A quick heads up before we begin…

As you guys know, I have a long-time relationship with Pearler. I own a tiny stake in the company as well our content partnership with the Aussie FIRE podcast.

But let me be crystal clear – this article is not a sponsored post and I do not get paid if anyone joins Pearler Super. I’m actually taking a risk publishing this as it could be perceived by ASIC as trying to influence people etc.

But that’s fine – as always, the purpose of this entire blog is to share exactly what I’m doing with my own money and why, explaining the strategy and thinking behind it. So I hope you find it interesting – feel free to send letters/snacks to my future prison cell 😉

Maximising your super is something all Aussies should be thinking about.

I’ve never been a huge contributor myself, but I still want the money that’s in there to be working as hard as possible. Because over decades, even a modest balance can grow into something meaningful.

And with that kind of timeframe, tiny differences in fees and returns can snowball into massive differences in outcomes – almost to the point where it doesn’t even seem to make sense!

So in this article, I’ll quickly explain why that matters… and why I’ve decided to move my super across to Pearler.

Hint: it’s for two main reasons which I think will leave me much wealthier over the next 30 years.

Take a 25 year old with a super balance of $50,000, who contributes $10,000 per year.

For simplicity, let’s assume their $10,000 contribution stays constant for the next 40 years. Here’s the result:

– With returns of 7.5% per annum, the balance grows to $3,174,000

– With returns of 8.5% per annum, the balance grows to $4,263,000

Over a million additional dollars – or a 34% boost in the value of their fund, just for a difference of 1% per year.

Now, you’ve probably heard examples like this before. And it sounds good in theory, but how can we actually make this happen in practice?

A few ways:

– Lower fees

– Lower taxes

– Higher returns

The first, is through finding super funds with lower than average fees. These tend to be industry funds – specifically the ‘indexed shares’ options they provide, which are basically the same as index funds that we invest in outside super via ETFs.

You can typically reduce your fees by around 0.5% per annum doing this. From 0.8% for a default balanced fund to 0.3% or less. So far, so good.

While these are great options, they’re still not quite the same as investing in index funds outside super. Why? Because big super funds are managed as ‘pooled funds’.

Pooled funds are basically where everyone’s money is lumped together in a single managed fund. When people withdraw money (or switch investment options), the fund is forced to sell assets and pay capital gains tax, which affects everyone in the fund.

To account for this, super funds essentially harvest taxes from the funds on a regular basis, to set aside for future tax liabilities (at a rate of 10% for long term gains and 15% for short term).

The value of your super at all times is after this tax has been taken out.

Note: this is why you’re able to switch options and change your allocation without incurring any tax.

Regardless of your own behaviour – if you buy and never sell – this tax is still taken out. For more info, read this detailed article. It applies to accumulation accounts only – when you switch to a retirement pension account, your super returns are not taxed.

Let’s look at how much it costs and some potential solutions.

The first way we can check the impact is by looking at the funds themselves and comparing the ‘Accumulation’ accounts and ‘Income’ AKA pension accounts.

Here are the returns for various options using Australian Retirement Trust (ART) as of August 31, 2025.

High Growth: 9.84% pa over 10 years (Accumulation)

High Growth: 10.79% pa 10 years (Income)

Australian Shares Index: 10.04% pa over 10 years (Accumulation)

Australian Shares Index: 11.16% pa over 10 years (Income)

International Shares Index (unhedged): 11.49% over 10 years (Accumulation)

International Shares Index (unhedged): 12.42% over 10 years (Income)

OK, so it looks to me as though it’s a very consistent 1% per annum lost to tax. Now, some of that will be tax on dividends, but given the overall performance, a lot of that is likely to be tax provisioning for capital gains.

Another way we can estimate the impact is through simple logic.

If we expect high growth assets and shares to have a long term capital growth rate of 5%-6% per annum, then having 10-15% of this harvested away amounts to 0.5%-0.9% per annum.

The middle point is 0.7% per annum – let’s use that as our base assumption for this tax.

By switching to an option where your super is taxed individually instead of as a pool with everyone else, this would mean you only pay capital gains tax when you actually sell.

And if you simply buy and hold until retirement age, then there won’t be any capital gains tax to pay. This means you can potentially benefit from an extra return boost of 0.7% per annum (say).

A couple of solutions are:

1– Start a self-managed super fund (SMSF). This gives you the most absolute control, but also the most complexity, admin and running costs. These typically only start to make sense when you have a fairly significant amount (several hundred thousand). There are some low cost SMSF providers available now online such as iCareSMSF and Stake Super. But you’re still looking at well over $1,000 each year.

2– Use a ‘member direct’ option inside one of the big super funds. Australian Super and HostPlus both offer these at reasonably good value. This lets you pick your own stocks and ETFs (within limits), and CGT is payable only when you sell. These come with brokerage fees and extra account fees (more on this in a minute).

Each of these adds extra downsides like more admin, more fees, and with the case of the second one, being locked in to a provider (switching means selling = CGT).

For the most part, average fees will be in the region of 0.4%-0.6% for balances under $200,000, assuming a low cost ETF portfolio. A good breakdown in this post.

So, the math points to paying an extra 0.2%-0.3% in fees (over a low cost indexed pooled option), for a potential benefit of 0.7% in tax savings, leaving you better off by 0.4%-0.5% per year. Not huge, and maybe not worth it for most people.

For these reasons, and not having an ultra large balance to justify an SMSF (and not really wanting the hassle of it), I’ve been reluctant to make any changes. I deemed my indexed shares option with ART good enough – no effort, zero admin, just pure set and forget.

Then Pearler came out with its super offering.

If you’re a Pearler customer already, you’ve likely heard of Pearler’s new super option.

