Welcome to the 413 new readers who’ve joined us since December!

The Strong Money community is full of thoughtful people who are passionate about financial independence.

Join us as we try to become a little wiser and wealthier each week:

It’s the end of January already, and we’re now well and thoroughly into 2023.

About now is when most people give up on their new year’s resolution and go back to life as normal, forgetting they ever had the idea to eat better/make more money/start investing/etc 😅

But this post isn’t about the new year. It’s about last year, and our personal spending.

As usual, I’ll unpack our household expenses for you all to see.

It’s not intended to be an example of what everyone should do. Rather, I share these details because I know how many readers love to see what others in this space are doing their own money.

But before we begin, I’ll give a brief explainer of our situation to give some more context for what you’re about to see.

Okay, with all that said, let’s get into the numbers.

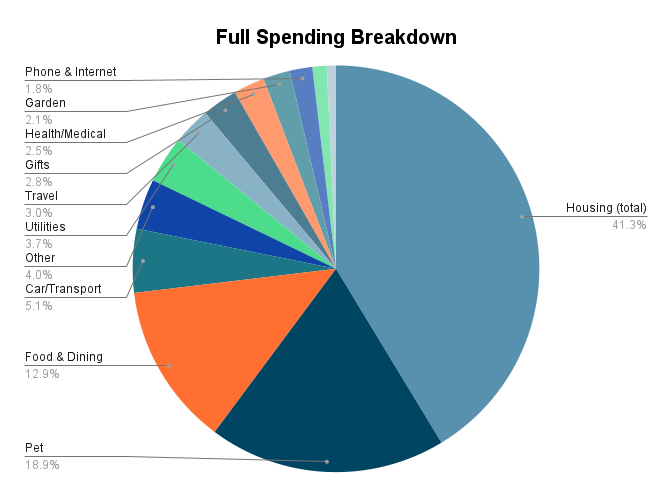

In our previous spending report, I revealed that our total for 2021 was $44,856. So how did we go in 2022?

Whoa… this turned out to be a pretty expensive year!

Overall, it definitely felt like we were just doing whatever the hell we wanted the whole time.

It looks like a huge blowout at first. But when you take away $10,000 of cancer treatment for our dog (including a small surgery), our spending was basically the same as last year. Some categories went up, some went down.

And just so you know, we also spent around $10,000 renovating our 50 year old bathroom! You can see the pics in this post.

But I don’t count renovation costs as part of our annual spending, because they were planned, expected and most importantly, built into our home-buying numbers and the decision around that.

Anything that’s not part of that will be included under the housing costs category, like any maintenance, repairs or minor improvements.

You might recall I also didn’t count the car purchase as an annual expense a few years back. I find this to be a more accurate view of household spending. Just as I wouldn’t say we made $10,000 of income if we sold it.

Now here’s a few more details and comments (excuses?) around certain categories so you get a better grasp on the numbers 😉

Rent/Mortgage: Interest rates are way up from when we moved in, so I expect our interest bill to be bigger next year. Luckily, this entire loan is tax-deductible as we bought the house with cash. More details on that here. I’ll still record the interest here as part of our household expenses, just because it would seem strange if I didn’t.

Housing costs: This includes council rates, insurance, and things like various repairs, along with some plumbing and electrical work that needed doing.

Groceries/Cafes: We take advantage of Flybuys Bonus points offers on a regular basis (eg. spend $50/week for 4 weeks, get 10,000 points, equal to $50). These are gold! We also get our groceries mostly delivered, saving time and cutting our driving and impulse buying (prices are generally the same). We also get a bit of fresh produce from our own garden as well as the community garden near our house that Mrs SMA volunteers at. Our café/restaurant spending continued its relentless rise upwards… pretty sure it’s tripled since we retired! 😅

Car/Transport: Mrs SMA drove to work more this year rather than getting public transport. Mostly because it saves her time and is less hassle, but partly because she has to carry a bunch of stuff in with her sometimes.

Utilities: We’ve now got a nice amount of electricity credit thanks to the WA government. Funny story: we actually ended up with triple the credits, since we had 3 electricity accounts opened at the time it happened. One for our rental, our newly purchase home we hadn’t moved into yet, and an investment property we were selling. It was purely by coincidence and I was sure the credits wouldn’t transfer once we closed the other accounts, but they did! Water went up because we’re no longer renting. In case you weren’t aware, water usage is insanely cheap, but water rates are expensive. The owner pays a hefty amount for the connection and maintenance of that water supply/infrastructure.

