While there’s no official start date, the modern FIRE movement is probably around a decade old at this point.

A wave of enthusiasm and optimism around a new life path spread once the wise words of Mr Money Mustache and JL Collins started catching on in the US.

In Australia, however, it took a few more years before bloggers like Aussie Firebug, Pat the Shuffler, and others like myself sprouted up.

Because while the fundamental message is the same – optimise the shit out of your spending, increase your earnings, and use all this spare cashflow to build investments and create freedom – the game plan needs to be adapted for the conditions of each country.

There’s a surprising number of ways in which Australia and the US differ. Sometimes Aussies are confused by reading US blogs and wonder what the hell they’re talking about.

In this article, we’ll run through what the differences are, and what we should keep in mind when creating our own path to FI in Australia.

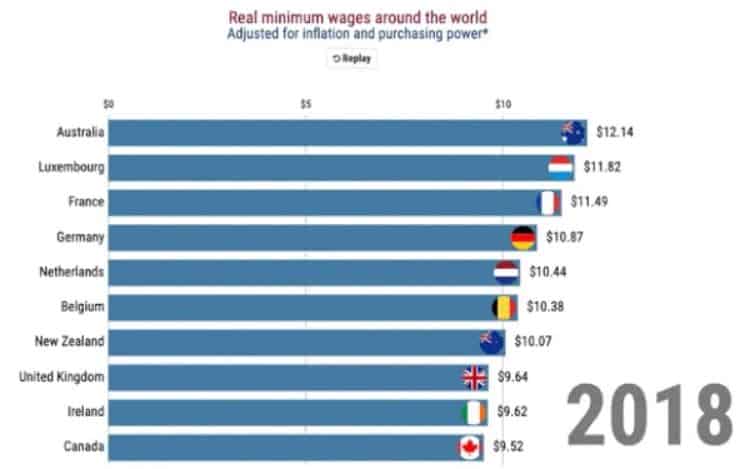

One noticeable difference between the US and Australia is in incomes. We tend to have a much larger middle class, where the majority of people make pretty decent incomes.

A big driver of the difference is our minimum wage being much higher than in the US. Even when compared on an equal basis using international standards, Australia has among the highest minimum wages in the world.

Now, these figures aren’t super-recent. But Australia has remained among the top of the list, after several more years of healthy increases to the minimum wage.

In the US, however, low wages are really low. Which shouldn’t be a surprise – we know inequality is an increasingly sensitive issue due to extreme differences in incomes and wealth from top to bottom.

Related to this, a lot of people who would earn relatively low wages in the US – like factory workers, labourers, those in social services, and office admin jobs – are paid much better here. Very, very few people as a percentage of the population actually earn minimum wage (just 2% according to see this article).

My own work history of labouring and warehouse work is a great example of this. All relatively low skilled and non-technical jobs. But I was paid a good bit higher than minimum wage. In the US, I would’ve undoubtedly earned a pretty modest income. But in Australia, I was able to earn well, with penalty rates and overtime making helping me almost reach six figures.

Now sure, we don’t have as many big fancy tech companies where people can earn huge salaries and get rich off stock options alone. But overall, I’d say it’s easier here for the average person to earn a strong income compared to the US.

In many ways, the cost of living is connected to wages, given the price we pay for almost everything has labour cost as a large input. This means, yes, our cost of living here is typically higher than folks in the US.

Add to that, housing in Australia is typically more expensive. Don’t get me wrong, the US has some expensive housing in their bigger, more popular cities. These costs are multiplied further by everyone there choosing to constantly dine at restaurants, go to shows and events, and so on.

That’s not most of the country though, as I understand it, so let’s leave the exceptions aside.

One key difference in Australia is that we don’t have an abundance of lower cost cities to choose from. Whereas the US has plenty of decent sized cities with local economies of their own, with housing available for well under $300k (even a bunch under $200k).

