Peter Thornhill is a well-known advocate for long term share investing.

He’s been educating others through his presentations and his book Motivated Money for almost two decades.

Peter’s teachings helped me make sense of the sharemarket and realise it’s not some crazy casino. It’s simply an emotionless exchange where companies can raise capital, and people can buy and sell existing businesses.

The craziness is what we as humans inject into the sharemarket (with our fear and greed) that gives it a bad rap.

There’s a lot of good content shared here. So please make sure you bookmark the suggestions for later on, because I’m sure you’ll get a lot out of them!

For those unaware, Peter’s core message is, we should be investing in shares for the growing income stream. Not focusing on capital growth or trading.

Over time, as company profits grow, dividend payments also increase, leaving the investor with little to do but sit back and collect the income.

As a side benefit, the shares will also increase in value because the company is more profitable – hence becoming more valuable.

I’ve written about the dividend approach on this blog too: Dividend Investing – The Perfect Fit For Aussie Early Retirees. And I also cleared up many of the common misconceptions of the dividend growth strategy here.

Two important things before we begin…

1- After doing this interview, I wrote a detailed guide of Peter’s investing strategy and how to implement it, which even includes some comments from the man himself!

2- I created a spreadsheet to keep a running estimate of my dividend income which helps me plan my finances and watch the progress. If you’d like a copy for yourself, simply enter your email below and I’ll send it to you.

Peter Thornhill: I left school in 1965 having failed most of the matriculation subjects (year 12).

Dad got me a job with a bedding manufacturer, embroidered sheets and pillowcases, as an apprentice sewing machine mechanic. Soon realised I could cross that off my bucket list!

Applied for a job with National Mutual in the actuarial department and went back to night school to complete my final year. Got married in 1969 and changed jobs to work for a GM dealership arranging finance for new cars sales.

In 1970, took off with my new wife on an 18-month working holiday. Almost 50 years ago, a one-way economy airfare was $400! We spent 6 months in the US, then to London and didn’t return for 18 years.

Initially worked for National Mutual in their London office, on the princely salary of £11 a week. Applied for a job in 1972 as a clerk with a merchant bank. Ten years on, I had morphed from a clerk to running the new business department and, following the 1973 – 74 financial disaster, took over the care of hundreds of orphan clients as a financial planner.

In 1982, I was approached by Henderson Unit Trust Management to join them and open an office in the Midlands, Birmingham. Moved the family to Kidderminster in Worcestershire.

In 1987, following a successful period in the midlands, Henderson’s moved me back to London to take over the South East of England. In the process, was approached by Mercury Asset Management, a subsidiary of the merchant bank, S.G Warburg. They offered me a job, sales director, back in Australia, as they were getting involved with Potter Partners, a Melbourne based stock broker.

Thus, in 1988, was born Potter Warburg Asset Management. I got mentioned in dispatches and in 1992, Perpetual Trustees approached me to join them as National Sales Manager.

They were about to launch the venerable Industrial Share Fund, previously an in-house trustee common fund, as a public offer fund. Moved the family from Melbourne to Sydney. Then, in 1995 MLC approached me to launch an industrial share fund, and so was born MLC Incomebuilder.

In April 2000, at 53 years of age, I resigned from MLC to pursue my true vocation; public speaking and wrote a book!

Peter Thornhill: No, it was a process of osmosis. The period of financial planning in the UK laid the foundations. Here I was dealing with 3rd and 4th generations whose wealth had come from investing in shares, living on the income and passing the corpus to the next generation.

Wealth was judged by cash flow, not the size of ones toys. I presently invest in a listed investment company in the UK that has been around for over 100 years. It has just celebrated its 53rd consecutive year of dividend increases. This meets my benchmark but is not newsworthy!

Peter Thornhill: The only thing that has changed, is the sheer volume of rent seekers that have entered the industry. Fund managers, soothsayers, fortune sellers, etc. All promising a quicker/better way to get rich.

What has stayed the same is the simple principle of wealth creation through human endeavour.

Peter Thornhill: No change, merely hardened. The pushback when I first arrived back in Australia, was what turned me in to the monster I am today.

Being told I was wrong, forced me to re-examine all that I had taken for granted in the UK, only to confirm I wasn’t. The pressure to conform was what eventually made me leave the industry.

Peter Thornhill: They are simple, they have been around for decades and suffer none of the structural problems associated with the managed funds industry. Too many people become slaves to their money. Money remains my slave so that I can focus on what really matters in life.

LICs enable us to sit back and get on with all that life has to offer. No favourites. My simple selection criteria is that they must have been going for a minimum of 50 years and the management must be integral. Reason for 50 years is that I am singularly unimpressed by the carpetbaggers who have entered the industry over the recent decades.

The managers from the funds management industry who have decided that a locked in asset base is attractive! They then launch a listed investment company and their management company then charges unconscionable fees.

Peter Thornhill: I don’t ever think about it. Since investing in Argo in 2000, we have made a further 24 additions. That’s more than 1 a year. Do you know how much time I spent looking at the discount/premium – nil. I have better things to do. Ditto with the other LICs we own.

Do I lose sleep that a few of the parcels were bought at a premium? By the way, what about the other purchases that were bought at a discount. Perfection is a dream with hindsight.

Peter Thornhill: If you seriously have nothing better to do and you are a qualified stock analyst, or fund manager.

Most people spend most of their lives wasting priceless time on things they aren’t good at. I counsel people to become brilliant at one thing and outsource their incompetencies.

Peter Thornhill: Yes, and liquidity. ETFs usually have a market-maker as the fund manager doesn’t provide a daily redemption facility. During the GFC, in the US a number of market-makers stepped back buggering up the liquidity.

Peter Thornhill: Waiting for what?

Peter Thornhill: Yes. This is the start of analysis paralysis. Wasting time every day watching prices.

Often, if they make a decision, the price may drop even further leading to regret which makes the next decision even harder. Or, a dead cat bounce starts it going back up, so they buy and it falls back again. The permutations are endless.

Peter Thornhill: Which ‘investors’? Imputation has only been around since 1987. What did investors agonise over before then? Other countries survive without imputation.

Peter Thornhill: Correct.

Peter Thornhill: Bollocks! There are two elements here; certainty or pot luck. Dividends are reasonably consistent over time. If, however, you are cashing shares to supplement your income you will be exposed to the fluctuations in share prices which may see you selling shares at a less than ideal time…. GFC anyone?!

Eating the seed corn is how civilisations implement Darwin’s theory by self-selecting themselves out of the human race. If you have a use by date on your birth certificate, it might work.

Sadly, if you retired too early with too little you have no choice.

Peter Thornhill: The portfolio tells me what our income and lifestyle will be, just as my employers told me what it would be for all those decades.

Nothing magic happens when you retire, your income remains subject to all sort of vagaries that plague the human race. Toughen up princess!

Peter Thornhill: Spend less than you earn and borrow less than you can afford. Huge debt is just plain stupid however, I understand that everyone wants to get rich quick. Time will do all the hard work if you have the patience.

It has always struck me as odd that if I tell people someone was negatively gearing into an investment property, he would be congratulated on the clever tax deduction he was generating. So why is it that losing money on property is clever when, with shares, everyone wants to see the book balance, i.e. income coming in equals income going out.

Why can’t one negatively gear into shares if it is such a slick idea? It certainly beats negatively gearing into property. Rents don’t increase like dividends do. Nor do you get franking credits with rent. Also, the holding costs and maintenance costs with shares are zero; unlike property!

Peter Thornhill: Yes, over the last 117 years we have never had a period where there has been more than 2 years of consecutive negatives. Besides which, why are people incapable of dealing with a little bad news?

Fear is based on ignorance and the sense of entitlement rules. Anyone who believes that governments are in control will always get a nasty shock.

Peter Thornhill: No. We have some superb global companies that far outweigh some of our largest companies; CSL and Cochlear immediately come to mind. Besides which, what would I know about shares to make me concerned?

Peter Thornhill: Not really. I think it is overplayed for most domestic investors. Also, events are not ‘local’, they are all global. The GFC being a classic example of sheer stupidity exported all over the world.

Peter Thornhill: (Yes), with leadership which, sadly, is hard to come by. We live in the world, not Australia.

Peter Thornhill: Is 100 companies enough? I’m comfortable that over the last 40, 50, 60 years, the older LICs have done the job; a steadily increasing income stream.

