It’s time for my mid-year portfolio update.

Seems like ages since the last one back at the end of Feb!

So let’s peel back the curtain again and you can see what’s been happening behind the scenes.

There have been a couple of small changes to the portfolio since last time, which I’ll share with you.

I’ll also reveal my favourite chart which has just been freshly updated – our passive income for the financial year just ended. Let’s dive in.

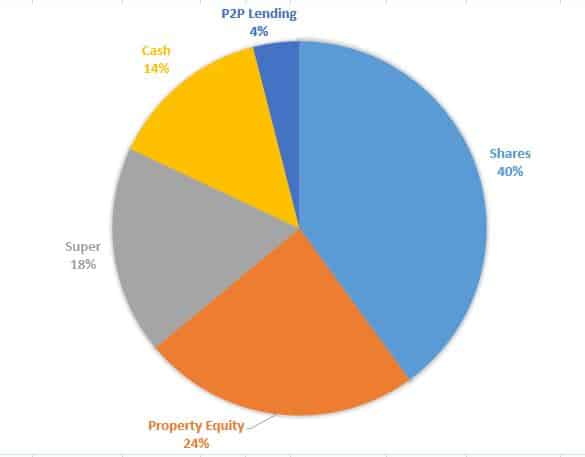

Below, you’ll see the latest breakdown of our net worth at the time of writing. Figures are in percentages rather than numbers for privacy reasons. I’m not anonymous like many bloggers and other than that, it’d just feel weird.

As flagged last time, I now include superannuation in these updates. I mentioned it previously and you all agreed it was a good idea. Thanks for your feedback on that!

Super wasn’t really part of our FI strategy, but it has continued to grow in value (and therefore importance), as part of our long term wealth, that will come in handy later.

Given this money won’t be touched for a good while, it will continue to become a bigger part of our net worth (and probably yours too!) over time.

What’s changed? Well, I marked down the value of a couple of our properties in Perth, after browsing similar properties for sale to get a feel for what they might sell for.

But the market value of our shares and super has also taken a hit. So all up, the allocation is quite similar to last time.

If you’re new here and wondering how we manage our cash in retirement, while transitioning from property to shares, this earlier update explains. You can also read about the transition strategy here.

My last update was right at the beginning of the coronavirus market crash. And that turned out to be a huge deal for basically everyone!

The economy was more or less shut down. Sadly, many people have died. While others started working (and doing everything else!) from home. It’s pretty clear that company earnings and dividends are getting hammered due to the sheer level of disruption from the shutdowns.

This means things could be looking sparse on the income side of things for the next year or two, while things slowly get back on track. We’ve never lived through anything like this, so it’s pretty crazy to watch it play out!

Having said that, it’s unlikely that the next 50 years has changed all that much from how it looked in January. Trends are still unfolding (perhaps accelerating), technology keeps evolving, and the world keeps turning.

While it’s far from ideal, there are plenty of positives we can choose to focus on too.

From my reading, residential property in Perth and Brisbane (where our remaining properties are located) was performing solidly until corona hit.

People have called a false Perth recovery for so many years I’ve lost count! While it’s early days, sales have picked up and now seem strong in Perth. I’ve also read that prices are starting to rise in parts of Brisbane. Irresistibly low mortgage rates will tend to do that 😉

From a rental perspective, the vacancy rate in Perth has been falling for years as building and investment has largely dried up. In fact, the vacancy rate has fallen from a peak of 5.5% in 2016, down to a low of 1.5% today, according to SQM Research.

That’s a huge drop and the lowest it’s been in more than 6 years. Rents now appear to be on the rise. Maybe we can claw back some of the steep losses from a few years ago!

As with most crises and fast-moving sharemarkets, there were opportunities available for those paying attention. I engaged in some behaviour which could be considered a bit naughty for a supposedly laid-back, do-nothing style investor.

You already know that LICs can trade at large premiums and discounts from time to time. Despite what some like to believe, LIC pricing is not always efficient.