Now yes, we do have regional cities which offer great quality of life and are well worth checking out as capital city alternatives. Especially nowadays, where so much work is done online, it creates more opportunity for remote work. But at the end of the day, most Aussies live in large capital cities and that isn’t changing anytime soon. So, despite it being our choice, it does mean housing costs are likely to be more of a challenge here in Oz.

Overall, I’d say for those in the US skilled enough to earn decent incomes, they definitely have an edge over us by having plenty of more affordable and economically viable cities to choose from.

The differences here are chalk and cheese.

I won’t pretend to know the ins and outs of either health system. But suffice to say, the US is a complicated and expensive mess, where healthcare costs more than it should.

For this reason, citizens are essentially forced to have insurance or face enormous out of pocket costs for hospital visits.

In Australia though, we have more of a choice. We have the relatively wonderful public healthcare system, where most things are covered by Medicare (funded by our taxes).

While many argue how suboptimal our system is, I don’t think any right-minded Aussie would trade it for what the US has. Something to keep in mind.

Of course, we can also choose to pay for private insurance which comes with additional perks and coverage. This is tax efficient in many cases where a family can have better healthcare options at a slightly higher cost (vs paying the Medicare levy).

For those of us who are happy to accept the benefits and drawbacks, we can elect to pay nothing (for most things) and use the public health system.

The particular strategies for individuals aren’t important here. It all boils down to the fact that, for practical purposes, the average Aussie has a lower cost of healthcare than our friends in the US, regardless of insurance or not.

Another key difference between the two countries is in government support for traditional retirees.

Both systems are relatively complex, so I’m forced to simplify for the sake of this article.

In the US, full retirement social security payments start from age 67. But you can also elect to start receiving smaller payments from age 62.

Here’s the part that will sound strange to Aussie ears: the payments also differ depending on how much you earned during your career!

Higher earners receive a higher social security payment than lower earners. This sounds pretty unfair on the surface. But it’s because they’ve typically paid much more tax over their lifetime. It’s a very different system!

Over there, social security is funded from payroll taxes. It’s seems to not be seen as a welfare system but a retirement system. Payments also scale up depending on years of work, starting from 11 years of employment (people who’ve worked less than that don’t get social security!).

There’s also no means testing. So a billionaire can (and will) receive social security upon retirement age, as bizarre as that sounds. Unless they voluntarily choose to opt out of it.

There’s yet another quirk of the US system. You can choose to delay receiving your social security payments up to age 70. If you do, you’ll actually receive more for every month you wait. I think this is a great option to have – a neat form of delayed gratification.

In Australia, from age 65-67 we’ll get a government pension regardless of how much we earned (or tax we’ve paid) during our lives. Everyone gets more or less the same amount, but there are limits. If we’ve built up a decent sized investment portfolio, those benefits will taper off and eventually disappear. Which makes sense – we don’t need them at a certain point.

Thankfully, if our investments turn to shit and deplete, we’ll then gain access to a pension income stream to help with the bills. While many argue relentlessly that it’s not enough or the rules are unfair, I think overall we do have a fairer and simpler pension system than the US.

Super for Aussies and 401k’s in the US serve the same purpose: for an employee to build up retirement savings through a combination of employer-funded contributions as well as their own.

We’ll gloss over the details of each particular system, because again, neither is all that straightforward. But here are some key differences…

Superannuation is a compulsory system, whereas my understanding is 401k is voluntary. Super is not accessible until age 60 or so, while 401k’s can be cashed out.

Superannuation is taxed when money goes in, investment returns are taxed, but it’s tax-free on the way out. On the other hand, a 401k allows for tax-free contributions, no taxes on investment returns, and is only taxed on the way out. Though I think there are other options (Roth 401k), where you put in after-tax dollars, there are no taxes on returns, and you can also withdraw tax-free. You can also withdraw the money after a minimum of 5 years.

Superannuation also comes with a set minimum percentage that the employer must pay, mandated by the government (currently 10.5%, heading to 12% by 2025/26). 401k’s seem to run with no set rates. Instead, employers offer to ‘match’ an employee’s contributions up to percentage of income.