Peter Thornhill: It reflects the endeavours of the human race. If you believe that human endeavour will come to an end, then you could consider investing in something else, but I’m buggered if I can think of what will replace it.

Peter Thornhill: Both. If mining companies are a great investment, why don’t other companies stop what they’re doing and take up mining? Sadly, the cash flow from mining is erratic in the extreme and fails my benchmark.

If property is a great investment why do banks lend you money to buy property? Why do all the listed property companies not invest in property but sell it to you?

Why has no successful listed residential property trust ever survived? And why are companies getting their (commercial) properties off their balance sheets?

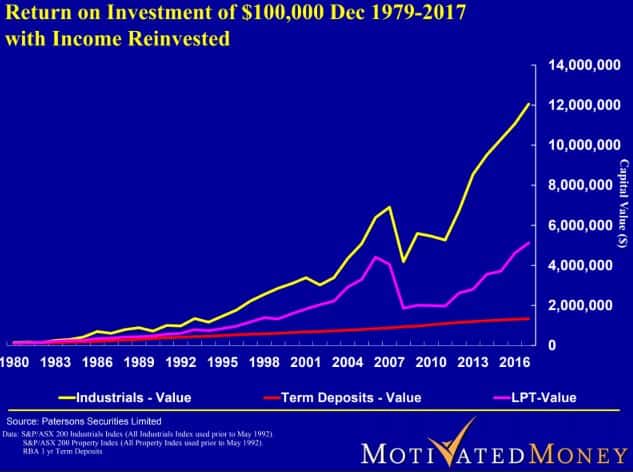

As a comparison, here are the returns of Listed Property against Australian business (ex resources) as represented by the Industrials Index.

Peter Thornhill: If it does not occur, then clearly no one would ever start a business, as there would be no point. We would all sit around and day-trade residential property, until we realise that there are no longer any companies providing the everyday needs we take for granted.

If you are running a business and your profits are not growing with inflation, then you are going backwards, with one inevitable result.

The good news is, you won’t be doing it for too long!!

Peter Thornhill: If you don’t have the discipline then don’t bother starting. You are only going to frustrate yourself and curse all those who make it.

Let’s go back to my benchmark for performance. I’m doing this for the growing income stream!

Refer back to the beginning; what about my UK LIC that has had 53 years of dividend increases. Where is the underperformance?

Peter Thornhill: NO discipline and too damned impatient.

Peter Thornhill: Benign neglect. I’m too busy romancing my wife all over the world to bother with trivia.

Peter Thornhill: I wouldn’t. Decades of presenting have made it very clear to me that a small minority intuitively get it and act. The bulk of an audience enjoy the presentation and do nothing. And the remainder hate me for exposing them to the mistakes they have made.

Peter Thornhill: Currently around $11 million. The dividend income on our return to Australia in 1988 totalled just under $1,000. Last year, our total investment income was approximately $400,000.

Peter Thornhill: Matching! Two savers in a relationship is nirvana. Two spenders is cosi cosi (so so). A spender and a saver is a disaster. One party will forever white ant the efforts of the other.

Peter Thornhill: Fear, pure and simple, based on ignorance. It looks like a casino and they have not the slightest understanding of the drivers of share VALUES. The sole focus is on gyrating prices and endless, mindless commentary.

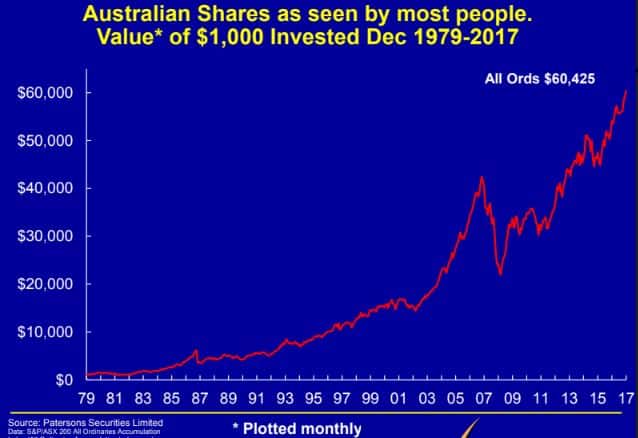

To sum this up, here are two charts. The first one shows how most of us look at the returns from the sharemarket.

And the second chart is how Peter looks at it.

Peter simply looks at where the market started, and his return up until today. He doesn’t bother with or care what happened in between to get there.

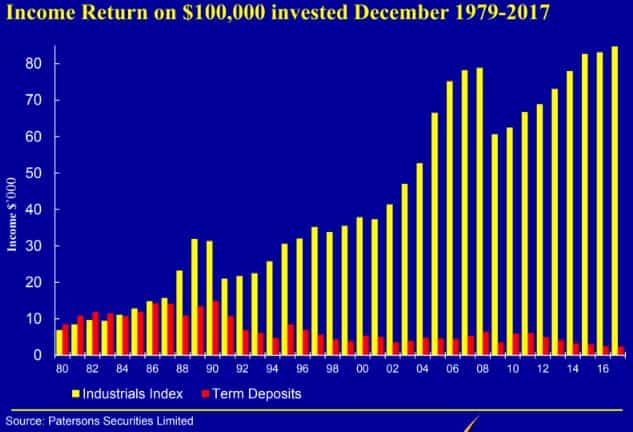

And as a final point, here is what Peter calls the ‘mothership’ slide – the foundation that the dividend growth strategy is built on.

Because of this, I feel it’s the most important picture of all!

It’s a chart showing the dividend growth of Australian business (excluding resources) since 1979.

No income reinvested. No money added. Just the pure and simple, growing income stream.

Personally, one big takeaway from this chat, is to be disciplined. Stay true to your strategy through thick and thin. If your underlying investment philosophy is sound, there is no reason to change course or second-guess yourself.

Also, to do better in the market, most of us should (ironically) ignore it completely! Simply continue to buy shares in your chosen investments and forget about it. Spend your time doing more productive and enjoyable things!

Admittedly, I’m guilty of being too enthusiastic about investing and spending too much time on it.

And as for the market’s wobbles and setbacks? Well, we just need to harden up and deal with whatever happens. Think of it as a constant game of ‘three steps forward, one step back’.

Another thing Peter reminds us, is the power of investing in business as a whole.

The relentless progress that’s made through innovation and technology, as well as the productivity, ambition and determination of other humans, is what underpins the sharemarket and our wealth in society today.

Let’s thank Peter for sharing his thoughts with us and being so generous with his time to answer our questions.

And don’t forget you can get Peter’s book on his website – www.motivatedmoney.com.au – which I highly recommend.

I’m sure you’ve enjoyed this Q&A with Peter Thornhill as much as I have. And hopefully it answers some of the common questions I see regarding this strategy and his message.

Please share your thoughts in the comments. As always, thanks for reading!

WANT PRACTICAL FINANCE CONTENT EVERY WEEK?

Join thousands of readers and subscribe to the Strong Money Newsletter below.

My thoughts on ‘The Great Taking’. An idea that the masses will lose untold amounts of wealth in the next financial crash, due to a deliberate plan by mysterious figures.

I explain why (and how) I bought a Tesla. The experience so far. How much it cost, and ongoing savings/expenses. Charging options + EV basics. Tax rebates + subsidies. And whether you should get an EV.

Get my latest content and thoughts straight to your inbox.

A fresh dose of financial motivation to power your journey.

Awesome!

This is great stuff from an investing legend.

Not legendary because he beat the market, but because he practices what he preaches, invests in LICs, ignores everything else, gets on with life and now has multi millions to show for it.

Must of felt a bit odd reaching out to Pete, How’d it go down?

Exactly Pat. It’s Peter’s discipline simple philosophy that’s the most admirable.

He’s not caught up in academic studies or theories. Peter is living the strategy!

Not odd at all. I emailed him a while back to say thank-you, and reached out again recently after I had this idea of a FAQ-style page. Thought it’d be helpful for a lot of people 🙂

Went down well Pat. We all deserve to have the basic knowledge to be able to make better quality decisions

Hi peter

My name is Jacqueline just been listening to you on podcast today

And very interested in investing LIC INVESTING FOR DIVIDENDS. how does one start this is there a guide for me to follow. Will I go through a bank and do it from there or a platform somewhere??

