Most people who want to retire early have got their finances in order.

They’re heading in the right direction – saving, investing, paying down debt.

And in most ways, they’re already well-off.

Despite this, some of these folks have next to no chance of retiring anytime soon. That is, unless something changes. Why?

Because they lack one thing: Focus. Let me explain…

I don’t mean these people can’t pay attention. Or that they’re not sure of their goal – they are. What I mean is, their finances aren’t properly aligned with their goal.

Sometimes there’s an assumption that having all sorts of different investments is the most sensible thing to do. Most of us have heard the phrase, “Don’t put all your eggs in one basket.”

This totally makes sense on the surface. But some people take this too far, and end up with one egg in 27 different bloody baskets!

This might sound really safe and conservative to some people, and therefore sensible. But all baskets are not created equal. To butcher the metaphor, some baskets are better at holding (and producing more eggs) than others.

It’s fair to say that diversification means different things for all of us. But the goal of Financial Independence is the same.

As you’re about to see, taking a scattered approach to investing doesn’t really line up well with retiring early.

Let’s look at a totally made-up example to illustrate what I’m talking about. Our fictional aspiring early retirees are good savers with limited knowledge on investing.

So they used what can be called a ‘Spray & Pray’ approach to investing. They tried multiple asset classes and strategies, hoping something would ‘work’ and make them rich.

During 10-15 years of saving and investing, their investments did okay, but none amazingly well. Because of this, they often got frustrated and moved onto the next idea.

The overall focus was achieving a high net worth, but they also had nagging worries in the background about an upcoming economic downturn (clearly avid news watchers!).

For this reason, they decided to spread their eggs across lots of baskets.

This meant keeping some money in cash and bonds, as well as crypto and precious metals like gold and silver (because you never know – presumably that’d be valuable when the world collapses).

Our couple stopped short of hoarding baked beans and toilet paper though!

The goal was Financial Independence by 35. After joining forces in their early twenties, a strong savings rate allowed them to build a fantastic net worth of $1.6 million.

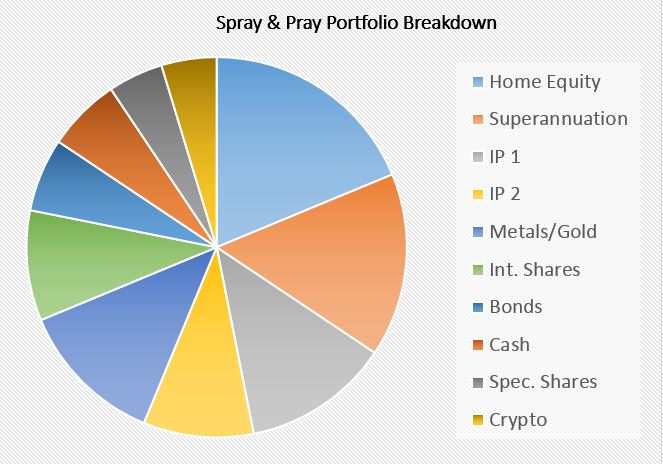

So, at age 35, are they now ready to call it quits and put their feet up for a while, before moving on to new adventures? Let’s take a look at their portfolio…

Home Equity: $300k. (value of home $600k)

Superannuation: $250k. (made extra contributions since it’s tax-effective)

Investment Property 1 Equity: $200k. (neutral cashflow)

Investment Property 2 Equity: $150k. ($5k per year cashflow negative)

Precious metals/Gold: $200k. (no income)

International shares: $150k. (pays $4k per year dividends)

Bonds: $100k. ($2k per year interest)

Cash: $100k. ($2k per year interest)

Speculative Growth shares: $75k. (no income)

Crypto/Bitcoin: $75k. (no income)

Quite a hefty spread of assets there. Here’s how it looks in chart form…

Most people would agree this couple have a very healthy net worth. And that net worth is parked in quite a diverse spread of places. Some would probably consider them hyper-diversified.

Sure, we can argue whether some assets are optimal or not. But they don’t appear to be doing anything all that crazy or reckless here.

At this point, a few astute readers will have already recognised the first issue. Despite the beefy net worth, across their whole portfolio, our couple is receiving just $3,000 per year in passive income.

