfolio to only 3 or 4 LICs, then I probably wouldn’t have BKI and MLT since they’re both managed by the same family and one of the reasons for having more than one is to spread the management risk around. Plus they only hold around 50 companies where the others hold 100+.

I do like AUI and DUI as well, and I think I’ll come around on Whitefield too, eventually!

I’m not bothered by a little bit of extra typing once a year at tax time – especially if Sharesight will give me a report anyway (but even if it doesn’t). I’d still be looking at keeping my number of individual holdings under the 10 free ones available to monitor in Sharesight!

We have recently restructured our home loan (which was all but paid off in the offset account) to include a line of credit which we will draw down on soon to buy some ETFs (our current thinking is roughly 80% VAS/20% IWLD at this stage). My husband is NOT keen on the extra typing for his tax return so we will limit the number of holdings in joint names for this reason.

But we’ll see how it all pans out.

Another great post. Thanks for being so transparent. I think it really hammers home all that you write about. My husband and I really like the KISS principle too. We have been FIRE for the last 2 and a half years, have no loans, no credit cards, no kids, never owned a brand new car and always keep them for at least 10 years, own our own home in Brisbane. Can’t do you a pie chart (lol) but our financials are almost too simple to warrant the trouble. We have 32% in 3 LIC’s (AFI, MLT, BKI) 11% in Ratesetter (signed up through your link – Thank you!) 15% in cash and 42% in superannuation (10-15 years before we can access this). For a bit of extra cash and exercise we deliver “junk mail” twice a week around our suburb. Like you we try very hard to be mindful of our expenses and I keep a detailed tally of our income and expenses (that came naturally after running our own business). We grow some of our own veggies too. Recycling, repurposing and diy is a part of life and I love the challenge of reusing and upcyling something that other people don’t see the use. A lot of people would think we live a boring existence but I am never bored! Our FIRST overseas trip will coincide with our 30th wedding anniversary this year. A considerable dent in the finances but having gone this long before heading O/S (and not being an avid traveller anyway) is no doubt a contributing factor to FIRE. Thanks for being a constant inspiration and reassurance that I’m not weird. Ha ha. I look forward to reading along with your journey.

Your welcome, glad you liked it. Thanks for such a great comment – I really appreciate you sharing your story Danielle, that’s amazing! It sounds like we share many of the same values, so it’s totally not weird 🙂

For all you younger investors reading this hears a good analogy for you.

I started investing in 1990 with a block of land, 1991 bought first share in AFI, 1993 built first residential investment – 5 units, 1996 bought first commercial property at a cost of 1.137 million.

Over the coming years bought and built property residential and commercial plus a share portfolio.

So how has it all turned out – pretty well overall, some might say very well but looking back if I put everything into AFI, investing all my spare cash and dividends back into AFI I would be wealthier now.

The big kicker is it would have been done with a minuscule amount of the energy and hassle as the above.

The lesson Ive learnt is don’t discount simplicity.

Don’t discount your ability to complicate things and don’t discount your bias to thinking your smarter that in average.

Thanks for sharing this Brett – fascinating! And a great example of the power of keeping things simple and sticking to diversified dividend paying investments.

Unfortunately, like you I am often tempted to ‘shuffle’ my portfolio around. I am not totally sure who takes the prize on this one! Though I am certainly getting better at avoiding that temptation.

The desire to keep things simple has been a guiding force as of late and I am happy for that.

Haha it affects us all it seems. Just to be clear I was just having a play with the word Shuffle, not saying you churn your portfolio 🙂

Great post – you write well.

Questions

– does your portfolio income of $15k in fy18 include the reits and p2p lending?

– best guess would be you have around 380k shares with a similar amount of home equity spread across 7? properties —- that’s a lot of property risk still, with not much equity in each on average , good luck keeping on offloading them, if I was in your position I’d be cutting losses and selling more of them…just an opinion.

– if you could wave a magic wand and convert your entire net worth into a portfolio of equal value – what would it be?

Thanks again.

Cheers Dave 🙂

1. FY18 only includes a little bit of REITs, most were bought in the last 12-15 months. P2P lending includes only a bit too, as the larger lump we had in there was not going to be a permanent part of the portfolio as we were spending the repayments, so I didn’t include that as income. This will probably reduce a little further but I will include the interest in this year’s figures because it’s more indicative of regular portfolio income (hope that makes sense).

2. 6 properties overall, yes some have small equity others larger. Yep plenty of risk here, but that’s what it is. Thanks for your best wishes, I might need it 😉

3. Tough question. To be honest, I think it would look something like my share portfolio does today, maybe just a little less in P2P Lending. Not to say it’s perfect, but I feel fine where it is and don’t have any major changes planned.

Thanks for the great post Dave, I got great insights and value from it.

Because I’m a newbie my portfolio is already simple lol , AFI, MLT, ARG, BKI , recently focused more on MLT & ARG and was thinking about WHF, not sure about that yet.

Question you said “Rather than trying to build equity, either through growth shares or leveraged property and then switching strategy later to focus on cashflow”

What do you mean by ‘to focus on cashflow’? Is this different from getting dividends?

