Welcome to Part Two of my interview with Pete Wargent!

Here, Pete shares his views on the current state of the Australian economy, as well as the long term outlook, and what this means for long-term investors.

Because if you read the news, you’d probably think the world was about to end! And every single day it’s forecast (or implied) that Australia’s prosperity is about to come to a grinding halt. Fear sells. It’s as simple as that.

But there’s something missing in this space. Balance. A story which looks at the risks and probabilities, thinks through those scenarios and offers a practical and realistic view on Australia’s future. Sadly, that type of content is almost non-existent!

Enter, today’s post.

Look, there’s a lot of noise out there in the financial media. Some threats are real, many are nonsense. And most people are left not knowing what to do about it all – whether it actually matters or not.

So here’s my idea: this humble blog post will serve as a guiding light on your investment journey. And hopefully show you that while there’s risks (like always), there’s far more reasons to be optimistic about the future!

Now, if you read Pete’s blog, you’ll know his data collection and insights are fantastic. And given his knowledge spans economic history, real-time analysis of markets and the economy, as well as being an active and successful investor, he’s in a unique position to comment.

In fact, because of this and my point about the news being mostly rubbish, Pete’s daily blog is my go-to source to find out what’s happening with the economy.

It’s always practical, well-reasoned and full of common sense. That’s why I really want to dive in here and get Pete’s views on all the most important topics. Let’s go!

Pete Wargent: Pretty soft at present, largely thanks to the credit squeeze and Royal Commission, which has finally brought a housing market and construction downturn into play. Plus, an election year rarely inspires too much confidence.

Inflation has been under target for several years, and there’s a clear output gap. I guess the economy might grow by about 2% this year, which is well below its potential.

There’s now a significant residential construction downturn underway. So there may well be pressure on the Reserve Bank to cut interest rates to stimulate the rest of the economy.

Company profits have been huge, largely thanks to elevated commodity prices. But they’re probably going to ease a bit at some point for the resources giants.

The housing market downturn in Sydney is now into its third year, and some areas have been hit quite hard, especially out west and where apartments have been built in high volumes. The most supply-responsive and premium property markets often tend to get hit the hardest.

Banks are probably easing back a bit on the credit squeeze now that the Royal Commission has wound up. But there are still Labor’s proposed tax changes to come in 2020.

Pete Wargent: Demographically we are changing, and the cities have some ongoing infrastructure challenges. That’s due to a high level of immigration and population growth in our three major capital cities and south-east Queensland.

Integrating a high level of migration from Asia might prove to be challenging at some point, though Australia has managed it relatively well to date.

And population growth brings opportunities both in real estate and in terms of continually rising demand, driving future company profits.

Politically we have been quite moderate and stable, but that could change, and globally a shift to the left seems imminent.

For the economy, a major challenge at the moment is getting wages growth up again after a soft few years post mining-boom, because there’s a comparatively high level of household debt in Australia that needs to be serviced and repaid.

I think wages growth will pick up eventually. But it will probably take time as there’s plenty of slack in the labour force.

Pete Wargent: Lots of things!

We are resources rich, which tends to drive a high level of national income. In fact exports are tracking at record highs, which doesn’t get mentioned much in our esteemed media.

Commodity prices will always go through cycles, but the urbanisation of China and other parts of Asia will drive tremendous demand for our resources over the next couple of decades.

Australia is mostly safe, and stable, with a great lifestyle and climate. So we continue to be popular for migrants, and we can afford to be somewhat selective in terms of the migrant intake.

Australia is a hugely popular destination for international students from Asia, and especially from China. Many of these young graduates will go on to seek permanent residency through sundry visa types.

Down Under is also great for tourism. Which is how so many bright, young, and well-travelled people first get to experience Australia. Indeed, this includes my good self!

Australia has a favourable population pyramid, with immigration focused on the under 30s age cohort. So we are nothing at all like Japan, where young and independent women don’t always want to partner up and have children, and the shrinking population has become increasingly aged and ‘top heavy’.

And we are perfectly located to benefit from the huge and ongoing boom in Asia’s middle class.