I witnessed swings in premium/discount for the same LIC go from +12% premium and -8% discount, in just a week or two. And to be clear, no news was announced and nothing fundamental had changed with the company.

This happens in times when the market moves quickly. People are slow to account for this when buying LICs. I’d say that, right or wrong, it’s because many LIC buyers don’t even consider NTA versus the share price.

Anyway, these are the kinds of pricing differences I took advantage of. I trimmed some of our Argo holding (when it was trading at 12% premium to NTA) and topped up our Aussie index fund VAS.

Not because my view on Argo has changed. But because I could turn $1 of assets into $1.12 of assets by doing so. For basically no cost and no risk. This move means we own 12% more underlying shares than before (along with the earnings and dividends).

Differences this wide is typically not common with old LICs, which trade close to NTA (or within a few %) most of the time. By the way, my podcast partner Pat created a handy LIC Premium/Discount Estimator for a few of the popular LICs.

I also did the same thing with BKI, which was also trading at a huge premium. Except as part of simplifying our portfolio, I decided to exit it altogether.

This time, I used the funds to top up VAS, as well as Argo and Milton which were both trading at decent discounts by the time of purchase (5-8%). I chose to keep Argo and Milton over BKI as they both have a larger number of stocks in their portfolios (which I prefer), plus they’re internally managed.

There was no tax payable on these sales. Instead, there were losses which I can use to offset future capital gains. We ended up with roughly the same exposure, one less holding, and have increased our underlying ownership and future income stream by taking advantage of these price differences.

This isn’t something I agonise over, but if a large opportunity pops up, it can be worth making changes.

The record keeping would normally be a nightmare with this sort of thing. But I’ve been using Sharesight for the last 5 years, so all gains/losses for tax purposes are taken care of. If you’re not already using Sharesight, check it out here – it’s completely free for up to 10 holdings.

To be honest, if I didn’t use Sharesight, there’s almost no chance I would’ve taken advantage of the above opportunities. I’m just too lazy to spend my time calculating gains and losses on all the different parcels of shares! Haha!

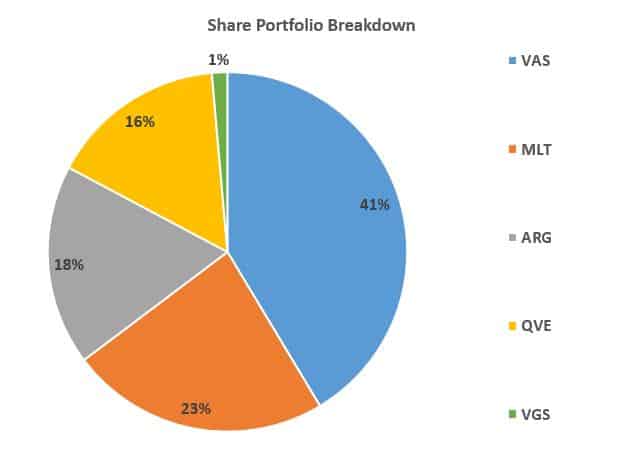

Here’s how the portfolio looks right now. You might notice a new addition 😉

Well well well, look what we have here! Yes, as mentioned recently, we’ve decided to add international shares to our portfolio earlier than planned.

We’ve chosen to do this with an index fund (VGS), as it’s a simple, highly diversified and low cost choice. We’ll steadily add to this over time, as with our other holdings.

There’s no mad rush to have it reach a certain percentage of our portfolio anytime soon. But you’ll see it slowly increase in size over time.

VAS is getting quite large these days, which is fine with me. Although as dividends fall this year, the effects are fully felt with an index fund, whereas the old LICs may be able to cushion the blow somewhat.

I’m half-expecting my LICs to have little change in their dividend payouts. But we’ll see what happens when they report their earnings in the next month or so.

In fact, QVE has already announced they’ll be paying the same dividend for the next 18 months, unless things meaningfully deteriorate further. As someone who enjoys a nice income stream, I won’t complain about that!