I’m still learning.

Thanks

P.D. I attended Peter Thornhill’s seminar on Saturday and he said he has also simplified his portfolio.

Good stuff Plutarch, thanks for the feedback!

In your case, you already have more than enough holdings, so I wouldn’t bother adding another similar LIC.

When I say income/cashflow/dividends I mean the same thing – focusing on the cash you’re receiving from your investments, instead of the market value and chasing capital growth. Some people go for capital growth first to build net worth and then later on sell those assets to invest elsewhere for income to live off. I don’t like that idea. My view is investing for growing income from the start makes more sense, and if you have a good savings rate, you don’t need high growth or use debt to achieve FI. Hope that helps.

Thanks Dave!

Dividends is the way to go for me.

I forgot to mention that I’m debt free, have no mortgage, no kids and single so lots of saving opportunities lol

I have no other Investments other than those LICs. I’ll stick to my plan.

My situation is nowhere near as simple as yours, but it seems to work well for me. I started out investing only in residential property in Melbourne, but quickly realized that shares were pretty good too, so I stocked up on bank shares and a few other company shares. I retired with my income coming mainly from investment properties and bank shares.

Over the years, I sold off all my investment properties (the last one went under the hammer in late 2017) and also sold some poor-performing shares. I gradually invested the proceeds into the ASX, mainly LICs. Apart from my principle place of residence and my modest super, my portfolio looks roughly as follows:

43% in AFI and ARG

23% in smaller LICs and ETFs – e.g. MIR WLE CIE AMH GVF VAS (and a couple of others)

16% in the big banks

9% in other individual shares – e.g. WES SCG WOW AGL TLS

9% cash

I can very easily live off the income from just AFI and ARG.

I hadn’t heard of Ratesetter before … it might be worth a look.

Thanks for sharing your experience Robert – certainly sounds like a very comfortable position to be in with plenty of cushion even if we had a nasty downturn! And great to see we’ve got a number of readers already retired, which hopefully serves as motivation for the others.

Sure, I wrote about RateSetter and how it all works here if you’re interested.

Hi Dave, Great article

Perth property, what a drag huh? I have a couple of units near the city and they have done very poorly over the past 10 years. Rents went up high and then down and values have been pretty disappointing throughout.

I don’t see values doing much over the next few years with credit rules and negative gearing looking less attractive but I do hold out hope for rents improving. There are plenty of big projects starting up and the credit squeeze makes buying pretty difficult for first home owners. I am going to hold on for the next 5 years as I think Perth rents will will bounce back. Are you less optimistic?

Haha yep a drag alright!

The forward looking windscreen is a bit foggy at the moment, hard to tell what’s going to happen. But Perth property appears relatively cheap compared to the other capitals and history. Rents have actually already started coming back, we’ve had a decent increase on one in the last couple of months – the vacancy rate has dropped dramatically in the last 6-9 months and building has pretty much dried up so the rental market should continue to improve. Mining has picked up a bit and with any luck the rest of the economy will pick up and we’ll see how we go from there.

Our Perth ones will be the last to be sold because as you say the next few years look quiet, so we’ve got probably another 5-10 years before needing to sell.

Hi SMA, Another great article. I’m in the higher tax bracket, currently hold AFI, WHF,VAS and a bit of VHY. After much consideration I decided to direct all future cash into AFI and WHF, and DSSP all the dividends. I will be aiming for a 50/50 split between them. I also really like MLT and BKI and the temptation to buy them is always there, but for the sake of keeping it simple I decided I won’t be adding them in the near future, plus no DSSP with MLT or BKI. I quite surprised that more LICS don’t offer it. Overall, I am happy with my portfolio selection its nice and simple and suits my financial circumstances.

Cheers Gene!

Sounds like a sensible option given your situation. You can always add other holdings you really like towards the end of your journey if desired, but no need of course. I’m not sure what’s required for them to offer it but perhaps a special tax ruling from the ATO is a bit of effort and maybe not many shareholders have asked. All the best on your journey.

As someone sitting on the sidelines fully invested in your journey, it was great to see a portfolio update, thanks for sharing.

I noticed you have decent amount (percentage wise) invested with P2P lending. We hold one years living costs at the moment as a buffer and I’ve just started researching what other options are available other than a bank account for a small portion of it. Obviously you have satisfied yourself with the pros and cons and i’ve read your post on the subject, but with your research, has P2P lending been tested in ‘rocky’ market conditions / recession?

Thanks, glad you found it interesting 🙂

The answer is no, P2P Lending (RateSetter) hasn’t been tested in a recession – it started in the UK in 2010. So at this stage 9 years with no investor losing a cent of principal or interest – thanks to the provision fund – which is a pretty good track record, but I’ll definitely be interested to see how it holds up under an economic downturn. The credit team does adjust the fees they charge borrowers based on outlook and likelihood of default, but I’m sure it’s not bulletproof.

The amount we keep in RateSetter will probably fall a bit closer to 5-7% of the portfolio – we had a larger lump in there but have been spending the payments as they come in. Hope that answers your question.

