![]()

As a part-time money nerd, I’m always interested in new developments in the finance space.

Especially where a fresh approach can improve on what already exists to make our lives easier.

One area ripe for improvement is the home loan space. Often our biggest expense, mortgages facilitate shelter and can even fuel our investment portfolio.

So anything that makes home loans easier, cheaper, or more efficient for the average person is a win in my book!

One company tackling this is Open Home Loans. They’ve brought new ideas to an old industry and look to be shaking things up.

I recently found out about the company and was keen to learn more. By the way, this is not a sponsored post and I’m not compensated in any way. I’m just a curious observer wanting to understand how it all works.

In this article, I interview the founder and ex-banker Sam Philipos and prod him with all the important questions of how exactly Open is trying to simplify and improve the home loan space.

I’ve included a pic of Sam below so you know who we’re talking to. I hope you enjoy the interview and if you have any questions, please leave them in the comments below.

Sam: Open is a fintech mortgage brokerage with a mission to empower individuals to pay off their home loan faster in the most simple and transparent way.

Through Home Loan Active Management technology, Open helps homeowners get and stay on their best home loan throughout their loan duration.

It’s different from traditional brokers because Open actively manages home loans for homeowners from the moment they take on a new loan, using Open Banking. This is the first of its kind. The refinancing pre-application process is also one of the quickest and easiest with homeowners able to pre-apply to refinance in an average of just 7 minutes.

Over the loan duration, benefits are significant such as savings on money, time, effort and having peace of mind knowing you’re on the right home loan.

Open is also radically transparent – equipping people with knowledge that helps them make the best decisions. Open provides that choice and that control. You have the ability to choose whether or not you’d want to refinance or not. It’s having regular expert and trusted information about your loan that empowers you to make the best financial decisions.

In summary, Open is:

Who: Digital Mortgage Broker that provides personalised active loan management to help homeowners achieve mortgage debt freedom faster and easier.

What: Uses open banking technology to analyse the customer’s financial situation and needs to deliver highly personalised home loan rate shopping, bank negotiations, and notifications.

When: Notifies homeowners if there’s a better home loan rate available that fits them, tells them when to stay or switch.

Sam: Yes – we were previously Benevolence Financial Group (bfgloans), a traditional mortgage broker, so we saw the problems our customers faced.

We saw the difficulties they faced trying to find the right loan, apply for the best loan, and manage it until it’s paid off. So we decided to step in and do something about it.

Our goal was to make this easier for our customers, especially their ability to actively manage their home loan and put the decision-making power back in their hands. This is especially important as the duration of most people’s home loans can be for 10, 20, or 30 years.

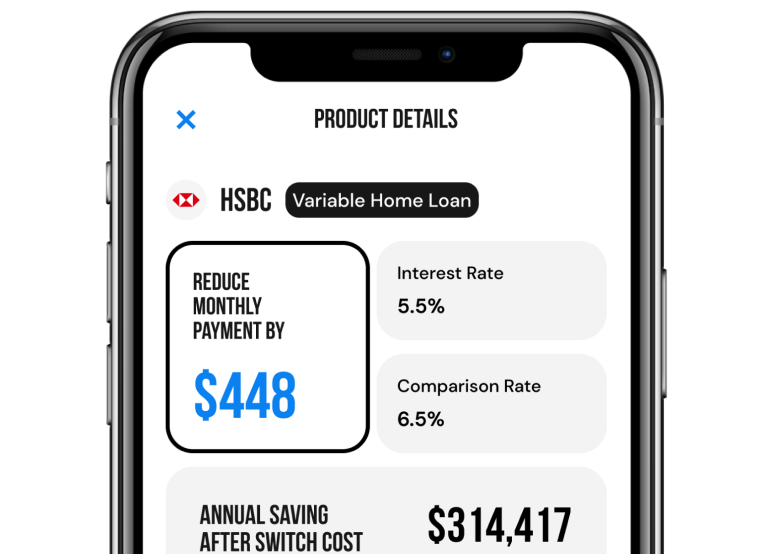

We changed things firstly by giving homeowners direct access to ‘hidden’ rates previously only accessible to brokers.

Secondly, we then made it super fast and simple to switch through our online platform, taking just 7 minutes for someone to apply to refinance – something that would usually takes two-three hours.

Thirdly, we have automated active management for our customers using a ‘tracker’ feature that will alert them when a refinancing opportunity arises that enables them to achieve their predetermined yearly mortgage savings.