Overall, I think most Aussies are better off with the superannuation system. On the other hand, from an early retirement perspective, a few of us would love to have access to the money like US workers do. It would also be possible for savvy people to retire even sooner if they received higher wages instead of superannuation.

As for property investing, again, things are very different.

Because of the many cheaper US cities I mentioned earlier, real estate over there tends to be very cashflow friendly.

It’s not uncommon to see US investors talking about rental yields (which they call ‘cap rates’) of 10%. In fact, this article lists a casual sample of markets around the US where the monthly rent is 0.8% of the price or higher. Some light reading tells me there’s more where that came from, with many being in average non-expensive areas, rather than slums.

As an Aussie, that’s absolutely mindblowing! Over here, as you all know, property is more about capital growth. Our real estate tends to have very low yield – usually 3-4% – and lower after costs. Sure, some markets are a decent bit higher, but they’re often questionable and still not even close to what the US has.

Another difference is mortgages. In the US, most mortgages are typically a fixed interest rate over 30 years. Imagine signing up for 30 years with a rate of 3% or so, as many folks did in recent times. That gives great certainty to homeowners, and for investors, that’s far less than the rental yields available.

Think about how good that is for a moment. These people were literally locking in a strong positive cashflow stream which will increase over time. even if it was 100% leveraged. Printing money.

Basically, US property is mostly high cashflow, lower growth. Aussie property is typically low cashflow, higher growth.

Which is better for FI?

Starting from scratch, property in the US will generally give you a good passive faster than stocks will. In Australia, it’s the opposite, where property is usually terrible for cashflow and shares are fantastic.

If I was in the US, I would most likely invest solely in cashflow real estate to build financial independence. It looks to me like the fastest way to create freedom. After retiring, I’d then look at diversifying into the stock market.

This might throw people off, as many assume I’m anti property. Not at all. I’m all about choosing the asset best matched for a specific goal and timeframe.

In this area, the two countries are once again opposite to each other.

The US is fundamentally a low yield, higher growth market. Australia is a high yield, lower growth market. This is partly due to the tax treatment in each country.

US tax rules make it more efficient for companies to pay less in dividends and instead use that cash to buy back shares (which increases earnings per-share leading to higher capital growth). Here, it’s more tax efficient for companies to pay higher dividends, so they can pass on the franking credits generated by the tax they’ve paid. Otherwise all those tax credits are wasted.

Even the makeup of the two stock markets are completely different. The US is dominated by relatively exciting technology companies. Australia is dominated by relatively boring old school industries like banking and mining.

Interestingly, both the US and Aussie stock markets have been among the top performing markets over the last 100+ years. But overall, we could probably agree that the US is broader and more diversified, with loads of innovative and dominant multinational companies. I guess that’s why the US market typically trades at a more expensive valuation than most developed countries.

We can see the many ways in which our countries differ for the average person chasing financial independence. But what’s the same?

I actually think the main similarities have to do with us as people, and our culture. We tend to have the same sense of entitlement, and the same unrealistic expectations.

We think that life should be easy. That we should earn lots of money without too much skill, training, effort, or time sacrifice. And we should be able to live a fantastic life, enjoying ALL the benefits of an affluent modern world, but the bill for this should be low enough so that we still have plenty of cash leftover to amass an impressive portfolio of investments.

We also have the same assumptions that spending less money leads to a miserable life. And that saving lots of money leaves us with a sad and boring existence.

Most of us don’t think for ourselves, instead believing what we see in the media, and accepting what everyone else does as ‘normal’. Only a tiny percentage of self-motivated individuals will ever have the courage and independence of mind to go their own way and create a different life from the masses.

We get sucked into the same psychological traps of marketing, slick advertising and peer pressure, making us buy a whole bunch of shit we don’t need in order to feel like we’re cool and we fit in. In turn, we’re trapped in jobs we don’t really like, unable to imagine life any other way.

Modern day self-inflicted slavery.

As intelligent and advanced as the world has become, the only thing that hasn’t really advanced, mentally speaking, is us. In fact, if anything, we’re regressing into a mindless state, lulled into a drooling hypnotic trance by technology and short-term dopamine hits.