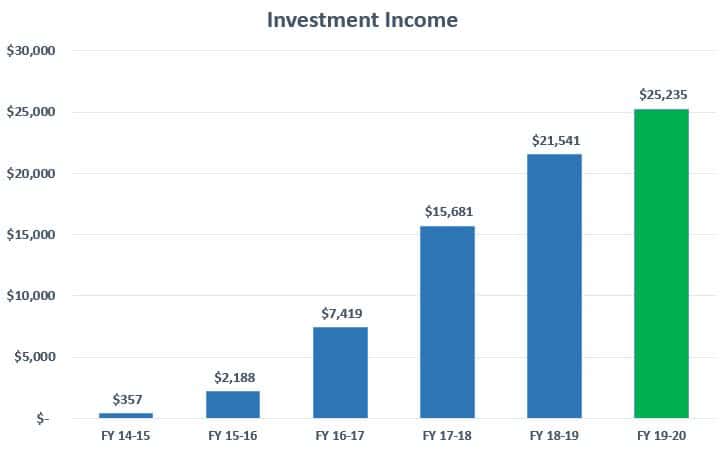

Below is the passive income stream received from investments for the most recent financial year. I just updated this the other day!

So you know, this chart includes franking credits and also includes interest earned from our peer-to-peer lending investment.

By the way, I created an easy-to-use spreadsheet to keep track of our portfolio. It gives me a running estimate of our annual income from investments after every purchase. You can download it free below…

Well, the portfolio’s income is still heading in the right direction. But something tells me this lovely trajectory won’t be sustained over the next year or two!

As mentioned previously, it will be slow going from here, since we’re now paying P&I on our remaining investment mortgages. We’ll still be adding to our shares each month or so, but less than in the past.

But instead of focusing on the negative, I’ll just sit back and enjoy the chart as it stands for now! 😀

Another positive is that, given our spending in 2019 was less than $40,000, this means our passive income of $25,000 gives us a ‘coverage ratio’ of over 60%. And as we steadily move more savings from property to shares, this will continue to increase and the two will overlap.

It’ll be fascinating to see how the next 12-18 months pans out. Honestly, I wouldn’t be surprised if our dividend income falls in the short term, despite adding to the portfolio. But we’re playing the long game here, so bumps in the road are expected from time to time.

Overall, the portfolio continues to move in a direction that we’re happy with – spitting out steadily increasing amounts of cash. I look forward to bringing you the next update, either late this year or early next year.

In the meantime, how’s your portfolio doing this year? Have you hit any passive income or net worth milestones? Share with me in the comments!

Note: If you choose a paid plan with Sharesight, this blog will earn a referral fee at no cost to you.

Why deliberate spending is my favourite money management style. What it really means and how you can use it as your situation and priorities change over time.

My thoughts on ‘The Great Taking’. An idea that the masses will lose untold amounts of wealth in the next financial crash, due to a deliberate plan by mysterious figures.

Get my latest content and thoughts straight to your inbox.

A fresh dose of financial motivation to power your journey.

That is a nice direction for investment income to go Dave!

Agree that the next 2 years or so might be an interesting path to follow on dividends especially, but as you say the longer-term historical trends still suggest equity investments will eventually be rewarded.

I’m curious, is it right that that would mean the P2P income is around 4% of your investment income, or slightly more or less? The income in that area is looking increasingly capped, if Ratesetter is any guide…

P2P would be more than 4% of that investment income, though it will be reducing over time as I simply let the repayments come in and don’t reinvest. As you say, the income (and therefore returns) are now much lower than a few years ago and I’m not sure how I feel about Ratesetter placing an upper limit on rates, considering it’s supposed to be market-driven between lenders/borrowers. Do you have a view on that?

Fair enough, thanks for the reply.

Yes, I definitely have a view. I think it’s a departure from the model of peer to peer lending. It’s something quite different if there is to be some arbitrary mediation of what lenders and borrowers can agree. No doubt there are risk or reputational reasons driving it, but it is not quite the same product as launched.