It’s basically like one of the ‘member direct’ options I mentioned, where you are taxed individually, not as a big pool with everyone else. Here’s a simple rundown…

It’s hard to compare with other similar options because they have different fee structures which stay flat as your balance scales up.

Here’s the best comparison I’ve found which looks at how they compare based on balance size including a low cost SMSF from Stake. Full credit to Reddit user ‘SwaankyKoala’ for excellent table (click to enlarge):

Switching to one of these options would likely net me an extra 0.4%-0.5% per year in tax savings as mentioned earlier.

As you can see, Pearler’s offering is cheaper for balances under $100,000. Above that point, the other options start to edge out. My own balance is around the six-figure mark. So while Pearler is a good option, it’s not exactly a clear winner in my case based on these figures.

However, there is one other difference that I find even more compelling and impactful. The specific ETFs you can choose. In particular, the introduction of geared ETFs.

I’ve spoken about geared ETFs in the past, like as part of this article, and in episode 38 of the Aussie FIRE podcast. I also wrote an article discussing the earlier style (higher leverage) ETFs here.

Go check out that content if you want to dig a little deeper.

The short story is there’s a new breed of geared ETFs which are more suitable for long term investing than the previous options, largely because they have lower levels of leverage.

In particular, Pearler super has the following investment options that piqued my interest:

As far as I know, these aren’t available with the direct investment options with other super funds. So until now, it wasn’t possible to build a geared super fund using ETFs without using an SMSF.

Why does this matter? Well, if you’re an experienced investor, I think super is the perfect place to use geared ETFs, for several reasons.

1- You can’t access the money, so there’s no temptation to pull it out or tinker

2- You’re already locked into a multi-decade timeframe by default

3- You look at it far less than your regular portfolio (probably)

4- There’s money automatically flowing in regularly to take advantage of volatility

5- And for me, super is basically ‘bonus money’ anyway, so I’m happy to take higher risk with this pot of cash

One hurdle is working around the percentage caps on how much I’m allowed to invest in each fund.

There’s also a 2% starting cash balance is required at this stage for admin charges etc. I’m told they’re aiming to lower this at some point, which would be good, but as your balance grows it naturally falls below 2% anyway (mine is already down to 1.75%).

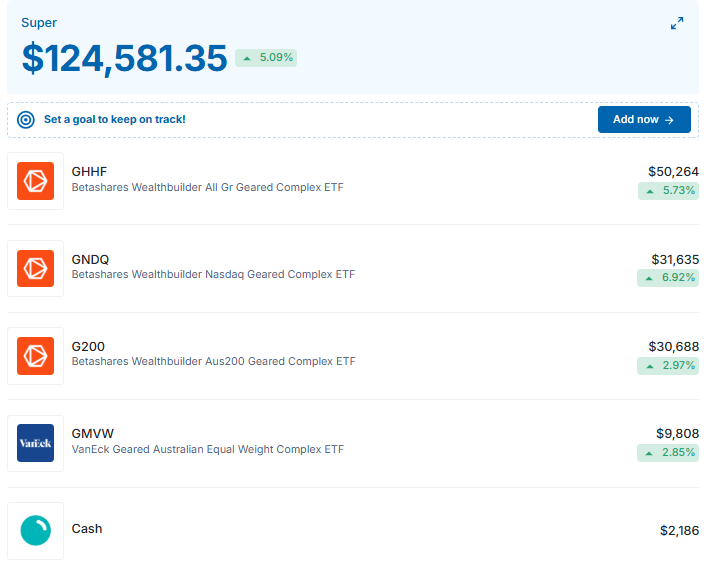

My preference would be to have my super invested in 100% GHHF (or 98% I guess), for simplicity and leave it for the next few decades. But the limit on that fund is 40% of the balance. So to work within the limits, I came up with the following allocation:

I don’t normally do this, but here’s how my super looks as I write this:

This allocation rounds out nicely to give me two things:

1- Maximum gearing – my whole balance is geared

2- An even split between global shares and Aussie shares

Why have I done this? What’s the potential benefit? We’ll get to that in a minute. First, let’s check how much this is costing – because it ain’t cheap.

These ETFs have fairly affordable management fees, without being ‘cheap’. The fees are currently 0.35% pa (for GHHF, G200 and GMVW) and 0.50% for GNDQ.

But it’s actually more, because fees are paid on the total amount of money being managed, not just the ‘net’ amount. Meaning, you invest $1, you get $1.50 of shares and the management fee is based on the $1.50. Which I do think is fair, given that’s the assets being managed.

So, the overall fees climb by the level of exposure you have. 1.5x gearing = 1.5x fees. This means 0.35% becomes 0.525%. And fees for GMVW which has 2x gearing becomes 0.70%.

Here’s the total management fee estimate for each:

Based on my specific allocation, this gives me a total portfolio cost of roughly 0.58% per annum. And if you add the Pearler admin fees of roughly 0.4%, I’m basically paying a big fat 1% per annum in fees!

Now, that 1% will obviously reduce as my balance grows, which is comforting. And I fully expect Pearler to roll out a ‘fee cap’ which would improve that again – I’m told it’s something they’re very conscious of.

But at this point, you probably think I’ve lost my mind. Is it even worth it?

I’ll be as reasonable as I can here, and tell you the exact estimates I’m making to frame this decision.

If we assume a long term market return of 8% per annum, what could a geared ETF portfolio achieve?

Well, with the funds I chose, for every $100 invested I get exposure of roughly $150.

This $100 earns a return of $8. The other $50 earns a return of $4, but has to pay interest of say $2.50 (a rate of 5%), leaving $1.50 surplus. So the hypothetical net return is therefore 9.5%, a return boost of 1.5% per annum.

