After last week’s post and thinking about the current health crisis, it’s easy to feel down.

We get concerned about the state of the world and, understandably, worry about the future.

But it’s time to bring some optimism back. We need some positivity to lighten our spirits!

So, in this two-part series I’ll share why I believe Financial Independence has actually become easier to achieve over time and how I came to that conclusion.

Then, in part two I’ll explain why I think we can expect this to continue, and possibly even accelerate. Alright, let’s get started!

If you follow mainstream media, you’ll often hear that people are struggling.

And they don’t mean poor people. Instead, these ‘battlers’ are firmly middle-class Australians getting squeezed by the ‘spiralling’ cost of living and numerous other pressures.

And all this is happening while the rich people grin and cackle, gently caressing piles of hundred dollar notes on their oversized marble desk in the home office of their waterfront mansion, which was purchased with just a portion of last year’s bonus cheque!

…Or something like that!

Well, there’s great news. This ‘big squeeze’ is not really true.

Of course, things aren’t perfect. Yes, there are a million finer points we could debate. But the broader truth is, becoming financially independent is more possible than ever before.

And it’s a trend I don’t see stopping. Here’s the thinking behind my optimism…

We can see (hopefully), throughout this blog how it’s totally possible for most middle-income Aussies to retire early.

With the only real requirement being to design an enjoyable lifestyle where costs don’t blow out, and religiously tucking away chunks of savings into sensible long term investments.

But doesn’t this make you wonder? How is this even possible in the first place? Why haven’t tons of people been doing this for decades? And why does it seem like all of a sudden it’s now totally doable for a large group of people (the FI community)?

Now, there have long been cases of those with wealth retiring from business to focus on other things. But here, I’m talking about the masses… the middle class.

Since I have plenty of time on my hands, I often wonder such things on a lazy weekday morning. And I’m a simple guy, so let’s break this down in simple terms 🙂

By the way, I’m no expert in economics or history, so forgive me for any inaccuracies. But I believe the broad principles and core message to be true.

Basically, because our standard of living has increased so much over the last 100 years.

What does this actually mean though?

Well, the portion of our income used to pay for genuine essentials has gotten smaller and smaller over time, as I outline in this post.

Put another way, our incomes have continued to increase faster than inflation, decade after decade. This is often brushed-off or overlooked – sometimes even denied! More on this soon.

Combine this with the increasing power of technology to create efficiencies, making things cheaper overall to grow, manufacture and ship.

Another reason, locally, is that Australia actually has the highest minimum wage in the world. Plus, we have other great systems in place like a healthcare system that our American friends can only dream of!

Yes, houses are expensive in some areas. But renting or other locations are a workaround. Home ownership is a choice, it’s not mandatory. We’re owed nothing. It sounds cliche, but the right mindset is critical.

To dig deeper, I explain how to deal with housing for low-income earners in this post. And I tackle the rent vs buy question here.

On this point, unfortunately 9/10 isn’t good enough for some people. Instead, they’ll focus on the one thing not in their favour to ‘prove’ why FI isn’t possible for them.

It should be clear to most observers that as a nation, our wealth and living standards has kept climbing over many, many decades. Over hundreds of years in fact.

You see this every day. The computers we use. The cars we drive. We can afford extended international travel, near-limitless restaurant food, regular beauty treatments, new kitchens, and the list goes on.

And we barely even bat an eyelid at this stuff. Because it’s normal now. But it wasn’t always this way. If you doubt this for a second, ask the older generations!

Capitalism, despite its issues, has played a pivotal role in this outcome. Our semi-regulated, mostly free-enterprise system has generally brought many wonderful innovations and created massive wealth, employment and increasing luxury for the countries who adopt it.

Humans have an almost insatiable urge to make progress and improve their lot in life. And capitalism tends to help that happen due to the in-built incentives for profit.

We are incentivised to create new things. To solve problems. To do more with less. Because, if others in the economy find our work valuable, we’re financially rewarded for that.