Australia has lots going for it, despite what you might read of our challenges from day to day!

Pete Wargent: Yes, there’s no question that population growth increases headline growth. And for Australia it’s been a stronger population growth rate than elsewhere, at least 1.5% or higher.

Greater Melbourne has grown by about 600,000 persons in the past five years, and Greater Sydney not far off 500,000. These are enormous numbers when you stop to think about the implications of it.

Australia’s population policy is quite favourable in terms of the make-up of immigration. Generally speaking, we do attract more young people and more skilled migration than elsewhere.

There can be downward pressure on wages as a result of immigration, but only when both the economy and national income is soft. There was no such downward pressure on wages when the mining boom was firing, for example, despite rampant population growth around that time.

I expect population growth to continue over the long run. Even if there are backlashes from time to time.

Why? The productivity commission found that immigration lowers the average age, increases the participation rate, and increases the tax take. So, on that basis, government of all stripes will inevitably be incentivised to keep running strong immigration programmes, and this explains the ongoing popularity of the Big Australia concept.

The forecasts expect to see our population expand from 25 million to 40 million or above, over the decades ahead. So while there are a range of forecasts, they do typically expect to see a very large expansion in the population.

Again, this is likely to boost capital city land values, demand for some types of housing, and will be very good for final demand and company profits.

Pete Wargent: Japan was a genuine basket case with a land price bubble bursting, a deflationary economy, and then a falling population due to its ongoing horrible demographic trends.

Since the introduction of inflation targeting, most developed economy central banks will now do almost anything to avoid the same fate, including QE and any number of other unconventional policies.

I’d estimate there to be almost no chance of Australia going down that path, over any meaningful timeframe.

That said, I do think Australia will experience quite a property correction from 2017 onwards in the two most populous cities, possibly bottoming out some time in 2020 for Sydney and Melbourne.

Everyone likes to pretend they can predict these things with some level of accuracy. But guess what? They really can’t. You can only make the best-informed decisions you can with the information at hand.

Still, I doubt there will be a repeat of the global financial crisis playing out here. Our demographic and cultural trends are very different from Japan.

This is a detailed and complex subject. But Australia has so many tools at its disposal if the mess really hits the fan, in terms of monetary and fiscal firepower. QE (Quantitative Easing) is now in the toolkit, and our free-floating dollar has been a tremendously effective shock absorber.

Those Armageddon predictions will always be there, but personally I don’t believe them.

Pete Wargent: Mining is already a relatively small employer at just a couple of percent of the workforce. But it generates vast levels of national income and royalties, and that’s expected to continue.

It’s a very capital-intensive business, and that clears out a lot of exploration companies in each cycle, and plenty of junior producers for that matter. Commodity prices will peak and decline cyclically, and some commodities could become less favoured over time, such as Australia’s two main types of coal (presently imported in vast volumes by China).

But I think mining will remain a key sector for national income, even though most new jobs will be created in the services sector.

Pete Wargent: It depends how you define advantage: if you look at the changing demographics of the country, there are far fewer Brits, Europeans, and Kiwis coming over, and many more migrants from China, India, and other parts of Asia.

So we are, in essence, becoming a more Asian-influenced economy. That’s helping to bring in stacks of investment from China and is delivering some challenges too.

So for the economy it could be a huge boost, when you think of the vast scale of China and all its increasing wealth.

Disadvantages? Well, over time we will by and large have Asian-style capital cities, so it depends if you see that as a good or bad thing, I guess. It’s no dramas to me, I lived in Asia for years and I loved it. Easy for me to pontificate casually, I guess, as I live at Sunshine Beach in the Noosa Shire.

But the quarter-acre block with barbecues and cricket in the backyard won’t be the norm in Sydney and Melbourne for too much longer. And culturally, it’ll just be different.

But any such congestion and indigestion challenges will be comfortably outweighed by the advantages, at least economically speaking. Our proximity to Asia will be a boost for our economy and for our industries: tourism, agriculture, education, resources, and so on.

