Most of you will have noticed the sharemarket has fallen in recent months.

A bit over 10%. Nothing spectacular to be honest. But enough to make new investors nervous.

Will the market keep falling? What should we do?

There’s lots of questions and concerns. And that’s completely normal. It’s not nice to see your investment fall in value. I feel it too.

But if we learn some fundamental truths about investing and the markets, we can then handle any scary times much better. So today I’ll share how I think about market drops and give you a sensible approach to follow.

Firstly, let’s put the recent fall in context. The market, as measured by the S&P/ASX 200, is down from a high of 6,374. As I write this, it sits at 5,680.

That’s a fall of 11%. Not great. But not unexpected.

After all, the sharemarket is a volatile beast. But you already know that, right?

In fact, the lack of volatility in the last few years is more unusual than the volatility we’re experiencing now.

The market can go almost anywhere in the short term, as it’s often driven by fear and greed. Lots of selling pressure (fear) pushes it down. And lots of buying pressure (greed) makes it go up.

By nature, this is a short term factor. But over the long term the market reflects how much value companies have created. More on that later.

Zooming out for a second, this page shows that 5 years ago the market was at 5,265. And 10 years ago, it was 3,722. (Yes I know it was higher before the GFC.)

Now let’s stretch our time-frame a bit.

In this data series, in 1992, the market index was at 1,358.

What stands out to me is how crazy (and way above trend) the boom leading up to the GFC was!

Clearly it’s not always smooth sailing. Far from it! But the point remains the same – over time, the market goes up.

The exact numbers aren’t all that important. The long term trend is what matters.

OK, maybe 26 years isn’t really that long. Let’s go back a bit further…

Basically the same story here. Some very shaky times, but ultimately, a relentless march upwards over 80 years.

The chart is from this page, which contains lots of great info on the history of the Aussie sharemarket. Well worth a read.

By the way, none of this includes dividends. We’re simply trying to put these price movements in perspective. Again, we see the same persistent long term trend.

In short, the market has increased many, many times in value from where it was 30, 50 and 80 years ago.

Our friends in the US always have mounds of data and examples of long term market returns and events throughout history. In Australia, sadly, we often have to get by with very little long term data.

But no more! The prayers of us financial nerds have been answered!

As luck would have it, while writing this blog post, the Reserve Bank of Australia (RBA) published a speech/paper called “The Long View on Australian Equities”, which is very interesting.

Purely coincidental – I’m not that well connected, I can assure you!

Anyway, there’s some great commentary and charts inside. Here are some of the best bits…

This chart shows that from the period since 1900, the total return from Australian equities would have multiplied an investor’s money by 1,000 times, after inflation.

And the following chart shows the total return for 100 years, broken down by indices and measured in nominal dollars…

Here, the total return comes to well north of 50,000x. Now, this isn’t adjusted for inflation, but still!

Also, it’s quite remarkable how close the returns have been for the indices over the very long run. Does this put the industrials vs resources debate to rest? I’ll let you decide.

But as I said in the Whitefield review, I’m no longer sold on the view that industrials will always win. A number of resources companies have proven they’re definitely worth owning as part of a diversified portfolio.

Now, how has Australia fared compared to other countries?

Pretty solid returns all round.

Let’s not forget, during those 100 years, we had the following:

Two World Wars. A number of market crashes. Political turmoil. An oil crisis. Terrorist attacks across the globe. And many terrible recessions, including the Great Depression of the 1930’s.

Despite that, shares have delivered the returns you see above. So it’s not a case of avoiding the market when bad things might happen. It’s about continually investing in the market, despite those bad things happening.

When investing in the sharemarket, this is the truly long term view we need to take. Sure, we might not quite be investing for 100 years, but we can stay invested throughout our lives, keep adding to our portfolio and gift that ownership to our chosen charities or children.

Ultimately, our loved ones and the rest of the world can then benefit from our foresight and strength to stay invested throughout the ups and downs.

All this after we’ve claimed our financial independence of course.

So, where is the market going in the short term? I have no idea.

But where is the market going over the long run? Up!

The market index tracks the performance of all the companies in a particular index – the top 200 on the ASX for example.

Each company in the index is weighted according to its market cap. So the biggest companies by value (like Commonwealth Bank and BHP) have the largest weighting in the index.

Over time, as companies slowly increase their profits, this makes them more valuable. And over time, share prices will eventually reflect that performance – for each individual company and the market index as a whole.

So, in the long run, the market goes up to reflect the higher profits made by these companies.

Because every day, those businesses (and the people who work there) are trying to come up with faster, better, cheaper ways to do things.

They’re each trying to beat their competitors, gain market-share and win over customers.

So they create new products and services, find ways to lower costs and increase productivity, which ultimately increases company profits over time.

