I started this blog a few months after I left work, back in 2017.

Since then, it’s steadily gathered readers and grown into a nice little community.

I hear from many of you on a regular basis. Some Perth locals have even become good friends.

And although you know a lot about me through my content, I don’t know that much about you. Not really anyway.

The Strong Money Survey sought to change that. And the hope was, your feedback would help me learn more about you and what you might need help with.

Because this whole blog exists to help people create freedom, not just for a mid 30s guy to entertain himself with his own musings and the odd rant (though that’s fun too, not gonna lie).

In this post, we’ll run through some interesting data points, common themes, and you’ll gain greater clarity on who exactly your fellow Strong Money readers are!

You already know they have outstanding intellect and taste in blogs… but what else? 😉

Let’s take a look at some of the more interesting findings from the survey.

AUDIENCE

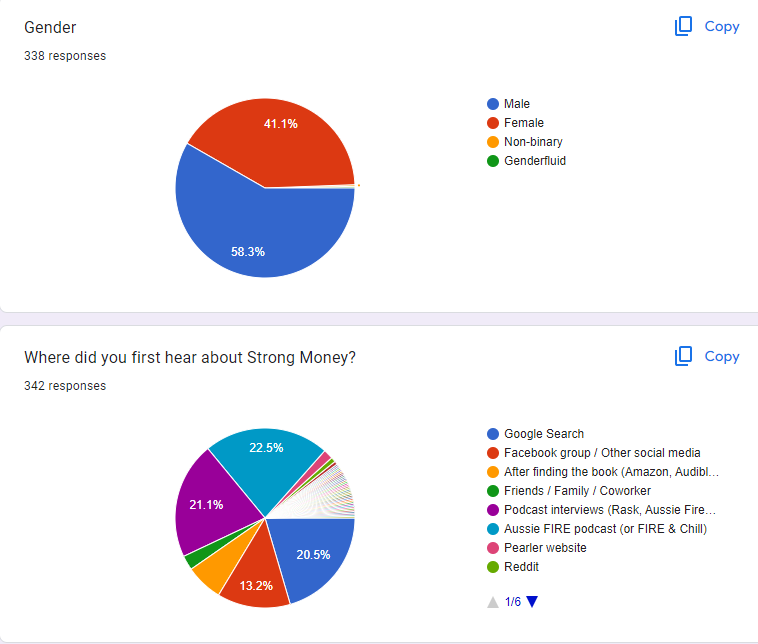

The gender split is more even than I expected. For some reason, I thought it may skew more male, simply because people like consuming content from people they can easily relate to.

I write for thoughtful people who are interested in ideas and making great financial progress in their life. I actually don’t care who they happen to be. And I won’t be changing anything to try to cater to anyone either.

It irks me when companies or individuals blatantly do that. I find it to be a backwards way of operating. The leader then becomes the follower, trying to be what others want them to be, rather than just who they are and doing/saying what they want. You might lose a few people along the way like that, but at least it’s real and genuine.

HOW YOU FOUND ME

As for where you found Strong Money Australia, it’s fairly mixed.

The biggest source of readers seems to be coming from podcasts. Whether that’s through me being interviewed on various shows, or through my own podcasts.

Combined, these channels accounted for more than 40% of readers. That’s way more than I would’ve thought. Audio is simply a huge market that people can’t get enough of, so it makes sense that lots of people might stumble upon me that way.

Then there’s good old Google Search at 20% and Social Media at 13%. A bunch of you wrote that you found me from media mentions, other FIRE blogs, and many said you’ve been reading so long you can’t even remember. Haha, I guess that’s a good thing!

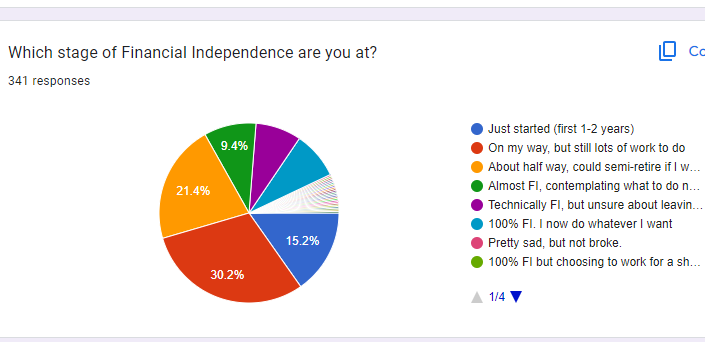

The options are a little cut off in this image, sorry about that. I’ll flesh these out properly. We’ve got roughly…

30%: On my way, but still lots of work to do. I imagine this as you’ve started and made progress, maybe a few years in, but you’re not half way yet.