Other: This includes all sorts like electronics, appliances, random spending, things for the house, etc. This year we got a fancy new cordless stick vacuum which is surprisingly fun to use 😁 We also got a new washing machine, sofa bed, pullup bar, 2 sets of table/chairs, and a new phone (second hand) off Facebook marketplace.

Phone/Internet: Both on Catch Connect for roughly $100/year, which I’ve found has been faster and more reliable than our old cheap provider Kogan. Our internet is Aussie Broadband which we’ve been with for a couple of years, and our current $65/month plan is more than enough for us.

Travel: No country trips this year as we got a little bit too busy with regular life. First, moving into our new house and getting settled. Mrs SMA then spent a lot of time planning out her gardens. Then I didn’t want to be away during turtle hatching (and later, laying) season. And of course, the book took up a decent chunk of time. But we both did family trips, and we’re currently planning a trip at the moment somewhere in south-west WA. We’ll do our normal thing and rent a pet-friendly house 🙂

Gifts: We splashed out a bit more than we normally do on gifts this year for each other, and then we had some relatives stay with us for Christmas which meant more presents and spending in general. By the way, I have no magic formular for dealing with birthdays and special occasions. I just try to shift the focus away from buying each other shit we don’t need, and more towards spending time together or doing something nice.

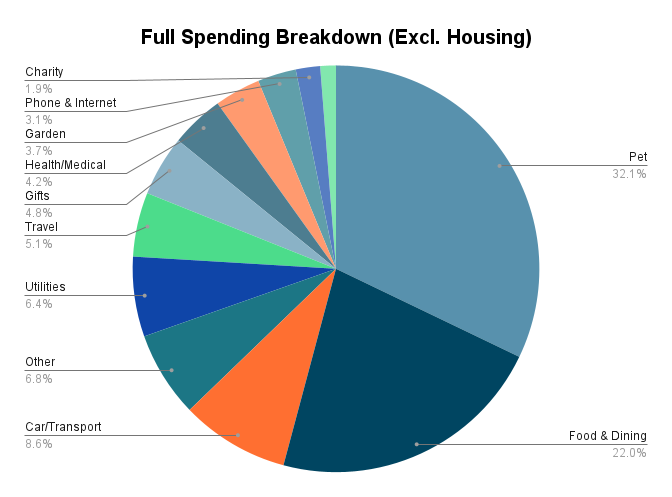

Given housing is typically everyone’s biggest expense, removing it for a minute can give you a much better glimpse of where the rest of your money is going.

Even here, the Pet category is throwing things out a bit. Aside from housing and food, our money is essentially spent in bits and pieces in lots of different places. Few thousand here, few thousand there.

I should point out something: we could easily reduce most of these categories if the need arose.

In fact, if we were still working full-time and trying to reach FI, there’s no way in hell I’d be satisfied such sloppy spending. I would be optimising the shit out of it!

I don’t use the term ‘sloppy’ to suggest it’s a high level of spending. What I mean is how little thought and effort goes into our personal spending these days 😂

Maybe in a future post I’ll flesh out how I’d approach our income and expenses in a ‘start from scratch’ scenario. Let me know if you’d find that interesting and I’ll bump it up the ideas list!

By the way, I don’t use any fancy software to track my spending. Just a very simple spreadsheet with categories on one side and months across the other. One day each week I take 5 minutes to check bank transactions and add them to the tally for whatever category they fit in.

I have recently been playing around with a spending tracker that Pearler is building. It’s actually coming along quite well and I can see myself using that instead of my spreadsheet sooner or later.

Gazing into my crystal ball, it’s unlikely our spending is this high in 2023.

Our dog won’t be going through another round of chemo. He’s actually had a small lump on his foot regrow, so he’s on some special tablets now. But we opted against more surgery or chemo.

He’s very happy, and there’s no guarantee more surgery or chemo will do much. And then he’d end up on these tablets anyway. So we chose not to put him through that. These tablets do seem to be working though, with the lump steadily disappearing in the first two weeks, so that’s a good sign.

