Welcome to a new series!

Where I take some recent reader questions, and do my best to answer them.

Basically, I’m stealing this idea from fellow blogger Aussie Firebug, because it’s genius! (I’ve already asked and he said it’s okay!) 😉

Since I’m replying to reader’s emails and helping where I can, instead of replying one-on-one, why not share that with everyone for maximum efficiency?!

Especially since many similar questions keep popping up, so now many more people can benefit.

Disclaimer: This is not financial advice, it’s for general information only and you’re solely responsible for your own choices. As always, do your own research before making financial decisions.

Hi there,

Hope you had a great Xmas and Happy New Year.

We have been busy buying LICs with the market being down. I have also been looking at A-REITS as some of them have good yields.

What are your ideas on this?

Regards, Lennie

Thanks very much, happy new year to you too!

Firstly, nice job with your continued buying while the market is down.

Real Estate Investment Trusts (REITs) are an interesting question. We do own a couple of REITs in our own portfolio, but I don’t necessarily recommend it for everyone for a few reasons.

For one, it’s taking individual stock risk. By choosing a couple of companies to put money into, is obviously higher risk than choosing a diversified fund like an index fund or LIC.

REITs tend to carry a modest level of debt. If management get a bit carried away or a bit sloppy in terms of managing this risk, it can have a dramatic effect on the company and on the income paid.

Many REITs struggled to get through the GFC. Some didn’t make it. And a number had to severely cut dividends. In fact, the REIT index was down by something like 80% because so many were over-leveraged, couldn’t get more credit and had to dump assets at low prices to meet loans that were coming due.

Since then, they seem to have cleaned up their act a bit, with more modest levels of debt and more sustainable dividends.

But we do already own some REITs inside the LICs we invest in. And REITs also make up around 8% of the ASX300, so there’s a fair bit of exposure already for those who own an Aussie index fund like VAS.

That said, some of the yields are quite attractive and many have been providing growing income streams for a while now, which is why we own a couple. But one issue is, unless you make them a large part of your portfolio the extra yield isn’t going to do much for your overall portfolio yield and income.

Let’s say you have 10% of your portfolio in REITs paying a 7% yield. And the rest of your portfolio is paying a 5% yield. This means you’re only getting an extra 2% yield on 10% of your portfolio.

This increases your portfolio yield by 0.2%. Not bad, but maybe not worth the increased risk. Plus the portfolio becomes less simple to manage and creates more mental clutter. Maybe I’ve just talked myself out of owning individual REITs? Haha!

Basically, if you really want to follow the companies closely and keep it as a small part of the portfolio, it’s probably fine for a bit of extra yield. But most people are likely better off sticking to the simple diversified funds that already pay very healthy dividends.

(After-thought: other high yield options include buying shares in BKI, or perhaps trying out Peer-to-Peer Lending)

Hope that helps Lennie!

Hi. My investment strategy is now income/dividend focused.

Do you have a post on your exact portfolio? Or general advice on what percentage to

invest into each LIC?

Thanks for the great content.

Kind regards, Jason

Glad you like the blog!

I don’t have a post on my portfolio, but I’m considering doing one soon. Not because it’s the best portfolio, but just to share my thinking as it grows and as I learn more, and maybe that’ll be useful for people.

I’ve actually made some small changes recently, and likely will continue to do so, mostly to make it simpler and more enjoyable to manage.

There’s no magic formula. Basically, I think it works well if one chooses a few funds they like and dedicates a certain percentage to each.

It really depends what one is comfortable with. Some have no issue putting everything into one or two LICs. But I’m not one of those people. For whatever reason, I prefer to have more than that – it’s just what I’m more comfortable with.

If sticking with large LICs or an index fund, I think it’s fine to put a hefty percentage in each, and doing it equal weight is the simplest way. There’s a ‘portfolio building’ post coming soon, because I think that might be useful, so stay tuned for that!

Don’t worry too much about the breakdown. Basically, you want to get exposure to a large portfolio of Aussie shares. Whether you choose an index fund or a couple of LICs, and in what proportions, it doesn’t matter too much.

If including other things like a small/mid cap LIC, then a smaller percentage in that would be sensible I think, due to higher fees. And if you want overseas shares, then that’s pretty simple – I’d just go for Vanguard’s VGS in that case, in whatever amount you desire.

Hope that helps a bit for now. And I’ll get working on those posts!

Hi David,

Last time VAS dividends were approx 112c per share (for the quarter), this time 71c.

I’m not at the stage where I’m relying on dividends for survival, but I’m wondering whether this is usual and / or consistent across dividend payers this quarter (e.g. such as the LICs you talk about) or due to something else?