Hi Jacqueline. I actually wrote a whole blog post about how to implement Peter’s strategy here – https://strongmoneyaustralia.com/how-to-implement-peter-thornhills-investment-strategy-in-2020-and-beyond/

Excellent Post today SMA!! Hearty Congrats on getting Peter Thornhill on to your Blog!

One sentence summed his approach up for me; “Wealth was judged by cash flow, not the size of ones toys.”

Why do we not heed this simple but sage advice??!!

I’m off to see PT ‘in the flesh’ next month in Sydney. Can’t wait.

Keep up the great work with your Blog.

Thanks Jeff!

That’s a good takeaway. I think most of us get caught up in chasing net worth/capital growth, when really, growing investment income is what’s behind it – the values/prices are just a side-effect of the earnings/income generated by companies.

I’m sure you’ll enjoy Peter’s presentation – I’ve never been, but heard good things. Have now added a reminder about it in the post, thanks for that.

Fantastic interview, I’ll be showing your blog and this article to everyone who discusses money with me, cheers!

Cheers Nick 🙂

Pure Gold.

Couldn’t agree more – it oozes simplicity.

An awesome post.

Invaluable advice and wisdom and the questions to match.

Well done SMA

Thanks John, glad you liked it!

You listed in this interview the LICs that Peter likely invests in as mentioned in previous articles and comments by Peter. Can you post a link to these articles? Also how can BKI be one of the LICs when it doesn’t satisfy the being around 50 year criteria?

Thanks

Kieran

Re PT’s LICs they’re ARG, BKI, MLT, WHF. Do a search of Cuffelink’s site on “Thornhill” and be sure to read the comments section after the article. Great value in doing do.

https://cuffelinks.com.au/?s=Thornhill&submit=Search

And PT’s criterea isn’t exactly what he says publicly his requirements are. BKI is less than 50 years old and both BKI and WHF are externally managed. Just equate it to meaning having been around a long time with a low fee, low turnover, dividend focused and minimal key person risk.

Kieran, we can only assume which is why I said likely. In this article, he discusses Argo, Milton and Whitefield. And in this article, in the comments he mentions BKI.

BKI is actually many, many decades old and was spun out of Brickworks – the building products company – which I mentioned in my review here. While it may not quite fit the 50 year rule, it’s effectively run by the Millner family, who also runs Washington H Soul Pattinson, a family investment conglomerate which goes back over 100 years. The Millner family are honest and reliable managers of shareholders capital. They’re focused on low-costs and delivering long-term dividend growth for shareholders. It could also be the case that Peter prefers BKI over AFIC because BKI has much less resources holdings – it’s much more focused on industrial companies – see Peter’s slide for why that’s important to him.

There’s not many LICs which meet this criteria, but in any case, I believe it’s more a general rule than an absolute rule. All the LICs discussed are similar. Been around a long time, very reliable, low cost and focused on long-term dividend growth.

Hope that helps.

Thanks for that. Was a great article to read. Not sure anyone can argue with his strategy

Am I correct in saying WHF (and QVE) have a comparatively high MER at 1% compared to other well known LICs?For example; ARG, AFI, MLT have all far, far lower MERs at about the 0.15% mark. Why are WHF so expensive?

Whitefield has a fee of around 0.35% and is 100% industrials. It’s a little higher but it’s a slightly unique company.

QVE is around 0.90% from memory, scaling down to 0.75% as it grows. This is a very different LIC. They focus on stocks outside the top 20, so more mid/small size companies.

The manager IML, has an excellent track record of strong after-fee performance with unlisted managed funds over the last 20 years, with a strong focus on dividend-paying industrial stocks. You can find more on IML’s website about their philosophy and fund performance. (for full disclosure, I own QVE)

LICs in this space tend to charge more (some charge performance fees too), as there’s supposedly more research involved and because they can. Managers in the small/mid cap space tend to have a better track record of beating the market as the companies are less followed/less researched/too small for big money etc (though that’s not really our goal here).

Dave I hope you don’t mind me adding comments where I think it might be helpful? You know what I’m like.

WHF’s fee is starting to creep up, now 0.40% according to recent annual report.

However in QVE’s case one needs to look at total cost (not just the mgr’s fee) which from memory is closer to 1.1%. But given the sliding fee scale as FUM grow hopefully it’ll get closer to around 0.9% over time. Still quite low for quality Mgr in the mid / small cap space. MIR has one of the lowest fee (0.60%) around for a smaller cap Mgr. A favourite of mine buy just a shame about the high premium in more recent times.

Not at all mate – welcome to comment as much as you like. Always good stuff.

Haven’t read Whitefield’s report but did notice the MER increase. Has the fee paid to external manager White Funds actually increased? Or Whitefield just had higher expenses this year? Fee still likely to head down rather than up over time though.

Good point re QVE – I’d forgotten to check that. I do like MIR also. Seems to focus more on small-caps than QVE, who seem to hold mostly mid-caps. Any thoughts on that? Fee is much lower for MIR as you said, and can also pass on the LIC CGT discount. Both good managers who are far more honest and shareholder friendly than others.

Re AFI,

I spoke to PT once about why he doesn’t hold AFI given he holds ARG. He said there was no particular reason, just the way it worked out. You don’t need to hold all of them to get the job done.

That said I personally prefer the four LICs PT holds over AFI due to being relatively smaller (more portfolio flexibility albeit ARG is still very large) and generally more Industrial focused.

BKI in particular is unique in the low fee older style LIC space given it’s minimal embedded capital gains (new investors aren’t impacted by sale of existing profitable assets) and at around $1 Billion FUM it’s in a sweet spot of being large enough to get good access to company management / deals but small enough to still be nimble portfolio wise and for new additions to have an impact. On top of that it’s a Millner entity so has access to considerable resources.

Thanks for clarifying Nodrog – helpful as always.

I was looking at Argo recently and although very large, they seem to be have the lowest weighting to large-caps, a healthy amount of mid-caps and the portfolio has (in my view) very good diversification. These things move around of course, but it was interesting to note.

As discussed previously, hopefully BKI can make the most of these advantages.

In any case, I think all the old-style LICs listed are good vehicles focused on low-costs, increasing dividends and I don’t think Peter would object to either choice.

Correct Dave. Trying for perfection is the pathway to madness. I accept slightly sub optimal arrangements for variety of reasons. See the post by Jeff below. The MER of Whitefield is higher than the others,not 1%, but it is also 100% industrials unlike the others that hold some resources. Frieda and I got to where we are today not by trying to finesse our holdings but by simply getting the basic strategy in place and then damn well sticking to it.

This was awesome! Well done Dave

Cheers Firebug!

Great stuff Dave. One question I have with the 4 LIC’s. If they are all basically the same holdings, why would you have them all?

Cheers Jason. Well, it spreads manager risk, in case something crazy got into the water at Argo for example 🙂

It also gives more opportunities to participate in discounted share purchase opportunities, as recently came up with BKI. And for those that bother with it, more chance to purchase one which might be trading at a discount.

Also, they will inevitably hold a few different companies so it can add extra diversification. And while the LICs try to smooth income, it’s not perfect, so holding a couple will smooth out the income stream too. For a couple of years recently AFIC’s dividend has been flat, while Argo’s has been growing. Holding both would result in slightly increasing income vs flat. So it has an averaging effect on performance and income, since we can’t predict this in advance.

Like Peter said, you don’t need to hold them all. Even 2 would give most of the same benefits.

Well done Dave in coming up with these good questions to Peter. Appreciate the time Peter and you have spent with this and the responses.

I did see you raised the question of Australia and the large LICs having a heavy weight to financial stocks and note Peter’s response he is not concerned by this. I am curious though if maybe that is the case because his own portfolio has so many individual holdings outside of the LICs. Would that water down his look through bank exposure to far lower percentage than the large LICs he owns have? Or would his own portfolio have over 25% to banks and he still maybe thinks that is a sound strategy? The higher bank exposure does help with the dividend flow.

Maybe he covered this in his book but it has been a long time since I bought it and I am away from home to try and dig it up and look. So I apologise if I am going over something that has been covered already. Or maybe is it something that he has avoided discussing too much as doesn’t want to go near the giving financial advice area. Or perhaps doesn’t feel that whether the difference in an investor owning say 10%, or 25% plus in our major banks is that important any way.

