Recent events have prompted me to think more deeply about our investments, our personal situation, and how I want to invest going forward.

Most of you will know, we’re steadily transitioning from property to shares over time. The strategy is a bit like this.

This lets us build our share portfolio in a more methodical way. Especially while I’m still learning, experiencing and thinking about all this stuff as time goes on.

We get to adjust things as we go, which makes this process more relaxed and less stressful. Compared to if we had decided to sell all our properties on day 1 of early retirement, and then need to invest all that cash immediately! Stressful much?

So, with all that said, let’s get into how I’m currently thinking about dividends, diversification, and our personal situation.

Unless you’ve been living under a rock, you’ll be aware of the huge disruption to almost every person and company on earth, caused by the economic shutdowns.

This means company earnings will take a big hit in the short term. And so will dividend payments. In fact, a number of companies have already ‘deferred’ dividends until a later date – which, let’s be honest, is really the same as paying zero.

And it does make sense. Companies can and should do what is necessary to stay afloat and come out the other side of this in a sound financial position. Dividends are a nice source of income for investors. But there’s no point paying out cash to shareholders if you may need it to survive!

For whatever reason, I started thinking of a bizarre parallel universe…

In this world, companies decided to pay absolutely no dividends for the foreseeable future. Mrs SMA and I also earn zero income, and have no ability to do so. It’s just us and our investments.

So I asked myself, “would I be okay trimming our shares to create income?” The answer came back, “well, yeah, I guess so.”

After all, in this universe, the companies held on to the cash – it didn’t disappear. Obviously, the share price would still be dictated by the market, but all else equal, their market value would be a bit higher than if they’d paid out the dividend.

So, with us having no personal income and no dividend income, then sure – I could sell a few shares to create some cash. This strange newfound mental flexibility had me thinking that I should probably be okay doing that during normal times too.

Until this point, readers will know I’d been strongly focused on dividends from Aussie shares, not wanting to sell shares to create income, whether by choice or necessity. But this weird daydream seemed to point out my stubbornness and lack of flexibility.

Oddly enough, I actually pride myself on being an adaptable person. For example, whatever happens during our early retirement, I have zero fear of us running out of money. We will make it work, whatever the circumstances.

So, essentially, my thoughts on our strategy going forward have changed. I’ll always have a soft spot for dividends, but I feel like more global exposure than we currently have (0-20%) is a good idea.

By the way, I created a spreadsheet to keep a running estimate of my dividend income and wealth breakdown. I’ve used it for years as a way to help plan my finances and watch my progress over the years. You can get it below.

Basically, we’ll move towards a more diversified portfolio by adding global shares to our personal portfolio.

Currently, we have our super setup as 100% international shares, which is 15-20% of our net worth, while our personal share portfolio is 100% Aussie shares. For more info, see our latest portfolio update.

We haven’t done anything yet. But in the coming months, we’ll add an international index fund – VGS (Vanguard International Shares) – to our portfolio, and casually add to it over time.

Where will we end up with our portfolio? Well, currently, I feel as though 25-50% international shares would suit us and our situation.

Over the very long term, 50% Aussie / 50% Global seems like the simplest choice, and a reasonably conservative one. So that’s the direction we’ll head.

Irrelevant side note: I’ve long thought that if I won lotto, that’s what I’d do with the cash. But I don’t play, so there goes that idea!

In case you think this is a wild change of heart, I’ve mentioned on this blog multiple times that we’d later add international shares to our portfolio.

That date has been pulled forward due to my thoughts on the subject changing, and the outlook for our personal situation evolving. We’re enjoying our individual part-time work more than expected, and earning reasonable income.

This also means our portfolio doesn’t need to be as dividend-heavy. So, after mulling it over for a while, here’s the thinking behind all this…

This should be obvious, but by owning international shares, we’re exposed to a much larger basket of companies. And those companies are operating in other countries and economies, each with their own strengths.