I haven’t accounted for fees here though, so let’s put it all together…

I’m now paying 1% per annum in total costs, instead of about 0.3% (all inclusive of Pearler admin fees, brokerage, and higher management fees on ETFs).

In exchange, I get tax savings worth 0.7% per annum and a return-boost from gearing of 1.5%, for a total benefit of 2.2% per annum.

When you net these out, the expected net benefit is roughly 1.5% per annum. Therefore, I expect my super to grow 1.5% per annum faster with this strategy over the long run.

That might not sound like much, but here’s what that looks like over 30 years assuming a six-figure balance…

$100,000 invested at 7% return with no money added = $761,000

$100,000 invested at 8.5% return with no money added = $1,155,000

Just for fun, over 50 years the results are $2.95m and $5.9m respectively – literally double the money.

And if I begin adding $30k per year (which I probably will) it ends up looking like this over 30 years…

$100,000 + $30,000 annually at 7% return = $3,595,000

$100,000 + $30,000 annually at 8.5% return = $4,882,000

1- The tax savings might be slightly higher since the gearing may lower the dividend yield due to interest costs. This means the net yield distributed by the geared ETF would be lower and therefore less tax on dividends. So it ends up being a higher proportion of capital growth vs income. It remains to be seen how much turnover these funds have over time due to rebalancing so I haven’t assumed any benefit.

2- If you’re wondering where the 5% interest rate comes from, this has been mentioned in a couple of places. Betashares has mentioned their cost of debt is cheaper than average mortgage rates (it was in the 5% range when mortgage rates were 6% according to this interview, and this article puts it at ‘well under 5%’ in July 2025) These funds are able to get ‘institutional’ borrowing rates – better than we can access.

The main downside – and it’s a big one – is volatility.

There will be long periods of underperformance due to gearing. Not only will the funds drop in value more than a non-geared fund, the fund will also take longer to recover due to interest costs eating into returns.

This can be improved by being able to buy more shares when the market is down. That can provide a magnified benefit from dollar cost averaging, given prices will be even lower than a non-geared approach.

I’m also basically locked in. If I want to switch to another super provider later, it will mean CGT to sell and move, which would partly defeat the purpose.

This also adds complexity and admin, though not much since it’s all part of my Pearler dashboard and the investing is all automated. And it may make my investing more stressful when I eventually see sharp declines – maybe a 55-60% fall instead of 40%?

So why am I comfortable with it? Because I meet three important criteria:

1- Super is bonus money, not part of my FI needs

2- I’m able to add to the fund to help improve the outcome

3- I’m comfortable with extra risk and have the stomach for it (due to point 1+2)

I also find geared ETFs interesting and appealing, so part of me sees this as a fun multi-decade experiment to satisfy my curiosity.

No, not necessarily.

If you have a balance under $100k, it might be.

Or if you want (and can tolerate) geared ETFs it could be. But if you have a high balance, an SMSF would probably be better suited (just more admin).

Or if you prefer normal ungeared ETFs and have a balance well exceeding $100k, then the other ‘member choice’ type options work out cheaper at this stage.

Or if you are happy with the sheer simplicity and hassle-free nature of a low cost indexed (or high growth) option with an industry fund.

I’ve been told Pearler is working on making the fees cheaper as they gain traction, and increasing the flexibility with ETF percentages – so I’m looking to see how that goes (and gently pushing for it in the background).

There are definite use-cases here, but it’s certainly not for everyone.

There you have it – my new super strategy.

In short, I’ve switched to Pearler Super to improve tax efficiency and access geared ETFs.

It’s higher risk and higher fee than the simple approach I had before, but with decades of compounding to work its magic, I’m comfortable with that trade-off.

Again, this isn’t a suggestion or a recommendation or anything like that. But it’s a fairly significant change to my long term investment approach, so I felt compelled to share it with you.

Time will tell how well it goes, but I’m excited to let this strategy run and see where my super ends up over the next 30 years.

Hopefully this gives you some ideas to think about if you’ve heard about the ‘pooled super’ tax issue, you’re a fan of geared ETFs, and you’re wondering how else you could maximise retirement savings over the next few decades.

Thanks for reading!

📘 My Book

Your complete guide financial independence in Australia. Available on Amazon, Audible and Spotify.

🏡 Mortgage Broker

Deanna and her team have helped me and many readers with home loan strategies over the years (including debt recycling). Check them out.

💼 Financial Advice

For those wanting personalised guidance with strategy, super, tax, or retirement, I can connect you with someone I trust. Find out more.

If you use the above services, this blog may receive a benefit at no extra cost to you. I only recommend things I use myself and genuinely believe in – thanks if you choose to check them out.

This article explains why being ‘priced out’ is mostly fear-driven hype – and how good financial habits give you the freedom to buy when it suits you (even if prices keep rising).

I just made one of the biggest changes to my investing strategy in a long time. I expect it to make a seven-figure difference to my retirement balance.

Money, freedom, and a better life - delivered to your inbox

Practical insights to help you build wealth & actually enjoy it.

Great read Dave. Very informative as usual. Just a typo with the ART Australian shares indexed fund 10 yr performance. The % return for income account you have quoted less than the accumulation account. I assume they’re arse about face. 😁Confused my ADHD for a moment🤣cheers and keep up the good work

Haha yeah sorry that is a typo, fixed up now, thanks!

Great Article. What is your exit plan or thoughts when you get the stage of being to access this money. Is it switching to non geared or selling down in a low tax environment or just leave alone as you have other funds etc.

Great question. I haven’t thought about it too much given how far away that is, but I imagine I’ll likely leave it in there and perhaps make minimum withdrawals (or leave in accumulation), since even at 65 my timeframe may be another 30 years.