I’m new to this so happy to be pointed in the general direction of an answer to read up on myself if this is a stupid question…

Cheers,

Craig

Hi Craig, Happy New Year!

That’s not a stupid question at all! Took me a while to get around the index dividends as well.

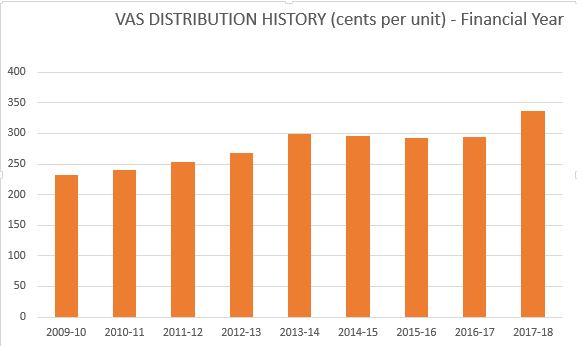

But we have to look at it on a year by year basis. And how I measure it is in financial years, as that’s how companies operate.

Looking at these figures, in the Financial Year 2016-17, VAS paid distributions of 294 cents per-unit. And during the 2017-18, it paid dividends of 337 cents per-unit.

Maybe think of it this way…

In any 3 month period, VAS will pay every dollar of dividends it receives from the companies in the ASX 300. Since most companies pay dividends every 6 months, and many pay during different months from each other, these dividends fall in different 3 month periods.

And from year to year, the same company will pay the dividend on a different week or maybe even month. That sometimes causes it to fall in a different quarter than last year. That’s why the quarter-to-quarter payments move around a bit.

Bottom line: every 3 months, we’re just getting whatever the largest 300 Aussie companies paid in dividends during that time. Over the 12 months it all evens out and VAS passes through everything it receives.

Here’s how it looks on an annual basis, for each financial year since VAS was created…

The difference with LICs is, they collect all the dividends over a 6 month period (from approx 100 holdings) and decide on a dividend to pay shareholders after that.

This gives more of a smoothing effect with dividends remaining very consistent over time. Not that it’s necessarily better, just different. Some people like this feature, and some don’t.

Hope that helps Craig, and thanks for reading the blog!

Just want to start of by saying you are really doing great by blogging

your experience.

My financial status in few lines is as below:

Our total income is less than $180k. We are recent immigrants to this country. We bought a house a year back in suburban Victoria, within our means. Also have an offset account.

After mortgage and other expenses, we still end up saving around $2k per month. We allocate it to things like emergency account, house maintenance funds, baby fund – expecting our first born in April 🙂

We have no other debt (credit card, car loans etc.) I’ve managed to save $2k just for investing into something.

From different blogs, it seems quite good to get into ETF or LICs, so my question to you would be – is $2k good enough to start investing in an ETF, considering the fees etc. I can allocate around $100 per month to this fund. Do you have any suggestions?

I will take any suggestion only as a general advice, and will not hold you accountable for any losses. Good luck with your blog. I’ll definitely recommend your blog to my friends.

Thanks a lot. Ally

Hi Ally,

Congratulations on getting yourself setup well already. You’re off to a good start, and by learning more about this stuff your future will be even better!

As for fees, they’re based on a percentage of your investment.

So, with a fee of 0.14% for example – like for Vanguard’s Aussie index fund, or a low-cost investment company like AFIC – your $2k investment would be charged $2.80 per year in fees.

And if you had $20k invested, your fees would be $28 per year. So it’s all relative to how much you have invested.

You could definitely start with $2k and buy a parcel of whichever ETF or LIC you like. But after that I would only buy in minimum parcels of at least $1k or $2k because you’re paying around $10 brokerage each time. So get started and then work on building at least $1k for the next parcel.

Hope that helps. All the best with your plans, and thanks so much for sharing the blog with your friends!

Hi mate,

Great blog and have been going through the backlog of posts. I’m also from Perth!

Quick question – whats your portfolio now? Do you provide info on allocation across LICs and the numbers out of interest? And do you still own any property?

Cheers mate. Tristan

Thanks for going back through all the posts, nice work!

Yep still living in Perth – in Wanneroo. Moved here from Scarborough last year.

Our situation is very messy right now unfortunately, so I don’t think it’d be much help. A fair bit (35-40% of net worth) is still in property. We’re slowly selling these down over time as mentioned before on the blog.

Then we have a fair bit (20%) in cash. This is for us to live on, to fund the remaining properties, and to invest monthly into shares. This gives us flexibility on when to sell properties, while dollar-cost-averaging into shares.

Also, we have some (10%) in RateSetter. I like it because it’s something different and enjoy the high yield monthly payments. For those interested, I wrote about RateSetter and Peer-to-Peer lending here.