Thanks for your view. Yeah it’s certainly strange and not what it is ‘supposed’ to be. Pros and cons to the change I suppose, but I wasn’t sold on it when I heard.

It’s probably got something to do with their plans to go public as I have read they are going to list on the ASX later this year or early next year!

Great decision to add international shares via VGS to your portfolio. I think many trying to FIRE focus solely on dividends from Australian focused LICs and ETFs, forgetting that Australia makes up just 2% of global markets. There are certainly some well diversified ETFs and CEFs (closed end funds similar to LICs in the US) that pay good dividend yields and perhaps offer better growth opportunities as as well. For simplicity VGS is a goody choice and buying now while global markets are down should prove a shrewd move. Be good to see how quickly it increases percentage wise in your portfolio moving forward.

Thanks Jason. It’ll be a steady increase over time. As mentioned in the post, no mad rush. I’d prefer it if global markets were lower but that’s okay 😉

VAS latest dividend payout was terrible, BKI was decent, both Argo and Milton didnt hold up that well IMO during the crash and I’m hoping they can sustain their dividend .

Apart from the supermarkets and utilities nothing regarded as defensive performed that well .

I wasn’t really expecting LICs to hold up from a value perspective, but they should be able to avoid large dividend cuts. You’re right, it’s a strange time with some unusual outcomes for companies so far. Let’s see what the next 12 months brings!

Hey Dave, thanks for the update.

The investment income graph looks really nice, slow and steady increase in passive income.

I just had a question regarding BKI. Aside from the process of simplification, were there other specific reason’s for you disposing of it? I’ve been on the fence with deciding what to do with my holdings, many people I know have disposed of them citing various reason’s.. the move the external management, the capital raising in 2018, etc.

In the end I decided to maintain my position as a small portion of the portfolio at 15%. The full-year results were released yesterday, along with the dividend announcement which was a reduction in the underlying dividends (as expected) however a special dividend mostly made up for the shortfall.

Interested to see where AFI and MLT stand in the coming weeks, especially after VAS’s latest distribution.

Cheers.

Cheers Scott. On BKI, nah not really mate. It really was wanting to reduce the number of similar holdings and I prefer the others. Having less holdings is making tax time so much easier!

As you referred to, BKI have made some questionable moves in the last couple of years, but I think they’ll still do fine long term. They’ve had a high payout for a few years now so a dividend cut was hard to avoid. The others are in a better place on that front, but we’ll see what happens 🙂

We’ll be getting our first BKI dividend soon – it was our first purchase on this journey so we’re very excited! Slightly disappointed that they weren’t able to maintain the dividend payout, but not unexpected in the middle of a once-in-one-hundred-years global pandemic! Was happy to see the special dividend almost make up for the shortfall anyway.

Very interested to see how MLT and ARG go soon. We hold one but not the other (yet) but it’s probably our next planned purchase.

Yes I was quite shocked at just how paltry the recent VAS payout was. My other holding is AFI (approx 50:50 with VAS) so it will be interesting to compare the AFI divvie payout next month. Still, we are living through a pandemic that has temporarily halted economies so perhaps not too surprising.

Asbolutely Jeff. This quarter’s payout was effected because it was when a few of the big banks pay. So with a large cut from NAB and Westpac and ANZ choosing to defer their dividends (which really means pay zero lol), that was the chief cause I believe. Will be interested to see the next year or two’s worth of distributions so we can see the real effects.

Haha yeah, putting the economy into the freezer for a while certainly has its consequences. I have a feeling AFIC will maintain their normal payout or very close to (they certainly have enough reserves and excess franking, from memory).

Great update! I find it super interesting that even after hitting FI you’re still changing your asset allocation! I love that! Did you initially add LIC’s into the mix to help soften the blow of any dividend and market fluctuations?