Thanks Steve.

Not sure of Peter’s reasons. It could be his direct stock holdings dilute it, or perhaps more likely, he’s simply happy to roll with whatever the big LICs hold in their big basket of dividend-paying stocks? They’ve all been going for 60 years plus, and would not have held major bank positions 30 years ago for example. In 20 years time, the market could be more dominated by healthcare or technology or who knows what!

Similar to an index investor, these days I’m mostly happy to go with the flow and accept the dividend flows from whatever our market/LIC holdings give us. If the banks become less relevant in the future, that will be reflected in the LICs and the index, and they will slowly be replaced/diluted by other companies – meaning we don’t really have to think about it too much. But for now, they do remain some of the best dividend-payers on the ASX.

Answered a lot of my questions fantastic to hear it from the man himself.Thank you very much.

Hi Jason, Dave’s got it. The four LIC’s have given us many opportunities to top up our holdings time and time again; at zero cost. This has been a great boon for our three sons who, over the years, have become really well disciplined in taking these up and building meaningful portfolios. They are ahead of the curve as they all started much earlier than we did as we had no guidance until after we left Australia and I’m a slow learner! Thankfully, they have focussed on their families and their careers and left money as their slave; it’s a beautiful thing.

Hi Peter,

I read your book Motivated money about a month or two ago. I was curious why you didn’t give specific examples of where to invest money e.g. LICs?

From memory (correct me if I’m wrong) I don’t believe you even mentioned LIC’s.

Hi Kieran.

Correct. Having quit the industry 18 years ago I have no licence and am not authorised to give specific advice; there are quality people in this industry better qualified to do this. I am attempting to give people sufficient knowledge to be able to ask powerful questions.

Understood. Are you happy to let us know which LICs you are currently invested in?

Thanks for your time

Kieran

No problem Kieran.

They are WHF, ARG, MLT and BKI.

Not much difference with our picks of LICs.. The only investments I hold are AFIC,ARG,MLT & BKI. Stayed away from Whitefield due to higher fees than other major LICs. Don’t do individual shares as I have no idea what I’m doing ????.

WHF stands out as an outlier with its MER of 0.40, as compared to the others all around 0.15.

Is there anything in particular that justifies this cost as compared to the other three. Currently it trades at a significant discount to NTA (which I know you say largely to ignore and invest regularly over time)

As older style LIC’s their portfolios obviously have similar profiles and overlaps.

Thanks for your participation in this thread.

As discussed in other comments, part of it could be Whitefield being a specialised Industrial LIC. But I think more of a factor is their size – Whitefield is only around $400m in size, whereas Argo for example is $5 billion. So being 10 times larger means costs are spread over a much larger asset base.

It’s somewhat likely that the expense ratio for Whitefield goes down a little over time, but no guarantees given that they’re externally managed.

Thank you for a great article. Great to hear it come straight from the horses mouth The article has answered a lot of my questions. Thank you again

You’re welcome Brian, thanks for reading!

Great stuff once again Dave . Thank you very much

Thanks for reply Dave. Reading this article has strengthened my thoughts that I will look to selling one of my investment properties to further invest in the share market and in particular a number of LICs. This particular property currently has not performed that well and costs me to hold and also contributes to land tax I have to pay.

Thanks for sharing Jason, glad it helped. The growing income approach is just so effective and hassle free. We’re looking forward to offloading another property next year too 🙂

Great article.

What are your thoughts, if any, on Wilson Asset Management LICs?

Thanks Adam. I have mixed feelings (I do own WAM & WAX). Wilson have proven themselves a good manager over 20 years, investing in small/mid-sized companies and delivered after-fee outperformance. But to be honest their fees are horrendous, which now bothers me, and I don’t like how they report ‘portfolio performance’ – it’s deceitful to shareholders who do not get those returns.

They have no track record in large caps and overseas equities (where competition makes outperforming much harder) so I think people jumping on the bandwagon are more likely than not to be disappointed with the after-fee returns. So far WAM Leaders has lagged the market despite them declaring ‘portfolio performance’ that beat the index. That said, if investors are blinded by the reported figures, they likely won’t know their real return.

Do you have any insight as t how they calculate their ‘portfolio performance’?

Simply how the portfolio has performed – before expenses, before management fees, before performance fees, before tax. The shareholder obviously ends up with a much lower return.

Hello …

As an owner of some shares in Wam Capital and having attended quite a few of their meetings , l was amazed at their admission that most of their stock selections are/were losers in actual fact !

As a former trader , l found that sort of result hard to take . Hence l sold out of Wam post-haste , but keep a few just to trade as circumstances dictate . l was never happy with the Mer nor Perf .

Best wishes , Rupert .

Hi Rupert. It’s true, their win/loss rate is unusual, but it seems to work for them as they presumably cut the losers quickly. It doesn’t really match how I like to invest these days either so I definitely get where you’re coming from. Cheers.

Remember Adam, they must have been around for 40-50 years at least. Also, anything that bears the name of the guru can be ignored.

Great get Dave.

My wife and I have been discussing Peter’s strategies all weekend since we discovered his work via some links in an earlier post of yours.

In regards using home equity to leverage the purchase of shares (the dividends of which go toward paying down your mortgage faster) I was wondering whether this was a strategy that you have used yourself (or would consider using?)

Also, I think I grasp the concept but I would love to hear the process as you understand it Dave?

Thanks very much.

Pete.

Cheers Pete!

I haven’t used it but I definitely would consider it. In fact, we actually have some non-deductible debt that we’ll recycle soon and use that money for shares, since the debt is already existing and we have a lump of cash destined for shares anyway. We’ll simply pay off that loan, borrow it back out, buy shares, and the loan is then tax-deductible against our dividend income.

Try this article for a good description of the general process – http://www.australiandividendinvestor.com/2016/11/17/debt-recycling-how-i-paid-down-a-mortgage-in-10-years/

Also, these days ‘line of credit’ loans tend to come with a much higher interest rate. An alternative is to keep a regular home loan and create ‘split loans’ – where after you’ve paid off 20k or 50k, have it separated from your existing loan, and borrow the money back out for dividend-paying shares. A mortgage broker will help with this.

Hope that helps.

Dave,

I have a redraw account on my mortgage. say I withdrew 20k from the loan on first day of the financial year to buy shares but kept paying off rest of my mortgage with salary for the rest of the financial year. can I claim the interest on 20k as tax deduction for full financial year. Or do the payments I have made throughout the year with my salary sort of repay that 20k I loaned? Or can they be seen as paying off the rest of the mortgage loan thus ensuring full tax deductibility for the interest on the 20k ?

My understanding is no. The loan must be completely separate from your existing home loan for it to be tax-deductible. You cannot simply redraw from a mortgage and start claiming interest as it’s a mixed loan then (personal and investment).

This is why you need a mortgage broker/bank to set it up.

Hi Pete. Dave has pretty much covered it but I’ll give you my tuppence halfpenny worth. When we returned from the UK we rented initially but the pathetic lack of long term residential leaseholds is a pain in the arse. We eventually bought in Melb and I started using the small dividend stream as additional capital repayments on the home loan. Got a bit sophisticated then and used the house as security for a line of credit to pump up the portfolio and the dividends. Line of credit tax deductible, home loan isn’t so seemed to make sense to use the dividends to accelerate the conversion of a non tax deductible debt in a fully tax deductible debt, n est pas?

Got moved to Sydney and repeated the process. Wiped out the mortgage. Eldest son did the same thing and wiped out his mortgage in ten years. In fairness, they did by a MODEST first home!

Thanks for the Clarification Dave and Peter.

I’ve just about convinced my wife to consider debt recycling seriously but she (and I to be fair) can’t quite work out one piece of the puzzle.

We get that the bi-annual dividends (which have been made possible by the share purchase from the line of credit) go toward paying down the principal of our home loan.

We get that the interest on the line of credit loan is tax deductible and that at tax time the refund will also be used to pay down the principal on the home loan.

What we can’t figure out, however, is when/how is the line of credit loan payed off? Aren’t we simply swapping our mortgage for another line of debt (admittedly with deductible interest) but the debt still exists?

Thanks again.

Yes. So if you wanted to become debt-free you’d simply pay off the investment loan.

