This portfolio update is a little later than usual.

Time kinda slipped by, and with the website update I just plain forgot about it!

Anyway, we’re here now. So in this article, I’ll share how our portfolio is progressing, give an update on our dividend income, and what we’ve been buying lately.

Let’s get started 🙂

Here’s a breakdown of where our wealth is located. As always, measured in percentages.

If you’re new here, I don’t share our net worth numbers for privacy reasons. I’m not anonymous like many bloggers, and feel no need to share everything.

Besides, it would be like telling your friends how much money you have on a regular basis. Wouldn’t that feel weird?

Since last time, shares, property and super are slightly bigger, as markets have risen. Cash is also dropped as we continue to invest every single month. No market-timing games here!

Without super, the breakdown is: 56% shares, 32% property equity, 9% cash, 3% p2p lending.

We’re planning to sell another investment property this year, given the strong current conditions of Perth and Brisbane (where our properties are located).

We won’t actually need more cash for a while. But there’s no guarantee it’ll be a good time to sell in 12-18 months. Why trade good conditions for the hope of great conditions?

The property we are planning to sell is in Brisbane. Reason being, it’s the one which has the highest amount of equity, which is what’s useful to us. Selling a Perth property with little equity is much less useful.

Well, since my last portfolio update, markets have been flying. The US market is up over 20%, and the ASX is up about 15%.

Remember the gloomy people who promised we’d have a second corona-crash, and the recovery was temporary.

Where are they now? Probably shouting at the sunshine somewhere.

From what I’ve seen, companies have reported pretty strong results in the last few months, which has helped underpin the recovery in prices.

And pleasingly, dividends are also bounding back from the frosty winter of 2020. I look forward to some (hopefully) bigger payments later in 2021!

From all reports, capital city property around Australia is pretty hot this year.

Mortgage rates at 2% are slowly getting built into prices, as has happened every time rates have come down. I don’t see this as good or bad – it is what it is.

But if you’re an owner of real estate (which about two thirds of the population are), you’ll likely see a boost in home value and net worth this year.

On the rental side, our properties in Perth have all recently had nice rental increases. And homes are selling quickly too, so prices are starting to move.

There’s a lot of talk about affordability – yes, even here in Perth! But everyone forgets that prices and rents are still the same or lower than they were 10 years ago.

In that time, wages have slowly increased and mortgage costs have massively decreased. A lot of moaning, no context or perspective. That’s the media for you.

Anyway, we’ll continue slowly selling down one property every couple of years as planned. And a bit of price growth before then would be nice!

Since my update in December last year, we’ve continued to buy shares every month as I mentioned. There have been some small changes too.

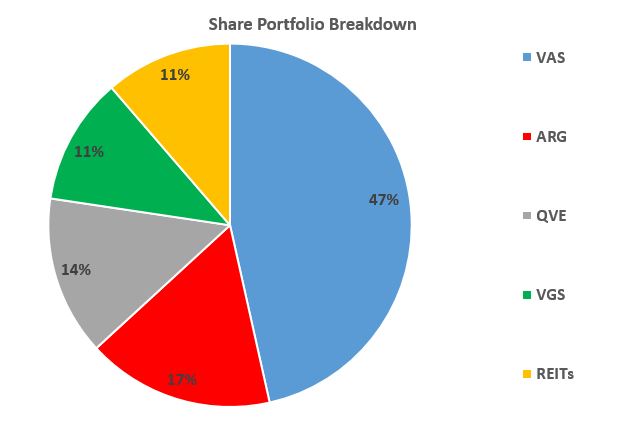

I added one more real estate trust to our portfolio – a large, diversified real estate investment trust (REIT) with a few hundred commercial properties and very long leases, run by Charter Hall (CLW).

We now have two REITs in our portfolio. To me, they look like good value and are throwing off attractive, sustainable income streams in the 6-7% range,

We’ve also been adding to our international index fund VGS. Both of these parts of the portfolio have become bigger sooner than I expected – partly due to their performance and also having extra cash to invest.