Thanks mate. We really have no choice but to change our assets over time, because our properties provide zero income (even paid off they’d be pretty poor at producing cashflow). LICs were chosen because our focus is creating investment income and mostly to just live off the dividends from shares. Low cost old LICs suit this choice, but I also like index funds these days too.

Hey Dave,

Love the blog, it is one of my must reads.

My 2 cents, for what its worth, on your asset allocation graph: Showing the gross value of the property assets is more meaningful than the ‘equity’ value. If your objective is to see what exposures you have to different asset classes, its the gross value that shows the accurate picture.

Keep up the good work.

Mike

Thanks Mike! You make a good point and that would be a more correct way to show total ‘exposure’. But for our purposes here, I’m really trying to display where our savings/equity is tied up (especially since we’re transitioning over time) and using the ‘net’ amount suits that better.

Off the subject a little perhaps Dave, what can you tell me about Self Wealth? Do you use them and are they reliable? Is your money safe with them? I have been trading through Bendigo Bank and since I like to make relatively small purchases like $600 of some small caps I’m interested in and the like, I am starting to rather object to paying $20 per trade. Also would you say that BKI is still a quality company as I bought them partly because you had obviously had faith in them in the past? love your blog mate great work.

I find Selfwealth to be reliable James. They’re a low cost broker to trade shares with. Your money isn’t ‘with them’ they’re simply a platform to buy and sell on. Your money gets invested into whatever fund/shares you’re buying. Your holdings are CHESS sponsored so your ownership is recorded with the stock exchange like most other brokers – https://help.selfwealth.com.au/hc/en-au/articles/360030950631-What-is-CHESS-and-CHESS-Sponsorship-

I definitely wouldn’t be paying $20 for every $600 purchase, that’s way too much. So I’d either buy in larger amounts or switch brokers. On BKI, for what it’s worth, I do still think BKI are a decent option as a low cost Aussie LIC.

Cheers Dave thanks for the feedback.

Hi mate,

Interested to know why you chose VGS over a VTS and VEU combo? I’ve done quite a bit of research on the pros and cons of each so I understand the factors there but still slightly surprised with your decision as the finance bloggers or hard-core FIRE guys tend to go with the latter. Cheers.

Hey Ian. Both are perfectly fine ways to do it of course. I chose VGS as it’s one holding versus two, it’s diversification is ‘good enough’ for my purposes, and I don’t like the uncertainty of the tax treatment of the US domiciled funds. If Vanguard locally domicile VTS/VEU or create an ‘All World ex Australia’ fund, then I might consider using that instead. But for now, VGS is good enough. The higher fee doesn’t bother me as it’s still very low and index fees will eventually end up close to zero anyway.

Hi Dave

Loved the update and congrats on the rising passive income. I wanted to explore your thoughts on breaking the rules of dollar cost averaging.

Current VAS price at 77 dollars is still 15% down from its all time pre -Covid high. Generally, if something is for sale at 15% off, there should be a buying frenzy. We cannot predict the future but I was wondering given the dismal short to medium term economic outlook – high unemployment, loan deferrals, likely corporate failures, whether it is better to hold onto more cash and splurge more when VAS dips again more than usual. This is timing the market but I have a view that this may be a better way to go in current circumstances. I think if someone had DCA into VAS for 12 months pre Covid, it will be a long time before they reach their average entry price whilst also suffering the lowest VAS dividend payouts in the history of VAS. Interested in your thoughts.

Hey Ken. Nobody can tell you how to invest, so if that’s what you want to do then feel free. There’s no point me trying to talk you out of it because you’ll always feel like you should’ve ‘gone with your gut’ anyway.

I will say there is absolutely ZERO value or point in looking at past prices paid for parcels of shares. Somebody who bought VAS in 2010 does not receive better returns from here compared to someone who bought in 2019. Therefore the time we bought in the past is irrelevant when making investment decisions today. This is called anchoring and it’s a dangerous way to think about any investment. All we have is today and the future. If you still think shares are a good long term bet (20-50 years) then it’s worth buying, if not, then make other plans.