Some people (like Peter) would keep it as a cheap source of capital to invest with, but others would rather be debt free. Each to their own 🙂

Correct Pete. The initial aim is to convert the debt from non deductible to deductible. Once that is completed you continue your mortgage repayments (instead of pumping up your lifestyle) and all the cash flow now goes to paying down the debt. You may, like me, find that the slow but steady growth in the portfolio and dividends becomes irresistible! I’m headed for 72 years of age and I’ve never repaid the line of credit. The dividends now are approaching 3 times the cost of the tax deductible interest we pay. My favourite line in my presentations is “perception is reality” and clearly we all have our own ‘realities’ otherwise we would all be doing exactly the same thing!

It rankles with me that so much valuable cash is tied up in a unproductive lifestyle item so our plan is to continue using the flat as security for the line of credit and continue investing in productive assets. On final death the loan will be wiped but we will have been able to use the value positively in the meantime. I should add, as I don’t want people to get the wrong impression, although our asset base and income continue to grow it is not out of greed. Our wish is that on final death, half the estate will go to our children and the other half will go into a charitable foundation. The income from this will be gifted, in perpetuity, to things we feel are important. In the meantime,blessed as we are, we continue to gift during our lifetime.

Wonderful comment Peter, thank you.

There is a large and undeniable opportunity cost in having a paid-off home!

That’s awesome Peter thanks so much for the clarification. I look forward to the irresistible feeling of an income producing share base soon!

Pete.

Hello Peter, just finished your book, and im converted, I have been investing in shares since 1987, but like many I have chased growth. Am now realising some big gains and selling some dogs and buying LICs.

One question, my line of credit is now 6.53%, ( Nov 2018) am I not going backwards after interest on the current average LIC return.

Regards Chris

In case Peter no longer visits here to reply, I’ll just make a comment.

In terms of cashflow, you may be down a little each year after interest costs, but on a long term total return basis, you will still likely do ok. Reason being, the total long term return (including growth) is likely to be higher than 6%. But to be honest, that rate is too high. I’d be switching banks or at least negotiating hard on the loan you have – that rate is not competitive right now and most banks are willing to offer decent discounts to retain customers!

Hope that helps Chris 🙂

WOW Dave, amazing work pulling this together! I can’t believe I haven’t heard or read much from Peter Thornhill, but love his philosophy and very excited to dive deep into all these links you’ve shared! (Although I think I’ll always have a value-investing bent in me!)

Cheers,

Frankie

Thanks Frankie! As Peter said, it’s not newsworthy. Sadly, nobody is excited enough by this style of investing for it to catch on!

Enjoy all the reading/watching 🙂

Always interested to know what Pete would recommend for super. Should we all go all in on LICs and focus on income or is capital growth the way seeing as we can’t benefit from it until 60.

Can’t speak for Peter but he would certainly suggest going 100% shares, as opposed to a balanced fund or whatever the standard is. I’d agree with that also. Likely to deliver the best return over the long term.

This approach is not income at the expense of growth. Please see my older post here – Should You Invest For Income or Growth?

Take a look again at the result from investing $100,000 in 1979, into Australian Industrial shares in the article. Reinvesting the dividends and the balance reaches $12 million today. Although income is aim, capital growth is very very evident in this strategy – it’s just not the main focus, more of a side benefit.

Without reinvesting dividends, the $100k parcel is worth $1.8 million. This means capital growth was 8% per annum. No guarantees of the future of course, but there’s definitely capital growth following this philosophy.

Tim, I can only endorse Dave’s comments below. Since the bulk of the return comes from cash flow and NOT CAPITAL GROWTH stick to dividend paying shares. One thing Dave didn’t ask and I forgot to mention were some word definitions. INVESTING: The use of money productively to produce a regular income. SPECULATION: Buying and selling in an attempt to benefit from a fluctuation in the price. Pretty straightforward!

Dave do you feel this way of investing is more in line with people who are retired or near retirement as opposed to people with 10-20 years plus to work?

This strategy makes sense for anyone. Honestly, I wish I’d started this way 10 years ago. And I don’t see any better strategy for when I’m Peter’s age either. The result is an ever-increasing income stream and wealth to go with it. It’s not income at the exclusion of growth/net worth.

My favorite quote from this is “This meets my benchmark but is not newsworthy”. Sensible, long term decisions and average, slowly increasing returns don’t make the news but create a slowly increasing reliable income stream.

Great read Dave. Thanks so much for this.

Great article SMA! I really enjoyed readingMotivated Money and will def be putting my name down if PT does a Melbourne event soon. Great blog btw.

Cheers

12th September Kew gold club event hosted by income solutions. I’ve signed up for it anyway.

Great work putting this together Dave! A fantastic resource.

And great to see Peter on here providing further feedback. Appreciate it!

After attending your seminar in Sydney last October, I’m bring a friend down to see it for himself in August. Looking forward to it.

I ordered Peter’s book last night and can’t wait for it to arrive.

Hi there, can I ask if you had trouble ordering it? I tried to order it from his website, it said it was successful, but I haven’t been charged yet, and that was a few days ago.

Apologies Nick. This blog has boosted orders and as a self published author with staff of 1, daughter in law who looks after the distribution, our resources are a little thin. I’m in Melbourne for a few days but I understand Charmaine has responded to you.

Enjoy the read.

Peter

Thanks for the reply, Peter, and not a problem regarding the small delay. I’m glad the sales are getting a boost! Charmaine has responded, yes. I very much look forward to reading the book.

Peter – you should look into producing an e-book version on Amazon. Would remove a few barriers of production and is very easy to do for self publishers,

I read Peter’s book recently and found it an excellent read. However, I was surprised he did not mention LICs as an investment vehicle in the book, but rather focussed on ‘industrials’. It was the videos on his Motivated Money website, particularly the Switzer interviews, where he mentions that he uses LICs as a core part of his investment portfolio. In my experience, a lot of Australians don’t know about LICs (they’re too busy obsessing about their negatively-geared investment property!). But, mention AFIC, Argo, Milton, BKI, Whitefield etc. and you draw blank stares.

If Peter ever releases a new edition of ‘Motivated Money’, it would be very useful to explain to readers what LICs are and how they are a very good vehicle for income-based investments.

Otherwise Dave will have to define LICs when he publishes his book; Strong Money Australia!!

Ha Ha!!

Can’t speak for Peter, but it’s definitely sad that this approach is not well known, and how effective it is as a simple way to invest for financial independence – hence why I talk so much about it on the blog!

He possibly didn’t want to speak about specific companies as it may appear to be giving direct advice? Perhaps I shouldn’t even be mentioning them either? Probably doesn’t take much to get into trouble these days.

I think that would be a good idea, Peter can even use these FAQ at the back of the book, as I’m sure that would be the next stage of curiosity with readers wanting to implement the strategy.

Otherwise yes, if there’s enough demand for it (I’d be surprised), maybe I’ll squeeze a book out someday 🙂

Hi Dave

Amazing article. I am only new to THornhills approach but been reading a ton on FIRE lately and investing. I currently have VTS and VEU and am now moving significantly to VAS and Oz market to focus on dividend growth. Reading Thornhills book to. I have a question. I am considering moving my VTS and VEU to VGS. Reason being DRP and also its Aussie domiciled and the dividend yield appears to be better. Also no issues with estate tax (US), etc. What are you thoughts on this? Wise move?

Cheers

Lloyd

Thanks Lloyd, glad you liked it!

As for your holdings – some general thoughts…

Overseas shares such as VTS and VEU will have solid dividend growth over time so you aren’t missing out by keeping them. VGS is simpler in that it’s an all-in-one option. The only difference I believe is that it doesn’t include emerging markets (like VEU?) or US small-caps (like VTS). Its fee is also a little higher. Personally, I would choose VGS because it’s Aussie domiciled and mainly because it’s simpler having one holding, but that’s up to you of course.

Plenty of other dividend focused articles on the blog here to keep you amused for a while.

Thanks for the reply Dave, one other issue for me with the VTS and VEU is the estate taxes. They seem unavoidable. Do you think this plays a big role or is something not to be to concerned about?

Cheers

Lloyd

Can’t say I really know much about it to be honest. I’m not sure whether it would be enforced or not, but I guess that’s a reason people choose VGS – for ‘just in case’.

If you end up with a large estate I guess it’s one of the better type of problems to leave behind.