Of course, there’s a lot more to life than profit, and non-paid work is incredibly important (if not more so). But here we’re talking about the system as it relates to incomes, wealth and FI.

The ongoing investment of capital into new projects and technology has created huge innovations and efficiencies, creating much more output per person over time.

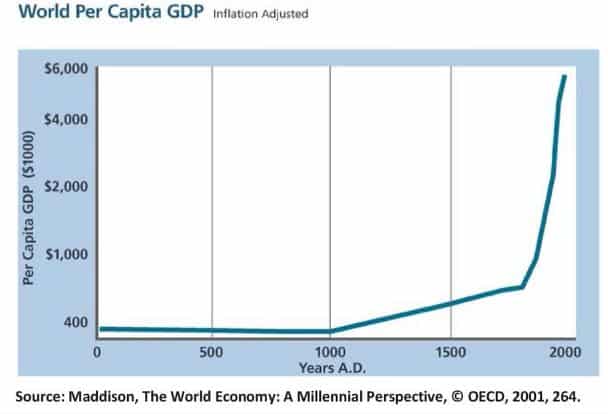

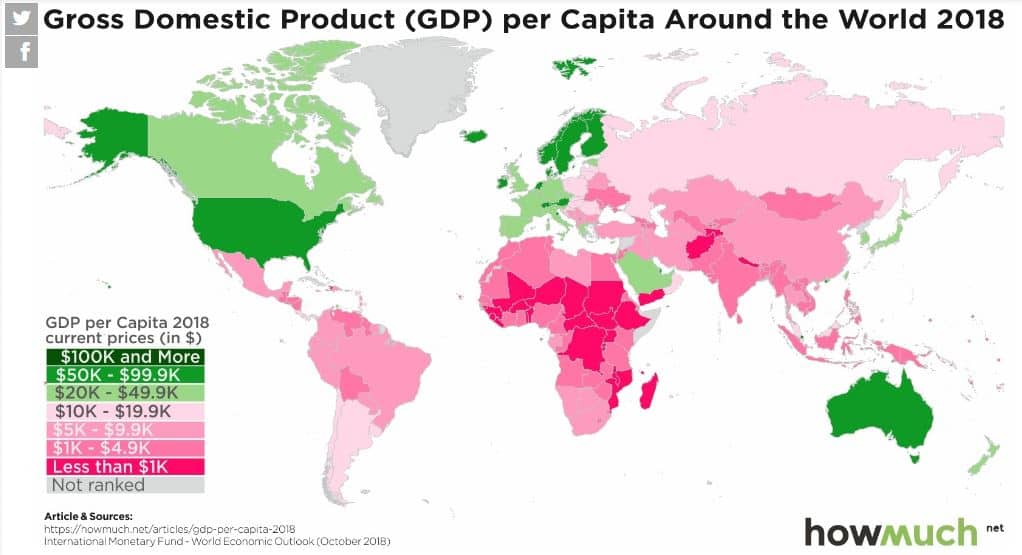

This is most evident as trade, capitalism and technological advancements took off.

See below, the history of world GDP per capita. The second image shows which countries have prospered the most. It’s clear that western countries like Australia have absolutely blossomed.

Innovations and efficiencies allow companies to earn more profit from the same amount of customers. Yet, customers increase over time too thanks to population growth.

In turn, companies can afford to pay higher wages while creating wealth for owners. This boosts the income and prosperity in society.

Efficiency is key in all of this. Each incremental improvement creates higher profits and/or lower costs in real terms.

This value-creation leads to large portions of people with more disposable income than before. And, over time, consumer-driven economies were born.

In case you missed it, incomes have been growing faster than living costs for over 100 years. I did a deep dive into this topic in a previous post: The Real Cost of Living – An Inconvenient Truth.

As part of that article, I used the following from Australian Bureau of Statistics (ABS) to illustrate my point. In 1966, the average Aussie full-time wage was around $60 per week. See here.