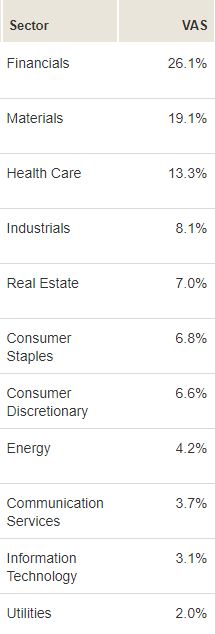

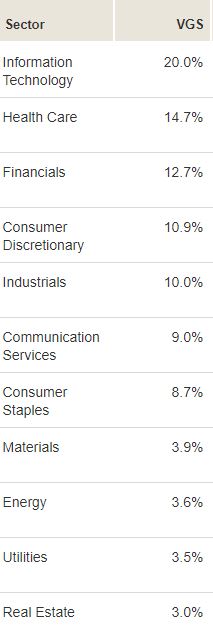

More importantly, it offers a unique and complimentary spread of sectors and businesses to what we have here in Australia. We can see this from the sector breakdowns for the ASX 300 (VAS) compared to Developed Markets outside Australia (VGS).

As you can see, we have more resources, real estate, and financials. And other developed markets have more technology, communication and consumer stocks. Complimentary, no?

Mash ’em together, and then dividends and profits are coming from a bigger, more diverse base. Just out of interest, here’s what they look like combined….

Financials: 19.4%

Health Care: 14.0%

Info. Tech: 11.6%

Materials: 11.5%

Industrials: 9.1%

Cons. Discretionary: 8.8%

Cons. Staples: 7.8%

Real Estate: 5.0%

Energy: 3.9%

Utilities: 2.8%

Recent events have highlighted risks (in all areas of life) that seemed almost unimaginable six months ago.

As mentioned, the pandemic has caused many companies to severely reduce or halt dividends entirely while this thing plays out. Not ideal for investors who are reliant on their dividend income, especially some older Aussies who have large holdings in bank shares!

Some commercial tenants are refusing to pay rent, or demanding serious rent reductions. This affects the ability of REITs to pay their distributions. These two sectors provide a decent portion of the income paid out by ASX companies. Other sectors are obviously being affected too.

Owning global shares alongside would reduce the drop in dividends across a portfolio, given the different sectors.

The old fashioned LICs will attempt to smooth out the fall in dividends for shareholders, by using small amounts of cash and excess franking credits. But the underlying dividend cuts still hurt their ability to do this for very long.

Some folks increase diversification by adding small/mid size companies to an Aussie portfolio, given our market is dominated by large companies. I’ve done this myself.

But adding international shares tends to achieve much greater diversification, for very little cost. That’s when it comes back to our desire or bias towards receiving higher dividends or not. More on this in a minute.

Now, I’m not sure if this is a rational reason, but who cares. There are a number of companies which impress me and that I’d like to own more of.

The obvious examples are US tech giants like Google, Amazon and the like. Of course, I’m impressed at their size, which at $1 trillion each seems ridiculous in itself!

But what amazes me most, is how incredibly invasive they’ve been in our lives. To the point where most of us couldn’t think about life without their Apple iPhone, or having the ability to ‘google’ something.

That’s what’s fascinating – our sheer reliance on them. We notice their tentacles surrounding us, but we embrace it and pull them closer.

So yes, I’d like to own a bigger slice of companies like that. And it’s worth saying that some great companies pay no dividends.

I like the ease and simplicity of dividends as much as the next guy, but I don’t believe it makes much sense to exclude a giant like Amazon from a portfolio, just because it doesn’t send a sliver of cash to shareholders each year.

You could argue it was a speculate investment in its early days. But that argument is now out the window as it becomes a modern day version of Standard Oil.

No company lasts forever though. So at some point, today’s giants will be overtaken by other enterprises. In this case, I’ll end up owning those too.

