The 4% rule has been discussed endlessly in the FIRE community over the years.

And for good reason. It’s important to know what returns we can expect from our investments to keep everything humming along in the wonderful world of early retirement.

The 4% rule has been covered from all angles, with people suggesting it’s too optimistic or too pessimistic.

Well, today I want to share another point of view. I think much of the debate actually ignores the most important factor when it comes to financial independence and living off your wealth. And I’m calling it: Your flex rate.

Everyone has their own personal flex rate. And it’s unbelievably powerful, yet for some reason, goes mostly ignored. In this post, I’ll explain:

— What the hell your flex rate is, and why it helps maximise your long term freedom while ensuring you don’t run out of money.

— Why lack of flexibility is causing unnecessary fears, leading to more wasted years in the workforce, giving up freedom to an unsatisfying job.

— How being adaptable can be a million-dollar skill up your sleeve (or at least half-a-million).

— Why we have more control than we think over our long term financial independence.

— How to adapt this ‘flex rate’ factor to your own situation using a nifty calculator.

On top of that, you’ll even get some ranty vibes coming through (it’s been a while!). So, get comfy (maybe grab a coffee?), because this is a meaty post. Let’s get into it!

Throughout this blog, I’ve been a big proponent of people remaining flexible with their finances, before and after reaching financial independence.

In my view, it’s a core pillar of financial strength (and personal strength for that matter), both of which are at the heart of this blog.

It’s also the reason why I have zero financial fears in my life, despite the Strong Money household not being ultra-wealthy, still having a pile of property-related debt, and having no qualifications to fall back on. I did have a forklift ticket, but it’s expired 😉

And while I understand the fears around leaving full-time work, there are people in the FIRE community who are millionaires or multi-millionaires, have hit their ‘number’ and are still worried about running out of money. As if somehow they’ll be forced to watch their accounts evaporating and their lifestyle disintegrating into rags and breadcrumbs like a slow-motion train wreck, as they look on helplessly and unable to do anything about it.

Well, dear readers, I have excellent news! This fear is completely unwarranted, and the power to control your financial independence is back in your hands. Until recently, I could only offer simple calculations and some logical principles to help you achieve this. But not long ago I stumbled upon a calculator which had exactly the thing I wanted to calculate!

Basically, how does my portfolio fare if I’m able to reduce spending or increase income by a certain amount when the market goes down?

The reason there are fears around living off a portfolio of shares (and the 4% rule in general) is we don’t get a guarantee.

Sometimes markets go through long periods of horrible returns. So anyone who is living off a portfolio will see their portfolio value and dividends cut (sometimes drastically) at various times.

This means you won’t get a perfectly rising and guaranteed income stream from your investments every single year (regardless of asset). One inefficient solution for this is to work longer and save more money.

An alternate solution, which I’ve heartily recommended in the past, is to simply be flexible with your spending in retirement, along with being willing to earn a little income should the situation call for it.

Intuitively, I knew this had to have a massive effect on the long term certainty of a portfolio, but I couldn’t ‘prove’ it. Until now.

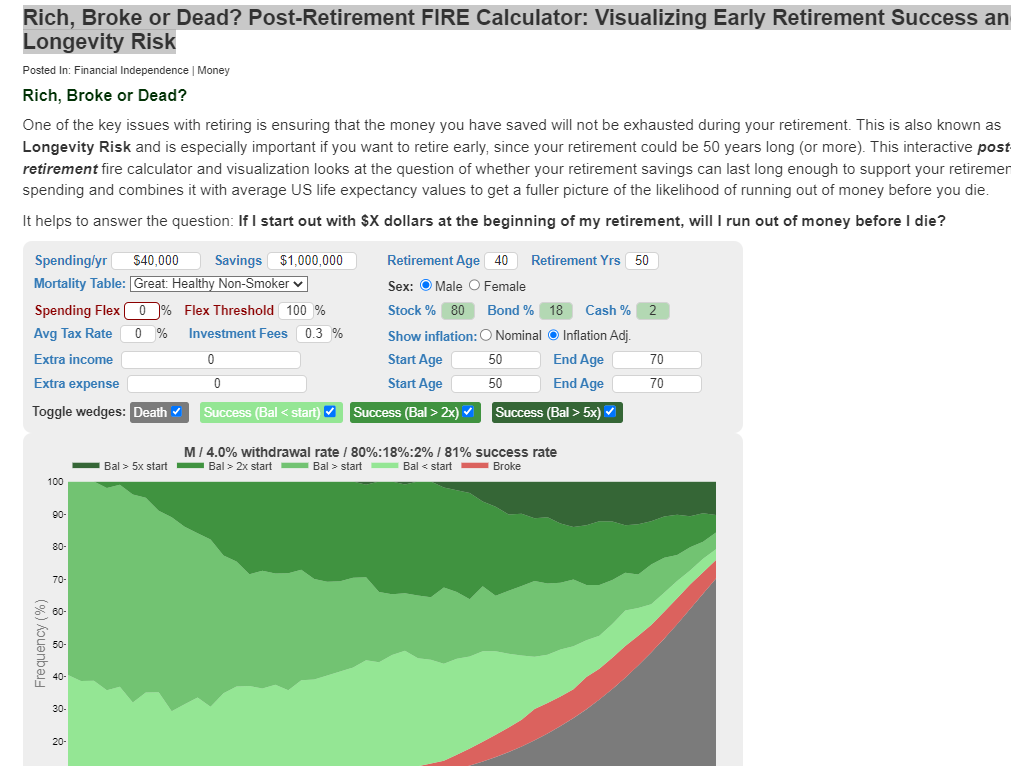

A site called Engaging Data has created a calculator with the catchy title of… “Rich, Broke or Dead? Post-Retirement Calculator: Visualizing Early Retirement Success and Longevity Risk.”

Rolls off the tongue, I know. Here’s a sneak peek.

But seriously, this calculator is fantastic. It helps put our wealth and life into proper perspective. It does this by letting you play with different inputs and timeframes to see whether you’ll end up… Rich, Broke or Dead.

Now, I know that’s a little morbid. But including mortality is actually the healthiest possible way to consider our long term future, because investing and life aren’t that different. We’re dealing with probabilities.

Go to this page to check out the calculator. You might want to play along as you read this, or just save it for later 🙂

Anyway, the reason I like this calculator so much is because it has the sweet function of adding a ‘flexibility’ component. Meaning, if you’re able and willing to reduce your spending (or make some income) when the market takes a hit, you can add this in and re-calculate your ‘success rate’ based on different levels of flexibility.