Fast forward to 2016, and the average Aussie full-time wage was $1,533 per week. See here. That means the average Aussie wage grew by 6.7% per annum.

According to the RBA Inflation Calculator, the average rate of inflation over that 50 year period was 5.2% per annum.

Clearly, even if you’re not into numbers, this shows wages have outpaced inflation comfortably for the last 50 years.

Interestingly, if wages only grew with inflation, this $60 per week would be $758 in 2016. But the actual full-time wage is now double that!

This means we have twice as much income now, even after adjusting for inflation.

Logically, this should translate into a comfortable 50% savings rate. But unfortunately, it doesn’t work like that. Because our desires and tastes keep expanding to match our income.

This could be true. But the median full-time income is actually very similar to the average, sitting at $1,500 per week in 2018. See here under ‘Distribution Of Earnings For All Employees’.

And for completeness, let’s now look at minimum wages to see how they stack up.

The federal minimum wage in 1966 was $38 per week in Australia. See here.

By 2016, the minimum wage had grown to $672. That’s a growth rate of 5.9% per annum. Again, that’s ahead of inflation of 5.2%, but not by quite as much as median or average wages.

Thanks to compounding, even a minimum wage earner now has 42% more income, after inflation, than the equivalent worker 50 years ago.

Most people think inflation is much higher than what is reported.

That’s because our human bias tends to focus intensely on stuff which gets more expensive, while playing down or ignoring things that have gotten cheaper.

According to the Reserve Bank’s own paper, the inflation figures typically overstate what households actually experience. The CPI inflation figures are actually conservative for several reasons.

— Because it’s a fixed basket, as prices change they assume our behaviour stays the same. But when we optimise our spending as prices change, by shopping around or substituting items, we actually experience much lower inflation than is assumed.

— It also ignores online shopping, and the absolute bonanza of lower cost products available to us, compared to what’s available in traditional retail stores.

— The basket is adjusted every few years to become more relevant. As households adopt newer products, services and generally fancier stuff, it’s then included in the prices they track. These are lifestyle increases, so this ends up overstating actual living cost increases.

— The basket doesn’t properly adjust for quality. On average, the quality of the goods and services we buy tends to increase over time, come with more features etc. This also tends to overstate inflation.

So, I think the inflation figures are actually pretty generous. They account for our increasingly affluent lifestyles, yet our incomes have still outstripped these costs handsomely.

Now I’ll let the RBA’s paper speak for a minute on the topic…

“Over time, individuals may not compare the cost of achieving the same standard of living, but rather that of a ‘reasonable’ standard of living.

Real consumption per person has risen substantially over time, indicating that living standards have increased.”

“What is a reasonable standard of living has also increased, as households have become accustomed

to consuming more goods and services and those of a higher quality.As a result, perceived increases in the cost of living may partly reflect the cost of attaining a higher standard of living for many households.

There is also evidence that individuals’ perceptions about their wellbeing are formed not purely in absolute terms, but partly by comparing themselves with those around them – colloquially termed ‘keeping up with the Joneses'”

The truth is, there’s no shortage of income here. The real challenge is resisting the ever-increasing amount of temptations.