Our housing costs will go up with increasing interest rates. We’ll also do at least one country trip this year, maybe two if we are organised enough!

We’ll probably spend a bit more money on the house too. Solar panels are on the cards (after our electricity credits run out), and we might get some work done on the exterior of the house. Hmm, maybe it’ll be a more expensive year than I thought!

By the way, if you’re reading this and hungry for savings ideas, check out my content on the following categories: Holidays. Cars. Food. Phones. Fitness. Fun. And of course, Housing (this article, and this podcast).

Our spending may look high, low, or ‘about right’, depending on who you are and your own personal situation and tastes.

But therein lies an important point: there’s no set amount of spending which magically creates a happy life. A good life is made not bought.

This also means there’s no set amount for what you need to retire. It’s all personal choice.

It depends what you focus on, how you want to spend your time, and how you measure your existence. You can have a happy (or miserable) high spending retirement, or a happy (or miserable) low spending retirement. And there’s no rule that says you can’t switch from one to another at any time you like.

I know I’ve said all that before, but it’s worth repeating. For some reason – probably clever advertising, lack of examples, and strongly held beliefs often created by advertising itself – we find that hard to believe.

Anyway, this is how we’re choosing to spend OUR retirement. And that may change in any given year. Which is the fantastic part of all this – being able to change anything at any time because your priorities change.

How was your spending in 2022 compared to the year before? Did inflation have much effect, or did you manage to keep things steady? Let me know in the comments.

Mortgages: Interest rates have moved up a lot since this time last year. So it’s worth looking around to see if you’re still getting a decent deal.

Negotiate with your bank to see what they’ll do for you. Alternatively, check out my personal mortgage broker – More Than Mortgages – if you want someone to shop around for you or to help with anything home loan related.

So you know, if you end up getting a loan with MTM, this blog may receive a referral fee. I only recommend things I use myself and genuinely believe in.

My thoughts on ‘The Great Taking’. An idea that the masses will lose untold amounts of wealth in the next financial crash, due to a deliberate plan by mysterious figures.

I explain why (and how) I bought a Tesla. The experience so far. How much it cost, and ongoing savings/expenses. Charging options + EV basics. Tax rebates + subsidies. And whether you should get an EV.

Get my latest content and thoughts straight to your inbox.

A fresh dose of financial motivation to power your journey.

Love it mate! Sounds like you’re really enjoying early retirement and not getting too hung up on squeezing every penny to see how low you can get your expenses! Hope your dog’s health improves this year.

Haha, definitely not. Thanks Chris, hope you have a great 2023 mate 🙂

Thanks for sharing Dave, love your work! I can definitely see the effects of inflation, my expenses have risen over 10% on previous year and the full interest rate rises haven’t yet kicked in on the mortgage. I may also just be spending more, we were in lockdown in Sydney for much of 2021 so our spend was at an all time low for 3-4 months.

Cheers Marie!

Yeah the interest rates will be a big kicker in 2023 for a lot of people I reckon. Comparing spending to 2021 with lockdowns would definitely have impacted the comparison. Either way, may be worth going over your expenses to see if there are any obvious improvements that could be made 🙂

Hey Dave,

As always I love your honest approach to these annual updates.

I’d be interested to hear your ‘start from scratch’ scenario for income and expenses.

Appreciating other people’s approach to this has always been interesting to me…

As you say, there’s no perfect way, only your way. But that doesn’t mean you can’t derive value from differing perspectives and then iterate from there.

Cheers,

Kris

Cool, I’ll make note of that 🙂

Absolutely, you nailed it – there’s value in taking bits and pieces of info from everyone’s situation and applying it to our own.

Fascinating insight into how someone else spends their money, thanks for sharing Dave!

One comment and one question – I agree that Flybuys can be like gold, and the Woolworths equivalent “Rewards’ is excellent in its own way too. I was able to redeem over $420 cash at Coles late last year, compensating for the effect of inflation. With ‘Rewards’ one can get cheaper petrol to the tune of 4c per liter, or 8 c per Liter at Ampol for the first three purchases using their app on your phone.

Question, what did you spend on books, courses or other means of self-education? Or is this included in ‘Other’?