21%: About half way, I could semi retire if I wanted.

15%: Just started, first year or two. Still figuring things out.

9%: Almost FI, contemplating what to do next. How exciting!

9%: 100% FI. I now do whatever I want. The glory group 🔥

8%: Technically FI but unsure about leaving work. I knew this was a decent number of people. And guess what? A bunch of that 9% – Almost FI – will make its way into this group relatively soon.

A bunch of the personalised answers also mentioned being FI but still working due to enjoyment (which I would add to the other 9% FI doing whatever they want).

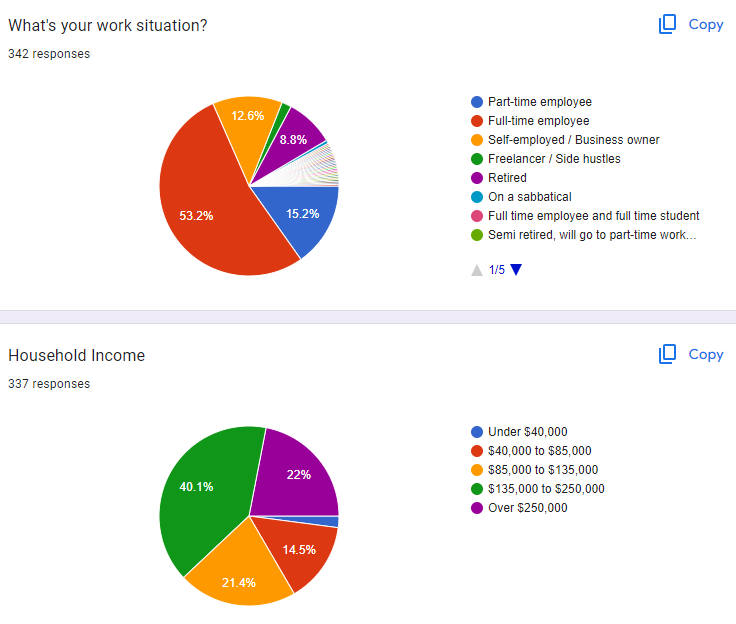

With this level of progress in mind, let’s now take a look at the money side of things. What does the income, wealth, and work situation look like in the Strong Money community?

More variety in work situations than I thought.

I suspect that’s partly due to many survey respondents being part of a couple where one does part-time work due to parenting needs.

On the income side, things look pretty healthy, with 62% of the audience comprising households making more than $135,000 (often much more).

Nearly a quarter of the audience makes a quarter-mill per year 😲 That’s incredible!

I’d say a good portion of the red group – 14% earning between $40,000 and $85,000 – is comprised of singles, younger readers, and retirees.

So, as a group, you’re definitely earning decent money. But have you been able to translate that into wealth? Let’s take a look.

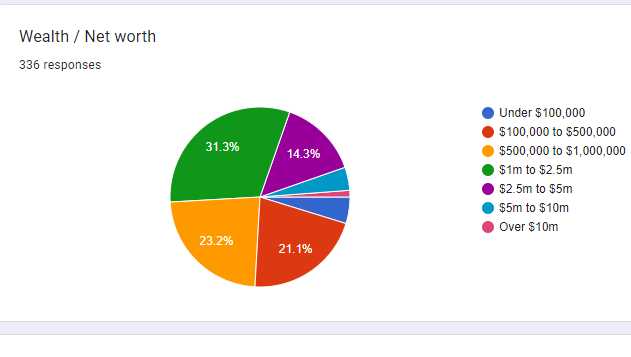

Holy shit! Adding up the percentages, I can see that roughly 20% of the audience have a net worth of more than $2.5m.