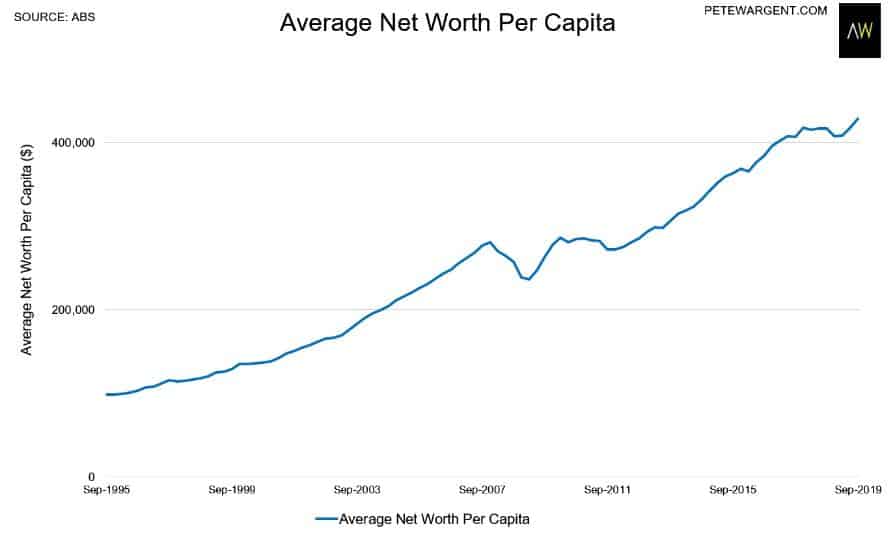

Even in the recent sluggish decade after the GFC, wages have continued to grow faster than this overstated inflation figure. Not only that, but wealth per person has also continued to grow…

The average person on the street would probably dismiss these charts and angrily tell you where to shove them! But that’s because they’re caught up playing the comparison game and focusing on what people further up the wealth/income ladder have.

So even with a less-than-exciting economy, and despite the inevitable bumps in the road, wealth and real income per person have continued to increase steadily over time.

If you’ve been paying attention, I’ve used some of these snippets before. And I’ll probably use them again in the future.

That’s because this shit is important! And it amazes me how many people don’t realise the affluence and incomes we have available compared to the past. Just because it feels normal, doesn’t make it any less incredible!

Over time, the wealth-generating machine that is the global economy has given us more and more income over the years. And, as we can see, this has easily exceeded inflation over time.

The benefits are even more pronounced for people and households who make an actual effort to save and be more efficient (that’s you and me). We’re the ones who tend to get the most from this system.

We benefit twice over because we then invest our surplus cash into productive companies. And this takes on a life of its own, creating wealth and providing us with another source of increasing income over time.

I’m not saying our economic machine works great for everyone. There are always exceptions.

Building wealth and retiring early will prove unattainable for a certain portion of the population.

The sad fact is, many Aussies live week-to-week, with their earnings going out just as fast as it comes in. This is clear with the current workplace shutdowns in the economy and endless queues outside Centrelink.

The incredible part is the numerous interviews of previously employed people sharing their sudden job loss in the last few days. And, amazingly, they proceed to explain that, as of right now, they have ZERO ability to pay next week’s rent or to buy food for their family!?!?

Now, I don’t want to be insensitive. Some people have genuinely tough life circumstances. But sadly, often this week-to-week living is middle-class Aussies who have unwittingly accumulated poor financial habits.

Hopefully you can see the overall trend here, and where my optimism comes from.

Over time, our economic machine continues to generate more income and increasing affluence per person.

That’s why I say Financial Independence is getting easier, on average, with every year that passes.

For most of us, we’ve never had the opportunity that we have today. Even since I began my journey over 10 years ago, things are easier today (coronavirus aside).

Wages have continued to rise in real terms, and the underlying cost of living isn’t increasing by very much at all. A good amount of it, if we’re honest, is optional extras in a modern-day wealthy country.

As the years go on, this extra income gives us a growing surplus to build a strong financial base for ourselves. And that helps underpin a free and happy life.

Next week, I’ll cover why I think this is likely to continue, and possibly even accelerate over the next 10-20 years. Thanks for reading!

Why deliberate spending is my favourite money management style. What it really means and how you can use it as your situation and priorities change over time.

My thoughts on ‘The Great Taking’. An idea that the masses will lose untold amounts of wealth in the next financial crash, due to a deliberate plan by mysterious figures.

Get my latest content and thoughts straight to your inbox.

A fresh dose of financial motivation to power your journey.