Anyway…

Overall, I’d say the average Aussie has it better than the average American. Most of us are comfortably middle class and we have relatively low amounts of poverty.

This means we’ve been cushioned from seeing many people in real hardship. The US has more poor people and less generous safety nets. But this also means we can lose perspective.

It means we’ve drastically lowered the benchmark for what qualifies as ‘struggling’ and ‘just getting by’. These words are thrown around so much to the point where, in my mind, they’ve lost all meaning. ‘Just getting by’ is simply another way of saying ‘I spend everything I have’.

Sometimes it’s genuine and the person is buying nothing but essentials. But many times, if not most, it’s an optional outcome. By that I mean it could be improved with knowledge and better choices.

I’m not saying that to attack these people, merely to back up the point that our perception of hardship has changed dramatically over the last few generations.

Okay, all that was perhaps a little cynical and negative. Let’s bring it back to an important question.

Taking everything into account, I think it’s probably about the same for most people.

The biggest standout benefit of the US for the average person is probably the lower cost of real estate across so many parts of the country.

The biggest standout benefit of Australia is probably the better wages across most industries, even for lower skilled and non technical work, and better systems in place (health, super, pension, etc).

In both cases, if you can earn a strong income (easier in Oz) while living in an affordable location (easier in US), financial independence will be MUCH easier to achieve.

Of course, there are plenty of individual cases where each country will look dramatically more attractive depending on the situation.

Here’s a little summary on which country I think is the most attractive in the various areas.

Wages: Australia

Cost of living: US

Healthcare: Australia

Pensions: Australia

Super/401k: Australia

Real estate: US

Stock market: US

I’m sure there are plenty of other ways the two countries differ. In fact, let me know what else you can think of in the comments below, or if you have a different view.

In truth, our countries, cultures and lifestyles are probably more alike than they are different – especially when it comes to achieving FI. But as you can see, there are some interesting differences to keep in mind.

Whichever country we happen to live in, the recipe for building wealth is the same.

If we make a concentrated effort to take advantage of our opportunity, then creating a life of freedom is well within reach 🔥

Here are some resources you may find useful on your wealth building journey:

Sharesight: A great portfolio tracking tool for share investors, and free for up to 10 holdings. It tracks all dividends, franking credits and capital gains, which is incredibly helpful at tax time. Saves me a lot of time and headache!

Mortgage broker: My personal broker of 10 years is More Than Mortgages. Highly rated and award winning, Deanna and her team been super helpful over the years and can assist with anything home loan related, including refinancing and debt recycling.

My book: After 5 years and hundreds of articles and podcasts, I decided to distill everything down into an easy to follow book. Designed as a complete roadmap to achieving financial independence and retiring early in Australia. Available in paperback, ebook, and audio.

Just so you know, if you choose to use these resources, this blog may receive a financial benefit. Thanks in advance if you do. To be clear, I only ever recommend things I use myself and genuinely believe in 🙂

Why deliberate spending is my favourite money management style. What it really means and how you can use it as your situation and priorities change over time.

My thoughts on ‘The Great Taking’. An idea that the masses will lose untold amounts of wealth in the next financial crash, due to a deliberate plan by mysterious figures.

Get my latest content and thoughts straight to your inbox.

A fresh dose of financial motivation to power your journey.

Hello Dave ,

Thankyou for another banger !!

I was thinking 🤔, if it’s true that the average American home has a firearm , without SAFETY (add this to your list ) , I would think it’s us Aussies who are the clear winners 👍

Cheers

Thanks Jimmy!

Haha, that’s a great point, I didn’t even think of crime etc. We definitely have greater peace of mind here in that regard.

Thanks for the insights, Dave.

A couple of personal observations from my interractions with the US middle class. (I’m an Aussie, working for a US corporate for many years) – they are far more mobile than we. It’s not a ‘big thing’ to move state for education or work. That’s linked to being a much larger, less centralised population. Say, 15 times the population, and correspondingly more cities.