Pete Wargent: Again a much longer answer is possible. The BIS (Bank for International Settlements) found that the number one early warning indicator for a recession leading to a banking crisis is high debt serviceability ratios (DSR), rather than the absolute level of debt itself.

So, although household debt levels are high, structurally lower interest rates mean that a higher level of debt can comfortably be serviced at the present time.

Yes, I appreciate that over the very long term we could see inflation take off and rising interest rates. But I just can’t see that as an issue facing us over the next decade or two. Maybe that will change, but at the moment most developed countries seem to be more at risk of grappling with deflation.

Australia’s DSR was flashing red in 2007, but it is much lower now. Interest payable to income ratios have fallen by more than a third, and they are still falling further.

So there’s plenty of debt, but most households are servicing it easily. And Australia also has a unique approach to mortgage buffers, which are at unprecedented levels.

Borrowers in most countries don’t use offset accounts like Aussies do. So here, it has made perfect sense for investors to use interest-only loans and combine their savings or transaction account with an offset facility. It’s been a tremendously tax-efficient approach, and it reduces the interest payable on the loan.

For sensible investors it’s been the blindingly obvious thing to do. But regulators have seen it differently, and perhaps understandably they now want to see more Aussies paying down their debt. That’s fine, but it will be a drag on consumption, and will slow the economy down somewhat.

Debt to income levels have been falling since the middle of 2018, and I think that we’ll see a steady deflation over the next year or two as well.

(Pete wrote an excellent article on this topic here)

Pete Wargent: The RBA’s 90% confidence interval suggests annual GDP growth will remain firmly in positive territory. So less than 10 per cent, on that basis.

But I try never to take anything for granted, and within reason anything can happen in the short term.

Given the monetary and fiscal firepower at Australia’s disposal and the tendency for our dollar to respond quickly to risk, I reckon we’d bounce back quite quickly if it did happen.

Pete Wargent: No chance of them standing back, is my belief!

The central bank mandate is for them to target full employment, as well as the inflation target.

Interest rates would therefore likely get cut towards the zero lower bound.

The Aussie dollar would likely go to 60 cents US, or perhaps even much lower at 40 to 50 cents US, and that can act as important stabiliser for our economy. In fact, it already has been since the dollar was floated in 1983.

During the mining boom, the Aussie was buying something like 110 US cents at one stage. Today, it’s nearer 70 cents, so that’s the floating currency doing precisely what it’s supposed to do.

The Reserve Bank of Australia recently discussed the possibility of quantitative easing (QE) being introduced into its toolkit. ‘Go hard, go fast, and don’t die wondering’ in their own words, or something like that. I’d have to go back and check the exact quote, but it was Debelle that said it late last year.

And there might be buying of mortgage backed securities (RMBS) to add liquidity and support the housing market, while positively influencing the price of credit.

Massive fiscal stimulus could be deployed, including nation-building programmes of various types.

There are so many stabilisers that can and would kick in. And that’s why, while a downturn might be painful, I believe it would be relatively short lived.

Curve balls? Well, a dramatic drop in the currency could import some inflation. But presumably this would be looked through, if it was deemed to be a temporary issue.

Pete Wargent: Totally.

Net debt is projected to head towards zero over the forward estimates. And if needed there is ample potential for running big deficits and the government borrowing to invest in infrastructure and building programs, or even public sector housing construction.

After all, why have a AAA-rating if you’re never going to use it?

Compared to the US, or Japan, or Britain, or many European countries, we have a very low level of government debt as a share of our GDP. And that’s a powerful tool to have at our disposal.

Pete Wargent: I think it was Jim Rohn who said summer seasons follow winter seasons, and Democrat governments follow Republican governments.

Same here in Australia: we will continue to shift from Liberal to ALP, and back to Liberal and then back to Labor again. There’s a chance that we’ll shift to the left politically over the decade ahead. But Australia’s politics tends to be quite centrist overall.

I believe whichever political party is in power, it’s unlikely to matter all that much to markets and the economy over the long term.

Furthermore, it’s something as an investor that you have no control over. So my advice is, don’t spend too much time worrying about it.

