Welcome to the new readers joining us in 2022!

The Strong Money community is full of thoughtful people who are passionate about financial independence.

Join us as we try to become a little wiser and wealthier each week:

Firstly, if I haven’t spoken to you before this article, Happy New Year!

I hope everyone’s feeling well rested and ready to get back into the swing of things 🙂

What better way to start the year than to review our spending from last year to see how we’re tracking! I encourage you to do the same at home… you DO know how much you’re spending, right?

I started these spending ‘reveals’ so you can see what’s happening behind the scenes, that I’m ‘walking the talk’ of frugality (at least to some degree), and so you can see how we’re spending our money in early retirement, while managing to enjoy life without spending a fortune.

Before we get into the spending report, I’ll provide a short re-cap of our current situation for those who are new to the Strong Money blog.

Here’s some context around the numbers you’re about to see.

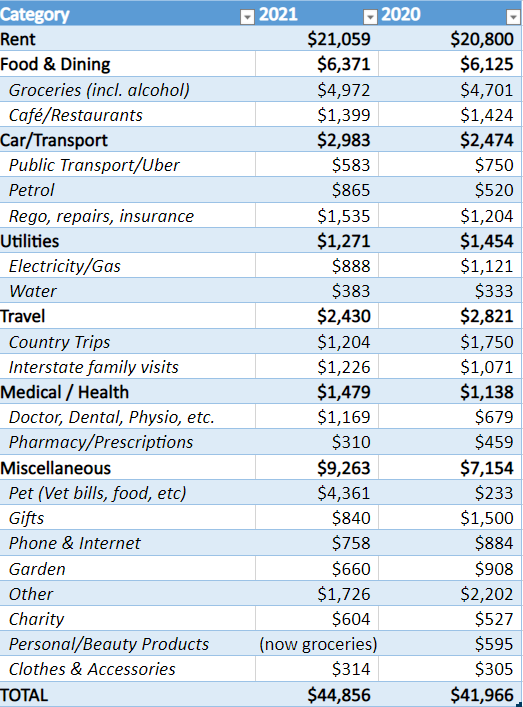

With all that said, let’s get into the numbers. In our previous spending report, I revealed that our total for 2020 was $41,966. So how did we go in 2021?

Below you’ll see a complete breakdown of every category of spending comparing both years.

The total bill in 2021 for running the Strong Money household came to $44,856. So an increase over the prior year ($41,966), but not a huge blowout.

By the way, I don’t have a ‘target’ or a budget for our spending. Think of it like a rolling financial documentary I’m watching unfold and simply taking notes from!

Of course, we’re mostly in control of what happens in this particular documentary, but I’m not delicately scripting this shit out! We just buy what we need and whatever we feel is worthwhile 🙂

So, we somehow managed to live another satisfying year without the bill blowing out to $100,000!

For some people, it might sound like we’re living in some parallel universe, but the things we enjoy spending our time on happen to not cost very much. And no, the cost of living in Perth (aside from housing) is hardly different from the eastern states.

Alright, onto the area-specific comments to share a few more details!

If you strip out the vet bill, our spending was pretty similar to last year. Some things rose, others fell.

While I haven’t recorded every single year, our spending has been roughly this level for the last 7-8 years now, with basically zero effort.

Not only that, but I could think of at least 10 ways it could still be lower, should we ever need to flex our frugality muscles. So even if certain costs rise, or we decide to spend more in a few areas, this could easily be offset with savings elsewhere.