Despite their enviable wealth, they’re another example of being equity rich, cashflow poor.

For completeness, let’s say they spend a total of $50k per year: $20k for their mortgage (home purchased years ago), and $30k for personal spending.

Looking at this set of spaghetti finances, I’d say not very close at all. Unless something drastic changes, that is.

Clearly, the current mix of assets doesn’t look to be getting the job done. But why is this?

First, putting extra on the mortgage saves interest, but it doesn’t improve cashflow.

So extra funds parked here earn a return, but it doesn’t change their $50k annual spending until the entire thing is paid off, which gets rid of that monthly mortgage cost.

Second, given their age (35), Superannuation won’t be accessible for the next 25-30 years. Tax-efficient for building long term wealth? Yes. Handy for retiring in your 30s? No.

Next, given the relatively high ongoing costs and low yields associated with most residential property in Australia, their investment properties aren’t very good at generating income either.

If these assets were paid-off, it would be better. But even then, the net yield will likely be quite low.

Finally, the money sitting in cash, bonds, metals, crypto and speculative shares provide very little or no income whatsoever.

So, what could they do to improve this situation? Let’s take a look.

At the broad level, what’s needed is for this couple to focus their savings on the goal of Financial Independence.

First, they could sell their metals and bonds which would basically pay off the remainder of their home mortgage. Straight away, this would knock out their $20k annual mortgage repayments.

With this one move, cashflow has improved dramatically and they now only need to cover $30k of living expenses, not $50k.

What else?

Next, I’d probably look at selling the two investment properties (IPs). As we can see, these are generating no income, yet there is a good chunk of equity sitting in there.

That looks like an opportunity to me!

So from the $350k of equity, after capital gains tax and selling fees, we’ll be conservative and assume sale proceeds of $250k.

They could also sell their bitcoin and speculative shares and raise another $150k. They could be up or down massively on these so I’ll take the middle ground and assume no tax for simplicity.

Speaking of tax, they may choose to do this process over a couple of years to minimise CGT on the properties and make the transition much less stressful.

Also, investing $50k of their $100k cash pile would improve passive income further.

In total, these changes result in $450k of cash which they can add to a more sensible income-producing share portfolio.

Our couple already have $150k of international shares. So let’s say they add Aussie shares to this and go for a split of 50/50.

How does their net worth picture look now? Let’s look at where their savings are parked and the outcome of these changes.

Home Equity: $600k. Now paid off.

Superannuation: $250k.

Aussie shares: $300k.

International shares: $300k.

Cash: $50k.

Here’s the new net worth breakdown in chart form…

As you can see, a lot less moving parts. It’s simpler overall, but there is a huge amount tied up in home equity and super.

While this might look sub-optimal for early retirement, in this case, it’s actually not detrimental. Luckily, our couple has relatively low expenses and doesn’t require a huge personal portfolio to live off.

The home equity now provides ‘paid-for’ housing. And their $600k share portfolio should sustainably provide around $24k per year in passive income.

With personal spending of $30k per year, this only leaves a cashflow gap of $6k. This means they need just $150k more in shares to retire forever.

And that would only take a couple of years to achieve from this point. What a massive turnaround from their starting position!

All by structuring their finances in a much more focused way that is 100% in line with the goal of early retirement.

Of course, they could semi-retire straight away and only need to earn a very small amount to plug the shortfall.

Another option is they could start living off a larger percentage of their portfolio by selling a few shares each year, because super is still growing in the background and will become available later on.

Of course, we can argue that they could’ve still retired with the Spray & Pray portfolio too, by selling off bits and pieces over time and living off the proceeds.

And that’s fair. In fact, it’s kinda what we’re doing ourselves.

We stopped work essentially in a negative-cashflow position and a pool of equity. We’re selling down properties over time, living off some cash and building a share portfolio simultaneously.

I outlined this strategy in the following post: Turning Equity into Income – Property-to-Shares Transition Strategy.

So yes, they could have muddled through from where they were. Retiring with a less than optimal portfolio can still be done.

But guess what? It also kinda sucks. It’s not fun to have lots of outgoings and little income. Or to be juggling a messy portfolio in retirement.