Other drivers are more important. Most of the what governments do these days is tinkering around the edges, rather than wholesale reform.

Pete Wargent: Most of the western and developed world has become considerably wealthier, and Australia has been a bit luckier than most for the past 30 years.

Resources and demographics have helped a lot. And I believe that over the long run, stock market returns have been helped by a number of monopoly type businesses, or at least oligopolies.

We aren’t unique in that.

But we do have a fair number of big companies that have been around for a very long time, especially when you compare this with other countries.

The purple bars show a lot of our companies are older than those in, say, the US, or Japan.

Pete Wargent: The stabilisers!

Of course there will be slowdowns and recessions. But there will be factors that help us to rebalance too. So the long run outcomes are likely to be very good.

Our population pyramid is also relatively favourable compared to many developed countries. So we don’t have the same population ageing issue that some other countries have. At least, we don’t while we keep bringing in young immigrants to work and pay tax.

Of course, they will age one day, so some people describe this as a form of Ponzi scheme. Whatever, it is what it is!

The important point is that the outlook for the dependency ratio in Australia is comparatively favourable compared to many developed countries. So this works in favour of our economy.

Pete Wargent: I believe it to be true we haven’t been at the cutting edge, but we are evolving.

Think how much has changed in 20 years – it’s a huge technological shift, even if it doesn’t feel much like it in real time.

Pete Wargent: Definitely!

Technology makes us wealthier.

Some low-skilled jobs may become obsolete. But the economy has generally created new jobs to replace the old and I expect that will continue. And so do people more intelligent than me, importantly!

Pete Wargent: It’s hard to predict the future, but broadly yes. The services and tech sectors are growing and I bet that will continue.

Manufacturing has been in structural decline for years, and mining actually employs comparatively few people, especially once the mines are constructed.

About 250,000 or so, which is nothing when you compare to, say, healthcare and social assistance, where employment numbers have exploded higher over the decades.

There are stacks of industries that could increasingly thrive in the decades ahead.

For example, think of green industries, and renewable energies or energy sources. Healthcare research, new pharmaceuticals, and start-up biotech firms. Genetics, and genetically modified produce. Electric vehicles, drones, space travel…or virtual reality.

There are so many possibilities, that it’s impossible to predict.

This is an argument in favour of an ‘all-caps’ approach to investing.

Furthermore, the early adopters aren’t always the most successful businesses.

After all, aviation has been an amazing industry for the advancement of the world. But you wouldn’t want to have sunk all your money into Wright Brothers Inc. (or Ansett for that matter).

It’s a strong argument for a decent level of diversification, and owning some index funds, ETFs, or LICs (I’m not going to recommend any products here, so definitely DYOR).

And there will be surprises.

If you read Nassim Taleb’s work, such as The Black Swan, we have a tendency to believe that history moves along in a smoothly predictable and linear fashion.

But in reality, the world darts around in random and unpredictable leaps that we simply can’t see coming in real time.

Did Bill Gates predict how the internet would explode into our lives in The Road Ahead? Not really. Although he later grasped the importance of it.

These things only ever seem blindingly obvious in hindsight.

So, there will be surprises. And while it might seem boring, you could do a lot worse than owning all the major companies in your country…and continuing to invest in them on an ongoing basis.

Yes, there’s an argument for buying more when they are cheap, and less when they’re expensive. So if you have the skills to do that, go for it.

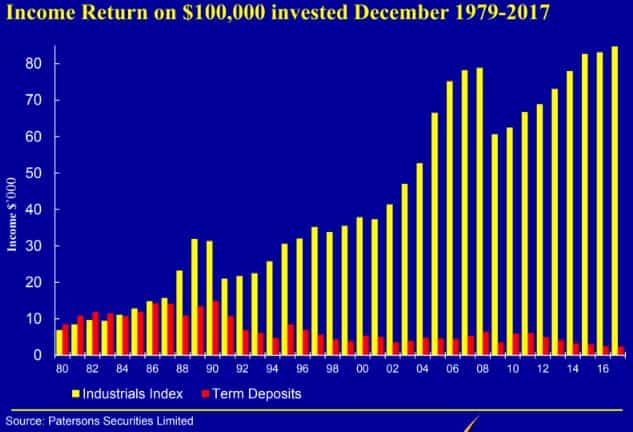

I’ll throw in a few charts below on the long run measures of stock markets, so you can get a feel for some of these concepts if you aren’t familiar.