Also, population growth means more customers. Simply put, businesses find a way to sell more things to more people over time.

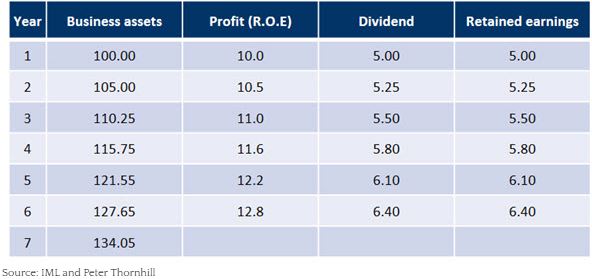

A major way companies increase profit is simply by expanding, using retained earnings. This is best shown by the following table…

Quite simply, if a company makes $10 in profit, it will keep some of it to be reinvested back into the business. This should result in more profit next year, and so on.

Over time the company keeps growing in size, continually reinvesting to increase its future earnings. All while keeping shareholders happy with an increasing stream of dividends.

And it’s roughly like this for all the companies in the market index (or inside our LICs). Although they may be paying out healthy dividends, each business is still reinvesting and working hard to grow future earnings.

That could include anything from spending on research and development, investing in new technology or equipment, expanding a factory or just opening a new shop.

So it makes perfect sense why company earnings grow, dividends increase and the market goes up over the long run.

And because Australia is a prosperous, relatively well managed and stable country, with bright people and solid population growth, I don’t see this changing any time soon!

Look, I won’t sugar-coat it. The sharemarket is probably going to have a few pretty dramatic falls over the course of our lives.

I don’t mean 10% drops. More like 30% drops. Maybe even a few 50% drops. And when it happens, don’t be surprised. It’s not a bug of the markets, it’s a feature.

That’s just what happens. See my other post on this topic: What if Australia Crashes?

So we can either accept it, or we can freak out about it. But we can’t control it. And I think that’s what scares people the most. Not being in control.

What we really need then, is some coping mechanisms. Some rules of thumb to go by. And a plan of attack for when these situations occur, so we don’t get all nutty and panic at the worst possible time.

We already understand why the market goes up over time and why we can expect that to continue. But what do we do when we see that red in our portfolio? Is there a way to get comfortable with a sliding sharemarket?

Yes, I think so. At least, from my admittedly limited experience.

I don’t have war stories from the GFC. Nor do I have memories from the 1987 crash (I wasn’t even born then!). But I do have a decent list of things that should help us stay calm and level headed in scary times.

Stop looking at the market. Seriously! You’re just going to make yourself more anxious.

The more you look at it, the more your mind will start playing tricks on you, and come up with reasons why this time is different and you should sell everything and run!

Go for a walk. Read a book. Play with your kids/pets. Do anything else, other than look at the market!

Regular readers will know that I don’t really focus on share prices too much. Even writing the earlier parts of this article were a bit of a stretch for me.

I just don’t find the price movements all that important, because that’s not a part of our personal goals. We don’t need the market to go up. We want company earnings and dividends to go up.

Remember, the earnings drive the market in the long term. Not the other way round! So focus on the cash generated by companies, not the price they’re selling for.

I know that’s painfully simple. But it’s still important to remember.

A downturn this year isn’t going to matter much in 20 years time. Especially so, since you’re going to be investing regularly and reinvesting your dividends.

Don’t sweat the small stuff. In the markets, that means the short term stuff.

Trust that over the next 50+ years the world and the Australian economy is likely to be much larger, and company profits much higher, as technology and innovation makes us all wealthier over time, as it has for the last 100+ years.

The large basket of companies you own inside your index fund or LIC will change around a bit. But that’s normal. No company lasts forever. As companies become less relevant over time, they eventually get removed from the fund and replaced by newer, more successful companies.

We have no control over the market. But we do have control over how we behave.

So we need to stay calm and divert our energy elsewhere. That energy is far better spent on enjoying our life, increasing our savings rate or simply sticking with our investment plan.

Don’t bother try trying to guess where the market’s going next. You don’t know. But don’t worry, neither do I! And don’t read articles or interviews with market pundits, because they don’t know either!

By the way, that’s actually a blessing. We don’t have to know. We just have to keep saving and investing regularly, be strong enough to stay invested, and focus on our long term income stream.

When the sharemarket is down, is the prime time to be topping up your holdings. And even buying more than you normally would if that’s possible. Maybe by doing some overtime at work, or finding a few more incremental savings.

How do you know shares won’t go lower?

You don’t. We can only know that looking back years later. But either way, you’ve increased your ownership and will now receive higher dividends because of it.

When prices fall like they have recently, the dividend yield is now higher. For dividend investors, that should be enticing enough!

I think this is what the average person on the street struggles with.