As an engineering sales manager, in Autralia I could work in Melbourne or Sydney, and I might have managed Brisbane. And changing companies would not have made much difference. My counterparts in the US had nearly 30 cities to choose from, and that was just within the one company.

The Australian taxation system (CGT and stamp duty) and small population, and few cities, are a significant structural impediment to moving to improve one’s circumstances.

A facilitator: they seem to have much lower changeover costs to sell a home, and buy another. For employees, at least some of their housing and work commute costs are tax deductible. On the flip-side, the family home is a taxible asset – not CGT exempt as it is here.

Entering into a long-term housing lease is quite common. I have friends who ‘bought’ a house, except it was actually a 20 year purely commercial lease contract, with options to extend and/or convert to purchase. I think long term residential tenancy contracts might even be illegal in much of Australia, but then, they lack the residential tennacy protections that we accept here.

Cheers, Nick

Cheers for the points Nick, really interesting!

The mobility thing and choice of cities is extremely useful, because I believe tax rates are different across the cities unlike here – is that correct? Obviously makes for a much greater opportunity to get an equally good paying job in a lower cost city.

I do think they still face the same transaction costs as we do, I’ve heard about 3-6% agent’s fees etc, as it’s normal for the buyer to also have an agent (I think it’s 3% each side or something). Interest is tax deductible on the family home (or something like that?), which seems pretty odd through the Aussie lens.

Nice run down, Dave.

I think you’re absolutely right about the bar for “struggling” getting lower. We’re such a lucky country we think the slightest amount of having to rein things in is a hardship (obviously this doesn’t apply to those who are genuinely living in poverty). I think a lot of us have trouble differentiating between wants and needs.

Thanks very much!

Yeah it’s not a popular viewpoint of course, but I can’t back down from it, haha. Especially since society’s opinion seems to be moving in the opposite direction where everyone’s a victim (200k income families thinking they’re battlers and that it’s not somehow self inflicted in most cases). Apparently the Aussie battler now drives a new land cruiser, has a 4 bedroom house and a restaurant habit. It’s disrespectful to people who are genuinely living in harsh circumstances.

G’day Dave

I enjoyed your perspective,and having friends and relatives in the US I reckon your not far from the mark. I write this from my first European holiday, currently Switzerland it took myself and wife 30 years to get here and I say as to cost of living I’m never complaining about Australia again. But Wow it’s amazing here.

Cheers Peter I appreciate that 🙂

And congratulations, hope you enjoy the rest of your holiday!

Dave – interesting article. I’m a dual citizen who lived in Australia for ~10 years, but am currently living in the US. Many of your observations are spot on.

I do find your ‘fairness’ comments come from the Australian point of view. For example, from a US point of view, people who earn more should get more from US Social Security since they contributed more in the first place. In fact, you will hear US people say that the system is unfair because they deserve even more – “it’s my money afterall.”

Which brings me to the fundamental difference between the US, Australia, UK – (a personal observation, not a value statement; and there is a lot more to this than I can draw out) – The US emphasizes individual freedoms and responsibilities over community; whereas most Aussies see value in curbing their individual freedoms for the sake of community (first time I ever heard anyone say they were happy to pay their taxes because they knew it was benefiting others was in Australia). Much of the rest of your observations flow out from this fundamental difference – health care (individual responsibility to provide and take care of oneself vs community benefit); Super/401k – my money, my choice (not compulsory); Innovative / tech stock market (individual freedom to succeed or fail vs. tall poppy).

Wages are higher in the US for almost all professional classes. It is the laborer / service class that has it harder in the US (as you say). Cost of living is lower in the US, but I give the edge to Australia for Quality of Life.

My take on the biggest impediment to Financial Independence in the US is the healthcare system. US insurance is employer-based, and as such, keeps many people tied to their jobs in order to afford health insurance. And without insurance, medical bills will bankrupt you. I would take the Australian health system over the US system in a heartbeat!

All that said, the US can’t be beat IF you have the drive and ability to be a high-income earner, and the wherewithal to know when to stop.