Pete Wargent: Yes. And hopefully central banks and governments have become a little bit wiser about managing the business and economic cycle, even if they can never smooth it completely.

The Reserve Bank’s Luci Ellis has done some great work on economic rationalism. I especially enjoyed the speech entitled Where is the Growth Going to Come From?

Well worth a read!

Pete Wargent: I’m not sure about that.

Perhaps the miners will lose some of their dominance in time.

One of the challenges is that the banks have become ‘too big to fail’, and a liquidity facility was even put in place for them to draw on to prevent failure.

The paradox of that is the major banks are now only incentivised to become even bigger, because then they are even less likely to be allowed to fail.

The only thing that can stop that is government intervention and more regulation, which I guess we may well see in time.

Reading The Myth of Capitalism by Jon Tepper on monopolies raised some interesting points for me, including on the massive dominance of some US tech firms.

So to some extent it might depend on intervention or regulatory measures or pushback to prevent monopolies from becoming too dominant in the tech age.

Pete Wargent: Some companies will fall by the wayside, but in aggregate…yes, absolutely.

Does anyone seriously believe this will change?

I have copied some figures below going back to 1900, if that’s a long enough timespan for consideration. And note the log scale!

If businesses aren’t generating returns on equity well above and beyond inflation then they will drop out of existence and will be replaced by those that are.

It’s actually amazing how few people understand this about stock markets. If only people focused more on the growth in profits over time!

Don’t forget that in Australia a big chunk of your returns in the future might well come from the dividend distributions rather than growth, as our tax system has moved us in that general direction.

In plain English, when companies make profits, they can pay out a share of those profits to shareholders (you!). At the moment, dividends are treated quite favourably for tax purposes, so these days Australian companies tend to pay out relatively high dividends.

Looking around the world by country, Japan has been the only basket case for nominal stock market returns. Though don’t forget returns should be measured in real terms (i.e. after accounting for inflation, or the rising cost of living).

By the way, the below chart shows how dividends have accounted for a greater share of returns since the 1990s in Australia. Far more so than in other countries, where companies might be incentivised to reinvest in growing their business.

As for the sectors…look, I have my views on the likely best performers.

I’ll leave it to the RBA to show that it probably won’t matter too much over the long run if you just own a bit of everything, even if I believe that the less capital-intensive sectors might be the best bet.

What this chart shows is that resources became a huge weighting of Australia’s stock market index around the 1970s, but much less so today.

So while there could be another commodities super-boom, personally I wouldn’t bank on Australia being the prime beneficiary of it.

The below chart shows the same thing in a clearer way.

Finally, as for whether the market is cheap or expensive: at the moment, neither is particularly the case. But these things have a way of balancing themselves out over time.

US stock markets have been fundamentally over-valued, especially if you are a believer in cyclically-adjusted PE ratios.

US stock markets have been through an enormous boom since the financial crisis, so a correction would not be a shock. And if that does happen, then Australia could follow.

But people have been saying that for several years. So who really knows? Think long term is my view.

Pete Wargent: Not really. I’m an accumulator, anyway, so I never pay any CGT.

Franking credit refunds are probably not a major issue for most investors, but slightly annoying for some. However, they will adapt, as we all must!

If the negative gearing changes are pushed through this will encourage a less speculative approach to property. But things will balance out again in time, as they always do.

In short, yields will have to go at least 1 per cent higher than they were. And perhaps more if interest rates rise again, as one day they surely will.

Pete Wargent: Overall, I think bright. And while automation will bring challenges, as a nation technology will make us significantly wealthier.

It might become cheaper to build housing in real terms. But as the population goes from 25 million to 50 million, I expect capital city land prices will be very high in the future, especially in the inner suburbs.