In fact, over 5% are worth more than $5m, including a few that are past $10m. Looks like we’ve got ourselves a sizeable community of high rollers!

I’m impressed with those numbers. Even though I could probably learn more from these people than they can from me, the fact that they choose to hang out here means the rest of us are on the right track 😄

For those wondering, I did not specify what assets to include in the calculation. So this is likely to be all sources of wealth: home equity, investment property equity, shares, super, cash and possibly even other assets like a business.

This lines up with the earlier finding that lots of you are half way to FI or further. That’s way further along than I had assumed, which is fantastic. It could also be because my content tends to go beyond just beginner stuff, so those further along gravitate here.

Free Resource: I created a spreadsheet to keep a running estimate of my dividend income and wealth breakdown. I’ve used it for years as a way to help plan my finances and watch my progress over the years. You can get it below.

Not everything is sweet and rosy though. There are lots of nagging concerns and anxieties below the surface.

— Many of you worry about the following things: not having enough wealth to live on, house prices, mortgage repayments, sharemarkets being expensive, dealing with rising expenses, finding meaning after FI, and more.

— Some of you worry about how to pull the pin. Some of you worry about how on earth you’re going to stay full time work and slog it out till you reach FI. You could try semi-FI instead?

— Some of you are struggling to save more. But those further along are struggling with spending more (scarcity mindset).

— High income earners are stressed and want to slow down and semi retire but aren’t sure if they have enough. Lower earners are stressed and are worried about how to balance home ownership, lifestyle desires and FI.

See the similarities? Regardless of the situation, there’s always something to worry about.

Of course, some people worry more than others. But there’s a common thread tying all these together.

All this just means you’re human! Good luck getting through this life without any anxieties and worries. That ain’t happening.

I’ve talked about many of these things in the past, and I will again in the future. But many scenarios are unique to the individual and not easily solved with a blog post.

Even if the ‘advice’ or ideas in an article are a good solution, it may not gel with the person on the other end. In any case, there are often many possible solutions to the same problem, meaning I could write the same case study in 5 different ways.

Said another way, the most appropriate answer to a question depends on the person asking it.

Some of you actually asked for content that I’ve already created.

Here’s a few links to topics that were requested…

Getting your spouse on board: How to Get Your Spouse on Board For FIRE

How to deal with taxes after FI: What Are Taxes Like When You Retire Early

Talking to friends and family: Dealing with Awkward FIRE conversations

My detailed property-to-shares transition strategy: Turning Equity Into Income

Having fun without breaking the bank: 50 Low Cost Enjoyable Things To Do

There were also requests to choose articles by category from the blog’s library. You can do this already – simply click ‘Articles’ then click on the menu tab, then hit ‘Topics’. Or use the search function above it.

Some of you said you love recommending my book, and that I should promote it more (no really, people actually said that).

The problem, apparently, is that many folks you know don’t read anything. Haha, not surprising in this day and age.

Firstly, thanks! It’s amazing to see people finding valuable enough to recommend to others.

As for the non readers, tell them to get the audiobook! Either Spotify or Audible will be the best bet for most people, and they may already have a subscription so it’ll be basically ‘free’.

Audio has actually proven to be, by far, the most popular version of the book. Is that the convenience of audio, or my angelic voice? (not looking for feedback on that one) 😁

If you’re wondering what others like about the Strong Money blog and my content/messaging in general, here’s the common themes, distilled from many hundreds of comments:

— Simple, clear and easy to understand.

— Down to earth, and relatable. I make FI seem achievable.

— It’s about more than just finances or maximising money.

— Transparent, honest, and I share what I’m doing.

— No bullshit. I don’t sugar coat things or mislead.

— Optimistic and positive. I encourage an abundance mindset

— Credible. I actually left work and have walked the talk.

— Aussie focused. Breaks down complex topics in a logical, pragmatic way.

— Real life stories + examples from my personal life.

— Open minded. Multiple angles / strategies / viewpoints considered.

Anyway, back to you…

I’ve noticed that lots of you are focused on paying down mortgage debt right now. Given current interest rates, that’s not surprising!

A paid off home is extremely useful in levering yourself out of the workforce, given it dramatically reduces your expenses.