There’s a great article here – The Rise and the Fall – explaining the inevitable rise and fall of businesses over time. It’s exciting and sad at the same time.

By adding global shares to our portfolio, there’s also less chance of a poor long term outcome. I’m not talking about a few years of volatility. Here, I’m talking about decades of economic and corporate performance.

There’s always a chance Australia doesn’t do as well as the rest of the world. Mind you, it could also do better. But by diversifying, this averages out, helping to insure against a poor long term outcome.

A combo of global and Aussie shares seems high risk in theory, due to the volatility of markets. But if we look forward 50 years, the chance of this mix delivering poor returns, seems very low.

Indeed, if that does happen, we’ll probably have bigger problems on our hands!

Any changes to tax policy and franking credits would likely have an affect on what companies do with their excess cash. This risk to dividends has had plenty of air time in the last two years.

Tax benefits were not my main motivation for investing in Aussie shares. But changing the current system would make Aussie shares less desirable to some extent.

It does seem fair that there is a limit placed on franking refunds at some point. While it’s not a big deal to remove a tax incentive, it could have some unintended consequences.

If dividends are no longer tax effective, companies may decide to dramatically lower dividend payments and use cash for other purposes. Whether for research and development, growth plans, or share buybacks (which are like dividends).

Some of these efforts will bear fruit, others will not. You’d hope companies would use the cash wisely if this did occur. But it could create a problem for income focused investors.

If the franking system is scrapped altogether for some reason, the high yields of Australian shares could become a thing of the past.

We could move to a US style system, where companies pay out around 40-50% of earnings, versus 70-80% here. The remaining cash tends to get used for buybacks (which boost earnings per-share, and as a result, share prices) and other things.

The point is, we could end up with a dividend yield of 2-3% like some overseas markets. That would mean much more savings are needed to retire on dividend income alone.

Or… one has to be open to selling a few shares to create more income. While less convenient, the above system isn’t the end of the world. Some of the returns would simply move across from the income column, to the growth column.

Here’s roughly how it works: Instead of paying a 4% dividend, a company could pay 2% in dividends and buy back 2% of its shares. This shrinks the amount of shares in the company, which increases the stake of remaining shareholders by 2%.

As mentioned, each person now owns 2% more than before, and earnings per-share increases. Of course, if you wanted a 4% dividend, you could then sell 2% of your holding, and you’re back to square one.

Anyway, some people think franking credit changes in Australia are inevitable at some point. It’s certainly a risk to be aware of. Which brings us to the next point…

Readers will have heard me say that being an adaptable and flexible person is important, because no early retirement plan is bulletproof. Well, this is me eating my own cooking!

I don’t want to be so religious in my approach that I ignore changes or other ways of doing things. So, rather than be reliant on dividends alone, I’ve decided to be more flexible and be willing to trim our holdings to create income if needed.

It’s true, I would prefer to ignore the market and just receive cash dividends, but it makes sense to leave that door open. Having said that, I’m confident my love of receiving income from investments will not go away.

When we have an economic downturn, market crash, or, say, a global pandemic, the Australian dollar tends to fall. When that happens, global shares are worth more in Aussie dollars.

Not only that, but global dividends are also worth more when converted back into Aussie dollars.

In practice, if we’re experiencing a global recession, a lower dollar means global shares and dividends would hold up better as a result. That’s a nice bonus for a portfolio if it occurs, and perhaps a bit of comfort when the shit hits the fan.

Holding both local and developed markets gives you more chances to buy what’s on sale. These markets will both take turns at struggling, and out-performing. Plus, the currency movements mentioned above mean they will often move differently to each other.

When one is up heaps, the other might be up a little. When one is down a lot, the other may only be down a little.

In practice, that’s an opportunity to buy what is cheaper, what has under-performed recently. Doing this over time is another form of dollar-cost averaging and a form of value investing with zero effort.