Here’s the breakdown of our share portfolio at the time of writing. You may notice something else…

Astute observers may notice something missing… Milton. That’s because I sold it after their second disappointing dividend announcement.

Why? Well, because management basically made no effort to smooth the dividend, despite years of saying things like “we have ample cash and franking credits to support the dividend.”

And there was no good explanation. This inconsistency really annoyed me. I don’t expect miracles, but they didn’t even try. Other LICs have done much better in this area, despite the massive drop in income from their portfolios.

So I spread the funds across our other holdings like real estate and VGS, while also buying a decent amount of VAS, since Argo was trading at a premium.

I mentioned this decision in a forum and people seemed to think it was a big deal, and that I was being reactive. But it didn’t feel like that.

If one of my investments isn’t going to meet my expectations (and there’s another good option), why would I cling on? I’m not married to any investment.

You should fall in love with investing, not your specific investments.

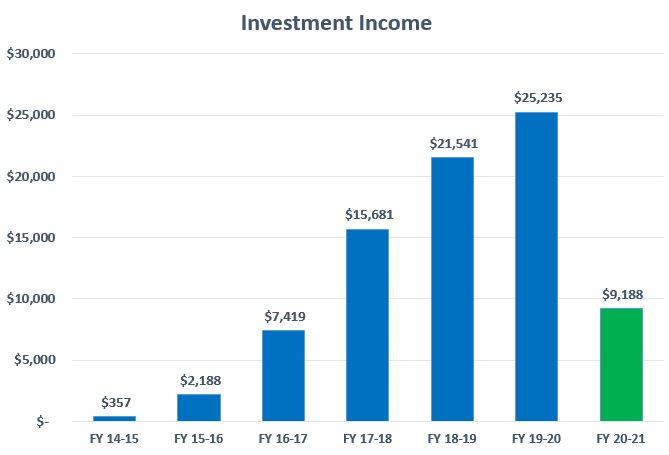

Alright, it’s time to see how our investment income fared during the second-half of last year.

I measure this by financial year, so here’s what the first 6 months of 2020-21 looks like.

Damn…

Even with a recovery of dividends in the current six months, I don’t think we’ll be matching the income from last year! This chart’s lovely streak will come to an end 🙁

Despite that, I still find this metric to be the most enjoyable way to measure my portfolio over time.

I haven’t included interest earned from peer-to-peer lending, since I can’t get a 6 month interest summary. While it won’t be enough to keep the streak going, I’ll be sure to include that in the end of year numbers.

In the new financial year, I’ll share the full-year results, and towards the end of the year, I’ll do another update of what we’ve been buying, along with the other tally I’m trying to grow over time – charity donations.

If you’re interested in the spreadsheet I use to keep a running estimate of our annual investment income, use the form below to get a copy automatically sent to your inbox.

For new readers: You might be wondering how we consider ourselves ‘retired’ if our passive income of $25k isn’t more than our household spending of $40k. I explain exactly how it works in this article. Short answer: cash from offloading property.

You can also find a detailed article on how we’re turning our equity into income, using my property-to-shares transition strategy. Feel free to skim through it to get the basic idea 😉

The last 12 months has been a really interesting time to be an investor. We’ve seen highs and we’ve seen lows.

And just like always, those who kept their cool and stayed focused on the long term are the ones who came out the other side wealthier than before.

While the dividends are starting to recover, our share portfolio’s value is at a record high. That’s what happens when you do what Peter Thornhill suggests when prices are falling: “hold your nose and keep buying more.”

That’s enough from me. How are your investments going? Let me know in the comments below…

My thoughts on ‘The Great Taking’. An idea that the masses will lose untold amounts of wealth in the next financial crash, due to a deliberate plan by mysterious figures.