You can account for future possible income streams, like part-time work, superannuation or pension payments. You can even account for future expenses over certain time periods, and lots more.

Alright, enough of the explanations. Let’s run through some actual examples so you can see what I’m getting at, and why this is super exciting for the FIRE crowd.

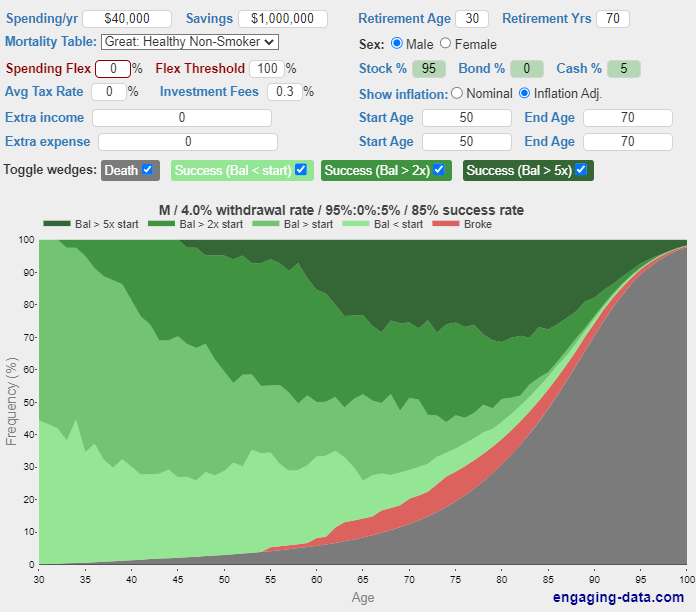

We’ll begin with a standard example (if there even is one?) of someone who retires with $1 million portfolio. By the way, for this and other examples, I’ll be using the following inputs/assumptions:

— Portfolio of 95% shares, 5% cash.

— Healthy, non-smoker.

— Investment fees of 0.3% per annum.

— Retirement age of 30.

— Retirement period of 70 years.

— $40,000 spending, adjusted for inflation (4% rule)

There are countless variables, but this is what I went with. Feel free to choose your own inputs after reading through my examples. So, given the above, how does the long term picture look for our early retiree?

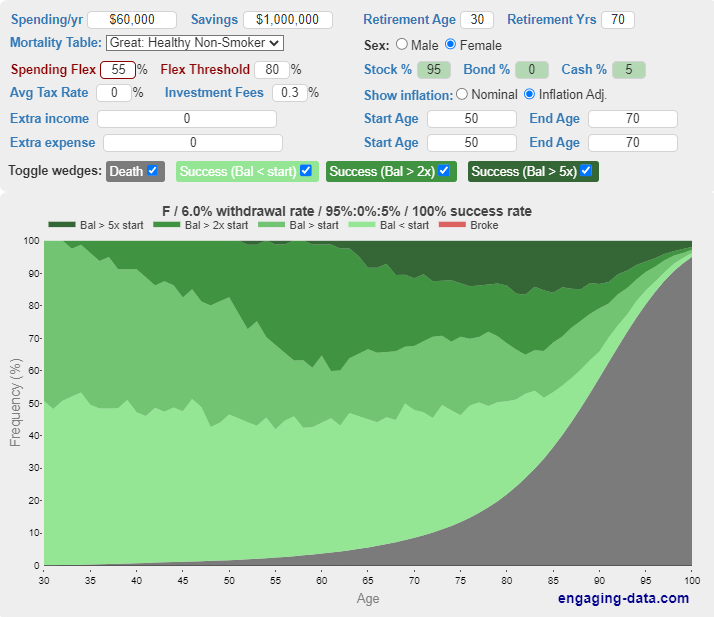

In this case, a 4% withdrawal rate had a 85% success rate. (link to this example)

This chart is overwhelmingly green, meaning wealth is intact or higher than the starting balance. You can already see that as this retiree ages, their chance of dying (in grey) is much higher than the odds of running out of money. Here, we see the overwhelming (and slightly disturbing) likelihood of ending up either rich or dead.

But the red slice is where our early retiree runs out of money in a handful of cases. This is what causes anxiety among many people. Because with a crappy stretch of returns, it’s technically possible to deplete a portfolio to zero.

Well, that’s assuming we stubbornly increase our spending every year with inflation, regardless of what’s going on. Has anyone ever actually done that? I doubt it.

And we’ll also completely ignore any superannuation, inheritance, and the government pension, which by itself is enough for most retirees (ourselves included), and would kick in around the time those Broke scenarios do.

So, in my view, we’re already being painfully pessimistic. But we’ll roll with it anyway! Let’s see how we can improve this outcome.

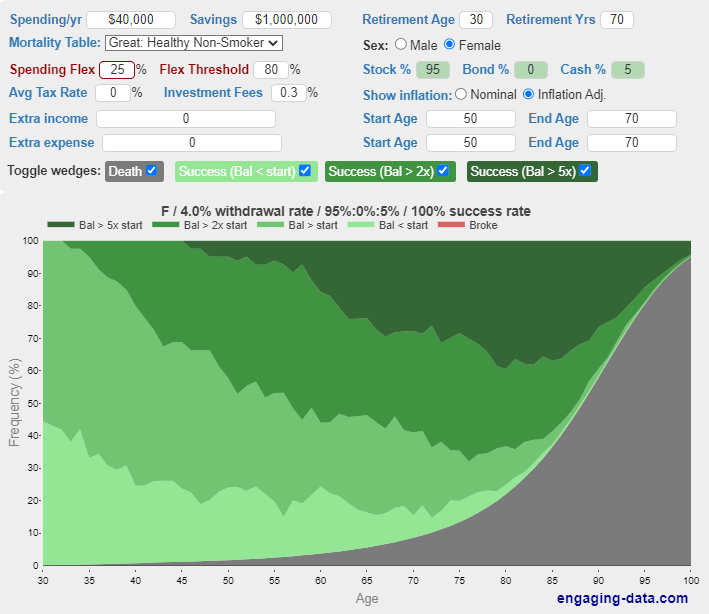

Suppose our early retiree manages to squeeze a little flexibility into their plans, to the tune of 25%.

What does this mean? With spending of $40,000 per year, this flex rate amounts to $10,000. Maybe they reduce spending for a while, or earn some part-time income.