Many of you are also struggling to find others similar minded to you. There’s no easy fix for this. Online groups help. So does getting along to in-person meetups. I’ve been hosting these in Perth and folks are really enjoying them. Other states have meetups too – check Facebook groups like the Aussie FIRE Discussion group for more.

A common theme in the responses was that you’re happy I don’t just promote a bunch of random shit or create expensive courses to get paid. You like that I only endorse or promote things I actually like and use myself.

Speaking of which, my new course is open for the next 48 hours, so sign up right now for $997, get lifetime access and a signed free copy of my book…

Hahaha just kidding, couldn’t resist 🤣 Anyway…

On this topic, some of you wanted to know more about what I use / recommend. These will always be available on my Resources page, which I’ll try to keep updated.

I also don’t want to make it a mile long, so will add to it sparingly. The newest addition to that list is Solar Quotes, the website I used to learn about and find reputable solar installers in my area (a notoriously tricky industry to navigate). That’s my referral link so if you end up using it to get some local quotes, this blog will receive a small fee as a thank you for referring you.

It’s pretty rare I find a company that I’m happy to recommend, but this is one of them. I found the Solar Quotes site to be super helpful in learning about solar and what to watch out for (because there are some traps out there).

At this point there are probably tons of things I could do to make money, but almost none of them are appealing. I’m very conscious of wanting to provide as much value as I can WITHOUT you paying for it.

Don’t get me wrong, I will remain open to partnerships or advertising only where things are nicely aligned, like above. Given my fussiness I expect these to remain few and far between, which is perfectly fine!

There are no immediate plans to change anything fundamental about what I’m doing now. But I’m still thinking through all the info and ideas – there was a lot to digest!

I’m still going to keep writing articles and making podcasts. And you certainly gave me a lot of future topics to cover, leaving me unable to hang up the keyboard anytime soon! So much for retirement 😉

Having said that, I do plan to cover two types of content that were hotly requested…

One of those is more content around navigating early retirement and challenges for those closer to FI. While I’ve covered a bit of this already, there’s plenty more to do.

This is actually the area that Book #2 will focus on. It’s such a big conversation with so many things to cover that I decided it’s worthy of a book. Especially considering there isn’t really much on offer for people in this space – somewhat young and wealthy, and contemplating life outside the traditional workforce.

Anyway, that project is underway as mentioned a while ago. The draft is coming along pretty slowly to be honest, but I’m treating any progress as a win.

The other content idea is case studies and interviews with readers.

You guys are dying to know what others are doing, and how they’re going about things. You want to see more examples of real people doing what you’re doing, and see behind the curtain.

So with that being the case, who wants to be first?

If you’re willing to anonymously share your situation, strategy, goals, wins, and challenges, please get in touch through my contact page and we can chat further.

By the way, you do not need to be at a certain level of progress. I want to showcase lots of different situations.

It’ll be very gentle and open ended where you can share whatever you’re comfortable with, in the spirit of sharing with others. This will help others see what real people like them are doing, offering inspiration and motivation.

If you want the content, you’re gonna have to help me out with this one!

Here’s something I wish I asked: do you invest in shares, property, or both?

My hunch is that around half of you invest in property as well as shares.

Whether you started out in property like I did, or you’re deliberately following a blended approach, I reckon there’s a large amount with at least one investment property.

Even though the FI community talks about shares and index funds non-stop, I suspect the shares-only investors are actually a smaller group than those with a mixed portfolio.

Let me know in the comments whether you invest in both, or just one or the other.

We’ve developed a nice little community here over the years.

And even though our focus is on freedom and a strong set of finances to allow you to live your ideal life, there are plenty of differences too.

Specific personal goals vary, as do your motivations, strategies, and of course, personalities (which affects your mindset and everything else). ‘

I found this exercise really interesting, and it reminded me of everyone’s unique situation. That does make writing trickier, but it’s helpful to know nonetheless!

Thanks again to everyone who did the survey. This won’t be a regular thing, but I may do another one at some point in the future.

At least now I have a better picture of who I’m talking to, what you value most about what I do, and how I can better help you going forward.