On the other hand, having low outgoings and passive income from investments is very fun! And having a simple set of finances is surprisingly fun too.

That’s why I strongly urge people to set things up simply from the start.

Another point to mention is that when you zoom out, our couple had an odd bunch of assets.

They were approaching investing half in the Armageddon-is-coming camp, and half in the Prosperous-future camp. Add to that, they also succumbed to get-rich-quick thinking from time to time.

But since these mindsets are somewhat contradictory in nature, it’s hard to build a concrete strategy by combining them. You’d be forever second-guessing different parts of it.

Before investing a single dollar into an investment, you have a choice to make. You either think the future is probably going to be pretty good, or it’s not.

If you think things will generally turn out okay, despite the ups and downs, then buying-and-holding shares and/or real estate over the course of many decades makes perfect sense.

But if you think otherwise, then investing in these assets probably isn’t for you. Instead, hoard cash, put your tin foil hat on and join the Baked Bean Brigade or the Kleenex Krew and bunker down for the coming apocalypse.

Markets are scary, I totally understand. But that’s not an excuse to listen to the doomers and load up on speculative, non-productive assets.

If you want to punt on bitcoin or gold or marijuana stocks, that’s fine. But don’t confuse this with long term goal-specific investing.

As we’ve been discussing recently, we need to remember the progress humans have made and have faith that things will continue to improve in various ways.

I’m not saying you shouldn’t have different investments in multiple asset classes. You can!

Just make sure they all combine to make a portfolio that can deliver you the income and growth you need to sustain a comfortable early retirement.

Even though this is (yet another) silly made-up example, I hope it illustrates an important point. Where we put our cash really matters!

Sometimes, having a high net worth is not enough to become financially independent.

Our portfolio must be built in line with our personal and lifestyle goals. If yours isn’t, then start taking steps in that direction.

A simple portfolio of good quality income-producing investments, and maybe a paid-off house, is where you want the majority of your long term savings to be.

Diversification and focus don’t have to be opposites.

You can still have a highly diversified portfolio, while having that portfolio intensely-focused on the goal of early retirement.

Thanks for reading!

Here are some resources you may find useful on your wealth building journey:

My book: After 5 years and hundreds of articles and podcasts, I’ve now distilled everything down into an easy to follow book. Designed as a complete roadmap to achieving financial independence and retiring early in Australia. Available in paperback, ebook, and audio.

Mortgage broker: My personal broker of 10 years is More Than Mortgages. If you’d like help refinancing or getting the right loan for your needs, get in touch with MTM. They have fantastic reviews for a reason. I’ve worked with them for 10 years and they’ve been excellent.

Sharesight: A great portfolio tracking tool for share investors, and free for up to 10 holdings. It tracks all dividends, franking credits and capital gains, which is incredibly helpful at tax time. Saves me a lot of time and headache!

Just so you know, if you choose to use these resources, this blog may receive a financial benefit at no extra cost to you. Thanks in advance if you do. And to be clear, I only ever recommend things I use myself and genuinely believe in.

I share what we’ve been up to in our 7th year of retirement. Hear about our trips and travel plans, finances, volunteering, and more.

Discover how 21-year-old Kyle, took a pay cut, switched jobs, and is setting himself up for financial independence by paying off debt, living simply, and investing for the future.

Get my latest content and thoughts straight to your inbox.

A fresh dose of financial motivation to power your journey.

Hi Dave, Enjoyed your article and you articulate clearly about the dangers of being equity rich and income poor.

My thoughts are that the traditional LICs – MLT, ARG, AFI- may not be in a position to grow their dividends in both the short and medium term (5-7 years). With the current crisis, governments around the world are printing money to keep their economies afloat. This will likely lead to deflation followed by hyperinflation. Even, Geoff Wilson, the recent staunch defender of franking credits in Australia, has changed his position in that he now believes that we cannot sustain credits refund. If the traditional LICs reduce their dividend, I suspect that many retirees who have based their retirement plan living off Aussie shares income may be in for harsh times – unable to keep pace with hyperinflation, especially if they are older or close to stopping active work. What do you think ?

Thanks Ken. Yeah it looks likely that company profits will be flat at best for a while, so dividends are more likely to go down than up!