Hi Dave ,

Great read as usual,

For simplicity would it be easier just to invest in GHHF as it is fully diversified ?

If you are intending to invest 2.5 k per month over the next 30 years you’ll not have to worry about the volatility!!

Hey Mick. Yes that would be simpler, but the rules are maximum 40% in GHHF, that’s why I’ve added the other funds.

In theory, if investing regularly, the volatility could actually boost performance further due to being able to buy at even cheaper prices during downturns vs normal funds.

If people have their insurances (income protection etc) with their super just be aware if you change now you’ll need to do a full medical and there will likely be exclusions. This is all since covid.

Insurance can be affected by switching super, but I’ve never heard of mandatory full medicals. Is that really true? Can you point me to somewhere I can read about it?

Hi Dave ,

this is true we set up a smsf and took out insurance back pre covid and the insurer sent out out a medical professional to do the full medical at home !

So I wonder if it is SMSF specific then, or every super fund?

Possibly smsf specific

An advisor told me one time that anyone can take out an insurance policy through their super up to a certain amount even with pre existing ailments and the insurance company has to accept this ,

That was a good few years ago whether it still applies i don’t know

Thanks Mick – I’m happy to be shown otherwise since that would be news to me, so we’ll see if the other commenter replies.

Are Pearler planning to add insurance options down the track? That’s one reason I wouldn’t change at the moment.

Yes within the next 6-12 months, it’s a requirement of the regulations from what I’ve been told so definitely coming – same as retirement/pension accounts, which they haven’t built out yet but are coming.

Hi Dave, have you considered how the risk adjusted return looks if interest rates rise? Given this is a 20 plus year plan there is a real non zero risk of interest rates rising to a point that leverage is no longer profitable. At this point you can’t just deleverage.

Have you considered the drag on your portfolio using pearler fees compared to a smsf in say 10 years time when you have a significantly higher balance? With a smsf you can just change provider without realising capital gains if the admin provider changes fees or a cheaper option becomes available. Have you also considered the cost of stake smsf can be halved if you invest yours and a spouses super into the same smsf?

Hi Dean, good questions.

There will absolutely be periods where leverage is not profitable during various markets – that will happen at high and low rates, just due to different market environments. By definition, anytime returns are under say 5% pa at current rates, then leverage is not profitable. So I’m just working on simple long term averages and what I consider reasonable expectations. In the case that it doesn’t work out as expected, I’m also fine with that (and importantly, unaffected) – I simply made a big long term bet and it didn’t pay off.

After talks with the Pearler CEO I do expect there to be a fee cap at a decent level at some point in the next few years, meaning benefits of scale will kick in and the costs will come closer to the other options for larger balances. So I did think about the SMSF route and the longer term picture, but I preferred this simpler approach – a little bit like many will still prefer the index option with industry funds even with a big balance.

The tricky part is that not only are those lower return periods and higher interest rate periods unprofitable, how the fund internally rebalances the leverage bands (selling in a declining market) and how they pay for the increased cost of leverage (may need to sell shares to cover interest cost if interest rates become to high, especially for ggbl with its lower distributions) may become a lot worse off then may be first apparent.

Yeah it’s a magnified outcome – the drawdowns will be sharper and longer. I can’t imagine you’d have 7%+ rates for very long during a heavy market downturn – so while it’s a possibility, those conditions are unlikely to remain concurrently for a drawn out period.

Re the new GGBL – cool, I hadn’t seen that recent development.

Yeah you are probably right. Would be cool to see a maths wiz back test the data to approximate ggbl returns for the last 30years if it existed. Could use the returns for van0003au(managed fund version of Vgs) as it has been around for a long time and use 1% higher then federal reserve cash rate for leverage cost. Factor in the higher mer for ggbl as well as managing the leverage within the rebalancing bands as per their pds and then we would have an approximation of how ggbl would have faired.

Yeah that would be interesting, I’d read that 🙂

Start and end dates matter too, and DCA vs stagnant investment, so it all gets rather complicated very quickly and would only work as a very rough guide at best.

Great read as usual this has been on my mind for a little while. For simplicity whilst trying to figure it all out. I have stayed in my Hostplus pooled fund and changed it all to 100% Indexed International Shares my balance is currently 320K. Will look into this more as we enjoy our mini-retirement can’t believe how quickly the time is going two months gone already. I am revamping the blog too with this time off. Living Life on My Own Terms:

Thanks TR. Great to hear you’re enjoying a mini-retirement!

I really do like the indexed industry fund options and have had that setup for the last half-dozen years or so. Very simple, low fee, and never have to even think about it.

Hi Dave,

Another banger article as always! I recently switched from Hostplus growth indexed option, and the fees are a lot cheaper than my previous super fund (Cbus) with the same investment option.

It’s crazy how little optimisations make a huge difference over many decades. It’s such a shame that most people are completely unaware, which I think is bonkers!

Thanks James. Nice work mate – and yeah totally, those little long term tweaks really do turn into massive numbers!

I have also messaged Pearler to enquire about capped management fees.

I like the idea of escaping the pooled investments. I have been invested in the same account/fund for almost 20 years without switching so the tax provisioning must have hurt during that time.

I also like the idea of geared investments for the next 20 years of growth.

But my balance is enough that the Pearler management fees are a lot higher than where I am so I’m staying there for now.

Yep makes sense.

I’m fairly sure the cap will come. I think they’re just trying to find a good balance of being appealing while also being affordable on their end. If cap is too low it becomes loss-making for them I believe.

Hi Dave, I think your reasoning is sound and I have no doubt that when you do access your Super, I’m sure you’ll have a lot more than if you didn’t go down this way.

What I’d like to know is, “Why”? Not trying to gate keep here, but you have already retired. You’ve hit the mark and won. You have achieved what presumably all of your readers want to.