Thanks for being part of the Strong Money tribe 💪💰🔥

And now you know who your fellow tribe members are too!

Thanks for reading!

Here are some resources you may find useful on your wealth building journey:

My book: After 5 years and hundreds of articles and podcasts, I’ve now distilled everything down into an easy to follow book. Designed as a complete roadmap to achieving financial independence and retiring early in Australia. Available in paperback, ebook, and audio.

Mortgage broker: My personal broker of 10 years is More Than Mortgages. If you’d like help refinancing or getting the right loan for your needs, get in touch with MTM. They have fantastic reviews for a reason. I’ve worked with them for 10 years and they’ve been excellent.

Sharesight: A great portfolio tracking tool for share investors, and free for up to 10 holdings. It tracks all dividends, franking credits and capital gains, which is incredibly helpful at tax time. Saves me a lot of time and headache!

Just so you know, if you choose to use these resources, this blog may receive a financial benefit at no extra cost to you. Thanks in advance if you do. And to be clear, I only ever recommend things I use myself and genuinely believe in.

Learn how our EV performed on our recent roadtrip and holiday in Southwest WA. What I learned from the experience, plus lots of pictures, recommended places to eat, and more 😉

The numbers behind our recent solar installation and how much we’ll save. A breakdown of solar FAQ, whether it’s a good investment and what to watch out for.

Get my latest content and thoughts straight to your inbox.

A fresh dose of financial motivation to power your journey.

As a data visualisation professional, may I make a suggestion?

Can you turn your pie charts into bar charts? It’s a tad hard to compare the size of the segments when there is more than one slice. Some of the pie slices are quite small and they’re a bit difficult to see.

Somehow I missed the survey but looks like you got enough responses.

For that final question to ask, you could possibly do an investment survey. Probably worthwhile asking what level of mortgage debt is included as well.

I’d suggest a different question for each investment type asking the allocation so we can see what percentage is held in shares, property, other assets, cash, or crypto.

Yeah looking back, quite a few good questions I didn’t ask 🙂

Hey Dave, I didn’t respond to the survey but wanted to let you know I’ve been around since the start (I think Aussie Firebug sent me your way) and wanted to thank you and congratulate your readers for everything you’re doing and creating.

FIRE is mentioned in mainstream media way more now than when you started, and that’s a good thing — before I stumbled across FIRE blogs in 2014 I had no idea what to do with the extra money I was making so I just blew through it all. FIRE got me focused and has changed my life, and with it my family’s quality of life. I’d like to think we’re good people — don’t waste money on mindless purchases / services / comforts, help others financially (donations) and with time (volunteering) and every time an article pops up on my news feed about mortgage stress or the cost of living, FIRE gives me the ability to skim past it like I have a new superpower rather than read it with a sense of impending doom.

Anyway, this is a long-winded way of saying thank you for creating a space for FIRE-minded people to gather and either get or stay motivated. It’s helping create better people, communities and society. One day we’ll get there and you can hang up the keyboard. Till we get there though, please don’t!

Thanks very much Chris! It’s great to see it catching on incrementally and really heartwarming to hear from people like yourself who’ve made positive changes from the content – it really motivates me to keep going so thanks!

Nice one Dave. Some great survey feedback!

I’ve been following along for several years now. I don’t mean to blow smoke up your arse, but you are a true gem in this space; your authenticity, passion, encouragement and relatability shine through.

Keep fighting the good fight mate! Thanks for everything 🤩

Haha cheers Nick, much appreciated mate 🙂

Great data Dave, thanks for sharing. I forgot to submit my survey but I’m also one of the $100k -$500k net worth singles who are <2 years into this adventure. The fact that so many high net worth and high income Aussies are paying attention to your story is motivating and reassuring for us beginners!

Great to have you here Jez!

I’ve been following you for around 5 years years I think. I have to say your content has been quite unique among many others I consumed, and you’ve provided insight around issues in a way that gave me much to think about. In particular, what if everyone went FI? And also about how you set up your life in retirement, what to tell people asking (still a sensitive point for me). Now thinking a lot about the Die with Zero concept that seems like a natural progression for FI people, and how to stay mentally and socially challenged in a work free environment. I do a ton of things, but is it enough? Also interested if you’ve addressed strategies with super as one approaches the retirement age. I’m not sure I’ve seen that on your page. The tax benefits are compelling, and interesting to what degree you make confessional and non confessional contributions to buff it up. Anyway good opportunity to give you a big hearty thank you for your content over the years, thay has definitely impacted my journey!