I don’t buy the theory on deflation and hyperinflation. Many people said that was inevitable after the GFC in the US due to the huge experimental QE policy/money printing and that turned out to be completely wrong – inflation has been low and stable the whole way through.

The continued power of technology to make things cheaper, strong competition, and the low amount of spending demand is likely to mean high inflation is pretty unlikely. Times are definitely going to be tough for those who don’t have any backup plans in place or who don’t have enough savings (which is why I hammer those points repeatedly).

And you raise a good point – there will almost surely need to be higher taxes to pay for the rescue packages at the moment. Maybe that comes from franking refunds, or maybe somewhere else – nobody can say at this stage.

There is no magical asset that can save people from these issues – sharemarkets are still going to remain a sensible place for long term savings to earn any decent return to keep up with inflation when interest rates are zero.

Stay calm mate if that happens were all in it together

Do you really want to be buying overpriced gold coins etc?

Current Lics such as Milton yields 7.1% Gross, Assuming

1) Franking gets removed

2) No growth in dividend for 10 years

Taking into account that interest rate is roughly 2% on loans, and will likely stay this way for the next 5 years….

Its still a sound investment. What else would you suggest ?

Your questions are:

1) hyperinflation

2) removal of franking

3) Lics not able to grow dividend

which we all have no control of….

why dont we just focus on things that we can control….

1) change lifestyle habits to live a more frugal life and more cash flows to invest

2) work more or see if there are ways to get alternative income to buy more income-producing assets

3) if you are happy with international ETF generating less income but that makes you sleep better then do it

I do think Australia will do well over the long run, we have abundant resources, hard working and young population demographic, can be flexible around immigration laws hence can attract young talents around the world…. Good government (not perfect and do make mistakes), innovative companies that can compete on the international stage…. and also good corporate governance which means companies can raise capital and grow…

I love your posts Dave, and I agree with your thoughts on gold and bitcoin. BUT, I’m still not entirely convinced on your concentration into AU shares for cash flow.

As you rightly mentioned rebalancing out of a more diversified portfolio with a combo of Australian and International shares is as easy as it was to buy into the portfolio in the first place. Depending on personal circumstances selling small packets of shares can be optimal cf. forced dividends in terms of choosing when taxable hits occur, and in who’s name. And it’s not exactly hard to do (for someone who has probably made 100’s of share purchases over their decade to FI.

As with property, selling isn’t the only way to access equity as I’m sure you know. Using LOCs for instance offers a simple way to tap equity without realising those gains to early in the peace.

We have a cash flow neutral property, a positive property, and an Australian and International Ex. super portfolio. And while it may be more complicated, I sleep better through pandemics than if I was 100% AU. Also our nearly paid off PPOR is interest only with an offset, meaning every dollar extra in the emergency fund/offset does improve our cash flow and bring us closer to FI.

Cheers Hugo. The example here is 50/50 Oz/International, that’s not concentrated in my view. I never mentioned my approach here at all, just this example. And remember, you only need to be convinced by YOUR approach, nobody else’s.

Yes, there are a million ways to create and then manage a portfolio including this one. I had to choose something obviously for simplicity, rather than running through multiple examples. Equity can be tapped in the IPs sure, but after retirement borrowing power will be killed so refinancing will no longer be an option, so at some point there will need to be other actions taken.

So it was really about laying out a basic approach to illustrate the general message and avoid making the example overly complicated/long.

Ah yes great point on interest only with offset! Most people probably prefer not to run it that way, but I see your point on it still improving cashflow. What’s your plan during FI though? Pay it off? Can’t stay interest-only forever unless you somehow have great borrowing power after stopping work. Edit: Sorry I just re-read it’s already nearly paid off… so since it’s not a large amount it won’t matter either way.

This is one of the best articles you have written – hit the nail on the head! If we are going to achieve FIRE, then we really need to be specific about what the long-term goal is and stick to the strategy that will get us there. I talk to people all the time that change up their approach to investing on the daily. They think the world is ending so they stock up on gold bars and toilet paper, then the next minute they are dabbling in crypto and have found the next growth stock to take a punt on, then out of the blue they casually announce the purchase of an investment property, then regrettably they want to get back into shares and are asking about ETFs and LICs. It’s confusing as heck and must feel like a wild ride for them, but are these people actually getting anywhere with their financial future? Being a long-term dividend investor is boring because I already know the amount of passive income that needs to be reached and roughly how many years it will take me to get there. However, it’s important to know exactly what you are aiming for otherwise what is the point? The whole thing becomes an elaborate game that never ends.