Dave – can I first say that you have some super-keen readers that respond to your posts so quickly! I always find I’m one of the slower to respond, with my comments right down the end… I can only dream of having such a loyal reader base one day 🙂

Notwithstanding that, I think it’s great you added VAS to your portfolio. It offers a great, mostly franked dividend – Indexing Ian would be very proud 🙂

Cheers, Frankie

Thanks for that Frankie – yes I’m very grateful to have readers that keep coming back, and leave comments too!

You’re right, Ian would be nodding approvingly I’m sure 🙂

Love it again, Dave. Really enjoy the portfolio updates so please keep them coming.

I’ve still not pulled the trigger on anything further than AFI & WHF as i dont even do anything at tax time due to DSSP! As simple as it gets currently.

I keep flirting with the idea of three more categories; Small Caps / Asia Specific / Broad Global. Im at my number where i invest my chunk of $ again and going with AFI while i still ponder but i was hoping for your next LIC review to possibly be in the small cap or Asian sector? Very demanding i know but you don’t ask you don’t get hey..

Thanks mate

Having zero to do at tax time is pretty damn cool!

Out of those 3 choices, the one that probably makes the most sense if you want more diversification would be global shares. There’s already some small companies in AFIC and WHF and Australia has a growing number of companies which have Asian exposure, obviously mining, food etc.

Haha I’ll see what I can do, but it’s pretty unlikely to be an Asian focused one, as I don’t really follow those.

Hi Dave,

Can i ask your opinion regarding the feasibility of Margin Lending

Pro’s and Con’s ?

I own my Home , is it viable to borrow money at around 5% to invest in shares ?

do you have an opinion ? and of course i wont take this as advice!

Thanks Again

Brad

Is it viable? Yes. Is it a good idea? Depends on the person, their risk tolerance, investment strategy, cashflow management, temperament etc. Can’t give a blanket answer.

Main pro is you might be able to achieve a higher total return over a decent timeframe by using leverage. Main con is the certainty of debt and the uncertainty of sharemarkets. Over the long run things should be fine, but that’s not enough to keep some people from getting worried and selling out during a scary period.

I’m neither for or against really. I really like the simplicity and thought of having no debt and a share portfolio. But I also think that leverage used sensibly can enhance returns, a bit. Generally I’d say it’s better to focus on saving more and keeping things simple because the relatively small profit margin from using leverage is perhaps not worth it, for the extra bit of risk and uncertainty that comes with it.

Thanks Dave!

Great advice and covered all the areas i was not sure off.

Brad

Hey, love this update. Heading down the same path offloading property etc. Had a massive opportunity to make matters less complicated with shares, though like your (previous) self, have an unintentional tendancy to overcomplicate matters. My query is, why did you bother to repurchase individual stocks inside super? And does your fund have an annual premium to do so (plus brokerage)?

Thanks Michelle! Shares definitely makes things simpler and offers much more income in Oz. Haha don’t worry, I think I still probably overcomplicate things a bit!

The individual stocks were part of a stock picking experiment, so I still wanted to continue this. Yes there was some super fees and brokerage to do this. We’re now winding this up though as I’m not interested in continuing and are switching back to a low cost shares option.

Hi Dave!

Do you have any tips on selling property? How do you choose real estate agents? Are you in favour of pre-sale house staging or is it not really cost effective? We don’t have any investment properties, but we are thinking about selling our own house (which is mortgage free). We want to downsize from a 4/2/1 house to a 2/1/1 rental apartment closer to work so we can get rid of one car and invest the money in LICs/index funds. I don’t know if this is a good idea, but both me and my partner are completely sick of cleaning the roof every couple of months and looking after the garden which is a lot of work in a leafy Brisbane suburb!!

Hey Olga, I don’t really have any insights on this. I follow the plain vanilla approach of looking for a highly rated/recommended agent and then just following their advice on how to best present the property – only thing that has been recommended has mulching the gardens for one property pre-sale.

If the property is well located and presents well, you shouldn’t have any trouble selling it for a decent price. Hopefully markets pick up after a couple of rate cuts but it’s different everywhere, so who knows.

I like your idea overall. You’re likely to end up with much less hassle, no ownership costs and a large passive income from investing the money elsewhere, which should more than cover your rent – there will be some extra tax each year but you’ll have much more flexibility, cashflow and convenience with the new location, smaller property and one less vehicle. All the best with it!

Hi SMA, thanks for all you do to clear the path for us!

Hey just curious why did you sell AFI? I’ve just found your blog and have devoured most of the blogposts, and so far I would’ve thought you were such a fan of AFI especially with the advantage of DSSP. What made you change?

Thanks!

Rick

Cheers Rick. Thanks for reading so many posts!

As mentioned, it was due to my desire to simplify the portfolio and the fact that AFIC was trading at a large premium, so offered an attractive price to sell. We’re on very low/no tax rates at the moment due to early retirement so the DSSP was not being used.

Also, there isn’t much difference between the ones we sold and kept, so we could’ve gone either way. I don’t think any less of AFIC than the others to be clear. Hope that makes sense 🙂