Hi Lloyd. One thing everyone should be aware of is that ETF’s are still managed funds and, in my eyes, suffer from one major drawback. Any income from dividends and capital gains from trading must be distributed each year. So, depending on turnover, the ‘dividends’ they pay are often inflated by your capital coming back as taxable income. This is another reason I left the industry!

LIC’s, as companies, do not suffer this same treatment and can retain profits and reinvest them for shareholders.

I have seen a fund distribute 20% of investors funds each year for two years. Unit price goes ex div and drops by that amount and you cop the tax bill.

Pay particular attention to turnover as it can be a devil in the hands of ‘active’ managers.

Peter

Thank you for the response Peter, much appreciated. Have given me a lot to think about.

Hi Nick, no issues at all with ordering book. Maybe try again.

Agree…great read

Have just purchased Peters book. Loving it as well. A question.if may. Peter shows an example of dividend recycling using a line of credit against your home with the dividends used to pay down the mortgage. How would you use this strategy if you are mortgage free ?

Is there anything to be gained by borrowing against the house with no mortgage to pay down ?

Well it’s simply a case of whether you want to borrow money and pay 4-5% interest to buy shares. Your total return may be – dividends of around 4% (plus franking), plus growth of dividends over time (say 3-4% per annum). Capital growth would most likely follow the dividend growth over the long term.

Interest rates can increase of course, leading to negative cashflow in the short term, which might be fine depending on your situation. It would likely create greater wealth but it’s not without risk.

Although contrary to what others might suggest perhaps debt is best used when margin of safety is high and risk low such as in times of market gloom. Of course given human psychology based on fear this is when most find it hardest to act. However the reward can be enormous.

Good point, though I think if someone has no debt going into a scary scenario, they’re very unlikely to take on debt when we’re in it. I would probably lean toward using debt as a more permanent feature to grow the portfolio, rather than be super opportunistic, just because it’s simpler/less thinking/less bravery required. Incredible for people who manage to pull it off though!

Continuous buying on the way down and back up would still generate very healthy returns.

Half way through Peter’s book and on Monday will transfer some money I have in off-set accounts against investment property and buy first parcels of ARG, BKI, MLT and WHF. I will then add to these on a monthly basis.

wow wow wow. the more you write Dave the better it gets.

I had a question for Peter. How about if you don t plan to stay in Australia?

You will then get taxed at the non resident rate and then lose all the good aspects of LICs. I own some but vast majority are us shares directly bought there

great work both!

Cheers mate, glad you enjoyed it.

I don’t know the tax outcomes from living overseas, but the core traits (in my view) of LICs/Dividend Investing still remain – a growing income stream from a large group of companies in a simplified way for a low fee.

Interesting! When we left in 1970, we didn’t plan to stay in Europe for more than 18 months. When I was head hunted back to Australia in 1988 I wasn’t sure I would stay as our ‘home’ was the UK. We are resident in Australia and live in the world! The end result is that I have holdings in both countries, both LIC’s and pension funds.

Home is where we hang our hat!

We pay tax on our global income in Australia having declared our interests to the tax authorities in both countries. The double tax agreement with the UK means we lose none of the benefits associated with LIC’s. I refuse to be an ‘absentee landlord’ and buy direct shares in another country. It is a pain in the neck having to do it in this country alone!

thanks both. the country i m originally from (france) does not have a tax treaty with oz (this could change obviously…)

as non resident i would then be taxed in the 30s%. a big chunk in retirement…

hense my reason to look away for now.

on a side note dave i can t seem to receive notifications of comments?

also… referring to your comment of buying directly into another country… this is exactly what i m doing (direct index trading eft vangard through interactive brokers) (!)

Great post. I am eagerly awaiting my copy of peters book.

As a beginner , I have thousands of questions.Apologies. I was almost convinced to buy ETFs based on few FIRE portfolios. But now I want to follow peters advice. How can I buy the LICs for regular investing?

Is it through for eg. selfwealth or comsec like platform or directly with the LIC.

What option in LIC I should choose in order to get the dividends instead of reinvesting (with aim to buy quarterly bulk buy to save on brokerage)

Peters advice was to buy without timing the market. So should we not actively watch for LIC trade at discounts.

Debt recycling is not palatable for me but what should be the priority for someone at 45 yrs with two kids – priority to pay the PPOR mortgage both P&I and how much in addition to invest on shares.

Cheers

Gman

Thanks Gman. I’m sure you’ll enjoy the book.

I don’t have the same feelings about ETFs as Peter does. The ones I’m talking about are very low turnover index funds, where distributions are almost entirely dividends most years and the income stream can be expected to be more reliable and tax efficient than typical managed funds which trade a lot and pay out capital gains. So if you like index funds, you can still focus on the dividend stream from that.

Yes, you’ll need to open a brokerage account with whoever you like – Selfwealth or commsec is fine.

After purchasing shares you’ll receive a letter in the mail asking if you’d like to reinvest your dividends. If you’d like to get the dividend instead of reinvesting, simply ignore it – you should automatically receive the dividends into your brokerage account.

Correct. Peter is saying it doesn’t matter, the discounts and premiums will likely average out over time. Just buy when you can afford to 🙂

Many thanks Dave. I explored your blog all day. So much of useful information presented in a simple way for beginners like me. I have recommended to my friends.

Cheers Gman, I appreciate your comment and thanks for spreading the word!

Hey Dave

1st of thanks replying to my email earlier on this month I haven’t had the time to respond yet sorry about that

Plowing through your blog from start to finish when I get a chance currently on smoko

My question is about ETFs what type of different ETF are you and Peter talking about

A200 Vas Veu vts??

Blog is 🔥🔥🔥

Hey Earl. Yeah when speaking about ETFs I’m basically always referring to index funds like the ones you mention.

I wrote about Aussie ETFs here: https://strongmoneyaustralia.com/my-changing-thoughts-on-index-funds-in-australia/

And international ETFs here: https://strongmoneyaustralia.com/guide-to-investing-in-international-index-funds/

Hey Dave,

Really good interview and I’m glad so many people are getting on board with dividends and LICs. The last graph is great. I think you raised some very good questions and important questions about potential problems. We have a slightly different strategy but hopefully works out well for us both 🙂

Mr DDU

Thanks Mr DDU!

Absolutely, it’s great to spread the word and share this philosophy/strategy with people. It’s so simple, effective and mostly goes unnoticed.

Great article. Read Peter’s book in a day I will sit down and read it again. One question I would like to put to the forum; Is a line of credit different to a margin loan? I have a fear that the banks are a bit skidish with ML’s even if the borrower is not.

Great stuff. I must have read the book 7 or 8 times!

Yes a line of credit is usually where money is borrowed against property (home or investment property), where margin loan is borrowed against a share portfolio. The rates are much cheaper generally for borrowings against property. The cheapest margin loan currently is NAB Equity Builder for people who don’t own property. It looks okay but is not without risks of course.

Would this approach work with something like ASX.A200? I like the idea of investing for dividends but from what I understand a LIC can go belly up and you lose everything, but in an ETF even if the ETF provider dies, I still get the underlying shares?

Yes the income stream approach works for index funds as well. The income stream will just be more variable than the LICs.

Low turnover index funds/ETFs distributions naturally consist of almost entirely dividends (because they’re extremely low turnover), as opposed to typical managed funds which can often pay out large capital gains and have huge tax implications.

Technically yes, the LIC can go under if it is somehow fraudulent or mismanaged, takes on heaps of debt etc. But keep in mind, some of these LICs have been going for 50-90 years and owns shares in a large numbers of companies (like an ETF) does. Their profitability and ability to survive is almost entirely reliant on the underlying companies they’ve invested in. I personally think the risk is so remote I don’t bother thinking about it. If it bothers you stick with the index.

If a LIC goes belly up the assets are still available as secured assets for the creditors. Can’t imagine what would cause a company whose sole assets are shares in other listed companies to go broke? Do you have an example are you just floating a vague premise?

Hi Dave.

Thanks you so much for all the clear information on your website. Your website is what first alerted me to the Peter Thornhill investing approach. I’ve now read his book and feel empowered to take control of my financial future. Buying into LICS’s like ARG, MLT, WHF, BKI instantly resonated with me. I’m pretty new to share investing so it was nice to hear that the share market isn’t a big roulette wheel, and financial discipline and common sense CAN prevail.