I think part of this “is it enough” will always be with us as humans. It’s just that the traditional path gives us a way to fill our time that suppresses a lot of those natural questions we have. The fact that you wonder it means you care about what you’re doing, which means you’ll continually reassess and reprioritise as things changes, which damn near automatically ensures that your time is well spent.

It’s just another version of “Am I saving enough” “Could I be happier” and so on. This relentless self criticality that most of us have. But here’s the thing: the people who never wonder about how this stuff, like how they’re spending their time… are the ones who waste the most of it.

Super at a later stage is a good topic, which I haven’t covered specifically, other than to say it’s often a smart strategy depending on certain things. Will have to note that down for future!

I invest in shares and ETFs only. I like the simplicity.

Hi Dave,

I enjoyed reading your post about the results. I remember that Aussie Firebug conducted a similar survey among his followers and being an IT professional, he utilized tools to present the data well on his website. You could consider a collaboration between you and him for a new survey that could potentially attract a larger number of respondents.

In response to your question, I invest in both shares and property. However, I find the following question more targeted: ‘If you invest in property, what was the date of your last purchase and your age?’ I believe this question will yield more interesting insights.

I am 41 and I own 3 investment properties, with my last purchase made in 2016. This was shortly before APRA made it difficult to obtain interest-only loans and tightened lending requirements. Most of the people I’ve met through my residential property investing circles tend to be older, having purchased properties from the late 90s to around 2017. I think age will be a big factor in this question. My observation is that most of the Fire crowd is generally younger, and views investment in real estate as either unethical or too risky due to bad tenants.

Cool to see the results, even if I missed the survey.. I’ve been following you for so long that I fall into category ” don’t remember how I found the blog” .

I loved Fire and Chill and now listen to Aussie FIRE podcast and wonder if you and Hayden can have Pat as a guest speaker on one episode to get an update on his ” shuffling” over the last 2-3 years, I miss his voice and your rants.

Second this. Please get Pat on the pod!

Same! It would be good to hear from Pat.

Haha, I’ve talked to Pat multiple times in the last 12 months, but he’s enjoying anonymity too much for an interview yet… great for him, but sadly for us 😉

Hi Dave. Great survey. I missed it. Have been a bit busy lately. Went bushwalkijg in Kosciousko National Park in Mid April and ended up needing help from the Police to get back to my car. In the process i ended up sleeping under the stars one night. Luckily the weather was good but I am still suffering from very cold hands and feet.

I am not your typical FIRE person as as was already retired when I found you. Been retired since 2008 and have been using the FIRE concepts since then Both my wife and I are now retired and we have an income of around $100,000-$110,000 py, no mortage. I have a CSS (older Fed Gov) pension and my wife has a small AustSuper pension. I am lucky as I setup a SMSF fund way back in 1998 and adopted investing in shares and LICs and now ETFs as you guys have. Anyway keep up your good work.

Hi Dave,

1 investment property and Shares (ETF’s)

Thanks for the content, especially the Fire and chill pod, was super helpful when I was starting out.

Shares only (but curious about property)

Thank you Dave for taking the time. Missed the survey, too busy unfortunately, but much of this article and the one on IP transition to income resonates with me more frequently in our mid 50’s.

Thanks Dave, Quite interesting.

Would be good to know if people include the equity in their PPR in their Net Worth figures. Personally, I prefer a measure I call Income producing assets which excludes the PPR & mortgage.

My logic is that you have to live somewhere. No right or wrong & I measure both but prefer IPA for my FIRE number with a fully paid off PPR.

PS – another Bar chart over pie chart vote (I spend a lot of work time in Power Bi & Excel – Pie charts are banned 😉 – Happy to help you with automating the data set & visuals if you like)

I’d say yes, home equity is generally included in net worth. I can appreciate you’d prefer to see an ‘investment’ only metric though.