They see (or hear about) the market going down. And they know individual companies can go bankrupt. So they put all that together and think “holy crap, you can lose all your money in the sharemarket.”

But the market can’t go broke. It’s just not plausible for the 100-300+ major companies that make up the Aussie market to all go bankrupt at the same time and have a combined value of zero.

That’s the difference between picking a couple of stocks and buying a diversified fund like an index fund or an old listed investment company.

Unless Planet Earth itself is coming to an end, the sharemarket isn’t going anywhere. It will continue to reflect the prosperity and efforts of the human race, and that’s the fundamental reason I believe it will continue to rise.

I’m an optimist by nature. And history suggests it pays to be that way.

If we’re expecting a dim future, why bother investing? Just buy baked beans and bottled water, and head to your underground bunker instead.

We all suffer the same emotions. It just takes a little effort and discipline to stick with our plan.

A great quote from experienced investor Peter Thornhill regarding the GFC: “you’d have to be dead not to feel it!”

Yet paradoxically, Peter has also said he looks forward to a GFC. If you haven’t already, check out my full interview with Peter here.

So the point is, we’ll all get worried when the next crash comes around. But if we have a solid strategy in place and remember some fundamental truths about the market, we can feel the fear and invest anyway.

It’ll probably feel like the world has changed and we should be ducking for cover. But remember, the scariest times to invest usually turn out to be the most profitable.

Look at the long term price charts above, and tell me when you wish you had invested? At the lowest points right? Or simply whenever the chart begins, and then held up until the present day!

Try to look at the sharemarket with fresh eyes. Pretend you’re a new investor again.

Re-learn how long term investing in shares works, and more importantly, why it works.

Remember why you’re investing in the first place. Accept that falls and crashes are part of the deal. Not to be feared but to be expected. And those scary times are partly the reason why shares offer higher returns than other assets over the long run – to compensate for the risk.

Talk to investors who have been in the game longer than you. That can help put things into perspective and remind you that the market will fall from time to time.

The important thing is to keep your head in the game and stick to your plan. You can even automate your investing to make it easier.

Finally, come back to blog posts like this one, or whatever helps you remember what long term investing is all about.

Anyone who is going to be buying a lot of shares over time, should be hoping for lower prices. Why?

Because then we’ll be able to do most of our buying at cheaper prices. And building our portfolio at lower prices and higher dividend yields, means a greater return when the market eventually increases.

Not convinced yet? Well, here’s Warren Buffett on the subject:

“If you plan to eat hamburgers throughout your life, should you wish for higher or lower prices for beef? Likewise, if you expect to be a net saver during the next five years, should you hope for a higher or lower stock market during that period?

Many investors get this one wrong. Even though they are going to be net buyers of stocks for many years to come, they are elated when stock prices rise and depressed when they fall. In effect, they rejoice because the prices have risen for the ‘hamburgers’ they will soon be buying.

This reaction makes no sense. Only those who will be sellers of equities in the near future should be happy at seeing stocks rise. Prospective purchasers should much prefer sinking prices.”

Buffett has also said:

“I like buying more as it goes down, and the more it goes down, the more I like to buy.”

Finally, here’s a short video with Uncle Warren explaining how he thinks about short-term market movements and long term investing.

For dividend investors, it gets even better.

Lower share prices mean higher dividend yields. This means our portfolio generates more income, sooner. It actually speeds up our progress!

And that’s true even if we experience a recession and dividends go down for a while. Because dividends fall less than share prices, the yield on offer will be very high indeed.

So if we can do more of our buying when there’s a bad patch, we’ll end up better off when the market and dividends inevitably increase again.

Market falls can prove to be heaven on earth for dividend investors!

Focusing on income instead of prices, makes riding the waves of the sharemarket a lot smoother. Especially when you consider that we’re not reliant on market prices to reach our goals.

Compare this to a capital growth focused investor, who is waiting for their portfolio to hit $X in value so they can retire and slowly begin selling down.

They could’ve been coming up on retirement this year as their portfolio grew nicely over recent years. Now they’ve been set back until further notice, simply because the market has fallen.

Your early retirement date is then dictated by market movements. Maybe that sounds OK to you, but personally, I’d find that incredibly frustrating and that strategy is not for me.

Anyway, for us dividend investors, we simply keep purchasing shares and watch our income relentlessly increase. Not because dividends never go down. But because our long term result is overwhelmingly driven by saving, regular investing, and reinvesting our dividends, as I highlighted in this post.

This means you don’t even need to look at the market.

I know that’s easier said than done. We all want something to look at! So what do we do?

Well, here’s what I focus on instead…

One big thing that helps, is by tracking the annual dividends generated by your portfolio.