Obviously, the reverse is also true. If you’re living off your portfolio, you could trim the one which has performed better recently, while also topping-up whatever is lagging.

Adding a global index to our portfolio arguably makes the portfolio stronger and lower risk. In the sense that it’s able to withstand more things going wrong than a one-country portfolio. The increased likelihood of a solid long term outcome is what I care about most.

Granted, this combo will still be volatile and get hammered when markets head south. But the long term result should be better than many other options. And it’s one I feel confident about.

Investing this way should lead to a stronger financial position than we’d otherwise have. And building financial strength is kind of my message around here, so maybe I should take it more seriously! 😉

As we’re now 3 years into ‘retirement’ we are able to get a good handle on what we want life to be like going forward.

In my experience, for the first year or two, you’re still getting used to your new life and creating a lifestyle that is enjoyable and satisfying.

Anyway, the realisation is that we’re both likely to earn some sort of income for the foreseeable future. Mrs SMA plans to keep working part-time, and I’m happy doing my own thing with this blog which also produces some income.

So while it’s nice, we don’t really need the higher income from Aussie shares as we anticipated before. Because of this, even with a lower yielding portfolio, we may not even have to sell shares at all.

Plus, as our allocation to shares increases, it feels safer to have a larger spread of companies, with less of our savings invested in each business.

For example, CSL is a great company. But do I really want to end up with close to 10% of our net worth in one company? Not really.

I still think of myself mostly a ‘dividend investor’. Just with some added flexibility.

To me, companies and the sharemarket are a handy source of cashflow. And I’d prefer most of that came from dividends.

It’s a simpler and more hands-off way of generating income to live on. But if it comes to it, I will trim our shares for income if needed.

The lower income from global shares is made up for with higher earnings growth, partly due to share buybacks.

But even then, a 50% Aussie/50% Global portfolio would still deliver close to 3.5% per year in distributions, plus franking credits. Not bad.

Also, I still think the future for Australia is bright, as highlighted well by Pete Wargent in our interview here. But we can never be 100% certain, so I’m hedging my bets.

Some may assume I’m panicked by recent events. But I don’t think that’s it. Large market falls and dividend cuts are something I’ve written about several times on this blog, and are certain to occur over any long period.

This isn’t about that. It has really come from an ongoing process of re-thinking diversification, what makes sense for our situation, and then somehow finding a loophole in my own flexibility (or stubbornness!).

By the way, nobody should be reading this and assume they should change the way they’re investing. We have to do what feels right for us, individually. We each have different circumstances, are wired differently, and have other factors to weigh up.

The FIRE crowd knows this all too well, but I’ll say it anyway. Whatever it is, we should do something because it makes sense to us after thinking about it carefully, not because other people are doing it.

Irrelevant side note #2: I’ve noticed that even long term investors tend to continually re-evaluate their portfolio, or even their strategy, as time goes on. It seems to be the natural order of things.

The one sentence summary? I’m tweaking our strategy and adding global shares sooner than planned, since my thinking and our circumstances have both changed a bit.

So there you go. A combination of regular daydreaming, newfound mental flexibility and other realisations are to blame for this long-winded post!

But hopefully you found it interesting! And, selfishly, writing helps clarify my thoughts.

We’ll soon begin a slow and steady path towards more diversification. This should result in a stronger long term portfolio, with more certainty of a solid outcome.

We can then enjoy owning a larger spread of businesses, from more diverse industries and multiple economies, and of course, the still-healthy dividends that flow from that…

WANT PRACTICAL NO BS FINANCE CONTENT EVERY WEEK?

Join thousands of readers and subscribe to the Strong Money Newsletter below.