One thing I like with long term Dividend Growth Investing is that it is possible to take advantage of a market downturn. Peter Thornhill spoke about this in his Switzer interview. He mentioned CBA and WES as examples he bought at a discount during the GFC.

As a newbie I have a question about that:

Would it be a good idea to own small parcels of shares in a few high dividend paying companies like CBA and WES so that if the market goes south in a big way you can access any special share offers by the companies? Or is it OK to wait and see?

By the way. I love the constructive discussions accompanying each article. Very positive community here. Something that’s rare to find online these day.

Cheers.

Thanks for reading Paulie!

Great to hear you’re motivated to start investing and this approach resonates with you 🙂

As for owning individual shares for opportunities like that – it’s definitely an option, but some things to remember… GFC type scenarios are very rare so you may be waiting a long time and these LICs own large amounts of CBA and Wesfarmers anyway, so they’ll be taking advantage of any discounted opportunities for us, in a way where we don’t have to think about it! And if it’s somehow an irresistible opportunity you could always buy at the market price which will be low in that situation anyway.

It’s simpler to sit back and let them do the job for us and less holdings makes admin and tax time easier too. I like the lazy option 🙂

Appreciate the nice feedback, and welcome!

Great interview with Peter and I fully agree with his investing approach and would like to thank him for sharing his knowledge. Can you offer any more detail on debt recycling?

I currently aim to pay my PPOR mortgage down to zero (not pay it out) and utilise the equity through redraw at as compared to the existing home loan rate <4%.

Yeah the interest is tax deductible on LOC but my mortgage rate is still 2% cheaper to begin with and will always be lower than an LOC!

Am I missing something or just found an even cheaper way?

Thanks Adam.

Yes you’re correct, a typical home loan (especially for PPOR) is far cheaper than an official ‘line of credit’ style loan. It’s just that you may be required to pay the loan principal down over time, whereas LOC balance will stay the same. With a standard home loan, you can always increase the loan later anyway if it’s getting paid down (unlikely to be interest only forever).

Another thing to consider is if money is being devoted to paying down the principal as would be required with a typical loan then it means the monthly cashflow situation will be worse than just paying interest only (obviously). So it may be a cheaper rate, but forced principal payments on a large loan can mean debt is reducing and less can be allocated regularly to growing the porfolio, or less positive cashflow (or negative) from the portfolio.. It’s definitely cheaper but may be less than optimal.

Best scenario is a cheap home loan on PPOR which is interest only and can be rolled over every 5 years. But that option is essentially being phased out (strongly discouraged) in the current environment.

HI Dave, Are you looking at doing a review of WHF? I have invested in BKI, ARG, MLT and WHF but still would be very interested in seeing your review. Do you worry about WHF’s higher fees?

Hi Jason, I probably will do a review of Whitefield, though don’t own it myself.

The higher fees aren’t great, but you could do a lot worse! If I was a high income earner I’d probably lean towards Whitefield and AFIC because of their tax effective Bonus Share Plans/DSSP.

Hi Dave,

I would love you to do a bit more of a comparison on DSSP / DRP / Bonus Plans

I’m quite green currently but hungry to learn. I’m in AFI with just about ready to go on my next parcel. I’m completely sold on just topping up my LIC’s as an easy investment plan but would like to keep it clean and not go above three. I really want to scrutinise the best three for me and just keep adding without too much thought. I want to keep my main focus on savings rate and then when ready to buy just look at my three and choose the one with the best discount compared to the historical (1 year only) discount. That’s my plan anyway!

I’m in a higher tax bracket (90-180) and realise the franking credits will still mean I owe some additional tax. I’m wondering if there’s certain LIC’s that would be favourable for somebody in my scenario.

My shortlist which I wish to reduce to two considering I already own a large market cap fund:

MLT ARG BKI WHF

At the minute favouring BKI for more flexibility with their FUM but any reasons these would suit a higher income earner?

Thanks and keep it up, love your work!

Thanks Paul. I’ll write about this soon, but in short, the Bonus Share Plan/DSSP options make sense for high tax-bracket earners and I’d likely use it myself if I was starting again today.

Predicting which (similar) LIC will do better in the future is not a game I play, but based solely on tax alone, Whitefield and AFIC would be what I would lean towards. It doesn’t mean I’d ignore the others though, just makes them more attractive for tax-efficient accumulation. This is not advice though 🙂

It then becomes a trade-off between tax efficiency and diversifying between LICs – only you can decide what feels right for your situation.

Thanks for feedback Dave. I have also been looking at DUI. I like the look of it and its fees are low as well. Do you have this one and do you like it?

I do like it, it’s a good LIC. Great low cost, low turnover, long term focus, wonderful dividend history. But no I don’t own it – have to draw the line somewhere 😉

Thank you for this amazingly insightful blog. A few questions if that is ok, what are your recommendations for early investors , seeking to primarily hold LICs for long term dividend growth, who are wanting ETFs? And is there a reasonable proportion 80%lic/20%etfs? And if I was to buy the 4 Argo/afi/blk/mlt what proportions of each do you recommend or does it not matter so much? if investing in etfs that’s give dividends would VAS but advised, or a more diversified auto balanced etf like VDHG. Thank you.

It’s all quite a personal choice, as we’ve already discussed by email.

My view is the investor has to choose the international component themselves, whether they want 0%, 20% or 50%+, which is usually best implemented with an ETF. For the Aus shares component if they prefer the dividend focus of the LICs then they can simply add a couple of those instead of VAS or in addition if they like. I’d probably just go with equal amounts because it’s much easier to manage, less thinking involved etc.

Dear Dave and SMA Followers,

I had the very good fortune of attending Peter Thornhill’s seminar in Sydney on the weekend. The seminar was great; especially if you have read his book Motivated Money. But even if you haven’t read the book, I highly recommend seeing and listening to PT in the flesh. He is a very engaging and witty presenter. He has a sardonic sense of humour, reminiscent of Paul Keating… The investment topics will leave SMA blog readers drooling for more!! Great stuff. Thank you Peter! And he signed my book too!!

Thanks for reporting back Jeff, I was hoping someone would 🙂

Haha I love Peter’s humour – I’m sure the presentation was incredibly interesting and entertaining!

Just a reminder everyone, Peter has another seminar coming up on the 23rd of September if you’re interested, I’ll be going along, can’t wait!

Just so everyone knows – where will it be held Nick?

Sorry, I should probably mention that 😉

Same place as above in Sydney, The Vibe Hotel : https://www.motivatedmoney.com.au/presentations.php

Although it looks like it’s already sold out, but a new session might be added soon.

Hi Dave & Peter

Another great post love reading your blog & love Peter’s book, I have just finished it thanks for the recommendation. I cant thank you both enough for sharing your work and making it easy to understand.

I have been sharing your blog with my husband and it has changed our perception of money and what financial independence means to us. We are just starting our journey to FI and hope to influence our young family by setting a positive example.

Looking forward to reading more of your work, this is the first blog I have read and I am loving the positive community and reading about a real person.

That’s wonderful, great stuff Serena!

Happy to have you here, and thanks for reading 🙂

Hey Dave & Peter,

Interested on your take on the Whitefield CRPS

https://www.asx.com.au/asxpdf/20180907/pdf/43y44czyfjbw1w.pdf

Sorry Paul can’t really comment, I have no knowledge/experience with those! Hopefully someone else can chime in…

I personally think it might be a very minor positive but this news should have been known about for a long time. I think from memory WHF raised some convertible debt finance about 5 years ago when market interest rates were quite a bit higher than now. The reset date has arrived meaning that the rate they have to pay on these convertible securities will be lower. Also some holders of the convertible securities will convert them to shares. In both cases that reduces borrowing costs, helps the earnings of WHF and gives them scope for larger dividends. Since our market is so dividend focused that could be a positive.

A potential negative is that the convertible security holders get a discount with the new shares they get issued by WHF if they go down that path. This will dilute the NTA value a little, I don’t know how much though.

Someone please correct me if I am wrong as I am not a holder so quite possibly could be! Just going off some scribble notes I wrote ages ago. Someone may know more about possible dilution to NTA also.

For the readers of this thread and those that are interested in the investing style discussed here and WHF, I am guessing it is just a bit of noise and business as usual, don’t stress. ????