Read my post on timing the market again. Playing this game probably won’t be as easy as you think 🙂

Hi Dave,

Thanks for sharing this update. You are saying that your passive income from investments covers 60% of your annual spending and also, that your properties are not generating any income. May I ask how you cover the remaining 40% of your expenses, given you consider yourself retired?

Cheers,

Matt.

It’s explained in the previous updates I linked to in the post. How we manage our cash is mentioned in this update, and our transition strategy to live off assets while transitioning from property to shares is here. Hope that helps.

Keep these updates coming mate, love these ones!

We sold a property last year and have been phasing cash into the market gradually with a big loading up in March. We track everything by passive income and use the previous year dividend and just keep updating unit quantities.

We hit 25% of our annual expenses covered this week so was a nice win. We make sure we take time to celebrate these milestones as they don’t come around too regular…

Hope to be fully invested by end of this year which will put us at 35%-40%

Love tracking it this way so thanks for the post a year or two ago that advised it!

Awesome stuff Paul, great to hear it! Sounds like a familiar approach 😉 Well done on your progress, and thanks for sharing.

Hi Dave,

Can you clarify something? How can you say you have reached FIRE when your expenses are 40k and your passive income is 25k? Where do the remaining 15k come from? You work for them therefore you are not FIRE?

Dude, I literally just answered this question to another person. Check the other comments. It has been asked and answered multiple times now. We use cash from a property sale while we continue to buy shares (kinda like when ppl sell down their shares to live off over time) is the super-short answer.

Another great report – love reading how your portfolio is performing and changing. Especially love the passive income graph – that’s awesome!

One question though – I’m very confused as to the logic behind selling an LIC simply because it’s trading at a premium to the NTA if the sale still results in an overall loss to you. I don’t understand how that improves your portfolio, returns or gets you closer to your goals. I’m hoping you can explain this a bit further so I can understand. Thanks!

Hey Miranda. Well, if an LIC is trading at $1.10 per share, but it has a portfolio worth $1, then it’s trading at roughly a 10% premium to its NTA (the value of its assets). If you sell this asset for $1.10 and use it to buy something else which costs $1.10 which also has $1.10 of assets, then you have increased your underlying asset base by 10%. The tricky part is, the actual VALUE of the shares you own in each case are the same. But you now get access to a larger asset base because the underlying asset base you own is worth more, so you therefore are earning returns and dividends from the increased asset base.

What you bought the first LIC only matters as far as capital gains tax is concerned. I hope I haven’t confused you further haha! There’s no need to do any of this of course. Just a pricing difference I decided to take advantage of.

Thank you for that explanation Dave. It kinda makes sense in one way, but still kinda doesn’t in another so I won’t worry about it. I don’t really intend to sell anyway – I was more curious as to the logic behind it.

Hi Miranda, I’ve also had trouble with this. I tend to have to sit with things like this for a while to wrap my head around it. So, don’t laugh, but I was eating an orange, so I used an orange as my “LIC”. Here goes.

1 orange has 10 slices. Each slice is worth a $1.

Some how I bought an orange with 9 slices (One slice missing), but I still bought it for $10.

An opportunity came up to buy a full orange (10 slices) for $10.

So I sold my 9 slice orange for $10 and bought the 10 slice orange for $10.

Effectively adding an extra slice to my “orange” holdings, with no extra cost.

Except if capital gains/loss come into play.

In Dave’s case he sold his orange for $9, losing one dollar.

But he’s using that $1 loss to deduct from any profits he makes in the future, to pay less tax.

I hope this makes sense.

Or that you didn’t understand this already 😀

Or that I didn’t over simplify this, works for me though 🙂

Dave correct me if I’ve got the wrong end of the stick.