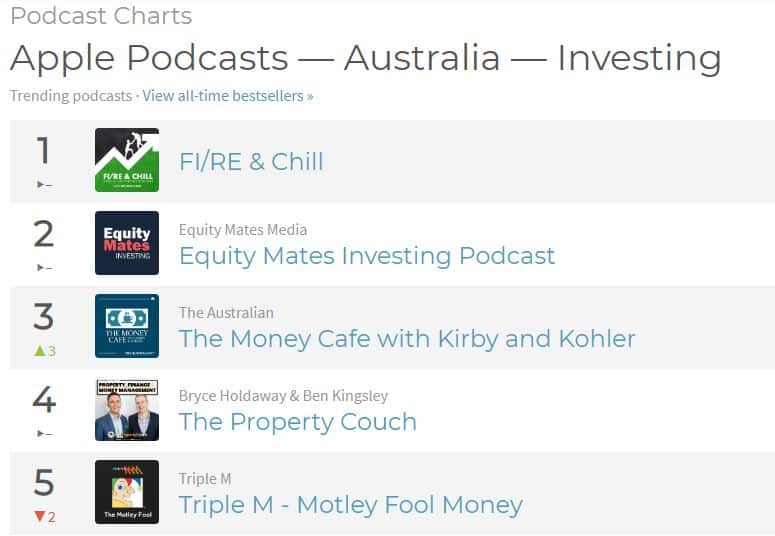

p.s. Pat and I are overjoyed at the positive response we’ve received for the podcast so far. Because of your support, we somehow managed to hit #1 in the Apple Podcast charts for both ‘Investing’ and ‘Business’ categories.

Big thanks to everyone for listening! How cool is it that a dedicated FIRE podcast gets top spot?!

Learn how our EV performed on our recent roadtrip and holiday in Southwest WA. What I learned from the experience, plus lots of pictures, recommended places to eat, and more 😉

The numbers behind our recent solar installation and how much we’ll save. A breakdown of solar FAQ, whether it’s a good investment and what to watch out for.

Get my latest content and thoughts straight to your inbox.

A fresh dose of financial motivation to power your journey.

What are your thoughts on International LICS for diversification like WGB, TGG and PAI?

Hi Trent. Haven’t looked at those, but I’m not keen on international LICs generally. They tend to be very high fee and/or high turnover, meaning tax inefficient and/or short term focused. Then you have to hope the manager is going to perform, which is hard given the high fees. Choosing an index for me made more sense because it’s cheap, simple and I don’t have to think about it.

That’s a well thought through position, SMA. Welcome to (more) global diversification club! 🙂

Many of the same factors are behind my VGS holdings, as well as the other international shares exposure in Vanguard funds, as part of the FIRE portfolio. That has provided a buffer through the events of March, in fact, much more than I had anticipated. Part of the challenge will be transitioning to your desired level of holdings over a reasonable time period? The other part is reaching that final decision about the ultimate level. I’ve also been attracted to the 50/50 split for simplicity, but for the moment the target is 60/40 in favour of Australian shares (which themselves will have some global equity correlation).

And congratulations on the podcast hit!

Thanks for the encouragement on both fronts! 🙂

What caused you to be surprised? Was it that the US didn’t fall as hard or the dollar cushioning the fall?

Haha yeah it could be tricky. But it’s not something that worries me, so it will just be a steady increase in diversification over time as opposed to something I want to hit immediately. Will still keep buying Aussie shares at the same time. Can’t be certain of where I’ll settle, 50/50 appeals, but maybe when I get to 70/30 or 60/40 I’ll feel more than comfortable and just leave it – who knows.

Considering Australia’s nominal GDP accounts for less than 2% of the global economy it’s definitely wise in my opinion to branch outside of one single country (home country bias). Personally, we invest in VTSAX in our US accounts (US index tracking over 3,000 US stocks) and VUN and VDU in our Canadian accounts (US and ex-US index funds). We live in Canada and do not hold any individual Canadian funds or Canadian index funds even though there are favourable tax rules in place if you do. Way too heavy in natural resources for my liking and our economy is also less than 2% of the world economy. Clearly I’m team index vs dividends as like you mention dividends can get cut anytime and are no where near diversified enough. We’re aiming to get to a sub 3% withdrawal rate (should be there within a year for our hopeful family of 4 at the ages of 35 and 33) so we can essentially live off the dividends of highly diversified index funds. We’re very conservative with our withdrawal approach but it lets me sleep very well at night.