PPR (principal place of residence) being counted in net worth is an absolute must. If you don’t, it’s like saying “I have $1m in shares that pay me dividends that I use to pay rent. You have to live somewhere though, so I’m not going to count that $1m in my net worth”.

Or put another way, PPRs do produce an income — just think of it as sufficient income to cover (most) housing expenses.

Dave,

Fantastic content as always. I didn’t get a chance to participate in survey but interesting stats nevertheless.

I used to listen to Fire & Chill pod and found you via AFB. Your content did certainly helped me a lot in my early days of my FI journey along with AFB. I have now reached semi-FI with a prospect of not having to be enslaved with my job to support kids & mortgage for financial security.

I feel great as I take some final strides in my few years of full employment as I look forward to the prospect of being fully involved in raising kids, supporting my older parents and living a more purposeful life – something I never dared to think let alone to action.

Cheers,

A

It’s the possibility for freedom + a more self-directed and tailor-made life that excites me the most and is what I’m trying to spread. So I love to hear experiences like this! Great work 👍

Shares only – ETFs , LIC and Investment Bond. Mortgage free PPR. Previously individual shares, managed funds and investment properties

Interesting to see other people’s situations

I have shares in a super fund my own home plus 2 investment properties

Cheers keep up the good work 👍

You’re a legend Dave.

I invest in shares and commercial property.

I am also retired:-)

Nice! 🙂

Amazing survey Dave!

What I found the most interesting is where most people are at in their FIRE journey, and it definitely seems like a large portion of the audience is at least close to Semi-FI or full FIRE.

And wow, I didn’t know the Strong Money Australia community was absolutely loaded! There’s quite a bit of people with net worth above $5M, which is absolutely insane!

Anyways, great content mate! It’s quite rare to find an honest, genuine and no-bullshit financial content creator that gets straight to the point and that doesn’t try to sell you their $999 “get rich quick” course every chance they get. But you’re one of those rare content creators and honestly you’ve helped me to filter through all the noise and BS in the financial space!

Many thanks to you Dave and I wish you nothing but success! If I was to listen to only financial 1 content creator, that person would be you!

P.S. Also looking forward to the second book 🙂

Wow that’s quite a compliment James, thanks!

Thanks very much for the article Dave. I found this really interesting. I’m only invested in shares, no investment property.

Cheers Rebecca!

I’m not surprised of the level of wealth. Anybody paying attention can see this. All the shopping centres, cafes, restaurants are full. Tradies booked for months in advance, so many expensive cars, housing, etc, etc. Virtually everybody pays by card and paying more for the privilege of doing it. Not many bat an eyelid about it, I can tell you. Prices constantly increase and we all just shrug and pay up.

We are rich people – probably the richest in the world. I know many are struggling, but in this country, that is a minority. Most people here are saving or investing 20% or more of their income and then find that there’s “not much left over for fun”. Well, duh!

It’s true, what you’ve outlined makes perfect sense and matches my own observations. Just seeing it in the results was a surprise for some reason – it probably shouldn’t have 🙂

Very interesting read. Thanks. As you asked, I have only ever invested in shares, and and all my money there. Started with investment trusts in the 90s and then moved into ETFs in 2005 to 2006. Never been a buyer of individual stocks as I am not smart enough to do the analysis and do not have any. “edge.” I own the unit I have lived in for years but do not count it as part of my net worth (as you have to live someplace).

Thanks for sharing!

Can someone help me understand why “you have to live somewhere” means you don’t count your house / unit / whatever in your net worth? I keep seeing it. Isn’t it like saying “you have to eat something” and not counting the portion of your investments that pays for your groceries in your net worth? I’m completely baffled by this. Plus, if you sell the place you own and pay off your mortgage (if you have one), you get actual money afterwards. That money doesn’t disappear, it can be used to pay for stuff like rent or a new place. So it’s net worth. What am I missing?

It’s because Aussies are rich and retirement without a pension or defined benefit scheme here for most people is having a home plus investments that produce an income and never selling a damn thing and simply gifting the lot to the next generation tax free. Most people will happily quote their investments that produce an income rather than their own home, even though neither home nor investments are intended to ever be sold.