The answer appears to be simply, “mo money”! I could be wrong, but it seems against the lessons of the early fire people. This is doubling down and even gearing to have a bigger pot for when you’re old and already been retired for 30 odd years at that point. What are you wanting to have when you’re 60 that you don’t have now apart from, “mo money”!?

Today’s lesson seems to be, keep optimising and let’s gear it up forever even after retiring. Let’s get more, more, more! I honestly thought you were at the point of, “enough”. Not, more, more, more.

I guess I probably approach it differently from many people. I don’t believe in the mantra of ‘when you’ve wone the game stop playing’.

By this logic, any extra money I have I may as well park in cash, since the idea is to only take as much risk as you ‘need’.

It’s not about ‘wanting’ anything I don’t have now – it’s simply for the sake of enjoying the game – I’m not sure why that’s confusing or why it seems like a contradiction.

Where have I said once you reach FI you should deliberately stop growing your wealth from then on? With extra money that you decide to invest, you have 3 options for what to do with it: take more risk, less risk, or the same risk. It’s a personal choice and I don’t believe any one of those is right or wrong. There are limitless options rather than a set of rules people should follow.

As stated, I’m happy to take extra risk since more wealth over the long run will give me more options on what to do with it. Even if I don’t find this money useful, I can donate massive lumps to charity each year for example.

I’m not sure what ‘lessons of early FIRE people’ I’m going against, nor do I really bother what they are. I simply do what makes sense to me, regardless of what the standard approach or philosophy is. As for ‘today’s lesson’ I thought I was extremely clear that this post is not instructional, it’s for the sake of transparency and explaining what I’m doing.

I understand that we all need to keep our money invested to keep some growth because going cash could mean you could run out. You already have invested to the point where reasonable assumptions and historical returns say that you’re more than fine.

It’s not stopping, “playing the game”. It’s let’s make the final score even higher. You’ve been telling us for years that your lifestyle is simple and you have more than enough to sustain it.

What it appears for all fire bloggers, there is no such thing as, “enough”. It’s let’s keep going forever. I thought I had been reading the ideas of somebody that had really figured it out and was more interested in optimising life knowing that the financial side was more than taken care of already. It appears there really is no such thing for most people of enough. It appears we all want more and more.

I think you’re missing the point of what I’m saying. When people talk about enough, especially myself, it’s about reaching the point where you can unchain yourself from the need to keep working and giving up your LIFE and TIME in the pursuit of more money. In that case, you are literally giving up your freedom and life energy for something you don’t need. By definition, I’m giving up nothing so that logic doesn’t hold.

‘Enough’ has nothing to do with not maximising your long term wealth, or not optimising your portfolio for future optionality. As I said, there are three choices for what to do with what I call ‘bonus money’ in the context of investing. You seem to be only capable of thinking that one (or maybe two) of them is correct, and the other goes against the entire message somehow.

It’s actually quite amusing that you seem to be now trying to make a moral judgement based on an investing strategy and what is literally the clicking of a few buttons on a screen. This tweak has changed nothing about how I spend my time, zero change in my motivations, zero change in life philosophy, zero change in values and principles followed. If you choose to see it otherwise, that’s really up to you – feel free to believe whatever you like.

What I’m getting at is the source of why push for more and more. I’m not seeing too many fire bloggers eat their own cooking. Even after supposedly retiring, they continue to earn more and never really living off the investments.

The legendary 4% rule gets bandied out slot in fire but I don’t believe I’ve ever seen anyone do it. It seems to be untested in the real world. Most (maybe all) just strive to make more and more money.

This concept of always trying to get more money by always optimising and gearing investments, etc. suggests there is never enough. It also makes the writings of a do called utopia if every Jody strived for this financial nirvana a fairytale. The more money people have, the more money that is out there. The more money that is out there, the more everything costs. It is seeming like every single one of us are really trapped rats. Even if you retire early, you have to keep taking bets on finances to keep pace or get left behind.

I am in contact with literally thousands of people across the country in my job. I’ve never seen a single person do it. Not one. Whether it’s possible for them financially or mentally it doesn’t matter. Every body wants more, more and more.

Maybe it can be seen as me making moral judgements, but I’d really love some social proof. Somebody who actually did it and lived off the investments only which is meant to continue growing regardless, but you see, nobody does that. Everyone continues to actively grow their investments. Creating more money out there, trapping every single one of us until you get too old in your fantabulous Byron hinterland property, nice car and possessions, fine all your fancy holidays and did with an enormous stack of money which may or may not go to some relative.

You’re defining ‘eating their own cooking’ by ceasing any wealth building after FI. That’s a rule that you are applying.

Regardless, the reason I believe it happens, as I’ve mentioned many times as an observation in the past, is because people young enough to retire in their 30s and 40s who don’t have to work end up having a ton of time and energy and the desire to be productive doesn’t disappear. So they start new things and some of those lead to more money (like a business or a blog etc), and some of them don’t (like volunteering, raising a family, etc).

I don’t see it as trying to keep up with anyone else – again that’s a measurement you’re applying. I couldn’t care less what everyone else does. I also don’t see anyone as being trapped – I see it as consciously deciding how to allocate your time, energy and money in a way that you are happy with. I see this investment tweak as a fun multi-decade experiment.

If you think it’s all based on fear of keeping up, or greed, or like a trapped rat or whatever else, that’s up to you. But if you’ve been a long time reader of mine, which I think you have, you’d know these potential causes don’t really line up with my mindset/psychology – which tells you it’s wildly unlikely that’s what’s driving it.

Also it’s worth remembering that FIRE content people by definition cannot possibly meet your rule since if they have a blog/pod etc they aren’t fully retired or may be making some cash from it. There are several people in the community who are actually FI who are simply quietly living their life – we just don’t hear about them because they are doing other things.