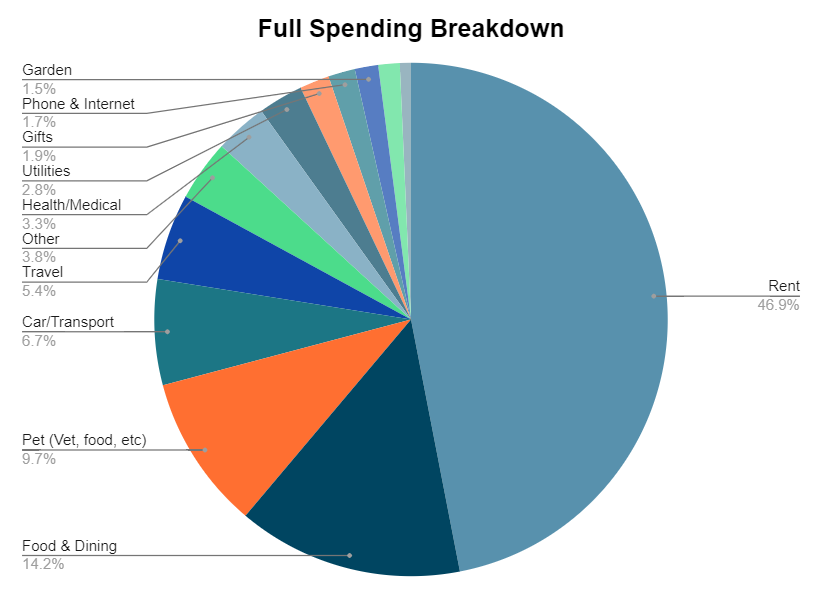

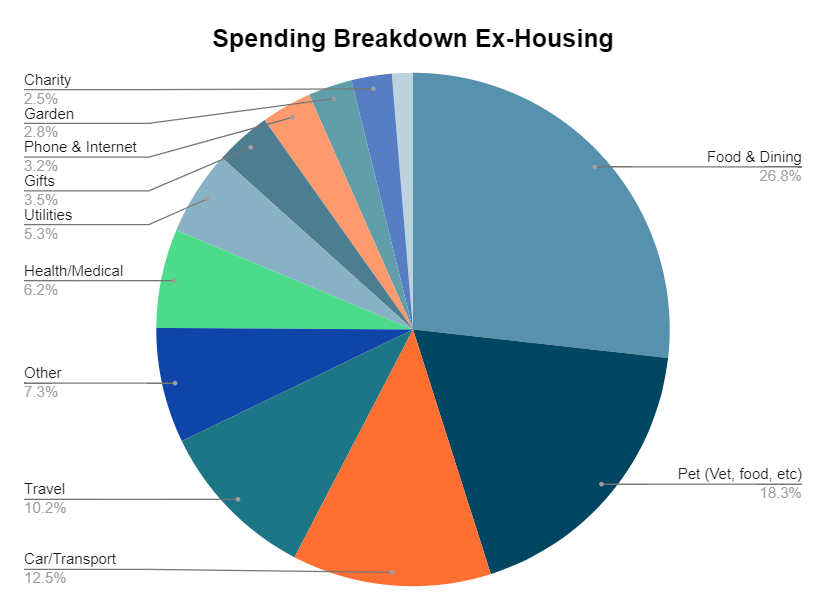

Housing looks ridiculous as a percentage of our spending. It really skews the chart, which is why I’ve also included the second one!

Guilty admission: I did absolutely none of this tracking on my FI journey. I simply used rough guesstimates, which later turned out to be fairly accurate.

The reason we ‘got away’ with this is because we adopted the habit of mindful spending. Think 50% Dalai Lama, 50% Scrooge McDuck 😉

Mindful spending is just a fancy way to say think about your spending before you do it, including lifestyle habits, rather than the compulsive, automatic or reactionary behaviour that most people operate with.

Self-questioning doesn’t sound very sexy, but it’s surprisingly effective!

After these updates, I always get questions around certain spending topics, so I’ll link a few pieces of content here if you want to dive deeper into what I’ve written about those subjects (and spending in general) in the past:

None of this is an instruction or expectation on my part of how you should spend your money. It’s simply to be open about how we spend ours.

In doing so, hopefully it inspires a few people to realise that a good life in Australia doesn’t have to cost an arm and a leg.

The new year is a great time to reflect on things and figure out what we can do better for the coming 12 months. We get to mentally reset and enjoy a fresh start.

That gives us a fantastic opportunity to examine our finances to see where we can optimise going forward. And when you do that each year, you may find that as your life improves and your wealth expands, your spending barely moves or even goes down over time!

Have you thought of how you might improve your spending this year? Did you meet your savings goals last in 2021? Share in the comments!

Recommendation: A shitty interest rate can cost you thousands in unnecessary interest. So an easy win to start the year could be getting a better mortgage rate.

Negotiate with your bank to see what they’ll do for you. Alternatively, check out my personal mortgage broker – More Than Mortgages – if you want someone to do the shopping around for you.

Note – if you end up getting a loan through MTM, this blog may earn a small referral fee. I only recommend things I use myself and genuinely approve of.

Why deliberate spending is my favourite money management style. What it really means and how you can use it as your situation and priorities change over time.

My thoughts on ‘The Great Taking’. An idea that the masses will lose untold amounts of wealth in the next financial crash, due to a deliberate plan by mysterious figures.

Get my latest content and thoughts straight to your inbox.

A fresh dose of financial motivation to power your journey.

“And no, the cost of living in Perth (aside from housing) is hardly different from the eastern states.”

Not sure where in the Eastern States I can rent a decent house in a good neighbourhood for $400 a week in SYD, MEL or now even BNE??

I’m impressed with your restaurant spending – only $100 per month?!

Thanks for posting.

Are you guys going to have kids?

Also (sorry, I can’t help myself): wait until you have kids! ????

That’s why I said ‘aside from housing’ 😉 We definitely have an advantage here in terms of housing affordability, no doubt about it. But even still, add another $10k per year and our spending is still at a reasonable level.

Nah definitely no kids. Haha, I think kids are another one of life’s expenses that people either make insanely high, or reasonably modest depending on their own personal decisions. I’ve had several parents reach out and tell me as much… one even wrote a guest-post for this blog on raising kids without the costs blowing out. I’ll leave it here in case anyone’s interested: Financial Independence With A Family

Without kids, my spending is $30,000 a year…with kids, it can be anything between $100K – $200K…..