The outlook for Australian businesses is good: banks, insurance, healthcare, pharmaceuticals, professional services, tech, and much more.

Pete Wargent: I think that’s about it. Just remember the awesome power of compound growth!

People overestimate what they can achieve in a year or three, but massively underestimate what they can achieve in 20 years, let alone 30 or 40 years.

Well, I hope you enjoyed that interview as much as I did! I sincerely thank Pete for his time and effort in answering these questions.

Don’t forget to read Pete’s daily blog, and you can get in touch through his personal website – petewargent.com – and his coaching website – gonextlevelwealth.com.au

By now it should be crystal clear – you can safely ignore the endlessly gloomy news headlines! You know better than that now!

My key takeaway is that we have a long list of very good reasons to be optimistic about investing and the long term future of Australia.

Not because nothing will go wrong. It will. But despite the inevitable bump in the road, we’ll continue to move ahead, adapt and prosper. As a country, and as individuals.

Of course, to really benefit from this growth and capture our own slice of this growing economic pie, we need to invest, regularly, in shares and/or property.

Benefit from rising rents and land values, by owning quality income-producing real estate to hold for the long term. Or, perhaps more directly, by owning a broad group of businesses through an index fund or diversified LICs, you’ll own a share in all the future profits and dividends of those businesses.

Whatever you do, keep investing!

Did you enjoy this interview? Let me know your thoughts in the comments…

Why deliberate spending is my favourite money management style. What it really means and how you can use it as your situation and priorities change over time.

My thoughts on ‘The Great Taking’. An idea that the masses will lose untold amounts of wealth in the next financial crash, due to a deliberate plan by mysterious figures.

Get my latest content and thoughts straight to your inbox.

A fresh dose of financial motivation to power your journey.

Really great in-depth interview. Thanks for the write-up Dave, and thank-you Pete for the insight!

Cheers Scott, thanks for reading!

Great interview mate !

Thanks Dave and Pete.

Good article, very interesting charts. Not sure about our immigration policy being akin to a ponzi scheme either. Doesn’t seem like the full picture. We’d need to ignore the fact that immigrants are likely to have kids who will be at least working age when they retire. And that they will build 30+ years of super to support themself in retirement age, still supporting the health industry, buying retirement homes, etc.

Thanks for the comment Mateo – all great points.

Haha I think ‘ponzi scheme’ is a pretty cynical way to view it, but I can see why they’d say that. It’s likely the same people that cheer on the demise of the economy!

Epic interview – thank you both for your effort!

Glad you liked it Mark 🙂

So many things to take away from the interview. Thank you both!

That’s great to hear, thank you for reading!

Great interview, really enjoying your blog Dave, thanks so much.

Question for you as a totally new investor : we recently saw a financial advisor, mainly due to my husband and I having differing views. He thinks we should just pay the mortage off much faster, I think we should invest. Anyway, financial guy recommended a split between the 2, but due to me wanting to put money into investing a minimum of monthly, suggested vanguard instead of LICs , as he said it would be too expensive to continuely put money into LICs (I am wanting to take advantage of dollar cost averaging). Do you have any insights into this? I know selfwealth offers $9.5 trades.. Thank you for your patience with this very novice question!

Thanks for the feedback KEK 🙂

I agree with the advisor that it’s probably best to pay off debt and invest since it will keep both of you happy. But in terms of costs, it costs no more to buy LICs than it does to buy a Vanguard fund. I’m not saying to choose LICs, just clearing that up. A Vanguard fund like VAS (for example) is a high quality and low cost choice.

I hope he’s not suggesting you open a managed fund account with them as the ongoing fees for those are quite high – far easier to buy the ETF version of the fund with much lower ongoing fees. Sometimes advisors will also charge fees on top of this for ‘managing’ your money, which I think is unnecessary for the vast majority of people since this stuff is all very simple once you get started. Buying Vanguard funds or LICs monthly is a very simple and low cost and simple way to invest, with no advisor needed. If you do keep using him, make sure you’re only paying him for his time, not an ongoing yearly or monthly fee! Just a few thoughts, hope that helps.