I explain why (and how) I bought a Tesla. The experience so far. How much it cost, and ongoing savings/expenses. Charging options + EV basics. Tax rebates + subsidies. And whether you should get an EV.

Get my latest content and thoughts straight to your inbox.

A fresh dose of financial motivation to power your journey.

Mate you need exposure to crypto. Bitcoin up 100% and Ethereum up 500% since Jan 2021.

That’s nice, not interested.

Excellent run down! I’d love to see the exact figures but understand your point on privacy.

My investments have been going quite well, but in the past few weeks a few shares have been hit – mostly just dropping from their post covid highs. But overall, net worth is increasing nicely!

Looking to buy a house this year, but Canberra prices and growth is insane!!! So just working on saving up a decent deposit.

Love your work.

Nathan

Thanks Nathan. Wow, Canberra too? Sounds like real estate in every city is booming right now.

Pretty crazy to think markets are now higher than before covid. An impressively fast turnaround from March last year!

Lol, short and sweet

That’s okay, but even a small allocation of 1-5% crypto to your portfolio will help with overall returns. Just a thought.

From the email I received from Dave:

Thought of the week: We live in a rapidly changing world where strange things have become possible. It’s no wonder people are attracted to speculative bets which may have a huge payoff. While most of your money is best placed in boring investments, having a tiny amount in other things you think have potential is maybe not as crazy as it used to be.

For me, that thought is what pushed me to put a tiny amount into crypto….

I recently unloaded Milton too for a similar reason, happy now.

Fair enough mate, thanks for sharing.

Forgot to mention, great new website!!

Also was looking to simpliying the portfolio & MLT was now not ticking all the boxes.

Haha thanks, appreciate that!

Thought of the week: We live in a rapidly changing world where strange things have become possible. It’s no wonder people are attracted to speculative bets which may have a huge payoff. While most of your money is best placed in boring investments, having a tiny amount in other things you think have potential is maybe not as crazy as it used to be.

I thought you were hinting at buying crypto?

Haha nah it was a more general comment. It occurred to me that so many crazy things are happening that you can’t blame people for putting money into certain things because almost anything is possible now. And I think that’s a bit unique to the modern era since tech and innovation is moving so fast.

To be clear, I still feel the same as before in that I don’t consider crypto a serious investment, but if ppl want to set aside a small % for things that interest them, or speculation, then no big deal (as I’ve said before).

And you know what, I actually saw a shitcoin recently that made me laugh and would consider buying it for fun – has a bulldog as the logo/brand/whatever you call it lol. But nothing has changed, my investment portfolio will remain shares and real estate only. Will keep you posted 😉

Mlt didn’t go down anywhere near as much as vas did with dividends, so happy about that 16% vs 66% if I remember correctly. But I couldn’t understand why they didn’t smooth out either.. with the decent cash buffer on hand… I’m hoping the dividends lost was due too taking advantage of cheap share prices….. so I’m holding for now. But yeah I fully understand why you sold

We can’t make a comparison between an ETF which simply tracks the index and a LIC with managers who hold cash reserves for a market downturn. VAS is expected, MLT made a decision to use the cash to grow their portfolio, rather than smooth dividends for investors.

That’s a good way of putting it Aurelia 🙂

Dividends for Milton did drop further than that. The September dividend dropped by about 20%, and the March dividend by about 35%. So overall maybe about 25-30%. VAS was more though, you’re right. But yeah, the whole ‘say one thing do another’ just made no sense and seemed disrespectful to shareholders.

Yeah I was also disappointed with MLT, especially the disconnect between their words and their actions.

In the end I decided to hold onto them as they only make up 18% of the portfolio and I’d have to realize some capital gains but I’m not sure I’ll add more, we’ll see.

Yeah fair enough mate. If tax was going to be an issue then I may have just held. They do trade at at decent discount from time to time, so you could just decide to be pickier and more opportunistic about it.

Hey Dave.