You can do this on paper, on your phone, or in a spreadsheet. Whatever is easiest for you. I don’t have any formulas or anything, just the annual income from each holding.

Simply write down all of your holdings and figure out how much dividends you’re earning per year from each.

If you’re not sure how, here’s what to do…

Go to your brokerage account and see how many ‘shares’ or ‘units’ you own of each company. Then your broker should also have data for that company for how much ‘dividends per-share’ that company pays. Have a dig around and you should be able to find it. If not, type the code in here and find the dividends paid in the last 12 months.

For example, let’s say you own 1000 AFIC shares. AFIC’s annual dividend is currently 24 cents per-share. So 0.24 times 1000, means your annual income will be $240.

And of course, to add franking credits in, you take that number and divide by 0.7 (for a fully franked dividend). This gives you a figure of $343. Now you just add that to your table or list. Then on to the next one.

At the end, just tally up the total income from all your holdings. And adjust it every time you buy more shares, or your holding has a change in the dividend paid.

Update: Instead of doing this, you can get the simple spreadsheet I use to keep a tally of our Annual Dividend Income…

Now you really have something to look at! Of course, you can watch the market all day, but your annual income doesn’t move just because the market does.

Personally, I look at this when I need to remember what it’s all about, and it’s such a great help. So this can really allow you to ignore the mood of the sharemarket and let you focus solely on your income goals.

Remember, for dividend investors, the price movements just don’t matter. Simply keep your eyes fixed on your growing income stream.

Of course, it can be argued that prices move lower to reflect the less bright outlook, concerns over interest rates, trade wars, Trump’s tweets, whatever.

Maybe. But I don’t buy that entirely. I think it’s more a change in sentiment based on the short term, when the long term outlook (50+ years) hasn’t really changed.

With the amount of trading in the market skyrocketing and the average holding period shrinking, I think it’s fair to argue that the market in the near term is driven mostly by short term thinking.

Personally, I don’t believe the market moves based on the next 50 years of earnings. Simply what people think will happen in the next year or two.

For example, expectation is growing that the US falls into a recession in the next few years, which obviously will lead to lower stock prices and lower earnings. So some investors are getting out now just in case.

But that’s not our game. Dancing in and out, trying to read the tea leaves and outsmart the market is an utter waste of time, effort and money. Because you’re going to lose in the end.

We’re playing the long game here. So unless you expect the future to be a nasty, scary place, then the only rational thing to do is buy more shares.

Basically, I don’t believe that where we’ll be in 2068 has changed too much from a couple months ago!

The power of technology and innovation will continue to drive productivity gains, increase company profits and increase our standard of living over the long term. Just as it has for the last 100+ years. And that’s what will drive the market over the long term.

Hopefully you find this post helpful in navigating the choppy sharemarket seas!

Have a look at those long run charts from the RBA again. How can you lose money in the market during a time like that?

Irrational behaviour, lack of diversification, or trying to time the market. Luckily these things are easily fixed…

By keeping calm, understanding how the market works and focusing on the long term. By investing in diversified funds like low-cost LICs or index funds, including international shares if you like. And finally, by sticking to your investment plan and buying shares on a regular basis.

I’m building my portfolio each month, regardless of what the market does. Why should I let the market convince me otherwise?

If anything, I’m becoming more interested buying shares now than I was a few months ago, when prices were higher and yields lower. Remember, if we wait, then we stagnate, and end up making no progress.

After all, our sole aim is to constantly increase our ownership stake in a large group of businesses, which will, on average, increase their earnings and pay us higher dividends over time.

So focus on the income. Focus on your goals. And focus on the next 50 years, while the rest in the market worry about the next 50 minutes.

As Jack Bogle wisely put it, “the stock market is a giant distraction from the business of investing.”

A reader shares their inspiring story of humble beginnings to building $500k of wealth in 5 years. He shares family lessons, how he and his wife increased their income, and their FIRE goals over the next 5-10 years.

Learn how our EV performed on our recent roadtrip and holiday in Southwest WA. What I learned from the experience, plus lots of pictures, recommended places to eat, and more 😉

Get my latest content and thoughts straight to your inbox.

A fresh dose of financial motivation to power your journey.

One of my favourite posts to date, top 5 for sure!

Brilliant refresh on what we all set out to do in the first place. I’ve not been on this journey as long as you but I’m quite happy that I get an initial excitement when I see red as I smell a bargain. As I’ve noted a few times I have AFI & WHF and buy every two months. Each time my goal is to try and reduce my cost base if at all possible and if not go for the closest. When I see my capital gain in red on Sharesight I can’t wait to jump on and buy more all with a nice little wink to my dividends column ????

I will be creating my income calculator on Monday and looking forward to updating that every purchase that’s an amazing idea and perspective, thanks for that! Then the next thing I will do it print the Buffet quote and put it on my wall in my office!