There are 3 people I can contact in my own city right now – 2 of them have been interviewed on this blog. But none of them are in Facebook groups, forums, etc. One is focused on travelling and enjoying the quiet life, the other is raising his young kids and is focused on his investments. Links below…

‘Michael’ who retired at 32: https://strongmoneyaustralia.com/reader-financially-independent-32/ – with a follow-up interview here: https://strongmoneyaustralia.com/follow-up-interview-early-retiree-michael/

And the guy I call MND, Millionaire Next Door: https://strongmoneyaustralia.com/reader-interview-a-real-life-millionaire-next-door/

Point is, these people exist and I hear from many of them. It’s just that not many want to be sharing their story with the world since they have better things to do 😉

Maybe I’m looking at it pessimistically, but from my viewpoint, this desire to accumulate more and more money even after supposedly retiring traps us all. It traps the rats that have “escaped” and the rats that are trying to “escape”. Greed by any other name, ultimately. Not thing to do with wanting to contribute or having “energy”.

This fact makes your musings of what might happen if “everybody pursued financial independence “ pure fantasy. Greed is what happens. More, more, more money!

I think he gets an adrenaline rush from his geared ETF super portfolio.

I had a look at gearing and it’s not for me nor are covered call ETF’s.

I’m not sure but I think he just disagrees with me on a fundamental basis. My argument is that this desire to continue accumulating money is detrimental to the human race experience. It’s possibly a mental illness. It’s hoarding whether it’s widgets or money, it’s the same thing. It traps all of us and it’s extremely difficult to break out of. Scared of running out of- must maximise – just in case, etc, etc.

These are points I think Dave could

explore if he’s truly retired. Possibly future writings for him. One of his mates that retired has become more

philosophical about it.

I think we would all be better off if we tried to learn The concept of enough instead of never enough?

Definitely more of a philosophical topic imo. On the flip side, if everyone in the world have “enough” and no longer need to work for a living, you’d need to grow your own food, make your own toilet paper and build your own car. Do you know how to fly a plane or do knee replacement surgery?

Forcing warren buffet to quit investing would probably kill him. He enjoys what he’s doing, the money is just a bonus. Likewise for many early retirees still earning some sort of income, they’re not doing it for the money alone. It matters more how people spend their money. My 2c

Interesting read Dave, dollar cost averaging paired with mild leverage throughout the accumulation phase within a super environment followed by the eventual capital gains exemption once retirement age is reached is enticing.

The switching of super providers affecting internal insurances is important to consider for people with pre-existing health concerns however the provided group covers generally aren’t enough to support a family claimed upon when considering current day housing/living costs, personalised insurance cover for young families should be looked into imo.

Cheers for the thoughtful comment Nathan

Could ASIC been onto something about the influencers or Australian FIRE movement. We found out about them through Pearler bank rolling the Aussie Fire book then most of them started changing to Beta shares products because they have lower fee etc. Now most of them have been in hibernation or are walking away from FIRE. The last few standing now somehow seem to stand with Pearler or Betashares or have changed track life happens. Could something fishy be going on.

I’m not really sure what you’re trying to say without saying anything.

For context, Pearler has been involved in the FI community since their inception as it was literally designed with this long term investing community in mind, since every other app focused on trading and pushing people to transact at at the time – nobody had auto-invest and things like that.

They see partnering with people in the space as a good alignment, and myself and others who have partnered with them at various times saw it as the same. It’s a natural evolution and very similar to using something, liking it, then telling your friends. I’ve also been fully transparent about my relationship with Pearler the entire time, including at the very top of this post.

I’m not really sure of the people you’re referring to or where Betashares comes in, or what ‘fishy’ business you are alluding to so I can’t really comment on that. If you’d like to be more concrete or accuse me of something, please do and I can respond to it. But this wishy washy suspicion is fairly useless to all involved.

Would be interested in your thoughts about Netwealth wrap super products. They seem to have a lower fee structure with broader investment options and monitoring.

I haven’t looked at those so I can’t comment much. It depends on what you want to invest in as far as ‘broader’ options go. But the fees look like a minimum of $800 per year from what I can see, plus a percentage, so not cheap. But it would likely scale decently if the balance is big enough. That said, at that pricing for a bigger balance there are SMSFs that would be competitive/cheaper – I believe some can be run for around $1k-1.5k pa.

It is disappointing that you didn’t address my takeaway from the post you got my tables from.

I say that, “it currently doesn’t make sense to use Pearler Super at all when it would be much cheaper to stick with indexed or geared indexed options in pooled funds, then switch to direct investing or an SMSF with a high enough balance.”

If one has read my article on gearing or has asked me about gearing in Super, they would know I’m referring to CFS Super and their CFS geared indexed options. I recently made a comment in that post roughly calculating that using CFS for gearing is around 0.30% cheaper than gearing in Pearler Super.

So I stand by my statement that it is currently cheaper to use CFS for gearing and then switch to SMSF at a high enough balance.

Hi SK. I was mainly referring to indexed pooled options in comparison. Switching to a individually taxed option still seems to be profitable overall after costs given the differences in net returns. From my math it looks like it can still come out ahead overall by about 0.4-0.5%. So then ‘cheaper’ doesn’t mean better. And this isn’t regarding gearing, but just the fee/tax tradeoff.

So you are disregarding the benefit of tax and only looking at fees, which I disagree with and that’s why I didn’t write as such.

I haven’t seen your comments around CFS gearing, so I didn’t mean to disregard that, but I’d be happy to look at it if you can send me in that direction? I found it difficult to find the right info regarding CFS funds, so I’m happy to look at what you’ve found.