Our retiree decides to start being flexible when their portfolio falls to 80% of its original balance, adjusted for inflation (noted as ‘flex threshold’ on the calc). Basically, if the portfolio is 20% lower than where it needs to be for their given spending and withdrawal rate, this is where the flex rate kicks in.

I’ll use this threshold for each example. I chose this level because it’s probably where a retiree would start getting nervous, and when they might consider tweaking something.

Alright, here are the updated results:

Finding: With a 25% flex rate, our early retiree basically never runs out of money with a 4% withdrawal rate. (link to this example)

(I’m using the ‘spending flex’ input for overall flexibility. It doesn’t matter where the $10,000 per year comes from – the outcome is the same. This is more useful than ‘extra income’ because that requires a fixed time period. You’re more likely to earn extra cash and spends less when the market is down, which fits better with ‘spending flex’.)

How long do you need to be flexible for? Just until your portfolio is back on track and above the 80% threshold again. Realistically, you’d likely do it until your portfolio can sustain your spending once again based on your chosen withdrawal rate.

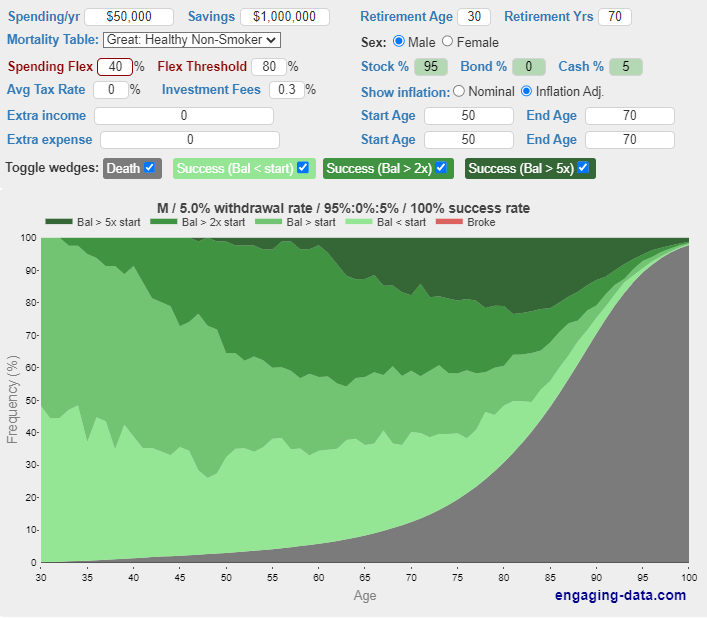

Okay, so a little flexibility gives a much better outcome. We’re feeling comforted now. But what if you have even more wiggle room? After all, many of us have a decent amount of optional expenses in our lives. Plus, more importantly, almost everyone I talk to either plans to work part-time after reaching FI, or is open to the idea.

This is where things get interesting. As it turns out, a higher level of flexibility actually enables you to live off more than 4% of your portfolio. Take a look:

Finding: With a healthy flex rate of 40%, our early retiree can live on 5% of their portfolio, essentially forever. (link to this example)

Here, the starting portfolio is the same – $1 million. And annual spending begins at $50,000. A flex rate of 40% would mean this person needs to have wiggle room of $20,000 per year.

That’s a decent chunk of change. But one person working just 15 hours (2 days) per week at $25 per hour would earn $20,000 per year. So it’s not difficult to achieve, if they wanted to keep spending the same. Side note: as of August 2021, the median hourly wage in Australia was $36 per hour.

Alright, let’s kick things up a notch. As our flexibility increases, so does the amount we’re able to spend from a portfolio when things are going smoothly.

Finding: With a flex rate of 55% and above – should we all that Arnold Flex? – our early retiree is now able to spend from their portfolio at a seemingly ludicrous rate of 6%. (link to this example)

Now, because of the bigger withdrawals from the portfolio, this likely means part-time work would become more frequent than earlier examples. But the point remains: the more we can flex our income and spending when the market is down, the 4% rule becomes increasingly and unnecessarily conservative.

Because our early retiree is spending $60,000, they need to create $33,000 of flex. Let’s say they cut spending by $6,000. Now they need $27,000 of part-time income.

That’s starting to sound like a bigger hurdle. But I’d say the majority of people who hit FI and retire early could still comfortably manage this.

For example, Mrs SMA earns slightly more than this herself from a 2 day per week government admin job. No special qualifications on her side either.

A couple would find it easy to earn $30,000 as the work can be spread across two people. $15,000 each = $300 per week = 2 days work at minimum wage (or 1 day each for well-paid work).

At this point, you’re either on board with my line of thinking, or you think I’ve lost the plot. Hopefully it’s the first one! But to show you I’m not just spouting magical numbers from some ivory tower and throwing down unachieveable challenges, let me share my own situation.

After 5 years of FI (or semi-retirement or whatever you’d call it at this point), I’ve been surprised from others and our own experience how simple it is to earn decent income doing enjoyable things.

It helps that work is naturally more enjoyable when it doesn’t take up too much of your time and energy.

Over the last couple of years we’ve ended up earning income in the ballpark of our household spending – $50,000 – with modest amounts of part-time work.

This effectively gives us a flex rate of 100%, before we even consider cutting our expenses (which we could certainly do). So, yeah, flex AF!

And we’re not alone. I’ve heard from many others in the same boat. You reach FI (or get close to it), then begin pursuing things which interest you while enjoying a generous dose of freedom and leisure, creating part-time income to the point where your investments are just kind of sitting there in the background!

At that point, the idea of running out of money becomes a source of comedy. Since you barely end up needing it in the first place! Okay, let’s summarise these findings.

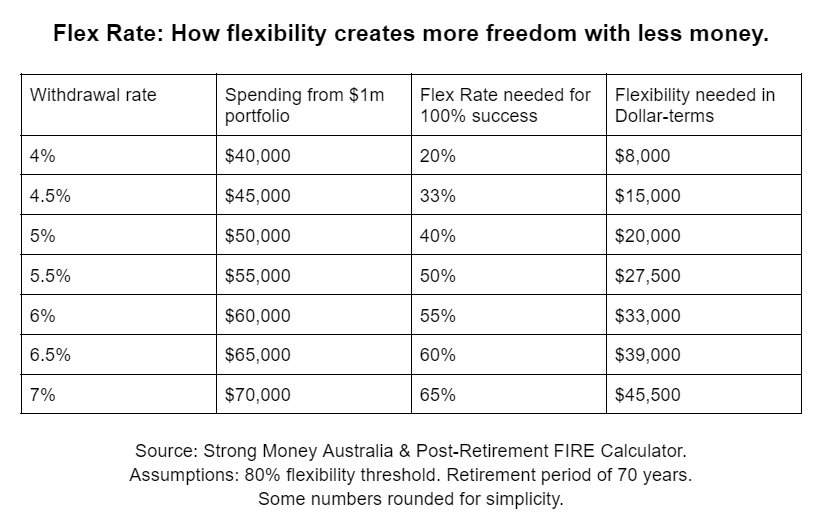

Here’s a table with different flex rates, what it means in dollar terms, and the withdrawal rate it works with.