Thanks for that Steve – valuable stuff 🙂

It looks positive with Whitefield announcing they plan to increase the dividend by around 11% this year, based on this increasing their earnings. Nice boost for shareholders.

I am curious to know about the 100k used as an example in the graphs. I don’t recall reading on his book if those 100k were from now or back then. Because 100k from 1979 now would be = $464,681.30.

Lastly, do you happen to know what amount was used as the reinvested income for the graph that goes to 12 million?

At the moment I am trying to decide between index or dividend investing. Both sound very appealing to me… that has me thinking though, what do you think would produce the most capital over the 30 year period? Because if you index and if it made x2-x3 the amount you could sell everything and just go to LIC’s for Income when you are ready to retire and you would be much better off…If the market is doing well of course.

Thanks for the comment Swifteagle. I fear you may be overthinking it.

It’s a simple 100k from back in 1979. The dollar amounts are less important, you can also use 10k or 1k if you wish – just take some zeroes off. The percentage returns are the same.

All dividends are reinvested in the scenario, whatever was paid by the industrials index each year (not a set percentage).

You simply can’t know what will do better over the next 30 years. But I certainly wouldn’t be changing horses later on and paying massive capital gains tax to then invest differently, especially since that relies on favourable market prices, as opposed to just the steady dividend flows.

This strategy is perfectly fine during accumulation phase as well as retirement phase. Franking credits pay majority of the tax every year. Please see my new article here on the tax efficiency of dividend investing – https://strongmoneyaustralia.com/tax-efficient-dividend-investing-dssp/

I can’t tell you what strategy to follow, but pick the one you feel the most comfortable with and one that you can stick with over the long term. Importantly, pick a strategy that you’ll still be happy with when the markets are down.

A fantastic Web site, this is a great article, thanks Dave and Peter this is so informative, I can’t put it down since I discovered it a couple of weeks ago. I own AFIC and ARGO and love the dividends I’ve received, I’m also looking at MLT later in the year. Keep up the great work guys.

Thanks for the feedback Don, glad you like it and great to have you here!

I’m loving the dividends too around this time of year 🙂

Hi Dave and Peter,

This article is great and the comments are just as helpful.

I have read PT’s book and believe this is a sound investment strategy, also.

Keep up the great work. Its much appreciated.

Thanks for reading Steven 🙂

Hi Dave, do you use DRP for your LICs or you do take the cash payment and then pay more LICs when you want to?

Did Peter mention what he does? From memory I thought I read somewhere he takes a cash payment.

Hi Jacqui, I rarely use a DRP unless there’s a decent discount. I prefer to take the cash and decide what to do with it. But reinvesting your dividends automatically is still an excellent way to do it! Less effort and no cost 🙂

From memory Peter takes cash and invests manually as well.

That would make an interesting poll question ?

I am new to this and currently have ARG and BKI. I have elected for DRP for both… simply as a set and forget plus to avoid the brokerage….which I accept is not much.

That’s a great way of doing it Ian! It’s likely to offer just as good a result with less effort, some of us just like the control over where to reinvest the dividends, that’s all.

I love the DRP worth my AFI, ARG, as I’m only 12 months into these shares I’ve already topped up a couple of times. Might look at some more as they have dropped in the last month.

No one rule fits all with DRP is my view. Completely dependent on personal situation.

I personally reinvest all returns but via DSSP & BSP as all I hold is AFI & WHF and am saving 9% tax this way. Works for me as I never plan to sell.

Currently researching some global options which I plan to start adding in late 2019 which I currently think I will accept dividends & invest manually.

Works for me but still open to adjusting my plan as I learn.

Thanks again Dave for the great site, genuinely get excited when I get the email notifying a new post! Keep it up my man!

Good stuff Paul, sounds like it’s working for you 🙂

And thanks for the kind words, I really appreciate it!

Hey dude,

This particular interview is my go to bible. It put be at ease when he advised he does not care too much around the politics of franking credits. I was a bit worried I must say.

I’ve saved it in my bookmarks and I’ve also got it stamped on our Whats-app LIC group I have with a couple of mates.

Enjoy the blog and look forward to the ongoing posts.

Cheers

Cheers II, that’s awesome!

Yeah I think everyone’s initial reaction is ‘holy shit that’s bad’, but then we need to take a step back and relax and see if there’s anything worth changing in our portfolio and whether it really means we should change our strategy. For me, the answer is a solid, no.

Things will change over time, income tax rates, business tax rates, a million other things, but if we just stay focused on that growing income stream over the next 50 years, I think we’ll be just fine. Thanks for reading 🙂

A silly / quick question if I may.

I currently have shares in a couple of LIC’s (BKI, ARG) and have elected the DRP for both. I just purchased another parcel in BKI today. Will there be a need to fill out anther DRP election form or will dividends for the new parcel of shares automatically go to the DRP because of the current DRP election that is in place ?

There’s no silly questions mate – we all come into this world knowing exactly the same amount – zero!

You won’t need to fill out another form, your dividends from the whole shareholding should continue to be reinvested via DRP, even as you buy more shares.

It’s one setting for your entire holding, so there’s no need to do anything. Assuming of course, you’re investing all under the one name.

I am just logging on to my Sharesight account and I actually dread looking at it lately! It is a constant sea of red everywhere I turn! I only have AFI, ARG + TLS but they have all copped a fair hiding this year. I’ve just been buying the 2 x LIC’s at market (I really like them but I seem to have bought them before this crazy market dip we are having at the moment) and also TLS (copped a decent whack there!)

As it stands, my total portfolio return is -8.11% with a capital gain figure of -11.15% and income gain figure of +3.04%.

I have only really started investing over the last year and a bit and I do like the safety of just buying LIC’s and have committed to buying AFI, ARG or MLT whenever I gather up $5k – which ever one is trading at a discount or close to the NTA. I have read somewhere that if you plan to hold for the long term, then the capital gain section of the portfolio doesn’t really matter if you are investing for income for future use 20-25 years down the track? Did Peter make any comment on this at all?

Just after some insight! Would welcome any feedback here. Is my portfolio shot?! Does it really matter for the long term? What does one do when your feel your being blanketed in red?!

Chris, as discussed by email, here are some thoughts for you…

1. It’s actually a blessing that you’re experiencing this now, rather than when your portfolio is huge. The market falls every now and then, that’s just what happens, so the first time you experience it, clearly it’s not as painful with less money invested.

2. You’re noticing how it’s not much fun to check your portfolio because it’s red. So stop checking it 🙂 Now I know it’s easier said than done, but seriously, the movements aren’t important – you’ll only drive yourself mad by watching it – or worse, convince yourself that shares are a bad idea and sell.

3. You’re spot on – it really doesn’t matter for those of us taking an income approach. We don’t need the market to go up to reach our goals. We only need to keep saving money, buy shares, collect dividends and reinvest. Over time dividends will increase with company profits which will speed up our progress. The market prices are a distraction.

4. I actually now look at the share price falls and smile. Honestly. Because as prices go down, we can buy all these Aussie companies at cheaper prices than before. And as a result we get a higher dividend yield too. Over the next 30 years the ASX will grow with the economy and share prices will eventually go up, but for now, we’d prefer them to actually stay where they are, or even fall, because we’re going to be buying lots and lots of shares over that time. So wouldn’t it be better if they were cheaper?

I feel your pain and it’s so common. It’s just a matter of getting used to it and retraining our brain that it’s actually a good thing. There’s more than a few things Warren Buffett has said about preferring prices to go down than up over time, and aiming to buy more when they are down.

Hope this stuff is helpful Chris. I’ll write a full blog post with my thoughts on it which hopefully can serve as a guiding light to come back to when you get nervous. Whatever happens, stick with your investment plan! You’ll be thankful you did in 10 years time.

Hello Chris, I started buying shares in 1987 ,just before the crash. I have been through many corrections and crashes since. At first it was hard to sleep as I watched my savings fall in value, but now I see corrections/crashes as part of the deal.

As Dave said, as prices fall, the dividend yield rises, and presents an excellent opportunity to add to your investment. The tricky bit is having some investable cash up your sleeve because no one rings a bell at the bottom of the market , and as the 2007 crash taught me, you have to just keep investing all the way down, even after everyone has given up and sold out.

Hang in there, because the markets having a clearance sale and the bargains could get bigger.