And the rest is in shares (30%), which will eventually grow to become the majority of the portfolio in time.

I don’t provide specific guidance as I don’t think it’s really needed (but I can’t anyway!).

The LICs I discuss are mostly ones we’ve personally invested in and which I think are a solid choice for someone looking to setup an investment income stream for financial independence.

I feel that either a couple of LICs, an index fund, or a combination of both is all that’s really needed to meet our goals. So I’d suggest others at least consider something similar. In my view, specific amounts in each don’t matter much, as they’re all similar in some ways.

As for numbers, I don’t provide the exact numbers just out of privacy reasons, but you can get an idea from the story of my journey on the About page.

Cheers, and thanks for reading!

Hopefully you enjoyed this post and some of you found it helpful. Reader’s names have been changed to protect their privacy 🙂

Remember, the point isn’t to follow my advice. It’s simply to share more of my thinking, to hopefully clear up common queries and allow readers to evaluate things for themselves.

As always, you can send me a question through my Contact Page, and I’ll do my best to answer it. Thanks for reading!

Now it’s your turn… how would you answer these questions? Have you got any additional insights to share?

Why deliberate spending is my favourite money management style. What it really means and how you can use it as your situation and priorities change over time.

My thoughts on ‘The Great Taking’. An idea that the masses will lose untold amounts of wealth in the next financial crash, due to a deliberate plan by mysterious figures.

Get my latest content and thoughts straight to your inbox.

A fresh dose of financial motivation to power your journey.

What a great service to the community, and I’m glad Aussie Firebug isn’t the only one doing this!

Ally’s question is one that comes up a lot, and I think you’re right. I worry a bit when I read people saying that you ought to save up a minimum $10 k before thinking about investing in an ETF or fund. While it minimises fees, it also denies the psychological benefits of just starting. Most starts will be imperfect in hindsight, but they set us on a road to more knowledge and better results. Six month of learning by actually being in the market and energised to learn more is much better in my view than optimising down to the lowest brokerage fee as a % of what is invested.

I’d be really interested to see your portfolio numbers, particular as you’re transitioning your types of investment, I think that would be intriguing for many others to see as well as so many people start in property as well.

Thanks FI Explorer!

Absolutely – couldn’t agree with you more on that point. I think investing smaller amounts regularly is far more motivating, builds momentum and keeps you reminded of and focused on your goals. Getting started, experiencing the market moves and then building the habit of regular buying is worth a lot.

It’s unlikely I’ll be sharing the numbers quite like you do, but I might share percentages and give a general overview of what’s going on behind the scenes 🙂

re: REIT’s….the risk is a bit overhyped IMO, sure I wouldnt make them more than 10% of my portfolio but you have to look at what type of REIT’s they are and not double up on the same type. ie I wouldnt own 3-4 REIT’s that specialise in Office building’s only. You want your REIT’s to be diversified and to cover different sectors ie healthcare buildings, childcare centres, industrial , storage space etc. Look at the balance sheet too, dont buy the ones with a truckload of debt and also look at the ones that have a good long history of paying divvies and increasing them. The GFC did a lot of good for REIT’s, it got rid off the dodgy ones and also made the ones that survived clean up their operations and balance sheets.

REIT’s are a bit like the banks and the Wilson LIC’s…they cop a slagging every week for different reasons from the share advisory services and the Financial planners but you look in those advisors own portfolio’s and its NSR, ARF, CMA,AVN etc as well as NAB, WBC, WAM, WAX etc….that are part of their own portfolio’s. They know if those easy to understand no brainer high yield stocks are doing well then income investors dont need FP’s, Active Fundies to do their stock picking for them and pay high fees for

little effort.

Most REITS pay quarterly which can be handy and if Bill( i want to short change you on your franking credits) Shorten get’s his way then I expect more punters to look at AREIT’s for the extra yield.

IMO they are part of every good balanced income portfolio but like Chocolate you dont want to over do them and view them as a side dish to your main course stocks.

Rant over…..

Thanks for the comment Mark, some good points there 🙂

I guess the other issue with REITs is the payout is usually close to 100% of earnings. Leaving less wiggle room should income drop or debt costs rise and lead to less sustainable dividends. We’re in a pretty good environment for REITs really, with interest rates being low and stable for quite a while.

Yep I think you’re right – people (mostly retirees) will be looking for yield elsewhere if franking refunds are axed. A few REITs in the portfolio are fine for those with the interest in it and find them appealing.

They payout 100% because they have to legally as they are a trust structure.