It’s a good way to highlight the value of flexibility in action.

We can also put a tangible value on our flexibility. Having $20,000 worth of flex in your situation is essentially the same as having an extra $500,000 of shares as a backup plan.

On our FI journey, finding ways to spend less comes with a multiplier benefit of say 25x, given we then need less investments to live on. And after we reach FI, our flexibility comes with the same multiplier benefit, given it’s the same as having a higher level of investments.

The higher your flex rate, the more ‘backup value’ you have in reserve. A number that’s unseen, but very real.

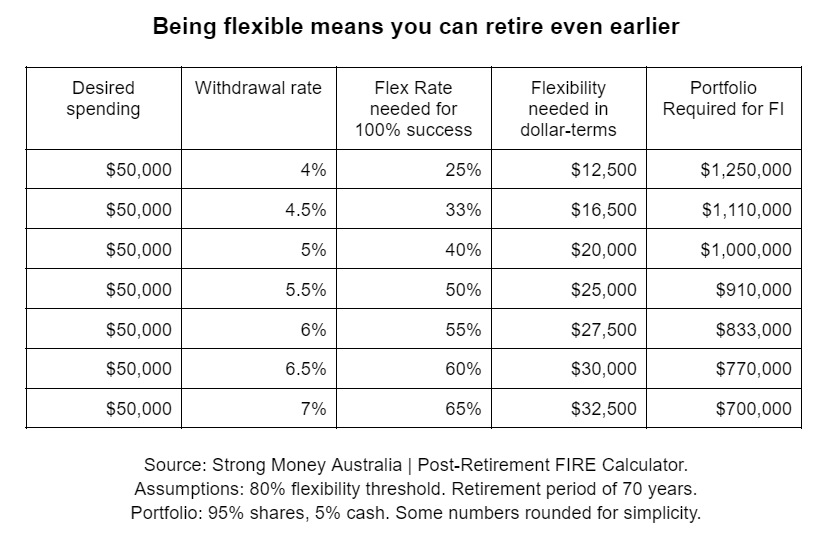

You might have already guessed what this implies, but let me spell it out anyway…

Depending on your personal flex rate, it’s entirely possible (and totally reasonable) to pull the pin on full-time work even sooner. Yes, you can confidently ‘retire’ with less than 25x your annual spending saved up!

Maybe you even pull the pin once you’ve reached 20x or just 16-17x (which equates to a withdrawal rate of 5% and 6%).

This can shave years off a typical FI journey, resulting in more freedom, for more people, sooner. That’s something which excites me tremendously!

Of course, after jumping this mental hurdle, you may seriously consider the idea of semi-retirement, a fantastic option for so many reasons I outline in this post.

All possible, once we get past our fears of not having enough money. And seeing how we can comfortably navigate the seemingly scary future, through a few simple decisions and a willingness to flex our financial muscles from time to time.

Some will say that a scenario involving part-time work or spending less means your FI plan isn’t solid enough. They’ll suggest it means you’re retiring too soon, without enough savings.

With a warm inner glow, you can ignore these comments. It means you’re a sensible human being who values your life and freedom more than giving up your best years in order to chase the slippery slope of greater safety and security.

It also means you can smile and scroll past the next article you see on “Why the 4% rule is not safe enough”, and how it should be 3%, or 2%, or whatever overly conservative and pessimistic nonsense is being blurted out.

Because, at the end of the day, you know that while you can’t control the market, you are in complete control of your personal actions and how you manage your income and expenses for the remainder of your life. And that, as we can see, is what truly drives a successful outcome.

If you read enough investing websites and chat forums, you might have noticed something. Investors who focus on living solely off dividend income don’t seem to have this fear of running out of money.

Why? Because dividends fall during recessions. So the investor naturally receives less income from the portfolio and has to make it up in other ways (spare cash, reduced spending, earn income, etc.).

In this way, there’s a form of forced flexibility built into the strategy, and because no shares are being sold, the investor knows the portfolio will never hit zero.

That doesn’t make it a magical strategy, but it does offer a built-in level of psychological certainty that often goes overlooked.

By the way, I created a spreadsheet to keep tabs on our annual dividend income as things change. I’ve used it for years as a way to help me plan my finances. Get it below.

Investors living off rental property income are in a similar boat. When rents take a hit, or they have an extended vacancy and unexpected repairs, they simply adapt and live off less income for a while, until things get back to normal.

The power in maintaining a healthy flex rate applies across the board, regardless of your chosen investments. You go with the flow and adapt.

Regular retirees are applying this strategy all the time without the need for a fancy calculator. Hell, everyday people are doing it too. When their situation changes due to job loss, health issues, whatever.

Humans have been adapting to their environment forever. Why would that change? To twist a Naval quote, you’re just a monkey with some savings.

Look, there’s probably a subset of the FIRE crowd who are drawn to financial independence due to the desire for safety and security. That’s fair enough. But in many cases, these people are still driven by a subtle and nagging underlying fear of not having enough money.

So, despite my best attempts, they may not absorb this message. The walls of their cocoon of worry are too strong to hear outside voices.

In my view, two reasons:

1– Because it’s not very sophisticated. It’s not intellectually stimulating, so the finance nerds aren’t really interested in it.

Far more exciting to debate future returns using market history across all countries and time periods, scraping together questionable data from 200 years ago.

Then plug all that into a spreadsheet with 127 columns and proceed to model 2,304 different asset allocation portfolios, tweak it using dozens of indicators and market valuation metrics, elaborate tactical and rebalancing strategies, testing various factors against each other, all in an effort to come up with the optimal answer to present to you.

But in all seriousness, the more likely reason this angle isn’t covered is…

2– Because it’s not the answer people want. Even if it’s the best answer, having to take action personally (and – gasp! – maybe make a few small changes every now and then) is not the solution people want.