Very nice on the Woolies rewards. I’m not clued up on how the Woolies one works, but I assume it’s similar.

Which one is better would you say? Coles does the fuel discount thing too by the way, with Shell.

I actually spent zero on books/courses/etc this year. I’ve been learning a fair bit from YouTube, podcasts, and still got a big list of books to get from the library which I haven’t got to yet!

There’s something just so lovely about going to a nice cafe. Especially when you can go during the week when everyone else is at work! I was in Sydney during its first lockdown at the start of the pandemic, and really felt how important local cafes are to people. Walking to the cafe to get a coffee was one of the highlights of the day. Hope your dog is doing ok!

Oh yeah, it’s fantastic going places during off-peak times – just a real delight! Other than that, they just feel like a nice, friendly, happy place to hang out and help form part of a community (as you point to). I know bloggers like me usually crap on the idea of the daily takeaway coffee, but that doesn’t mean I don’t like cafes 😁

Thanks so much sharing Dave, it’s inspiring to see that early retirement can be done and seeing the numbers to back it up.

Quick q (and sorry if you’ve already covered it somewhere) – do you have private health insurance? And if not, why not?

Thanks mate 😀

Thanks for reading 🙂

Nah we don’t have private health. Rationale is, we’re happy using the public system. If something is emergency, we end up in public anyway. If it’s not urgent, we’ll either wait on the public list, or pay out of pocket. We also don’t get the same tax benefit given low tax rates in retirement.

I had the same question. I assume in retirement you also do not have to worry about disability cover etc.

Nah, given we’re not reliant on personal incomes any more, we don’t see the need for insurances like that. We also have super in the background which we’re not reliant on, plus both of us earn some part time income, meaning there’s a lot of cushion already.

Thanks for sharing Dave. Nice insight into how to live a happy life. Hope your dog stays well. Yes my expenses were up as I bought another puppy! The price of dogs is now insane! He is worth it though. Here’s to a happy and healthy 2023

Thanks Anna!

Haha lovely, puppies have gotta be one of the greatest things in the world. What type of dog is it?

Hope your dog’s doing well. In 2018 we spend about $10k on chemo & surgery on our dog. She’s still with us 4.5 years later, just older, slower (“senior citizen”) doggo.

On another note gees you don’t spend much (well compared to us) on groceries. Do you buy meat ?

That’s fantastic to hear 🙂

As for groceries, we eat almost no meat ourselves, eating mostly a vegan diet. Included in those groceries is food for our dog including veg fish and mince. Maybe check out my grocery article for more details: https://strongmoneyaustralia.com/frugality-and-food-the-grocery-strategy/

Thanks for the update mate. Very keen on fleshing out a start from scratch post 👍

Cheers Russ, noted!

Thanks for detailed walk through. Out of interest, do you have any specific tool/app that you use to track your expenses?

Hey Nathan. Not really, as I said in the post: “I don’t use any fancy software to track my spending. Just a very simple spreadsheet with categories on one side and months across the other. One day each week I take 5 minutes to check bank transactions and add them to the tally for whatever category they fit in. I have recently been playing around with a spending tracker that Pearler is building. It’s actually coming along quite well and I can see myself using that instead of my spreadsheet sooner or later.”

Hi Dave you mention 7% interest, may I ask where you are getting that kind of return? My bank’s best return is about 2%. And share returns are not at a guaranteed rate, so am curious.

Thanks Debbie

Sorry where did I mention getting 7% interest?

2% is woeful! There are high interest savings accounts paying up to 5% at the moment, an offset account (if you have a home loan) would earn higher (or you could just pay down extra), share dividends may be about 4% on average + growth over time (total return perhaps 7%). Some savings accounts listed here: https://www.finder.com.au/savings-accounts/high-interest-savings-accounts

Great article and your spend was just over what I have calculated to live every year running two vehicles plus a motorbike but owning our own home. My wife has cancer so that has blown our budget a bit also and are yet to retire fully but want to semi do so very soon! PS I got here via your return comment to me on Livewire recently. Cheers, Warren

Thanks for visiting the blog Warren and checking it out 🙂

Sorry to hear about your wife, that’s totally understandable, I wish you all the best with your semi-retirement plans! Having more free time for the people and activities that are important to us is priceless.