Legend, keep up the increasing quality content.

Awesome work Paul, and thanks, glad you like it!

The income tally is made just for the sake of being organised/planning but it doubles up nicely as a tool to help us focus 🙂

Great article & great timing Dave.

As an early 60’s almost retired person I’d say I am ‘fully invested’ with some cash reserves & was aware a correction would come sometime so sooner than later is okay to test the buy & hold LIC income way as am very sold on this from PT & another forum you use. Purchased some in initial ‘big drop’ but will hold off ’til more div’s roll in next year unless the temptation is too much on a particular day, so this article is another great mentoring read on this investing path.

While I do keep track of income having an actual, specific scorecard was something I didn’t have, I made a temporary one up immediately just for fun but will perfect it over time. Dave you sure you’re not a 50 y/o old accountant an earlier poster took you for? It’s okay, you can ‘fess up to me, I promise I won’t tell too many people.

Keep the good work up!

Thanks monk. Haha no I promise I’m not a middle aged accountant! Just a little older in the head I guess… or are you trying to say I’m a bit boring? It’s okay, I can take it 😉

Good job setting up the ‘annual income scorecard’ too. Speaking of which, not long till dividend season again!

No you’re not boring Dave it’s that your understanding of the financials of what you write about are solid & am always amazed at the depth of some of your writings on LIC’s etc. Remember you saying nothing interested you at school yet here you are doing in depth stuff that most educators wouldn’t have a clue about.

Yep can smell the dividends coming !!

Haha that’s nice of you to say mate, thanks!

Yeah school wasn’t all that engaging – I think peak performance was around grade 2 or 3 when we used to do maths races lol, very fun 🙂

I agree, and that’s a very interesting RBA speech.

One conceptual difficulty I have with historically heavy analyses of what as happened is that while it provides good perspective on the generally superior performance of equities it tends to miss a couple of issues:

– there is no particular reason to be confident Australia will continue to enjoy what have been quite high equity returns, we may for example revert from ‘lucky’ to average

– similar to above, there is a survivorship bias at just looking at UK, USA and Australian returns as the RBA does: Japanese, Argentinian, and other markets looked great on historical numbers, until they didn’t

– there have been prolonged period where bonds outperformed equities.

None of this is to argue with the good core points, there is just sometimes a danger of missing what you might call ‘regime shifts’ by looking backwards. Perhaps this is one reason ‘permanent portfolio’ ideas are so persistent.

Appreciate you raising these points, as always, being far more well read than me!

At the end of the day, there’s no guarantees of anything really, and it’s up to each investor to decide for themselves what makes sense. Thanks for the comment mate 🙂

I think there’s a reasonable basis in financial history to remain confident in Australia. I read a book called This time is different by Reinhart and Rogoff. It reviewed about 800 years of financial history of different countries, asset bubbles, busts etc. While I was reading it I realised that the main difference between rich countries and poor countries is that rich countries have never defaulted on their bonds. Literally, there’s only a handful of countries in the world that haven’t had a default, Australia being one of them. If you think it’s unlikely that Australia will default on its sovereign debt over time (and I do) then it’s reasonable to think that we’ll remain prosperous. Good book by the way, but a little heavy on numbers, Manias Crashes and Panics by Kindleberger is similar but a more exciting read.

Dave this is some of your best work here. Thank you for the reminder that the ‘capital gain’ AKA ‘the current capital loss’ that is staring back at me in my portfolio at the moment is only a small part of the story! This post is a great reminder to focus on the end game and not the score at quarter time. As you say, it is about growing that constant stream of dividend income and increasing your holding in LIC’s! I’m now all about increasing my holdings in Argo and AFIC for the long term. Took the plunge and bought myself some more AFIC last week to add to my holdings/growing income stream. I have also created a spreadsheet that has the total projected income for each holding. When I look at it, I can actually see that over the last 2 years my income is 4 times what it was in the first year! When I focus on that, I can actually see that the income is growing and that is what matters the most! Legend. Great post and one I will be referring back to regularly.

Cheers for the kind words Chris!

Great way to look at it, really helpful to see that progress I think. Keep your eye on the prize mate 🙂

A gold standard post Dave.

I say to colleagues and friends who have recently been a bit smug with their comments to me re- the correction in the market, I say thus: “Someone else sold their shares for that price, but it sure wasn’t me” …..or…. “it all depends what they bought them for initially, they may have made a wonderful profit!”. I know it’s a bit of a smart-arse answer, but it helps to shift the persistence paradigm (urban myth?) of shares being super risky.

More WHF and AFI into the coffers at our place this month again – every time that $5000 gets saved – boom.

When’s your book due to hit the shelves?!