It’s like saying the answer to staying in good physical shape is to remain active, keep a careful eye on your nutrition, and adjust your approach based on results.

Funnily enough, I’m suggesting you do the financial equivalent of this (not a coincidence). So, even if these are the best solutions, ain’t nobody wanna hear that shit!

Give us the pill, the secret diet plan, the magical exercise routine, the guru with all the answers. But for the love of god, don’t give us a simple logical answer!

So there it is. How to secure your finances and prolong your investments forever in one simple factor.

On the FIRE journey, the most important factor is your savings rate. In retirement, the most important factor is your flex rate.

Flexibility really does equal freedom. It allows you to retire with more confidence and greater peace of mind, knowing you have far more power over your situation than many assume.

It almost doesn’t matter what the market does. With a healthy flex rate, you’re moving with the environment. It’s a way to be prudent and conservative without working year after year until you finally feel safe (hint: you never will because you’ll keep moving the target).

By taking charge this way, you create a titanium layer of financial strength that can see you through the worst of times. And in doing so, you basically guarantee a happy and prosperous future, backed by your own ability to adapt and go with the flow.

Then, you can get back to the real business of enjoying your freedom, rather than worrying about the future!

If this is all too complex, forget the numbers. Here’s the short version:

— If the market falls, spend less, earn some income, and you’ll be completely fine.

— The more flexible you are, the less you need to retire.

— The more you can flex in the bad years, the more you can spend in the good years.

I’m not saying this gives you a concrete mathematical formula to work from either. Complete certainty is an illusion.

Rather, the overall principle and the overwhelming value in flexibility is what’s important. And after preaching it for a number of years, I’m glad to have found some numbers to back it up.

If you’ve ever wondered why I seem hopelessly optimistc around early retirement and almost dismiss the idea of being financially fearful, now you can see why.

While some may quibble with returns or the finer details in practice, the concept is solid. Take an adaptive approach, and you can maintain a healthy level of wealth and maximum freedom at all times… while in the worst cases, still being in a position of mostly-retired.

More importantly, that freedom comes much sooner than slogging it out another decade for extra cushion “just in case.” Here, the benefit is front-loaded, when your life is most precious. Because, as the calculator reminds us, those future years aren’t guaranteed.

If you know someone struggling with fears around the 4% rule, or think more people need to know the power of flexibility, please share this post with them.

WANT MORE PRACTICAL NO BS FINANCE CONTENT EVERY WEEK?

Join thousands of readers and subscribe to the Strong Money Newsletter below.

Here are some resources you may find useful on your wealth building journey:

Sharesight: A great portfolio tracking tool for share investors, and free for up to 10 holdings. It tracks all dividends, franking credits and capital gains, which is incredibly helpful at tax time. Saves me a lot of time and headache!

Mortgage broker: My personal broker of 10 years is More Than Mortgages. Highly rated and award winning, Deanna and her team been super helpful over the years and can assist with anything home loan related, including refinancing and debt recycling.

My book: After 5 years and hundreds of articles and podcasts, I decided to distill everything down into an easy to follow book. Designed as a complete roadmap to achieving financial independence and retiring early in Australia. Available in paperback, ebook, and audio.

Just so you know, if you choose to use these resources, this blog may receive a financial benefit at no extra cost to you. Thanks in advance if you do. And to be clear, I only ever recommend things I use myself and genuinely believe in 🙂

My thoughts on ‘The Great Taking’. An idea that the masses will lose untold amounts of wealth in the next financial crash, due to a deliberate plan by mysterious figures.

I explain why (and how) I bought a Tesla. The experience so far. How much it cost, and ongoing savings/expenses. Charging options + EV basics. Tax rebates + subsidies. And whether you should get an EV.

Get my latest content and thoughts straight to your inbox.

A fresh dose of financial motivation to power your journey.

Hey Dave,

Great article. Will play around with the calculator.

In Australia we might receive around 4% in distributions a year and you’re not drawing down on your portfolio. I know distributions aren’t free money but when people talk about the 4% does that include distributions? Or does it also include drawing down 4% of your portfolio yearly on top of distributions received.

Hope that questions makes sense.

Thanks

Gabe

Hey Gabe. Yes, the 4% includes dividends/distributions. As you say, in Oz we receive that in natural income alone, so it’s with international shares which are low yield/higher growth where people are typically selling off small chunks over time. Hope that helps.

I came here to ask the same question! So that means that technically a dividend investor could live off the 4% dividends plus the 4% withdrawal rate?

Smashing post btw, Dave! Love to see you’re back 🙌

Thank you Nikki 🙂

No, no, not at all. For this kind of thing, the dividends and share sales are calculated as the same thing – they both come from the total return. So 4% dividends from a company is basically the same as getting no dividends and having to sell 4% of the holding. It’s a silly comparison, but hope you get the idea.

That calculator, together with your lived experience, should provide an added degree of comfort to those considering how much ‘is enough’. Thanks for sharing with the community Dave and for another excellent article.

Cheers Glenn, happy you enjoyed it 🙂

Definitely! I think people will be hard-pressed to find examples of early retirees from the FIRE community running into financial problems. And I don’t expect that to change in the future, even if we have a prolonged shitty market environment. Because of so many reasons, the worries are unfounded.

Hi Dave, I agree that there is a very high price for safety and it’s largely an illusion anyway. Put me in the camp of liking your new format. You are our Aussie MMM. You aren’t just talking about early retirement like 99.9% of FIRE bloggers – you are actually living it!

Thanks mate – very kind of you to compare me to MMM!

Great article and I am going to enjoy the calculator.

For a long time I have hated hearing those ‘4% rule failure’ articles that treat the 4% guideline as some set in concrete rule that cannot be modified.

Flexibility is fundamental with any plan, unfortunately there is no singular statement or rule that a reader can stamp onto their portfolio and adhere to. It is a concept that we need to explore individually but the majority of people seem to want a fixed hard rule to follow. Whether that is to absolve themselves of blame if it doesn’t work or because they have no self confidence I don’t know.

Haha well said Mango!

And same here – never really been able to stomach that style of content. It’s always overly pessimistic, doesn’t line up with any kind of lived reality and is void of all imagination. It also only focuses on risk of running out of money, but never the real cost of foregone freedom to amass more money in an attempt to be ‘safe’.

Interesting stuff thanks for sharing.

I also found that your current age and how long you will be retired make a big difference in these numbers when I played with it.