Just coming back to this comment, I guess it was fortunate I waited.. I sold MLT last week to take advantage of the merger premium and redistributed the funds into VAS as I wasn’t interested in holding SOL in the long term, I’m finding I’m leaning further into a simplified passive approach so SOL wouldn’t fit the bill.

Speaking of the passive approach.

Now that more of the portfolio is in VAS (I still hold AFIC) when it comes to dividends or in this case distributions, if I remember correctly from one of your other posts; it would still be suitable as an income stream, the investor would just need to hold more cash on hand to smooth out the distributions during a downturn?

Thank-you, appreciate you taking the time to come back and comment on old posts.

Very fortunate 😉 Nice work mate.

Yes that sounds right to me – VAS is still going to throw off a decent income, on average, but just fluctuate more from year to year than AFIC. If living on dividends, a bit more cash is definitely a good idea in that case.

Thanks for the update! Loving the new website btw!

I had no idea Milton cut their dividends, I’ve been wanting to sell them to simplify our portfolio but don’t want to get that capital gains tax. Do you think it’s worth waiting for the next down fall and using that to readjust, or ripping the bandage and use those fund to go into other ETFs like VGS and A200 and ride their nice waves?

Cheers mate! Hmm tricky one. Depends how badly you want to simplify, how much the tax would be, and how far it’d have to fall to wipe out your tax liability? Only you know these things. MLT will probably give similar returns to the Aussie market, so it’s not like you’re missing out or anything.

Looking good mate! Thanks for the update.

I was looking at buying a property in Perth later in the year, hoping for it to by retirement PPOR!

For what I would want, Sydney is just way too expensive, and even surrounding towns aren’t cheap. Had a look over at Perth and surrounds and couldn’t believe the value for money.

That being said I’ve never visited Perth before, but checking it out in June so I hope it suits me!

Keep up the good work.

Cheers James. The difference in prices between Syd and Perth is enormous now, funny to think 10-15 years ago they were about the same!

There’s a lot of places to choose from, so I’m sure you’ll find an area/property that’ll fit the bill 🙂

how do you track your dividen payments? Do you use sharesight or your own spreadsheet. If its the latter, do you mind sharing your spreadsheet

I use Sharesight for tracking, but also add in the total plus other investment income (like p2p lending) into a very basic spreadsheet. If you’re super keen, you can download the spreadsheet in a previous update (after the income section) by filling out the form and it’ll be sent to you by email.

Hi Dave,

So the hard question for you is:

By moving up the sale of your Brisbane property aren’t you effectively trying to time the market?

Did you have any firm rules about what would trigger the sale of properties in an IPS or similar? It looks like with the dividends you are likely to receive and with the current cash on hand you would have enough funds for several years before you would have to sell another property. I understand that selling would further simplify your portfolio but by selling early aren’t you effectively trying to call the top of the market? Going ahead with the sale would mean that you would have an awful lot of cash in your portfolio.

As the finance simpleton and wage slave that I am, I have thought for many years that Aussie property is overvalued and it will have to fall but it continues to rise. Now with the crazy crypto markets, helicopter money from the government and practically free credit on offer everywhere I’m wondering when the party is going to end. Are we going to see inflation rise when it does? Is having a huge excess of cash on hand a good solution no matter the end result? I dunno mate but there is probably another blog post in it 😉

Cheers,

Shaz

Good questions Shaz!

If I need to sell this year or next, and it’s a good time to sell now, then it makes sense to me to sell now. I would be taking my chances waiting another year and hoping for a better outcome, which is more akin to timing the market in my view. You may see it differently. With our last sale, we waited the extra year and the market was shit by the time we sold – had we sold at the previous good conditions the outcome would’ve been better. And by waiting the extra year (in our case), you then don’t have the same flexibility over whether to sell or not – that’s the trap.