Wow thanks Aurelia!

Oh see this is what I’m talking about – we need to invest in a goal-specific manner and understand HOW these investments are going to help us achieve the end goal. Fantastic (but sad) examples, thanks for sharing!

The funny thing about diversification is you think your capital will be protected or provides a hedge situation so that when shares tank, gold will go up or bitcoin will go up.

What this black swan has taught us is no asset is safe, Bitcoin which is perceived as a safe asset in market crashes actually did worse than shares. Gold didn’t do too well either…… investment properties? they’ve already introduced a law that you can’t kick your tenants out even if they don’t pay rent.

So the only safe asset is cash, but cash is probably the worst asset to own over the long term…..

I don’t listen to the media anymore as it will cloud my decision making, the answer is no one know what the world will be like in the next 5 – 10 years….. Media has claimed that there will be hyperinflation after GFC as governments print trillions of $$$$, well, that didn’t happen. Being Rational in investing doesn’t mean you will always get rewarded…. there are too many variables in effect, you never know what the market will focus on.

Media also claimed there will be unemployment greater than the Great depression, hopefully, this won’t happen…..

What we know is we can never underestimate the human spirit and our ability to adapt to change, Yes, the world will never be the same…but it won’t be that much different either…

In the early 1900’s, in the space of 30 years, our civilization has experienced, WW1, WW2, Spanish flu pandemic which kills millions and The Great Depression….. 30 years is not that long mate…..its amazing how we can adapt to change and come out better and stronger.

1) never try to predict the future 2) never underestimate the power of the human race 3) Save and invest consistently

Great points here Jack, thanks for sharing mate!

I don’t have anything to add 🙂

What Jack said.

I’m with you Jeff – I think Jack should start a blog 🙂

What Jack said 100%

I enjoyed reading this post. Anyone could find themselves in this position as no one is taught about investing and the pros and cons of choices while they’re in high school. So most people go about investing through trial and error, since their parents also didn’t learn anything about it.

There are millions of books out there, and property books have great points as well as stock investing books as well as gold bug bloggers. It can get confusing and it’s easy to be lead astray, especially before someone comes across the idea of FIRE which wasn’t around back when I started.

Yeah that’s very true Beth. Hopefully I wasn’t coming across as saying these people are dumb or should’ve known better – I didn’t mean that at all. As you rightly say, anyone can end up in this type of situation because comparing all the investment options and thinking about this stuff isn’t easy and doesn’t come naturally to most.

So let’s hope that more people stumble across the FI concept and the message of saving and simple long term passive investing 🙂

Occams razor: Where there are multiple solutions to a problem, the simplest solution is probably the best.

To me I take the advice of both Warren Buffett and Jack Bogle, the founder of Vanguard Index funds on this. I invest in low cost Index Funds. That way I get my fair share of the market return without having to pay “The Helpers”.

Cheers Ahjay. I heard that saying on simplicity somewhere before a while back, and it sticks in my mind from time to time – when there are two options, choose the simplest. I really like it

Hi Dave, I am selling off an IP later this year with the idea of investing the majority of the cash that this frees up into equities. I have a paid off house and a small amount (85k) invested in AU shares. My super is fairly good and is 70/30 international and AU shares. My wife is not as sold on equities as I am and would like some further diversification into property. What are your thoughts on DJRE as a small 20% component of my portfolio? It seems well diversified if a little high cost.

Hey Lunch. Sounds like you’re in a great spot already, nice work!

DJRE seems like a pretty good fund as far as a ‘property investment’ option goes. It’s very diversified and although not cheap, gives you great exposure to global REITs and a decent income if you’re into that sort of thing 😉

My only concern would be that because it’s listed it’s still going to be volatile like regular shares (has fallen quite a bit recently), so I’m not sure how your wife will feel about that? As part of a diverse portfolio though, I wouldn’t talk anyone out of it if they wanted more real estate than what is already included in ASX and global markets (which isn’t very much). Hope that’s useful 🙂

Thanks mate, I had noticed DJRE had tanked just as much as the rest of the world equities market. Appreciate your input and keep up the good work ????