I am not sure if you noticed but there is quite a difference between the Female and Male settings.

Men do not live not as long as Females. The current average male lifespan is 83 years old.

I did a check on your examples, I changed the calculation to live to 90 (above the average) and not 100 as you used in your examples. E.g I set retirement years to be 60 years.

This made a huge difference. In your initial example. Changing the setting to be Male and being retired for 60 years gave a 100% success rate.

So, in example One, If you remove all flexibility but lowing the retirement years to 60. The 4% rule has a 100% success rate based on living to 90.

I found this very interesting.

That’s interesting, nice finding. I ran a few other simulations, but obviously the possible options are limitless so I did stop after a while!

I did notice the longevity differences, which makes sense given females can expect longer life expectancy. Even more so that highlights the opportunity cost of staying in full-time work and foregoing freedom longer than is necessary! I typically try to pick pretty conservative examples to cover all bases, hence picking an extremely long retirement and a ‘risky’ portfolio of 95% shares. Glad you’re enjoying the calculator 🙂

of course averages are just averages and LOTS of people are different to average like my father who is 92 and well.

Hey Dave,

Long time reader, first time commenter! Firstly glad to see you back blogging!

I really enjoyed this article, you articulated flexibility in early retirement in a way it seems like an absolute no brainer. Using the calculator to do some quick calculations it looks like I can shave $300,000 off my FIRE number and more importantly probably retire years earlier by simply bringing in a bit of flexibility in to my retirement plan. thank you, thank you, thank you!

ps thanks for saving the turtles

Hey LF, thanks for reading & for the comment!

That’s absolutely incredible, congratulations 🥳 And you’re very welcome – it’s exactly the reason I felt compelled to write about this topic! By the way, I just updated the post with a new table which helps highlight how it can change our FIRE number. Under the section “what it means for the FI community”.

Brilliant article Dave. Loved it. This should be the final chapter in your book!! The power of flexibility and adaptability… And the link between physical fitness and financial fitness… You’re a legend!

Haha! There will be a section on flexibility/adaptability in the ‘living off a portfolio’ section, given how important it is, but not as much detail as here. Great to hear Jeff, and thanks as always!

Fantastic article, have been missing hearing you on the podcast! Just curious how would super get incorporated into this calculator – could you consider it or include it as extra income based on a forecast balance / drawdown from age 60? As a 41 year old with a healthy super balance it’s making me consider options to pay myself in life dividends sooner

Thanks! Tricky question. You could include super in the portfolio number if that’s how you plan to approach it personally, but adding it to later years using the ‘extra income’ tab may be the more accurate way to calculate it. Either way, for many ppl with a portfolio outside + inside super, some type of semi-retirement is usually very easily achieved, especially when a half-decent dose of flexibility is applied.

I consider taxable investments and superannuation investments all part of my portfolio. I will just be accessing the taxable investments first because I won’t be able to access superannuation for another 10-15 years. But it’s all one big investment

This article has blown my mind. You have explained it soo well as well (a podcast discussion on this would have been gold but understand why you guys no longer do fire and chill – dam u ASIC), but thank you for sharing this concept. I have spent quite a lot of time thinking about how much is enough and when to fire an this article

I have bookmarked this page as I’m going to need to it a few times for it to sink in. I might even have to print it out and laminate it. Thanks once again for sharing this concept.

Honestly Aly, this article is very likely against the rules. But it felt worth the risk to share this information, because I feel it’s such an underappreciated aspect of FIRE. I’m glad you got value from it!

Great post! This alings well with some of Mrs Flamingo’s writing on living life now vs delaying gratification. She is a big proponent of flexibility and part time work as well. I doubt the hardcore FIREys care can be convinced by anything, but I reckon semi-fi might be the way to go. Thanks for this post and the calc link.

Cheers Ric 🙂 Semi-FI has a lot going for it – makes the numbers easier, the lifestyle transition + the mental game too.

Ah yes, Mrs Flamingo has done a great job spreading the good word about semi-retirement and the mindset behind it.

Would be interesting to discuss how Real Estate fits into this equation regarding the withdrawal rate.

With real estate it’s actually extremely easy. What’s the rental income going to be after all costs are accounted for – the net cashflow? That’s the ‘withdrawal rate’ for that side of the portfolio. If one is selling down a property portfolio as we are, then it’s quite a bit more complicated. I did write a big post about living off a property portfolio while transitioning to shares (roughly what we’ve done/are doing) if you’re interested: https://strongmoneyaustralia.com/turning-equity-into-income-property-to-shares-transition-strategy/

Thanks Dave – always enjoy your articles.

Just one question: In each of your examples, the ‘Avg tax rate’ is left at zero. Does that mean these examples are net of tax? Or have I missed something?

When I plug in tax of say 32.5% it has quite a big impact on the expected outcome.

Thanks Don.

I have left tax out of the equation for simplicity. Feel free to add in your own tax rate, but remember to account for franking credits, which complicates the tax outcome further. You may pay much less tax (or no tax) than you think in retirement. I believe we covered this in a podcast on taxes, here if you’re interested.

To pay tax of 32% in retirement, you would need a personal income of $200k per person, which ignores franking credits and also ignores the capital gains discount when selling shares. The tax outcome is VERY low for a typical retiree living off a share portfolio.

Mate.

This post is epic!

Some real original thinking/findings in this bad boy.

That calculator is NEXT LEVEL.

I loved the fact that it includes the probability of death too. Really puts everything into perspective.

Keep crushing it 👊

Awww, thanks man! And YES, when we see the breakdown of colours (red for running out of money, and grey for dying), we see that everyone constantly worries about the red bit – which is the smallest part, so small it barely even exists! But nobody ever thinks about the grey bit and the life missed out on by stacking up more and more money.

Hi Dave,

Great article – who knew humans could be flexible/ adaptable!!!

As a retiree we are able to reinvest up to 25% of our dividends. This is our flex area.

Probably could have retired earlier – but it didn’t take long to accumulate – critical health event can hone your focus.

Cheers Dave

Note: Dave’s make a difference

Haha, yeah who knew right?! If you read about the 4% rule for a few days, you’d be left with the assumption we’re a bunch of drooling idiots with no capacity for making any changes whatsoever.

That’s a fantastic position to be in mate, nice work! Dave’s for the win 😉

Thank you Dave, another excellent article re-assuring myself that flexibility is so important not only in financial terms but life in general. Thank you 🙂

Absolutely Pete, and you’re very welcome!