Our cash runs out quicker than you’d think because we have 5 properties and we’re paying P&I on all of them at interest rates that are higher than an owner occupied home. Payments are also higher because we’ve had 5-10 years interest only on them, so the principal payments are now quite aggressive.

Yes, we’d have a lot of cash, but that’s just the nature of offloading property – we can’t sell a bedroom at a time. I’d still be dollar cost averaging into shares because it’s what I’m most comfortable with, rather than dumping a huge amount into the market.

As for inflation, I have no idea. I suspect that the power of technology will still help us avoid high ongoing inflation, even if we have spurts of inflation from time to time. It all becomes very academic and just guesswork really, not something I bother worrying about.

Hope that helps explain my thoughts.

Do you see your self buying into any more LICs with a better dividend track record (AFI, AUI, DUI, WHF)? Why/why not?

My preferred out of those would be AFIC, but it trade at a horrendous premium most of the time, so I’m not sure that’ll happen. AUI/DUI aren’t as diversified as I would like and WHF fees are a little too high for my liking too. I’m open to it though if some incredible bargains come along.

I remain quite boring with the following which I add funds to each month. I alternate each month between the three.

AFIC

WHF

Six Park who spread funds amongst VGE, DJRE, STW, VGS, VGAD, IFRA and IAF.

Not sure if I’m doing things right but ……….

Great news, there is no ‘right’ – so you just keep doing your own thing 🙂 Sounds sensible enough to me, thanks for sharing.

I bought CLW recently and it’s become popular as an income stock of late as it held up OK during Covid due to its long WALE theme…6% distribution, what’s not to like.

Held onto MLT but it’s in the sell basket if it disappoints next divvy payout.

Share your view on Crypto, only time before the banks bring out their own version and IMHO its gambling not investing.

Nice to see you in Money Mag too.. Keep up the good work.

Cheers Mark. Yeah CLW is very attractive in the current environment I think. Still way down from its previous highs, despite earnings and dividends being completely unaffected by covid which is quite incredible when you think about it.

CLW looks good and solid. Have you thought about their closed investments? Any thoughts on them?

Only briefly. There’s too many funds to look at to be honest. And none seem as large and diversified as CLW (could be wrong though). Plus, I was buying CLW at a discount to its assets up until recently because the share price was $4.40-$4.60 with portfolio value of $4.70. I also prefer listed because its simpler and easier to transact.

We are all taking slightly different approaches but as you say like in most things there isn’t only one right way. Trying to time the market (to some extent) is fun though. If it goes right you get to feel like a hot shot.

Good stuff Dave. Thanks for putting these out.

but Argo also reduced it’s dividend !

Hi Dave, great website and article. Absolutely love your LICs reviews too. Like you, I’m a Thornhill LICs fan, but I also see a place for the Vanguard’s products in the portfolio (e.g VAS/VGS). Noting that you’ve sold MLT, I’m wondering whether you have changed your long term view on LICs and the approach to living off dividends?

Hey thanks Marco. The answer is no, not really. I am still happy to buy certain LICs if they’re trading at a decent discount (as has been the case for a long while now) and I still prefer most of our passive income to be coming from dividends. While I’m open to trimming our shares for extra income (like VGS), to me, living off dividends is still a more enjoyable way to receive income in retirement.

‘Probably shouting at the sunshine somewhere’

I found that quote far too funny for some unknown reason!

Great update again Dave. I can definitely understand your frustration with MLT, I bought a large chuck of them a few years ago, bought the exact same ($) amount of WHF as the same time also. WHF has well outperformed MLT in the time I have owned both. In saying that I feel WHF’s recent positive performance has been buoyed by its large percentage of big bank holdings.

Also I think the fact MLT paid a nice divided in February 2020 just before the COVID crash hurt them a bit financially and mentally. Here’s hoping they regain confidence in the coming years.

I live in Brisbane and can confirm its a great time to sell here (like every other capital city by the sounds of it). Where abouts in Brisbane is your Investment Property, I know asking for an exact suburb is a bit offensive, looking more for a North, South, Western suburbs style answer.