Hey Dave, this was such a good read and so true! It is 100% your responsibility as an adult to ensure that you can pay for your bills, especially in the event that you lose your main source of income. There are now so many couples struggling to pay their mortgage because they decided to buy a million dollar home in the first place, and were completely relying on two people with average salaries to make the repayments. Oh and they had an overseas trip planned as well this year that got cancelled – where is the common sense? Like you, I don’t want to be insensitive as it’s tough to see people I care about in financial hardship. Hopefully this situation is a lesson for everyone to save up a cash buffer for their own financial security and to stop living paycheck to paycheck with a grossly inflated lifestyle that they can’t actually afford to maintain. It is sad to see but at the same time an important wake up call for many. We have a world of opportunity available at our fingertips living in a wealthy country like Australia. Be sensible with your money and grateful for the beautiful life you already have.

I agree completely. I don’t have any problems with being insensitive though. Those people who haven’t prepared to support themselves if they lose their job are stupid idiots.

Wonderfully said Aurelia, thanks for the comment!

Thanks for this article, they are always a great and informative read. Look after yourself and stay safe. Cheers Shane

Cheers Shane, you too 🙂

This …. “the portion of our income used to pay for genuine essentials has gotten smaller” Boom.

Thanks for the insight it a great read

In.wake of the current difficult situation this is a very uplift piece to read.

Doing things you like, getting out of rat race

Is easy if we have the right mindset

Keep up the good work lo o king forward for you next part

Glad you enjoyed the article, and thanks for reading.

I started pursing FI in the 1990s after I had left university without a student loan (because it was mostly free) and was able to buy a house at just on 3x my income. I was able to start investing at a young age. It’s different for kids coming out of the education system now. They face years of loan repayments just to get to a $0 net worth. I do agree that incomes are higher and there is a better margin for people these days who choose to live frugally. But student loan debt, childcare costs and expensive housing all seem to conspire to push back the age that the average young person can start making meaningful investments, and hence start benefit from the long term nature of compound interest.

AF –

Student loan debt is only paid back at certain income levels and only grows at CPI

Childcare costs are subsidised heavily for low income families, so if you have a high income you can afford the whole amount

Housing prices vary on where you choose to live, alot of places in outer suburbs less than $300K

Many people are trapped in a mindset that they have to live in a specific location, or have to maximize their income by living in inner city Sydney/Melb to the detriment of their finances.

This is also prevalent in many unemployed, they dont want to relocate to where the work is as it is easier to piss and moan about being unemployed in an area with no jobs.

In the last 2 decades we have seen a significant amount of less educated (non uni grad) people become significantly wealthy by relocating and taking opportunities in them mining sector. How? They simply moved to where the job was and left friends and family behind to forge their own path and work hard for great coin.

Excuses are easy, lazy and self perpetuating.

Hey AF – I have to agree with what JC has said. Many of these costs aren’t as bad as they’re made out to be,or the level of expensiveness is optional in many cases.

I have no issue with house prices being higher as a multiple of income because now we have insanely low rates and most are double income households making mortgage repayments quite affordable – the deposit is another matter but not hard with a savings habit. The other option is renting where rents have not grown at the pace prices have… not even close.

Student debt should mean a higher income later and a higher savings rate, which should more than compensate, and if it doesn’t, then it’s being done for personal choice, not financial reasons – that’s different. Regular unskilled workers in Australia (my partner and I were in this boat) get paid fairly decent wages, so there’s no issue saving there. And having children is a cost of course, but an optional one.

If kids are desired at a young age that’s fine, but it’ll slow down progress for FI obviously. The other option is waiting till later to have kids which removes the childcare issue entirely. It’s totally reasonable for a young couple who work and manage their finances well, to be fully or at least semi retired in their early 30s.

All of which are choices. Student loan..choice, expensive house choice..childcare cost again choice.

To add a slightly different perspective on income levels in this country:

https://www.abs.gov.au/household-income

Note the amount for Median weekly equivalised disposable household income increase over three periods.