Dave, AMAZING article! I wholeheartedly agree with everything here. As an early retire family in our 30s with 2 kids, we totally agree that flexibility is the key to all of this.

You literally nailed it with this quote:

“On the FIRE journey, the most important factor is your savings rate. In retirement, the most important factor is your flex rate.

”

Well done. Will definitely be linking this up in an upcoming blog post. Cheers!

That’s awesome Court, I love to hear situations like yours! Glad you liked the article, and thanks in advance for the future mention 😊

Great article Dave! I love how you point out that it’s so easy to bring in a bit of income a couple of days per week if reqd… And hey, who really cares what the work is, it’s not forever and doesn’t define you!

I recently saw a local job advertised for cleaning (5 x nights per week, 3 hours per night at $30 an hour). There’s your 20k per annum and it’s such a small amount out of your day I’d nearly say I’m still fully retired 🤷♂️

Exactly right Jared! I always try to be conservative with the earnings numbers given I know not everyone makes big money, but the hourly rates available are very healthy for non-technical work which doesn’t require a ton of training. $20k per year is easily achievable with equivalent of 2 days per week (like your example), and that still leaves one in the position of mostly-retired with a juicy nest-egg.

Hi Dave,

Brilliant post and love the calculator.

This has really helped me with my semi-FI way of thinking. It’s one and the same really, so it is building my confidence to forge ahead with my plans!

Thanks so much!

Hey Julie, thank you – hope you’re well by the way!

That’s fantastic to hear 🙂

with inflation and the ever increasing cost of living, good luck having an enjoyable retirement on a mere $40K per annum which is below the Australian minimum wage.

I suppose some people might be happy with that but certainly not me.

I’ve got great news Carl – you can plug YOUR OWN numbers into this calculator and test it for yourself. This post has nothing to do with telling you what level of spending is right for your particular household.

Some people are certainly happy with very little, and I say good on them – they’re able to meet their happiness needs on a lower amount of money. That’s a pretty useful skill and mindset to have I would say.

For some reason, every one of your comments comes across as a complaint in disguise. I’m not sure if that’s intentional or not, but it definitely stands out.

Great article. I retired/quit 3 years ago, at 44, with big plans to travel. Covid forced us to be flexible and adapt, so my wife worked for some time and it’s now me (part time). I’ll be honest, I do it mostly out of fear, as our spending rate has increased in retirement. The idea you discuss has always been there, but as a number’s geek I needed to see where/how to set my “guardrail”. This is really helpful.

The analogy of flexibility to stay in good physical health, really hit home for me, it makes so much sense. For example, if I’m diagnosed with something serious (the equivalent of an economic recession), guess what, I’ll do what it takes to adapt so that I recoup my health.

Thanks, and keep up the good work.

Thanks for sharing Douglas. Great way to think about it.

And I hear you with the numbers. Having this calc is handy, because as much as I can preach these principles, without lots of simulations to back it up it’s difficult to convince the numbers people 😉

Amazing content as always Dave.

Very interesting after a recent diagnosis and starting treatment shortly for cancer.

One that can potentially be cured via surgery but always the chance it may come back.

This highlights what I have been striving for and gives me more guidance to build in some flex for the future for me and the family.

Cheers

Cheers Positive! I love your outlook and focus – all the best with your treatment and future plans.

Very cool Dave, thanks for the post and for highlighting that handy calculator.

No worries Loza, glad you like it!

Thought your discussion around the psychological aspects of dividend investors should be better understood by fire participants. Many who are overly exposure to growth assets through passive etfs. It would benefit many to many greater exposure to lower volatility, higher income investments like infrastructure, property trusts and credit.

Peace of mind is greatly underestimated.

Cheers Tim.

Yeah, there’s a lot of debate around it and it always comes back to the psychological aspect of investing. It’s easy to dismiss, but from what we know about how our human mindset and behaviour, it shouldn’t be all that hard to accept alternative approaches as valid and useful in many cases, provided they still have a high likelihood of long term success.

Hi Dave

As The Psychology of Money author Morgan Housel puts it ‘Plan on your plan not going according to plan’.

Flexibility is key.

Cheers

Andrew

Haha yeah exactly!

Thanks for a great article and the link to the calculator.

My question …is there any scope to bump that up to a couples scenario for old fashioned couples like us that have finances totally intertwined.. there’s no his or hers its all ours.

I played around with a 50/50 split for both male and female…and wondered if that was close enough? Husband has already left the paid work force, I’m having trouble taking that leap of faith

Cheers GoodEgg.

That’s an interesting question. I would probably calculate both scenarios using the total portfolio and set to either Male or Female. Then you can just take the average of those results, since the only differing factor for the simulation is life expectancy.

You could also just choose your preferred retirement period which would do the same thing, so you’re pin-pointing your chosen timeframe. Don’t worry about trying to get it exact – the big broad picture is more important than the finer details.

It’s important to remember the pension (assuming you’re in Aus) is a very valuable backup plan in a worst case scenario where your personal wealth goes to zero for some crazy reason. For a couple, the govt pension is somewhere around $38k, which is like having a $1 million portfolio spitting out $35-40k in dividends which grows with inflation over time.

Im wondering why you deleted my comment? and questions

Were they inappropriate..?

Opps just found your reply…

Haha, sorry for the delay. My website is setup to hold a comment for approval if it’s from someone who hasn’t commented before, just in case its spam etc (which happens a lot)

This is my favourite bit and possibly my new mantra 🤣

Give us the pill, the secret diet plan, the magical exercise routine, the guru with all the answers. But for the love of god, don’t give us a simple logical answer!

Keep up the good work encouraging people to (occasionally) have to work to live rather than working to live!

Haha thanks Brenda, glad you like my little rant!

Very interesting article! While I agree with the principal, I can’t quite shake the feeling that some of it is over-optimistic. Maybe I’m one of those who can never be convinced 😅

As you’ve mentioned in the post, the flexibility would have to come from either earning extra income or reducing expenses.

On earning extra income: if the stock market has just crashed, the economy is likely entering into recession. Finding a job may not be easy in that environment? Also, for older folks or those with health troubles, picking up work could put a real dent into their quality of life.

On reducing expenses: for me at least, the “minimum” 25% cut would mean

cutting *all* discretionary expenses or moving to cheaper housing. For folks who are already living frugally, are 25-65% expense reductions really feasible without significantly degrading quality of life?

Sorry for the negativity – hopefully someone can assuage these fears!