Cheers

Haha thanks mate – not sure where that line came from, just popped into my head when thinking about the permanently gloomy people.

Whitefield would’ve also been boosted by since it used to trade at a large discount but now it doesn’t. Good to hear about the Bris market. Our property is in New Farm.

New Farm! O la la!

You will sell that house quicker then it takes you to read this sentence.

I look forward to your next investment update post sale! Keep up the good work!

Haha it’s a pretty simple townhouse, nothing too fancy. Cheers, I hope you’re right! 🙂

Hi Dave,

Not expecting a recommendation, more so just your thoughts. Although I consider myself a buy and hold investor, I used to hold both VHY and a Bond ETF. I sold out of them for a slight profit.

I know you tend to lean towards internal for growth and Australia for yield. In my circumstance I currently hold WDIV, DUI and ARGO. I was also considering adding in a Global Infrastructure ETF or LIC, I’m currently looking into IFRA, MICH and ALI.

Do you have any opinion on global infrastructure? It seems like it would be a way to get both income and growth, whilst diversifying away from Australia. My other question is do you have a max amount you would be willing to pay in terms of MER? I tend not to be much of a stuck picker, but I’m not quite OK with being fully passive. I’d be looking to allocate a similar amount to what you have in REITS, around 10% to 15%.

Hey Chris. Interesting question. I don’t really have a view on global infrastructure. The income portion is higher than global shares, but growth will be lower, which is the tradeoff. As you say, it’s return profile is somewhere in the middle of yield/growth. So if you feel it’s a good fit for your portfolio, then that’s what matters.

On fees, you may see I have an active fund which charges around 1% (which is very high) – I wouldn’t like to go over that, and keep most of the portfolio in low fee funds.

Thanks Dave. I’m not particularly in a rush, I’m mainly trying to decide between IFRA and MICH. I like the track record of MICH, the only thing that’s really putting me off is the massive MER. As for IFRA, it’s passive, has much lower fess and pays quarterly dividends. In the mean time I’ll just be investing into the same 3 funds as normal. I believe that global infrastructure does have a place in my portfolio, to me global infrastructure seems to provide a solid middle ground in terms of yield and growth.

Yep fair enough. I guess the other thing to consider is the Magellan fund is a very small portfolio (20-40 companies) versus 130+ for the Van Eck index.

Great article Dave and great new website. Interesting views about Milton, I of loaded some Milton at the start of the year and bought FMG which are paying 10% dividends 100% franked. I also bought some CHN which have doubled in price. What are your thoughts on mining shares atm?

Hey Don. I don’t really look at individual shares these days – with a few real estate trusts being the exception. Mining stocks could continue doing very well for the next few years, but keep in mind, the cycle will turn at some point and dividends and prices will take a hit. All that is to say, I have no idea what’s going to happen – you probably know more than me 🙂

Hey Dave,

What do you think of the CLW share offer? Will you be using it to expand your position or wait and see closer to the end and compare the share price then.

Hey Jason. Funny you ask – I just scheduled the BPAY transfer for it. I doubt the price will drop below that, but worth checking just in case. I find it pretty attractive in the current environment.

Hello Dave,

Another great post. What is the difference between VAS, VGS AND VDHG? I am reading alot about people simply holding VDHG these days.

I just started investing this year after reading your blog and Peter Thornhills book so I now regularly invest each month in MLT, WHF, ARGO, VAS each month I buy shares in one of those and rotate them each month ongoing.

I have no idea if these are too similar or whether there is enough diversification here and whether VDHG is somthing I should add on.

Any thoughts on this for a beginner investor with a Dollar Cost Avg and Long term frame of mind.

Hey John. VDHG is an all-in-one type of fund. Meaning it combines VAS, VGS and some other holdings to make a blended Aussie & global index fund portfolio. This way, people have only one holding to manage and buy each month which makes things a fair bit simpler.