Is your comparison including the CGT provisioning or just overall fees? Given tax provisioning is basically an indirect cost, I would want to include that in a comparison to see an investor’s net returns. So like the first example, I wouldn’t consider ‘cheaper’ as more appealing because of that.

Edit: I found your comment and it looks as though you’re just looking at fees, with CFS being 0.3% cheaper. These are still pooled options though, correct? That’ll mean potentially 1% pa in extra tax, which needs to be accounted for. If that’s true, I disagree that it’s a better option. I think we need to look at the overall picture, not just fees for basic ETFs or fees for geared funds – that’s incomplete.

Having a comparison include CGT provisioning is complicated because the answer can be different from person to person. So, I created a spreadsheet to try model the difference between Pearler Super and CFS -> SMSF: https://docs.google.com/spreadsheets/d/1qNn1Mj_1jlU4fbiXyCLQDP9lEiV3yhGPFBSmzGOXJ3A/edit?usp=sharing

With my base assumptions, the two are surprisingly close, however, that’s for people starting completely fresh. If you already have a decent chunk of balance, the CFS -> SMSF route looks more favourable, at least when plugging in my own variables.

A quick background on CFS geared indexed funds, around 0.45% gross MER and around 1% net MER, 40% – 50% gearing ratio (around 2.22x), and the Aus geared index is dynamically leveraged where it changes its leverage depending on the borrowing rate and dividend yield.

Thanks for the info, that seems a better comparison. Good spreadsheet too by the way, would take me till pension age to make that 😄

As you say the variables change it a lot – it’s an interesting exercise. The bigger the balance you start with, the sooner SMSF is more cost effective – that makes sense.

Starting from say $100k, it looks like the CFS > SMSF option starts to edge ahead after roughly 20 yrs under the current fee structure. $150k takes 8 yrs, and $50k takes 32 yrs.

After talking with Nick from Pearler about it a few times, I do expect a cap to kick in at a somewhat decent level, which would change that again. On that point, it looks like you assumed a fee cap of $3,630 in the modelling. But isn’t that for families? Unless I’m mistaken, the PDS says the admin fee is only charged on the first $500k for a single account (so wouldn’t it max out at $1,760 + brokerage/recovery?).

Actually there also seems to be something weird happening when I plug in a starting balance. Say $50k starting – the tax provisioning stops at $150k total. And it stops at like $110k balance when starting with $100k. It seems to be double counting starting balance and thinking that = $200k so tax provisioning stops, making the CFS section look better than reality and improve the breakeven point. Unless I’ve done something wrong?

Not sure how I got $3,630. Replaced this with $1,760 and fixed all the other mistakes you mentioned. Thanks for double checking my calculations!

Pearler now looks more favourable in a lot of scenarios and a SMSF becomes worth it if you already have over $150k. It seems my intuition underestimated how much the CGT provisioning would impact the portfolio at the beginning. Might actually consider Pearler Super, depending on if Betashares releases their super product soon.

No worries, thanks for creating it and updating the figures. I’ll grab those tables and update this post to match.

Hopefully Betashares super ends up better than Vanguards… which didn’t really end up delivering. They’re certainly outcompeting them on ETFs that’s for sure!

Oh, and also the my tables you linked in the article uses the wrong Pearler figures. I’ve updated the pictures in my post: https://www.reddit.com/r/fiaustralia/comments/1jqe95t/quick_comparison_of_pearler_super_vs_direct/

Hi Dave, really great article. Super isn’t discussed too much among FIREys, for obvious reasons, so I appreciate the deep dive.

I’d love to hear more of your thoughts on geared ETFs in future! It seems… unexplored. If you’re willing to bet on a broad market ETF like VAS, VTS, VEU, etc. going up over the long-term, then why wouldn’t you take out a geared ETF holding more or less the same assets? Sure, the fees are higher, but so are the returns. I just can’t see a good argument against it if you’re willing to buy the unleveraged version.

Thanks Geordie, glad you found it interesting.

In case you missed it, I’ve touched on geared ETFs before, and linked things in this article about it.

I discuss it in part of this article: https://strongmoneyaustralia.com/should-you-borrow-to-invest-in-shares/

I talk about it in this podcast: https://open.spotify.com/episode/2nuaPoGfGERJEz4aRUCKQL

And I speak more in depth about some potential issues in this article (except not specifically for the newer geared ETFs that I’ve mentioned here and in the above linked article): https://pearler.com/learn/read/leveraged-etfs

In theory, they’re a great idea. In practice, it takes a strong stomach and risk appetite. Plus there are potential complications when it comes time to live off the portfolio given the volatility will increase risk when you become reliant on it.

Thanks Dave! Looking forward to your new book. Keen to get uni done for the year and binge it when it comes out!!

I appreciate that and hope you like it 🙂

A tip for anyone thinking of switching super funds: if are planning to claim a tax deduction for after-tax contributions made into your OLD account, be sure that you submit a “Notice of Intent to Claim a Tax Deduction” BEFORE you close the old account. I naively waited until tax time and then contacted my old fund to get my “Notice of intent to claim” for the non-concessional contributions I had made at the early in the tax year. Unfortunately I found out the “Notice of intent to claim” can only be issued while the account is still open. So I’ve missed out on the tax deductions for the contributions I had made into the closed account last financial year. Bit of a bummer. It was an expensive mistake.

I hope others can avoid this costly error.

Damn that’s good to know, thanks for sharing. That’s a bit shit on their behalf lol you’d think it would still count… it’s just a form that says you contributed after all.