Thanks Phil! Haha that’s a fair answer I think, at least it offers a different perspective other than disaster for everyone.

Like clockwork hey? Very nice work indeed.

LOL the book? You know that’s probably a lot of work…maybe one day 😉 On a serious note though, if people were genuinely interested I would probably consider it, once the blog becomes pretty lengthy and hard to navigate and people just want the better bits distilled into something simpler.

Hi Dave

I’ve been following your blog for a couple of months now. When I first started investing I was playing around with mining stocks and options. That didn’t work out well for me, they were pretty much expensive lottery tickets and I ended up losing some money, which discouraged me from investing further.

However, I have recently changed my investment approach to focus more on long term growth and dividends. I decided to focus more on Aussie Shares due to their juicy dividends, as investing for just capital growth never made sense to me.

I currently have about 70k invested in a mixture of VAS, VHY and AFI and RateSetter, with majority of it being in VAS. I am planning to dollar cost average another 100k of savings into these next year, and then add 20k per year after that, which would equate to about 30% of my income. I will probably limit RateSetter to about 5-10%, as they haven’t been around for very long and I am more confident investing in equities.

I added AFI to my portfolio after reading your review of it and will probably direct more future cash into AFI, making it one of my top holdings. I particularly like the DSSP feature of it and it suits my situation well. I wish more LICs had DSSP. I might possibly add WHF later on, although I am still undecided about them.

You might have answered this question before somewhere, but I wanted to ask you, what is your opinion on VHY? It currently has a dividend yield of like 9%. If dividend income and early retirement are the goals, would it make more sense to divert more cash into VHY instead to retire sooner? Although their fee is on the higher end 0.25%, I still consider it to be fairly relatively low cost. And their holdings are solid blue chip companies that should continue to provide good dividends and some capital growths.

I am currently 38 years old, and hoping to partially retire by the time I hit 50.

Regards

Hi Gene, thanks a lot for sharing your story!

I think your investment plan sounds good, dollar cost averaging and continually adding savings – that’s where the magic happens.

Not really keen on VHY for a couple reasons. It’s far more concentrated than most old LICs or the index. Much less holdings and more sector concentration. Portfolio is changed around based on future yield, which means it’s less tax efficient and sometimes results in large capital gain payouts. I used to hold this years ago and experienced this.

Also stocks are hold solely for yield with no regard to growth. For example when I held it the fund owned BHP years ago because it was on a massive forecast yield, but that was because the dividend was becoming quite obviously unsustainable – the dividend was then cut and BHP was removed from the fund. Contrast this to the index and LICs which hold a larger number of stocks, some high yield low growth and some low yield high growth. This gives the portfolio better balance.

And with VHY if you look at the distributions, they fluctuate more than VAS and the LICs, so that’s not idea for retirement income either. Personally I just feel more comfortable with the larger more diversified portfolios of the index/old LICs, the lower turnover and the more reliable, and growing, income stream. Hope that helps, and thanks heaps for following the blog 🙂

Thanks Dave for a detailed explanation, I understand it now. I’ll probably keep whatever I already have in VHY without adding anymore to it, and divert future cash into AFI and VAS. Might also add some IVV or VTS in the future, just to diversify a bit internationally.

Thanks again, love your blog and will look forward to future posts.

Great post!

1. Only invest what you can afford to lose

2. Invest for the income

3. Invest with a mindset that you will never sell (super long term)

4. Diversify (asset class, industry, shares, country)

One question – do the returns on the aussie shares include franking credits (e.g. total return since 1900 AU/UK/US)?

Thanks very much Greg!

No, none of the returns data includes franking credits.

Wait, the share market is down at the moment? Haven’t noticed. I’ll check it out when I retire in about 15 years. 😉

Haha! Nothing worth paying attention too, just felt compelled to write about the topic. I like your approach!

Thanks for this Dave.

Cheers Mark!

Great post – just had a friend make a comment to me on how I was going last night at a friend’s birthday party given the recent drop in market. Think I’ll share this with them 😀

Thanks for that, glad you liked it. And hopefully it also puts things in perspective for your friend 🙂

Great post Dave, one of the best.

I’ve been mentioning that Buffet quote to a lot of people this last month, love it.

Cheers Andrew, that’s great to hear!

Very good blog post, thanks mate!

….forgot to mention – I’m loving the new SMA logo.

Is that a recent addition to the blog or have I just been super unobservant as per usual?

Oh cool, thanks Phil! No it’s definitely new, and it only took 20 months to get around to doing it 😉

Great Article mate and well timed, it really helps to hear this in times like this to help stay focused. Cheers!

Thanks for reading Peter.

Love this read. Only came across your site a few weeks ago and it has triggered me to get serious about my portfolio. Being 47yo I decided it’s time to stop messing around with spec stocks as I have been doing the last couple of years.