![]()

The system can be set to scan the market every three, six, nine, or 12 months, in search of a deal that meets their targeted savings without affecting credit scores. When a customer selects a new rate they’ll need to consent to Open Banking to go ahead with the digital application process.

Traditionally, there has been a gap in active home loan management because brokers incur new costs when refinancing a loan, especially within the first 2 years. Because of our tech and Open Banking, we’ve been able to reduce our costs that tend to prevent other brokers from actively managing customer home loans, which results in thousands of savings.

We’ve worked with a wide range of industry experts to design this. Some of the team included the former CMO of Finder, former CMO of Tic:Toc home loans , and former COO of Ubank. Having a wide variety of banking and consulting expertise helped us expand our vision.

Sam: Yes. Open offers the best of both worlds: convenience and flexibility of a comparison website, with the personalised service and expertise of a broker. We’re a unique blend of both that’s designed to make your life easier.

With Open, you can have peace of mind knowing that your home loan is constantly being monitored to identify opportunities for savings. This means you won’t have to worry about missing out on better rates or losing money in interest payments. The best part? We take out all the guesswork and do all the heavy lifting for you. You have control without the effort.

Say you have a 20-30 year loan. Imagine being able to take off that pressure and mental burden in managing your own home loan because Open is already doing it for you. If you personally feel that’s going to make a huge difference in your life, Open is for you.

Our experience is designed to save time, reduce effort and do things in the most transparent way.

Sam: When homeowners want to refinance, it’s usually broken into two stages: Finding the right loan and qualifying for it. Based on a single straightforward applicant, a refinance pre-application can be done within 7 minutes of the user’s time, provided they give us Open Banking access.

Typically, this process can take up to 2 hours. Open Banking allows us to verify their financial position faster. We still need additional documents based on the bank chosen, which we will communicate with the user to obtain. It takes us a couple of days to confirm this as we have brokers in the background double-checking everything.

Sam: Yes, there is a human component with Open. Once you finish signing up for Auto Negotiator or Pre-Apply, you can expect that an Open broker will reach out to you. They’ll contact you to either update you about whether or not there’s a competitive deal for you right now or whether you qualify for a loan or not.

Sam: An Open broker reaches out to you and verifies everything before moving officially to applications. The first part of the process is automated. You sign up, you get notified, and automation is made possible when you connect your bank through Open Banking. That’s why there’s less paperwork.

Right now, it doesn’t totally eliminate actual paperwork, but it will significantly lessen it up to 50% in the next few months. We are expecting to have that close to 70% by next year.

When you activate Open Banking on your account, it significantly speeds up the process because of the transparency of data in a secured environment. There are still other necessary documents that are not provided by Open Banking so you would have to send those over.

Sam: Under-the-counter rates, hidden rates, and negotiated rates all mean the same thing. These are rates that are only available through your broker or through a bank after you commence the process.

If you go to a comparison website, you won’t have access to this. You would get access to only advertised rates. That’s different from under-the-counter rates.

To empower customers, we wanted to make whatever data is accessible to us, accessible to our clients directly. We do this by gathering our internal data and third party mortgage data providers.

Sam: Almost 75% of all home loans funded are done via the broker channel (not straight through a bank or a comparison website) according to MFAA, 2023.

The trend has shown that ‘low cost’ online lenders have been opening up access to their products to the broker space for that very reason. Examples include 86 400 (now called UBank), Athena and ING are examples of this.

So whilst we don’t have access to all ‘low cost’ online lenders, we find that given our wide range of banks (up to 35 banks), we can usually find similar offerings with minimal differences.

In saying this, we are also working on ways to potentially work with other exclusive online only providers – on the principle that they have fair pricing, reliability, and great customer experience.

Separate note – Keep in mind that some online lenders also do not have access to offset accounts. Which at times saves more than having a purely lower rate.

Sam: Auto Negotiator notifies homeowners if there’s a better home loan rate available that fits them with their current bank or a new bank, telling them when to stay or switch. It’s designed to help homeowners to get big savings, faster and without the effort.

Here’s how it works – there are three steps involved:

First you need to sign up. Connect your loan details automatically through Open Banking or type it yourself. Set your minimum ideal savings worth refinancing for and let us know your feature requirements (e.g. offset account, fixed loan, type of bank etc).