Thanks Aleks, I understand why they do it. My point is, with a typical company a decent chunk of earnings is reinvested to grow future earnings, leading to a higher earnings growth rate and higher dividend growth rate over time. And the 100% payout means higher chance of dividend cut vs a lower payout from a company. So these things need to be considered also.

Awesome post mate as always…

Enjoyed the read..

Cheers mate!

Hi Dave, thanks for putting the time and effort into your blogs, I am getting quite a lot out of it.

I have been gaining confidence and moving towards income investing and away from growth stocks.

I hold some ARG, BKI, MLT WHF

I would be pleased to have your thoughts on WAM and WAX .?

Great to hear Kym – thanks for reading!

While I do own some of those LICs, I wouldn’t be buying them today. In short – They trade at high premiums, and I’m generally more cautious towards high fee funds these days.

Hey Dave,

I appreciate the blogs, very informative indeed.

I have a question about those of us who actually do not want to retire early.. (probably a vast minority haha)

My question relates to tax efficiency over the long term, because this is an area I am yet to comprehend. Would Aussies index funds like VAS trump a more dividend focused LIC over the long term (due to tax efficiency) if you were planning on working in a higher income bracket over the long term?

Only wondering because it seems throughout these (very well written) blogs, the focus on a dividend income stream is more applicable to only those wanting to retire early.

Thanks for the reply!

All the best for your future endeavors.

Thanks Keelan – interesting question!

For someone continuing to work for the foreseeable future and who may be on a relatively higher tax bracket (because they’re continually investing and investment income will keep growing), I think using a Dividend Substitution Share Plan (as offered by AFIC and Whitefield) would be more tax efficient over a very long time frame. Tax is effectively capped at 30% for the foreseeable future in this scenario, which is very attractive, even if they go on to slightly underperform the market. I wrote about these plans in this post.

This way there’s still exposure to a large portfolio of Aussie shares (which is the goal) and it’s very tax effective. If there’s no interest in using these plans, then all else being equal VAS will probably be slightly more efficient than LICs due to even lower turnover (less selling in the portfolio).

I’d probably also add an international index fund (like VGS) if I was planning on never retiring and simply keep accumulating shares – the dividend yield is lower, so growth should be higher. A combination of these two things is probably what I’d choose. Hope that helps 🙂

Hi there Dave. Great posts. Loving your content.

In terms of tax considerations would also be keen to hear your thoughts on investment bonds. Considering you pay no capital gains if held for 10 years and can add to these each year I think they have some merit.

For me the only drawback is a slightly higher fee(still under 1% if you shop around) but given the tax benefits thinks this outweighs the fee if held for at least 10 years.

I also haven’t seen much discussion on these in the few fire blogs I have read but know the barefoot investor has mentioned in his book.

Thanks.

Hey, great to hear you’re enjoying it.

I can’t help you out there as I don’t know much about investment bonds, they don’t seem all that simple to be honest so I tend to avoid. They may well be incredible, but I’m not aware of anyone making them a significant part of their portfolio (Barefoot included) so maybe that tells us something. I prefer to keep it simple and stick with what I know 🙂

If looking for higher than normal tax efficiency I’d probably just go for a DSSP/BSP as offered by AFIC/Whitefield. The much higher fee vs AFIC may compound to dilute a fair chunk of the benefit of it being capital gains tax free after 10 years.

I believe Aussie Firebug did an article (or podcast) about this a while ago. Maybe have a snoop around for that. Thanks for reading!

Great concept for a post Dave (doesn’t matter if someone else gave you the inspiration!) – awesome to hear people’s specific questions and have these shared more broadly – ends up helping more people, which is what this is all about right! (with appropriate disclaimers of course!).

Cheers, Frankie

Thanks Frankie – exactly! Why just keep it between two people when many, many more may be wondering the same things and can possibly benefit too 🙂

Hi Strong Money,

What are your thoughts about the future of index funds which the founder Jack Bogle was somewhat worried about?

Hi Shaquille.

Well Jack was concerned mostly about these large asset managers owning a huge portion of the stockmarket and giving them too much power. I don’t know the answer to that of course, but it would seem that these asset managers like Vanguard, StateStreet etc. are unlikely to act against shareholders long term interests because they’re the ultimate long term investor giving they rarely sell.

I believe that some of these asset managers already talk to large company CEOs and boards and do their bit to make sure the long term interests of shareholders are kept front of mind. And with Vanguard being a not-for-profit, it’s unlikely anything nasty is going to happen – if the others change their stripes, people can take their funds and go to Vanguard. But who knows, it’s still a risk, albeit probably a very small one. I don’t worry about it is the short answer!

Thanks for sharing your thoughts and explanations. You learn something new everyday.

Cheers

Thanks for reading mate!