Hi Dave

Thanks for another great article. If this pandemic has show anything is that world and its stock markets are truly globalised. I get a bit confused when people bag out Aus shares and their tax benefits, claiming you must have international index exposure.

As mentioned COVID has hit worldwide markets hard, I have taken some main indices and their relevant falls from the worldwide realisiation of the seriousness of COVID-19 (21Feb) to the ‘bottom’ (for now) that markets fell to (23Mar).

Dow Jones

21 Feb – 28992 points

23 Mar – 18599 points

A fall of 36 %

ASX all Ords

21 Feb – 7230 points

23 Mar – 4564 points

A fall of 37%

FTSE

21 Feb – 7403 Points

23 Mar – 4993 Points

A fall of 33%

As you can see, the All Ords fell almost the exact amount of the DOW Jones and only a few percent more then the FTSE. Either way, no matter where your held your shares, you would have lost a minimum 30% either way, the supposed exposure to the ‘rest of the world’ (yes i know their are other indices apart from the 2 main I have mentioned) has saved you next to nothing. Especially when they do not provide that high dividends and tax benefits Aussie shares do.

Another thing i don’t get is when people are like, ‘well franked dividends won’t last forever’. Hey that’s probably true, but if thats the case, all the more reason to get on the bandwagon now! Take the chocolates while there being given out people!!!

Hey David. Thanks for your comment!

It’s true, all those markets fell pretty much the same as each other in the recent selloff. One thing to remember is, the currency movement of the Aussie dollar falling would have meant a global index fund like VGS wouldn’t have fallen as much in comparison. And this (AUD falling) is what tends to happen during downturns.

I think the most convincing argument for having a healthy weighting to overseas shares is that it reduces the chances of a poor long term outcome. It’s possible for any country including Australia to struggle/underperform for a reasonably long period. So owning multiple markets has an averaging effect and smooths this out a bit. And that can help when there’s a goal in mind like FI or living off a portfolio.

While I’m comfortable with Australia long term and still enjoy investing with an income focus, I’m warmer towards international investing than I used to be and have become more flexible in my thinking.

Franking is really a bonus so if it’s taken away then so be it. It’s possible that if removed Aussie shares would take a hit to account for the loss of tax benefits, meaning there could be a future loss for investors similar in value to the amount of tax currently saved from having it in place. Net result is, jumping in for a benefit which may not last probably isn’t such a good idea. Other factors when deciding how to invest are more important I think. Hope that makes sense!

Except if you are unhedged then the fall in the AUD has softened your losses in international markets and improved the value of your international dividends.

Fair points.

As most, I feel that if franking credits ever do go, it will have a negative effect on the Aussie share marketas a whole. As an essential local industry the government will want to (and be lobbied) to protect it. How do they do this normally? By taxing the international equivalent (income and capital gains) at a higher rate (more then currently) as a deterant from moneying flowing out of the local industry.

Just something I think people overlook when they think they are one step ahead of the governments, ‘possible’ franking credit removal.

Well said , David C . Cheers , Ramon .

Hi Dave .

Thanks for a very thoughtful article . It has caused me to re-evaluate my whole portfolio .

Has anyone ever done a study of a portfolio structured on the notion of the application of an equal – weighted portfolio amongst every class of asset ?

Save on , Ramon .

Hey Ramon. Someone probably has somewhere in the world… but I haven’t got a clue where you’d find such a study. Google is your best bet!

Hi Dave,

Informative views. I’ll paste my two cent opinion from a post I made on a forum.

“…..the biggest factor I think. Yourself. Knowing whether you are influenced by the latest thing or by others and what you are going to do about that.

I ended up giving the bird to market commentators, the look at me types or what others think about my approach. They are irrelevant and an irrelevance.”