Hi Dave,

I love your content! I wanted to call your attention to the tracking error of leveraged ETFs – because they reset leverage on a daily basis, so in effect they “lock in” your losses on a daily basis too. As a consequence they will always underperform the 2x index on a long-term basis by design:

See quotes from investopedia:

– Leveraged ETFs a designed to deliver multiples of the daily performance of a specific index or asset.

– …. are used in scenarios when quick, significant market moves are expected. However, their complex nature and the impact of daily rebalancing make them unsuitable for longer-term investments.

I hope this is useful!

here: https://www.investopedia.com/terms/l/leveraged-etf.asp

Hey Bukszi, thanks! These geared ETFs do not rebalance on a daily basis – instead they rebalance within bands which are the limits of the ETF (say 30-40% for example), so that doesn’t quite apply. I explain that in the podcast I linked to in the article and discuss how these newer breed geared ETFs are different and why they’re more appealing than previous options.

Hi Dave,

No real mention on impact of volatility decay in geared ETF’s. Is that because the ETF’s you chose are internally geared? In the broader context of discussing geared ETF’s, it needs to be considered.

Hi Barefoot. Yeah that’s correct, these are a bit different as they aren’t rebalanced constantly. I did discuss that aspect in the podcast I linked to in the article where geared ETFs were discussed more at length. The aim of this post was to explain my changing strategy and the thinking behind it, rather than a geared ETF deep dive.

I’m wondering about the danger of being locked in compared to a super fund with a pooled approach.

With the pooled approach, you can change funds and investment options without costs (noting the cost is hidden).

Correct me if I am wrong, but with your approach, you can’t switch out of either Pearler or the selected EFTs without incurring CGT.

Both Pearler Super and the geared investments you’re using are relatively new, so what happens if they don’t work out and you want to switch to a different fund or different EFT?

Thinking this, I played around with some figures. Assuming assets are held for more than a year and super funds pay 15% tax on 2/3 of the capital gain, then the minimum holding period for the non-pooled approach to be better (assuming the non-pooled approach has higher returns) is:

Return difference Minimum holding Period

1.00% 0 years

0.75% 6 years

0.70% 8 years

0.50% 20 years

I must say this did surprise me – I was expecting longer holding periods. Even at the 0.75%/0.70% level, the difference between the pooled and non-pooled approach is less than $1,000. This means you can try a non-pooled fund and see how it goes, and if you find it’s not performing, you can switch back for a lot less than I thought.

So, in conclusion, I think your approach looks good. I’m suggesting it’s questionable if you only earn an additional 0.70%, and you’re expecting an addition 1.50%, so even if you’re out by 50%, you’ll be better off! And if it doesn’t work out, it’s not going to cost much to change.

Hey Roger – that’s correct, it’s basically a locked in approach to delay/forgo CGT, otherwise it does end up getting taxed.

One thing to point out here is the geared ETF options were really the driving force behind this decision – the tax saving alone wasn’t enough of a factor, otherwise I would’ve picked a different ‘individually taxed’ option earlier.

The main risk here is if Pearler Super shuts down for some reason (which seems incredibly unlikely, since they would’ve done this with a multi-decade horizon in mind). And as for geared ETFs, it’s possible I change my mind about these I guess, or the strategy itself doesn’t work out as planned. So yes, both of those are risks. And then there’s the idea of the funds shutting down, which also seems remote to me given they aren’t ultra niche options – they’re popular indexes with a bit of leverage. So I think it’s reasonable to expect them to be popular over time (GHHF is well over $100m already for example).

That’s my thoughts on it anyway!

Thanks Dave. I’m reasonably comfortable now that switching costs aren’t that high, so changing at a later date is not prohibitive (unless of course it goes really well, and in that case, why would you switch?).

I’m too old for Pearler Super, but I’ll get my kids to consider switching. They’ve been using Pearler for EFT investing since they were 18, so this is a logical next step for them.

Hi Dave,

I know that geared ETFs don’t have ‘margin calls’ per se, but is it possible that a big enough crash would completely wipe out one’s investment? I’m talking a Great Depression style crash with equities falling 80+% peak to trough. I know that style of crash is unlikely in modern times because of modern understanding of monetary policy etc. but is it theoretically possible to blow up one’s entire geared portfolio?

Anything is possible, but highly unlikely due to rebalancing if the market fell over an extended period. In a truly devastating scenario, the fund could also struggle to refinance credit, but they’d typically have backup lenders in place (which may or may not work). Or the fund may be wound up if it shrunk in size to the point where it wasn’t worth them running anymore. So several risks could play out, and for that reason I wouldn’t bet my whole FI portfolio on it.

Hi there

I invest from the Pearler account and stumbled acc this belong after an email that popped up.

I want to learn more about super. I am still learning and also wanting to figure out of my current super with Aware super when I worked for the government this was the default one. Nearly $80k in there and from what I can see I’m in a high growth 100% and unit price 12.099070. It’s says super long-term returns

8.83% p.a. over 10 years[P1]

A strong 8.83% p.a. over ten years to 30 June 2025 is great news for members in our High Growth option, where a majority of members are invested.

Would like to know advice on this and do I need to also look at fees? I remember in past I did a chat gpt and said the fees and other stuff were pretty low but yeah just feel I need to make sure I’m setting up the right thing with the right place before I could self manage.

Thank you

Hi Natasha. I can’t give you personal advice, but I will say that ‘high growth’ options tend to be fairly decent – better than the default or balanced options in my personal view.

I’m also a fan of using industry funds (like Aware) and picking the low cost shares option – that’s what I had for a long time before this switch, only I was with Australian Retirement Trust.

Thanks appreciate you replying !

Hi Dave,

Thanks for all yor hard work I’m a loyal reader and listener. A recent article on Firstlinks

by Peter Winneke titled 13 Reflections on wealth and philanthropy was enlightening in regards to Christopher and your discussion.