You’ll then get notified – through regular rate shopping, we’ll let you know when a better loan comes up that fits the requirements you set. You can choose to give us consent to negotiate with your bank first to see if they will match it.

Decide to stay or switch, it’s your choice. If your bank doesn’t match the offer, we’ll gather documents needed so you can proceed to be pre-approved for refinancing (in minutes). We’ll do the bank negotiation on your behalf. Once pre approved, we then submit your application formally to the new bank.

Sam: Currently, we show users a shortlist of options based on the loan they’re looking for. By the end of the year, we will have the option to show people only offers specifically related to them provided Open Banking access is provided.

Sam: Our team is diversified and consists of advisors, consultants and staff who have both banking and non-banking exposure.

As a Founder, I assembled a team that aligned with what I stand for: helping empower and improve people’s lives, and sometimes that may come at a cost that we are willing to bear. I also believe in the golden rule, to treat people how I would like to be treated.

Our vision extends beyond just home loans. It’s a future in which every financial transaction empowers people to achieve their purpose.

Think about your insurances, investments, savings, transacting, and lending – imagine if all of them were actively managed for you so that it’s simple, saves you thousands and saves you time. You’ll be in control and have your finger on the pulse, without the hassle.

Sam: Open has a wide panel of banks to have the right product for the right person. Our digital experience currently is focused on refinancing, yet we still can (and currently are) assist investors through the traditional process.

Stay posted, we’re bringing innovation in the investor space too.

Sam: We’re working around a way to make this possible – as long as we have ongoing Open Banking access. For our existing clients who have given us ongoing access, we don’t face this issue so you don’t have to keep updating information. For those who don’t connect their bank, we need to reach out to them every quarter to quickly check-in. That’s why activating Open Banking is really key. It speeds up the process.

Take note that Open Banking access expires after 1 year on Auto Negotiator. While Open Banking access expires after 1 day on Pre-Apply.

After Auto Negotiator access expires, re-activating Open Banking access can be done again in just a minute.

Sam: Yes. As long as you are a mortgage owner, whether you’re on variable or fixed, you have one or multiple mortgages, or you’re looking to get a home loan, there’s a stark difference when using Open.

First, our values are embedded in our name. Open is open. We set out to fix an industry that doesn’t always value transparency and we want to ensure we put our customer’s and their best interests first.

Second, Open offers an alternative to traditional mortgage brokers. The benefits of Open over the life of the loan are more savings, more time, and peace of mind. This is made possible through home loan active management and a faster refinance pre-application. This gives people the power of choice over their financial decisions.

Sam: From a personal perspective, I’ve seen firsthand the impact on families that are in poverty, due to circumstances outside their control. The ripple effects are significant and people in those situations need a hand-up to be able to overcome it.

My heart has been to help those suffering the most and my faith played a pivotal role in leading me to do something about it.

Sam: The assumption might be that Open only caters to refinances. We assist first-home buyers, investors and upgraders. Open is open for everybody.

Whether you’re an existing borrower or if you’re looking to borrow for a property, Open can work alongside you. The huge benefit with Open is, that you’ll get experts assisting you through this journey, possibly your biggest purchase, we know how crucial this is: not only in your finances but in your life in general (loan duration is usually around 10, 20, 30 years).

How did Open make active loan management become a reality?

![]()

I want to thank Sam for taking the time to answer all these questions.

It’s great to see some innovation in the mortgage space. There’s such an opportunity for improvement to make things simpler, quicker, and easier for those of us with home loans.

Having some tech automatically scanning for better rates for your specific home loan needs sounds like a really FIRE-optimiser thing to do. No need to create some elaborate spreadsheet trying to scrape data feeds or collect anecdotal online whispers of what rates are achievable 😄

I’ll be watching this space closely and would love to hear from anyone who’s already used Open (or about to). When I’m back in a borrowing power position I’ll be giving it a try (not quite there yet).

We’ve covered a lot in this interview, but you can head over to Open’s website to learn more or get in touch.

If you have questions of your own, feel free to put them in the comments and I’ll see if we can get Sam to answer them (either directly here, or by email and I’ll update this page).

Thanks for reading!

Learn how our EV performed on our recent roadtrip and holiday in Southwest WA. What I learned from the experience, plus lots of pictures, recommended places to eat, and more 😉

The numbers behind our recent solar installation and how much we’ll save. A breakdown of solar FAQ, whether it’s a good investment and what to watch out for.