If those are your holdings currently, yes they are very similar, so if you were going to add one for diversification, VGS would be the one since it is international and adds something complimentary. If you buy VDHG you are adding more Aussie shares (since VDHG has some VAS inside it). I wrote an article which breaks down the different choices for investing in international index funds here. You might find it helpful.

Thank you very much for taking the time to answer Dave. I will check out your other article as well.

I also dumped a big chunk of MLT after the last dividend. Was extremely disappointed with them. I used the money to take advantage of the cheap bank stocks and timed it perfectly. Sold them now and put it back into AFIC who DID smooth their dividends.

Very nice timing indeed Starbuck! Yeah the way it was managed was just disappointing and opposite to their messaging over the last few years.

>>> Astute observers may notice something missing… Milton. That’s because I sold it after their second disappointing dividend announcement.

Doh. Check out what happened today. MLT jumped 17% on the SOL merger announcement. It looks like a pile of dividends are on the way too.

Haha yes, I timed that one perfectly 😉 I had a good laugh when I read the announcement… oh well.

Hello Dave,

Love seeing the updates on your portfolio. As someone who is only a few years into the FI journey and living in Perth as well, it is very inspiring to see what can be achieved 🙂

On previous updates, I have seen your charity portfolio and I would love to know more about that. E.g. Do you keep the holdings in a separate brokerage? Is the portfolio all under a charity you have or do you just donate the dividends? Are the dividends counted as your income? Maybe you have explained in a different post? Maybe I am making it sound more complicated then it is 🙂

I just would love to start one myself as at the moment I just donate from my salary, but I think it would bring me a lot of joy to have a separate charity portfolio and be able to donate more and more over time 🙂 I know I could donate dividends from my main portfolio, but they way my brain works, is that I like to keep things for different purposes separate. E.g. I keep a separate ‘holiday portfolio fund’ from my main account. Should I/ could I keep them in the same account, probably. But I was saving money for holidays in a separate account and then just decided to put all of it into the stock market and let the dividends decide what my holidays will look like… which means I haven’t gone anywhere in the last 2 years, not that it matters anyway, cause where am I gonna go? 🙂

Anyway, would like to know more about your charity portfolio.

Thank you for your time 🙂

Hey Lillie, thanks for the comment!

There’s no actual ‘charity portfolio’. It’s just the amount of money that got donated in a given year. I just do this out of our normal bank account like any other bill. So when you see our ‘household spending’ posts, it shows the donations in there also as an expense.

You can certainly have a separate investment if you want to do it that way and allocate the dividends etc to charity, but for simplicity I just have one pool of investments and simply track whatever we donate to get the enjoyment/satisfaction benefits of trying to increase it every year 🙂

Hi Dave,

Just wanted to start by saying thankyou for sharing your FIRE journey with us all.

I’m curious to understand where the 4% rule sits within your FI strategy, if at all? By the looks of it you’re chasing passive income through dividends etc and not seeking to draw down on your capital base, is that correct? I ask as I’m in the process of trying to build out my own FIRE projections and am grappling with this question in regards to how I structure my portfolio. If you dont mind me asking what is the average dividend yield you use for your projections?

Hey Chris 🙂

Well I’m still essentially following the 4% rule or thereabouts, it’s just that my portfolio right now is quite dividend heavy, so that means no selling is required. I just find dividends a more enjoyable way to live off a portfolio. Having said that, I’m building my global shares portion out over time, and am happy to harvest some gains from that holding by selling some if needed, so I’m not against the selling approach.

Even a 50/50 Oz/global portfolio will currently result in a dividend yield of about 3-3.5% with franking credits, which is pretty good. So only a small amount of selling is required anyway to get to 4%. I’d say just start building your portfolio in a way that you’re comfortable with and you’ll tweak it along the way as the picture becomes more clear in your mind. Hope that helps.