Hi Dave

Thanks to you and Pete for providing such quality information. Like yourself, I have been following Pete’s blog since 2012 and he is the go-to guy for providing clear, commonsense, dispassionate analysis on two vital asset classes – shares and property.

Part 2 of this interview was especially helpful for me because I am quite uncertain where to invest over the coming years. I was keeping a lot of money in cash to avoid share market fluctuations while saving for a house deposit, but it doesn’t make sense to do this considering the gains that will be foregone.

Those charts going back to 1900 illustrate that point vividly.

Fantastic interview, thanks for sharing with the community.

Cheers

Dave

Great to hear you enjoyed it David! And perhaps it helped with your concerns about the sharemarket.

Honestly, if looking to use savings to buy a house in the next 5 years or so, I wouldn’t put that money into shares. There’s a real chance you end up with negative returns simply out of bad luck, even though the long term returns are attractive. The market is very unpredictable in the short term so if there’s a plan for the money then a high interest savings account is the best place for it in my view.

Thanks for reading 🙂

Thanks for the quick reply Dave!

I think he probably was suggesting opening a managed fund account, thats the only way I can see his comments make sense. Will heed your warning re higher fees.

Am I correct in thinking you just use self wealth and pay the flat fee? I was thinking of investing monthly rather than weekly to decrease paying the $10 weekly- do you think this would affect the dollar cost significantly?

No fees from him, luckily 🙂

Thanks again!

We may be getting our wires crossed on fees. There are two fees you’re up against. One is brokerage costs, which are about $10 per purchase with Selfwealth. I wouldn’t buy more frequently than monthly. You can still benefit from dollar cost averaging by purchasing every few months, doesn’t have to be weekly or anything crazy like that. Monthly is my favourite as it helps build momentum and stay motivated while not costing much.

The second set of fees are the fees of the fund you’re investing in. For a Vanguard Australian shares managed fund, the fees start at 0.75% per annum, and comes down the more you have invested. Advantage is you can Bpay money straight to Vanguard and don’t need a brokerage account. To buy the Vanguard Australian shares ETF (VAS) through your brokerage account, the fund fees are a flat 0.14% per annum. Huge difference in fees for the same investment.

Overall I think the lowest cost simplest option is purchasing the ETF version of the fund each month. But some people prefer having the managed fund for the Bpay option and not needing a brokerage account and prepared to pay more for that. Up to you what you prefer. Hope that all makes sense!

Yes, totally, thanks very much. I was talking about the brokerage fees. Thanks!

Sorry Dave, 1 last question.

Can you buy the ETFs through self weath with a credit card (thinking of points). I have searched +++ but cant find the answer- just that you can pay for the trades ($9.5) with card. Am I right in thinking you have to transfer funds into the ANZ bank account they set up for and then use that cash, and not a CC?

Thanks !

Yes you have to transfer the funds to Selfwealth to purchase as far as I know, so I have no clue whether that’s possible to manoeuvre with a credit card…

Timely interview as Pete is the latest guest on the ‘Australian Investors’ Podcast. Also great that I can read the interview on here as his accent is difficult for me to comprehend!

Thanks Aleks – yes I just saw that interview also, Pete’s been busy!

It’s nice to see a balanced perspective, especially against the negative backdrop we’re hearing from the media these days.

The take home message for me is that in the long run, everything balances itself out. Recessions and economic growth are part of the journey all investors have to take, and the best thing we all can do is to have faith in what we’re doing and to stay the course.

Thanks very much for the interview with Pete, Dave. I really appreciate the work you put into it. Great questions and great insights.

Thanks very much. The media is insufferable and have no interest in pesky facts, balance or putting things in context.

Excellent takeaway Ms FireMum!

Great article Dave! Really does put things into perspective with these insights. For me, I’m a happy LIC accumulator and will continue to accumulate and watch the projected dividend yield grow and grow regardless of the noise outside!

Cheers! Glad you found it useful 🙂

Thanks for doing the interview Dave. Very informative and puts a good perspective on Australia’s future. Appreciate all the work you put into this blog.