Get my latest content and thoughts straight to your inbox.

A fresh dose of financial motivation to power your journey.

Sounds good but why bring something to market that is not completely up and running with all features working. Open banking is not something I would sign up for to save and extra 10 mins work. Will look again in another 12 months, hopefully Dave you re-interview.

I think it’s common for companies to launch new offerings while still building out additional things in the background. Before that, setting up alerts and rules for possible savings and then not having to think about it or regularly check with a broker (or personally) what other rates are around is a super convenient setup for most folks I’d say. After all, rates and offerings are constantly changing which is the nagging part of having a home loan (having to stay on top of it to make sure you’re not getting screwed) 😅

I assume you’re joking Dave – surely no lender would screw its customers 🙂

Haha noooo 😏

Hi Matt, thank you for this question. The main thing missing now is some banks aren’t providing all information that they are mandated to provide by ACCC. The ACCC has made a statement a month ago threatening fines to banks who don’t provide all the information that is mandated by legislation. So we’re seeing in more than 80% of cases there are no issues.

how is this different to similar services like Joust? Also, can they also do construction loan?

I would imagine construction loans are probably fine as I’m sure they still have their full broker abilities to find a lender for that.

Good question, I’ve only briefly looked at Joust, but it does look similar at first. At a quick glance, it seems one difference is the automatic rate scanner/negotiator in the background that will alert you of better rates without you doing anything. And I’m not sure on the ease of use with applications on Joust – it looks as though Open is trying to automate and simplify it as much as possible using open banking. Edit: it looks like Joust is not actually broker, it’s just a digital platform which then passes you on to either a bank or broker.

Have you used Joust before? It also looks interesting.

Hi there, there are two main differences.

1. You can “Apply to Refinance” in just 7 minutes with Open. Meanwhile, refinance applications are time consuming with Joust and they do not do active loan management. After you take out a loan with them, they won’t tell you in the future when a better loan that fits you becomes available.

2. Open’s goal is to save you time when you’re applying and even when the loan is already settled so that you do not have to manually shop around afterwards, we also do bank negotiations on behalf of you. Open does all of this so you can save thousands yearly in interest, without the hassle.

Is it just refinancing or are they open to new applications as well?

Is the payment for the service still the traditional trailing commission model?

New applications for a home purchase or investment are also fine, as far as I know. And yes I believe their business model is the same as traditional broking.

Hi Loo, whether you’re a first time home buyer, looking for a construction loan, on a variable or a fixed rate, Open can be of service to you. We cater to both new loan applications and existing ones who want to refinance. There’s just a different process for new and existing loans because Open Banking only caters to refinances until end of this year. We can expect this to change by 2024.

And correct – there are no costs to you, which is the case with other mortgage brokers. The only difference is we’re the only digital mortgage broker in the industry that does automatic rate shopping, bank negotiations, notifications, and the fastest “apply to refinance”.

Open’s tech allows us to sharply reduce our costs which enables us to not charge. Our goal is to help people pay off their loan faster so they can achieve mortgage debt freedom. That way they can spend their time on things that matter most.

Dave! Thank you for taking the time to do this interview, I appreciate it. We’re excited to be making a meaningful difference in this space, take some burden off of homeowners, and help people consistently get yearly mortgage savings. Hopefully this helps them pay off their debt and achieve FIRE faster.

I’m coming over (digitally!). See you at Facebook, Instagram, or Twitter. Hopefully I can have the chance to interview you next time.

This isn’t going to end well for many because they fail to realise an optimum loan structure and active debt recycling can reduce your home loan much faster than simply choosing a loan with the lowest rate.

I can tell Sam doesn’t come from a Broking background, he has the mindset of a Banker, his first Broking business failed so he’s started this. He says the Broker industry is not “open” to act in clients best interest when this couldn’t be further from the truth.

With open banking your monthly spending can all be lumped in, for example you spend more over the holidays, open banking averages this amount to your application and can easily squash any chance of approval.

The tag line “refinance in 7 minutes” is misleading, Sam mentioned in this article “get pre-approved in 7 minutes” because he knows you cannot refinance your loan in 7 minutes. There’s a loan submission and approval process, paperwork after approval, discharge of mortgage and registration of mortgage etc.

I’ll be sticking with my Mortgage Broker who has been in the industry 10+ years and shown me time and again that lowest rate doesn’t mean lowest overall cost.

A good idea in theory just not in reality.