Ciao

Haha always enjoy your wise words SK! Thanks for popping by 😀

Hi Dave thanks for another great inspiring post. I was wondering what your thoughts are on comsec pocket? I’m seriously thinking about using it instead of vanguard. $2 trades under $1000 seems great to me . Happy Easter ????

Hey Luke. Don’t know much about it but it seems okay. The choices are pretty limited on there so depends on what you want to invest in. I’d prob prefer to stick with a single low cost brokerage account rather than use these smaller ones as well.

Hi Dave, I have been reading your blog for a while now and they are very informative, thanks a lot.

I start thinking about switching from Aus Super high growth option to Sunsuper 100% international shares, because it does make sense to buy aussie ETFs and cover the international ground within superannuation.

But I am also curious what are the key differences between Sunsuper 100% international shares (assuming you went with unhedged?) and investing in VGS directly. Tax benefit? or just lower management fee.

Hi Han, glad you enjoy the blog!

There is essentially zero difference between VGS and index international shares with SunSuper. The underlying investment is basically the same – covers developed global markets in one fund.

Thanks Dave, REST super also provides Australian Shares – Index and International Shares – Index, at zero investment fee. Are these two more or less the same with VAS and VGS? I can’t seem to find a whole lot of information online.

Yes, they’ll be roughly the same thing. REST use derivatives to create these funds though, which is the reason they’re able to be done at zero cost. Sunsuper & others we’re getting proper ownership of the underlying shares and the index is managed by Vanguard. Details on REST and some other near-zero indexes are a bit grey to say the least. Some mention of this in my post on super and has links to other info on there too.

Thanks Dave, I read your post and also Pat the Shuffler’s. So much information to digest and I also did some research too –

I find it interesting that when comparing performance, the Aus Super Australian Shares option or Aus Super High Growth Option is more or less the same the Sunsuper International Shares unhedged option over the last 10 years (net of investment fees and taxes), despite the higher costs (Aus Super High Growth Option has a MER of 0.59%).

Does that we should be less bothered with costs but more focusing on the return (net of investment fees and taxed)?

In some aspects yes, I wouldn’t just go for the cheapest option you can possibly find. Just to be clear, there’s no ‘best’ option, which it sounds like you might be trying to find.

For a long term investment like super, it just matters that it’s invested mostly in high growth assets like shares. I believe the reason Aus Super is more expensive is because they also own private infrastructure and real estate in their high growth funds. Any type of high growth or all-shares option with a good industry super fund will do the job – the best performing one will be dependant on the assets which have the best returns and only known in hindsight. Keep it simple and let it do its thing.

Thanks Dave, REST super also provides Australian Shares – Index and International Shares – Index, at zero investment fee. Are these two more or less the same with VAS and VGS? I can’t seem to find a whole lot of information online.

Dear Han,

Switching Super funds by choice is a big deal in my humble opinion. Before you switch, check to see if you will have the same/worse/better Insurance offerings (income protection, death and disability etc.) in the new Super fund. In addition, check the fees… Always check the fees..

hey thanks Jeff, appreciated the advice. One of the reasons i am considering to switch is Sunsuper has lower fees. I am actually planning to work overseas for a few years so not sure if i should be too bothered with insurance offerings ????

Could be a good idea to obtain taxation advice from a qualified professional about making or receiving from your employer super contribuions while working overseas. Can be a tricky area and the ATO can get awkward as can some countries tax arrangements on retirement funds.

Bit of a mine field in some ways. If you have a PPOR may be wise to check the arrangements about that to. Federal and State Governments have played funny buggers tax wise with some ex-pats even temporary ones.

100% will do, it sounds complicated enough…

Hit the nail on the head dave, thanks 🙂

Be interesting to see how much all the capital raising that is happening through discounted non-shareholder placements to institutional investors affects the dividend income over time.

Happened in the GFC and now during this Pandemic.

Having cash to take advantage of the capped SPP they offer in conjunction with the placement helps a little.

Love the blog Dave.

Easy to read for newbies like myself.

Thanks mate. Yeah it happens every time it seems, and has to hit earnings/dividends on top of the lockdown. This one is definitely worse than the GFC in terms of the hit to the economy and companies. Hopefully we can recover before it drags on too long and get back to some type of normality!

I love it when you make up “silly” examples. They really drive the point home. Another great post.