Interesting. There’s a lot of inputs to that I’m guessing so it’s hard to know what we’re actually looking at compared to just looking at long term full time wages. My simple mind prefers simple data lol.

LOL. So would I but it isn’t sometimes.

Still, just keep on investing when spare cash is available is simple and easily understood. That and not looking until you have spare cash again. What does that marmot say in those awful adds? Simples.

Let none of us ever forget that there are many, many people in the workforce who make nothing like the average/median income. Take hospitality/retail/child care workers for instance.

Of course. Part of my point all through this blog is that the median full time wage is very healthy, and even minimum wages are good here. With half the full time workers earning more than this, they clearly have an amazing opportunity to get ahead financially if they so choose.

Great read as usual Dave. In a nutshell; Stop buying sh*t you don’t need.

The FI formula is simplicity itself; Spend less than you earn, invest the surplus, avoid debt. Repeat.

It’s the psychology factor, the human factor, that is the hardest thing of all to work on…

Haha nailed it Jeff 😀

Hi Dave ,

Methinks you have omitted an analysis of the debt levels 2020 versus 1966

Take care . Rupert .

Hmmm, I’m not sure I buy the ‘debt’ point. Debt has gotten higher over the years because people have chosen to take it and because it’s affordable. If it wasn’t affordable, people couldn’t possibly service it. But for the most part, they very much can, due to structurally much lower interest rates than past periods.

It’s like a weighing scale… the cost of debt has gotten cheaper which lightens the scale… so people have chosen to add more… while keeping a balanced scale. Full-time incomes are what they are, debt is a choice. People can in fact rent forever and get the benefit of increasing real incomes, while avoiding debt if they like.

Great read Dave. There is also many more ways to create income earning side hustles (like this blog, Uber, Airbnb etc) then ever before and free internet tutorials on just about every DIY job you could think in and around the home, car and office. So there is no reason why most cant turbocharge their earnings/savings and achieve the dream of FI sooner coupled with everything you mentioned above. Thanks for writing and sharing such valuable content Dave

Excellent points Dan. Some mentions of those are coming in Part Two.

Thanks for the comment! A lot of this stuff comes down to whether you’re a ‘glass half full’ person in terms of how things are and also the future.

Luckily for everyone, the government is coming to the rescue and bailing us all out. Why save a portion of what you earn when you have a government that will just go ahead and do that? Thank god *someone’s* doing something about how useless we all are with our personal finances.

Haha that’s one way to look at it Chris, and I really hope that doesn’t become the prevelant viewpoint of society – forever living for today and hoping (expecting) to be bailed out when trouble hits… maybe we’re already at that point?

Sad as that is, if a large % of people think like that… the govt has little choice and almost has to cater to that.

The blog post at Greater Fool today talks about this — don’t worry about the virus, it says, we can cure that. Personal finance / greed / insurmountable debt / expectation that governments are there to bail us out financially because we’re so freaking hopeless at looking after ourselves on the other hand…

Hi Dave,

Your arguments resonate well with this.

https://www.youtube.com/watch?v=rvskMHn0sqQ

Thanks!

DG

Hey thanks DG that’s a fantastic little video!

That little video doesn’t take into account climate change nor the negative impacts upon the natural world, ( habitat destruction, mass extinctions etc.). Perpetual growth in a finite system is impossible.

BTW, a cure for cancer is also, if not impossible, extremely unlikely because cancer is not one disease, it’s just a way of defining a condition whereby an uncontrolled division of cells is occurring, for all sorts of different reasons.

Hey Dave, just discovering your site from Canada 🙂 We reached FI in 2018 for our family of 3 and so many of these points are spot on! And that’s coming from a math and Econ major 😉 We wrote a similar post last week if you’re interested in reading about our take. Cheers and glad to have found another like minded FI blogger across the globe.

https://modernfimily.com/covid-19-the-wake-up-call-we-all-need/

Hey Court. Thanks for stopping by and appreciate you confirming the points 🙂

Big congrats on your retirement too!