Cheers, James

Thanks James. If you agree with the principal, then that’s the main point – end of story 😁

The details are, funnily enough, flexible. Everyone gets to create a Flex Rate they are comfortable with. And if not, then be prepared to work longer before cashing in on freedom. It’s worth noting that if you go this route, the extra work is continuing + mandatory, whereas with the flex scenario, extra work is only required in crappy scenarios (many times you wouldn’t have to use it). Depends on the numbers of course.

It’s true that the number of jobs in a recession will be less (that’s *if* we’re in a recession, which by itself is uncommon, especially so during the early stages of one’s early retirement). But this is when part-time roles are more common than full-time roles as companies try to save money. Older folks still have the government pension should their investments start becoming depleted, which is healthy amount and ignored for these examples.

Thinking in probabilities helps. The chance of everything turning to shit is already incredibly low, then if PT income fails it’s much lower again, then if cutting expenses fails it’s much lower again, on and on. Remember, if you start depleting your portfolio, you can always do part-time work *after* the economy starts recovering and jobs become available. Then you have control over how long you work nd how you massage the numbers to get back to where you want to be. There are countless ways you could approach it, all up to the individual.

On expenses, it’s different for everyone. You’re assuming zero work is possible and a reliance solely on cost cutting. I would never claim a case for cutting expenses by 65% is a realistic scenario, and I absolutely do think that for already frugal people this would impact quality of life. Those people will obviously not choose to aim for 65% flex based on cost cutting alone, will they?

You seem to be painting extreme scenarios to what are already pessimistic cases, all while hoping for minimum inconvenience (that’s fear working its magic). I’m not sure these fears can be cured, as your mind can always come up with new situations and reasons why it won’t work. It might feel conservative, safe etc, but it keeps you locked in a full-time job, so the cost of this supposed safety is your freedom and all the life/experiences/enjoyment you could’ve had by realising how well-positioned someone must be to consider these examples in the first place.

These fears are really unfortunate and it’s something I’m really trying to make progress on. All I can think of is the life missed out on due to these fears, which goes unseen and uncalculated by the worriers. The foregone freedom is a LARGE + GUARANTEED cost versus the incredibly small chance that everything goes horribly wrong and for some reason you’re unable to do anything about it whatsoever (which sounds like a ridiculous tradeoff to me).

Hope these replies don’t sound too harsh. Thanks for your comment, and all the best! 🙂

While I wouldn’t want to use flex fi skills as much in my 60s or older. I definitely have the ability to be flexible if I retire late 40s to pick up some extra work.

I would be tempted to grind out 2 months of full time work though, so I could get back to my life 😎

Going full-time for a short period, like contract work or something, is an interesting way to do it. Get back to freedom ASAP, I like it 😉

I love this! I can’t stop running scenarios with the calculator… I think I have a problem. 😉

Haha! Well as far as problems go, it’s a good one to have 😁

Took me a while to comment (the joys of full time employment!) but thank you so much for writing this post and giving such a thorough explanation of how to use that amazing gem of a calculator you found! It’s a great way to have more confidence that you can retire on less (even though it is also common sense, as you said. We FIRE people do get obsessed with the numbers and graphs 😀).

I was getting depressingly red results until I put my retirement age as my current age, then added extra income (take home pay) for a few more years, as well as a later income stream from super and reduced living expenses after paying off the mortgage. Now it’s a lot more green, hooray!

Not sure if you’ve read Die with Zero, but since reading that book I do agree that the 4% rule might be too conservative for me. I don’t want to hoard wealth which keeps growing forever, but to have just enough to live a good life as soon as possible. I’d rather risk wasting my money than my life, as that author says. The grey death curve on the graph is a good, sobering reminder of that.

Thanks for your comment Lily! Really glad you like the post and finding it useful thinking about different scenarios, fantastic to hear.

I haven’t read Die with Zero, it’s on the list tho 🙂 That’s a good way to frame it – for some reason people seem hell-bent on optimising for maximum money rather than freedom and life.

I have been scrolling meticulously to see if Die with Zero is raised – thanks Lilly!

Dave, 100% read it, it’s well along with your thinking around flex, and really goes to the crux of the psychological aspects related to death, big health scares etc and prioritises “net fulfilment over net wealth”. Also has a few interesting calculators such as the spend curve to help you understand that your spend is also no linear as you age etc.

Thanks for this article, and appreciate your candor.

Thanks for that Kirsty, I definitely will! 🙂

The quality of your website and the content is amazing, well done – I need to read more of it.

Would you agree that by owning LIC’s like AFIC, you also have a built-in flex rate due to flat dividend payments based on cents per share? For example: I buy 100,000 LIC shares at $10 per. Each share pays $0.40 distribution. The economy collapses due to Corona 2 / GFC 3 / Negative gearing blow up etc… AND the value of 100,000 shares halves with each share now worth $5.00. I still have 100,000 shares generating $0.40 dividend per share each year, so my income from dividends remains at $40,000 per year.

Thanks Andrew!

Well, with that kind of example, living off dividends with LICs comes with its own form of forced flexibility. As dividends get cut, the LIC may hold its dividend steady, but is only able to begin increasing again once its earnings catch up, which depends on the dividends paid by companies in the portfolio. If dividends for the ASX kept falling though, at some point, the LIC runs out of built-up reserves and franking credits and is forced to cut dividends (possibly sharply). So it has its limits.

Overall, a smoother income can help as a form of stability to retirement, and I know multiple retirees who think of it that way and are very happy with the approach… despite risk of underperformance etc.

Dave,

You’ve nailed it with this article, and the linked calculator blew me away.

So refreshing to have the same ‘common sense’ message, now with a probability calculator. This is amazing.

Thanks for sharing your amazing thoughts. I got so much from this one!

Keep up the effort!

Cheers Matthew! That’s fantastic feedback, I really appreciate it.

This flexibility thing is a super important concept that has been bugging me for a long time, so it’s great to have found a way to flesh it out like this.

Another great post Dave, been following you for awhile you have a real talent for this. Will probably buy your book when it’s out, I have motivated money, I am a disciple of Peter (guru) thornhill. 👍

Thanks for following along Billy, great to hear you’re enjoying the posts 🙂

After all, we are just Monkeys with a plan old mate 👍. Good read and love the calculator.

Dave, you and this article got a shout out on chooseFI this week. Nice one!

Oh that’s pretty cool! What did they say? Hopefully it was positive 😁