That’s pretty good for personal spending. Haha, with kids… well, that’s your choice I guess, but it doesn’t have to be that way.

Seems like you are doing parenting wrong

Nice one! My spending alone in 2021 was $47,611. Highest expense was rent, but also included buying a motorbike (6k) ???? still achieved a savings rate of 41.8% though so I’m happy! I didn’t see your savings rate in your post, but who cares if you’re retired right? ???? goals.

Very nice work mate! That’s a pretty solid savings rate, even with the bike purchase so that’s great 🙂

I don’t calculate our savings rate anymore, and in any case, our finances are pretty messy given we still have properties with large mortgage repayments. As you say, given we’re in retirement mode it doesn’t really matter anyway… there doesn’t need to be a savings rate lol.

That’s great Dave!

Our solar system is 1 year old last month and has been worth every cent. It is so good getting a credit instead of a bill every quarter

Time for a post on Mrs SMAs veggie garden perhaps??

Ohh that’s fantastic Phil! Awesome to hear you’re now living in the land of power credits instead of power bills!

The garden post is a good idea, we’ve been collecting a few pictures of the various things on the go. Will have to check if we’ve got enough to put a post together 🙂

I hear you on the vet bill. My Scout did a similar thing a few years ago and having the surgery saved her life. Best $2,300 I’ve ever spent.

Oh of course, non-negotiable! 🙂

Nice work Dave! It actually looks fairly similar to our spending on a like for like basis and adjusting for household size, we just have some extra expenses like insurances, stuff for the kids, rates etc. I think it shows that people definitely can spend a lot less and still have a pretty good life, particularly once the mortgage is paid off given that’s the biggest expense for most people.

Thanks mate! Yeah absolutely! The mortgage is a huge weight off people’s shoulders and even that in itself makes something like semi-retirement very doable. Are you planning to get rid of your mortgage or keep it ticking away? We’re not dealing with that yet, but I like both options (maximising investments/having no house payment).

I think the mortgage is about one third of people’s spending, so yep absolutely massive. We don’t actually have a mortgage ourselves, I meant it’s an issue for lot of other people.

Oh wow, you’ve already solved that issue then 😉 Yeah I find the same, even up to 50% in many cases – a huge chunk of expenses.

Thanks so much for the post Dave, I really appreciate you sharing this information, great to have something to compare against and really question if everything purchased really is a need or merely a want in disguise! There is always room for improvement on our end:)

Cheers Cindy, glad you enjoy these posts! We can always improve, me included. And it’s not even about spending the least amount of money, it’s making sure what we’re spending on is really worth it after considering alternative options.

Good to see that living off 40K+ is achievable. It’s pretty much what we’re aiming for.

A small tip for saving is that you can get the “libby” app for books and audiobook for free using you library card.

You can also get “Kanopy” and “Beama” that are both film streaming services with your library card as well.

Anyway, great post and I really enjoy your blog and podcast.

Cheers Gabe, great tips. We’re big fans of the library and use it regularly!

If you think Aussie Broadband is cheap you should look at Flip TV! I am no promoter of them. They’re just my ISP.

Cheers for the tip Darren! Aussie broadband certainly aren’t the cheapest option, but they’ve been super reliable. I’ve heard some less favourable experiences with some of the slightly cheaper providers, but not sure how many that applies to.

Hey Dave,

That’s brilliant! It’s so refreshing to see this – I love my spend sheet, with yearly totals, monthly averages, and of course, graphs :-).

I split mine in to different categories:

– Fixed (costs which appear no matter what – mortgage, rates, strata, other bills)

– Essentials (groceries, transport, clothing, etc)

– Extras (entertainment, eating out, etc)

Basically, to work out how much I need to just live, versus how much I need for the lifestyle I’m looking for!

Happy to say, the FIRE journey might be starting quite soon, though still keeping my options open for some contract work. Next few months is looking promising!

Thanks for the inspiration!

Haha, wow you really do love it! 😉

I really like that you separate the basics from luxuries, I think that’s a really healthy way to approach it. Then we can better examine what’s really optional and question whether it’s really benefiting us or not. And great to hear about your rapidly approaching freedom date!

Hi Dave, thanks for post – great update. Your water category seems low to me. I see a comparable cost for water usage alone but then there are wastewater charges of about $800 per year (NSW). Might those be included in your rent? Cheers, Stephan.

I think it’s probably because you own your home? When renting you only need to pay for actual water usage, which is incredibly cheap. Water rates as an owner is the big cost, far more than usage. Our investment properties are the same – we pay $200-$250 every 2 months, and then there’s usually about $20-$60 for water usage, which the tenant needs to pay.

Hi,

I read your blog before moving to Australia, but reread this after I’m here. The groceries is really good for less than 5k a year! It’s impressive.

Cheers! Yeah it’s definitely doable 🙂 Each little choice we make adds up to a pretty big difference, just like our finances as a whole.