I already had a basket of blue chip shares which I was fortunate to receive as part of an inheritance a few years ago. I am reluctant to sell them due to CGT penalties so will keep them. They all pay nice dividends so all good there.

In the future though I have set my portfolio up to be a mix of MLT, MIR and FGG which I will be adding to on a 6 monthly basis of around $10k with all dividends reinvested.

Like you mention I have no issues at all with the current correction as it means getting more stock at a cheaper price hence a greater dividend yield. Winner winner!

I will also be setting up a simple spreadsheet to keep track of my dividend earnings. Thanks for this great idea.

So glad I came across your site. It has really focused my attention to where it needed to be. Keep up the great work.

Thanks for such a great comment Grant! Glad to hear it’s helped you focus on the main game (income) vs speculating. Creating your ‘annual dividend income’ scorecard is very motivating, can’t recommend it enough. Your future results will surely be a lot better now 🙂

Thanks Dave. I enjoyed the read. Thanks also for pointing out the RBA speech which showed the long term Australian equity data.

It has been a bit of a hobby of mine to try and find the most accurate long term Australian equity data for a while now. I have managed to put together a model primarily based on the following paper: “The historical equity risk premium in Australia: post‐GFC and 128 years of data” by Tim Brailsford et al. Interestingly I used the model i created and was able to replicate the RBA’s data quite nicely. In fact, the last data point in the model is $161,094.85, so to reiterate the RBA’s speech, If you had put $100 into the equity market in 1900 in a portfolio that tracked the stock market index (and VERY importantly reinvested the returns) you would have $161,094.85 today (end of 2017) after adjusting for inflation.

The data from Brailsford et al. actually goes back as far as 1882! So for a quick experiment, I extend the calculation back to 1882. I was able to show that if you invested $100 into the equity market in 1882 in a portfolio that tracked the stock market index you would have a tidy $927,648.17 today (end of 2017) after adjusting for inflation (shows the power of compounding).

In terms of the question of why does the market increase? I think the most interesting number that comes out of my model is the compound annual growth rate (CAGR). According to my model, the Australian stock market has grown on average since 1882 (to end 2017) by ~5.3% (not adjusted for inflation). What does this 5.3% nominal growth rate represent? Well, it could simply be reflecting the overall economy, which tends to grow at ~5%-6% pa (nominally). An interesting idea that I read in the in the following article:

https://www.scribd.com/document/101496700/“A-Roadmap-for-the-Australian-Stockmarket”

Thanks very much Jason, great comment, and thanks for sharing your own findings!

I do remember reading something about the older data which starts in 1875 being less reliable as mentioned in this article – https://cuffelinks.com.au/look-towards-your-investment-horizon/

It’s probably fair to say it might not be perfect but whatever data set will likely show that the market, company earnings, and the economy, have similar long term growth rates since they’re so closely related to one another. I probably didn’t emphasise the ‘economy’ part enough 🙂

Appreciate you stopping by Jason!

Yes absolutely the further back in time you go the more problematic the data becomes but it then begs the question of when do you set the starting point? Statistically speaking the results of any model a completely dependent on where you set the start and end points so how valid is any of it?!

One interesting way to look at it is to break it down into smaller chunks of time (e.g. 20 years chunks). They do this in the following paper:

http://drewwalk.co/publications/the-equity-risk-premium-in-australia-1900-2014/

(worth a read)

cheers J

That’s a good point. The shorter time-frames would be worse I would’ve thought, as it gives less time for the start/end dates to be smoothed out by the weight of long term returns.

Either way, I try not to get too hung up in the details of the data to be honest, and am guilty of just looking for simplistic takeaways. Maybe I’m just not academically inclined, but I always like to focus on the real world application and what it (likely) means going forward, because that’s what I find most useful. Will take a look at that paper though, thanks again Jason!

I actually completely agree. I started out thinking once I got the model as accurate as I could then all my investing decisions would be made simple. Boy was I wrong! I think there are certainly times to be guided by data but of course you can also get completely bogged down in it. It was actually when I came across Peter Thornhill’s Motivated Money ( a few years ago now) that all the ‘research’ I had done actually came together in my mind and I started taking action (i.e. have been accumulating LICs for the past few years) and feel very comfortable/confident doing it 🙂

The model is ultimately a guide to help me understand that the market is cyclical (and fractal) and to help me stay confident with my strategy (accumulating LICs) when the market is down! I also know people who use a similar model to guide them in writing put options (ASX index) during bear markets (to supplement their investment income).

Cheers J

Thanks for sharing your very own experience with analysis paralysis! And great you settled on a strategy and started taking action.

Well said – I think of it in the same way, as a guide to set expectations of what can happen in the market, and to put things (usually current events) into perspective.