Nicely done Chris. I hadn’t thought of it quite like that, but seems like a great (and nutritious) example 😉

Thanks Chris – that’s in interesting way of thinking about it! I guess the thing that confuses me is that sometimes the original orange has 10 segments and then for some reason at other times it only has 9, and at other times it might have 11. It’s still just the same orange though, which can be bought/sold for $10, regardless of how many slices it happens to contain at any given point in time.

I can kinda see that underlying value of the assets owned has technically increased in Dave’s example here, but I can’t see how that will create extra income for him in the future to offset his capital loss. I can also see a case for just holding on to what you have rather than crystallising a capital loss for a theoretical future gain.

Maybe I’ll just stick to the basics of buy and hold, since I don’t yet understand the full impact of Dave’s strategy here. I’ll keep thinking and trying to understand. It’s always interesting to learn new things 🙂

Miranda, because the underlying assets have increased – by definition that means you own more income producing assets (given the holdings are broadly very similar). Also, the future tax benefit is not theoretical it is very real, and is a tangible secondary benefit. Lastly, the price of the orange is dictated by the market and can be more popular at times and less popular at other times, even with the same underlying slices. So ppl can take advantage of this discrepancy if they’re watching.

Also, the capital loss has already happened, by holding on to one asset versus another, just because it’s your original one (assuming they’re similar), you’re no better off. If both assets go up at the same rate, then buying the one that is cheaper (or with more underlying orange slices lol) makes sense. That’s probably enough explanations.

Actually I wrote a whole post on LIC premiums and discounts which you can find here (if you haven’t already seen it) – A Complete Guide to LIC Premiums and Discounts

Very interesting to see your breakdown. I’ve never done it before but gave it a burl. Buggered if I know how to go about the passive income graph. But at this stage I’m not earning enough to bother. But chucking $10k every five weeks into shares (except when the missus decides to do up the kids’ bathroom) so hopefully that snowballs quickly and I will.

Current Portfolio

Property – 48% (that’s just our residence which we just paid off)

Shares – 11%

Superannuation – 32%

Cash – 9%

Share Portfolio Breakdown

DJRE – 4%

IAF – 2%

IFRA – 4.5%

STW – 16%

VGAD – 6.5%

VGE – 5%

VGS – 9.5%

AFIC – 20.5%

WHF – 32%

The ETFs are all invested by Six Park. I’m seriously thinking of pulling them and running those myself. The only benefit I can see with retaining Six Park is the diversity and hands off the wheel with re-balancing. Paying fees for the sake of it there. And the two LICs are bought using Self Wealth. WHF is looking a bit top heavy there but Thornhill would approve.

Hi Dave,

Thanks for sharing all this great info! Your blog has given me some good grounding for getting into the Aussie share market and more. My wife and I (she’s Aussie) are on our way back to Australia, so I’ve started the process of moving our investments from South Africa to Australia. This blog has been gol-den.

Shares

– I’m slowly migrating about $150k mostly into LICs and ETFs: ARG, MLT, WHF, BKI, VAS, IOO.

– I bought PL8 and FANG on a recommendation.

– I’ve also had recommendations for MGE, MICH, WAM, WMI, WLE, AASF.

– I’m weary of their management and performance fees.

– Growth (MGE) and dividends (WAM) seem really good, but how do they compare after fees are deducted…

– I like that some of them are less heavy in banks.

– I am after some amount of decent dividends, so that makes some options less attractive to me.

Setup

– I use Commsec, mainly because I didn’t know any better at the time.

– To mitigate their $29.99 fee, I buy parcels of at least $3000 at a time, making the fee come to 1%.

– I’ve signed up with Share-Sight, which is amazing.

– The next fun part is figuring Tax basics and Supers.

Cheers from chilly Cape Town,

Chris

Hi Dave,

Thanks for sharing, I find your posts cut through the rubbish and noise.

Currently we hold in value order –

QVE, WHF, PMC, MIR, MLT, ARG, BKI, WIC

I have found both QVE and PMC at more than a 10% Discount to NTA hard to resist over the past 6 months or so.

Again thank you for sharing.

Regards

Dangerous Dave