Thanks again for your posts. Thought provoking and enjoyable.

Thanks for your thoughts Brenan, very helpful!

I totally get the US point of view regarding social security, and I tend to largely agree with it.

Your points on freedoms and responsibilities is also spot on and a very important point. It’s a mindset and value system I think. I personally fall more on the side of the American mindset, of individual responsibility as much as possible. But I do value the Aussie safety nets as they’re genuinely needed in certain cases.

The tricky part is that both systems can end up going too far – with too much selfishness on one side (US) and too little personal accountability on the other side (AUS). So it’s a delicate balance to get it right with the benefits of each, and each person will lean a slightly different way. Appreciate your insight!

Great read mate! As someone who is semi-retired at 42 and has family in the States also this is a common conversation I have with my cousins.

General living expenses I think are a fair bit cheaper in the States than Oz like food and fuel etc.

Keep up the good work 👍

Cheers Jed, glad you like the post.

Interesting to hear that from readers like yourself and others with US experience and/or family ties there, very cool. Also congrats on your semi-retirement 😉

In regard to healthcare, I am shortly to undergo what could be a six hour operation involving two surgeons – one cutting into my neck and the other into my chest in order to remove a benign growth. No way could I get into the public system in a timely manner for the treatment of this condition so private it is. While I will be out of pocket for this surgery to the tune of around $7k I’d hate to think what it would cost in the American health-care system.

Remember good peoples that as you age it costs an effing lot in order to maintain you! 🙂

Thanks for sharing SK. All the best with it and take care mate!

Thanks Dave

Some matters are rarely discussed or raised with FIRE concept. At what point should you wind up your superannuation fund or arrange for another entity to administer it? What if you’re single? What if your partner is completely disinterested?

When I was in difficulty last year I didn’t want to have anything to do with investing let alone superannuation. Sadly, those Government bureaucracies couldn’t care less about that.

This time as the surgery will be major, just in case, I have wound up the fund with in specie transfers to my personal name – and saved my beneficiaries thousands in tax as a result!!

Maybe a matter for another article by you if you haven’t already done one.

All great questions mate, none of which I’ve really thought about to be honest.

I’ll have to ponder it. I’m also probably lacking some knowledge in that area too! If you felt like writing a guest post any time in the future with points you feel are worth sharing (on super, life, anything else) I’d be delighted to publish it and help you with it if needed 🙂

Hi Dave,

Long time reader/listener – first time commenter. The articles you write are really insightful and help me on the way to reach FI. A few article suggestion I have: Given such a large portion of the Aussie population are born overseas/have parents born overseas, what are your thoughts about an article on living your FIRE-life overseas (geo-arbitrage)? As you are in WA, what portfolio does one need to live in Bali? Or in Spain? Or Thailand? What are the tax implications on your dividends, franking credits and capital gains (if one sells stock)? Just a though! Keep up the good work! Seb

Hey Sebby, thanks for your support, glad you find the content helpful.

That’s a good set of questions. I really don’t have any knowledge in that area, so it’ll require a good bit of research, but I’ve noted it down and will look into it 👍

As a dual US/Canadian citizen who grew up in the states and now lives in Canada, I agree with your comments. Australia and Canada have many more similarities than Australia and the US.

Hi Dave,

I find your comment about getting good passives started super interesting, regarding the comparison b/t the US and Australia. If you had a choice between real-estate investing in the US or shares in Australia, do you have any thoughts about which between the two might leader to faster FI?

Hey Ben. Yeah, I’ve thought about this a bit actually.

I believe high yield US real estate would definitely be a faster approach to create strong cashflow for FI. Because not only are the yields high like Aussie shares, but you also can use leverage to speed that up a bit. Plus loan rates are typically fixed for 30 years so you get good certainty over your cashflow situation too. Rents are likely to be more stable than dividends most of the time too if we’re comparing it to an index fund.

In the US, I’d probably focus on trying to make that work and then later on I’d add in stocks for diversification and growth in the background.