Hi Dave, can you make a future post that discusses your direct share investing experiences?

I would love to understand what experiences caused you to conclude you couldn’t learn to profit from direct shares and switch exclusively to using only LICs and ETFs.

______________________________

Q1. How did you learn to invest directly in shares?

A1. I started my journey by reading investment books and attending free ASX Wednesday lunchtime lectures at the Australian stock exchange building in Collins Street.

I started investing using the A$10,400 bursary I saved as a Cadet engineer completing my final year of my Electrical Engineering degree.

______________________________________

Q2. Were you a trader or an investor?

I concluded my best chance for success was to “buy and hold” large cap Australian industrial stocks as an investor/business owner.

As a full time Cadet engineer, I didn’t have the time nor interest to track and actively trade stocks.

I didn’t want to deal with the volatility of stock prices of cyclical, resource and small capitalisation stocks.

I was also aware that I didn’t have the time nor expertise to purchase overseas investments.

So on the advice of a financial planner, I invested that bursary into two high fee, unlisted international managed funds run by Bankers Trust and Rothschild Australia and directly in the float of the Commonwealth Bank.

The Asian financial crisis crushed my managed funds, so I sold them at a small loss a few years later when they recovered some of their value.

I also sold my CBA float shares at a tidy profit after the GFC hit and I sold all my bank share exposure.

The lessons I drew from these experiences were fund managers stay invested irrespective of value. Only I care enough about my savings to act decisively to cull the under performing investments to preserve my savings value.

______________________

Q3. How many years did you spend before giving up on direct share investing?

After a decade of success as a buy and hold investor of large cap Australian investors industrial stocks, I become overconfident and broke my rules for avoiding all resource, small capitalisation, speculative growth & tech stocks.

My string of gains began to turn into increasing losses peaking with the TechWreck of early 2000.

Suitably chastised for my hubris by the markets, I sold off all my speculative losers to shrink my portfolio down to a small core of large cap Australian industrial shares paying fully franked dividends

I turned my back on direct share investments to focus exclusively on my career as an engineer.

It wasn’t until 2003 that I began to take an active interest in the Australian sharemarket again.

Ongoing high PAYG taxes and a recovering share market enticed me to revisit direct shares investing with a small margin loan.

At the same time, work began a major program to save money by cutting staff numbers which resulted in me accepting a redundancy package in April 2006.

I was now free to pursue full time my 17 year long passion for direct share investing.

I rolled my A$329K lump sum payout from my corporate super fund into my own Self Managed Super Fund (SMSF).

In 2020, my SMSF investments have grown at a rate of 8.1% pa CAGR over 13 years which compares favourably to the top industry super funds.

The SMSF is now worth approximately A$3.3M inclusive of additional annual super contributions since retiring from paid employment over the past 13 years.

My overall direct net equity growth Including my SMSF has been 26.5% pa CAGR over 29 years.

I post my Australian share investments on Instagram at @keith_invests for more information on my direct Australian share investments.

Like most things in life, your rewards are proportional to your effort.

My lifetime pursuit of value investing has been returned many times over in the financial freedom I have enjoyed since my redundancy more than a decade ago.

___________________

We in the FIRE community are often frustrated at how our friends and families misunderstand and/or are disinterested in the actions needed to embark on the path to Financial Freedom through frugal living and compounding investment returns.

My personal frustration is how the FIRE community focuses so much time on methods to be frugal and less on achieving higher compounding rates of returns.

Higher compounding rates of return means that there is less need for severe frugality to achieve FIRE making the message more palatable to the average worker.

Seems a little strange that you interviewed yourself on my blog, but hey that’s okay.

Most people in the FI community realise that your time is far better spent managing money better (by increasing your savings rate), than by trying to beat the market). This has been outlined elsewhere before, but here is my post about it: Saving vs Investing – Where Should You Focus?

I’m not going to debate with you about this as it’s largely a waste of time. Those who enjoy direct shares and find it works for them are free to follow that path, but it’s not for me and typically for most FI followers for the reasons I’ve already mentioned to you (time, enjoyment, lack of results, whatever).

My self interview was to illustrate the types of responses I was hoping to elicit from you on what experiences in direct shares formed your view. I think you have clarified it for me in that “lack of success leads to lack of enjoyment”. My lack of success investing in property is in stark contrast to your accumulation of multiple properties to achieve FIRE through income and capital growth. Basically Horses for courses. Thanks for the response.

That’s fair enough Keith. Funnily enough, I haven’t been ‘sucessful’ in property either. Half of our properties have had minimal capital growth despite holding them for nearly a decade with running costs every year. And the other half did okay, though after all costs not amazing, with only one providing some positive income. The real magic was saving lots of cash year after year to invest with – without that, we’d be nowhere.