Hey Court, thanks for sharing your approach. Sounds pretty good, and congrats on getting such a solid portfolio as a young family to enable living off less than 3%!

Whilst i’m not yet at Fire – what I’m actually going to do FIOR (Optional Retirement) the dividend situation doesn’t yet concern me for income – by the time i’m at FIOR (5/6 years time) the world could be a different place again.

I honestly think that strategies do have to be revisited on occasions, the world changes, so why not our strategies to match the current world order.

You should have a watch of this guys Investing DeMystified Videos…. So SO much sense – and oh so simple…

https://www.kroijer.com/

I’m still a big believer in the Thornhill method – my Super is set up 80/20 International Shares to Diversified Fixed Interest, Then everything else (Aussie LIC’s and Fortescue shares as i get them in my bonus) is in wife’s name as shes the low earner and thats our Australia Focus, We are just in accumulation and growth phase of our FI journey – late to it at 53 but i reckon 59 is doable 🙂

We also took advantage of the Covid Super Cash Out – My wife had an eligibility criteria – figured $20k invested how we want is better than $20k at the mercy of any government changes to super rules and future preservation age changes 😉 (She’s 48)

Keep up the great work

On a side note – does anyone have any great FI – Net Worth tracking Spreadsheets – Websiites they’d like to share or recommend??

Sorry, I can’t help you with the Net Worth Tracking spreadsheets, but could you please spell out FIOR and mention a little about this approach?

Thanks,

Hi Chris

FIOR – Financial Independence Optional Retirement.

Retirement scares me to be honest, not doing much till I wither away and die…. I’m 53 I’d like to get to 58/59 and have the option of retiring if I like, or not, or job share or not, or sit on my Verandah reading a good book with a coffee or not ????????

Also I like the idea of getting to that FI point and then just adding to it…. my plan when I depart this world is for my portfolio and super balance (what’s left at that point) to go into some kind of trust structure for future generations and a charity I support to have some dividend income whilst the capital remains intact.

My boys can have the house to sell and split but would like to leave a long term legacy that can’t be blown on consumerism (my eldest who’s 21 if he has a dollar in his pocket he’ll find a way to spend 2 ????)

I think we should look beyond our own personal FI and plan what our FI can do and help our future family generations, rather than just leaving them to spend away all our hard work

Hope that helps

Mark

Mate, I’m in a similar position to yourself… I’m 53 with wife (44), and only a few months into the whole investing scene. I can’t help feeling that I might have left it a bit late, but I’m doing what I can now to try and ‘cram for the final’.

Can I ask; was there a pivotal moment for you that pushed you towards FIOR this late into the journey?

Nige B

Hi Nige

Yeah after a couple of months looking into all this reading as much as I can, I’ve sort of come to the conclusion I’d hit my FI number right around my preservation age…. so what we have decided….. still push for Fi number but for me but concentrated mainly on maxing out what we can into super both concessional and non concessional as it’s all tax free at 60.

We are still investing outside of super (Mainly LIC’s) but only occasionally now all with DRP in wife’s name as she’s currently zero tax bracket…. when she gets to around 55 we’ll divert her investing and smash her super, then the LIC’s divis can be used at that point as some nice extras or just then throw them into her super or LIC’s depending on our tax situation.

I don’t intend fully retiring to be honest… I’d be too bored but my job allows job share etc, although to be honest I’m pretty sure I’d lose it to automation in 5-10 years so if theres a redundancy available I’ll rub hands and say thank you very much ????

Not sure if we can get in touch privately but happy to discuss more outside of this forum

All the best

Mark

I use the madfientist spreadsheet for tacking spending and net worth, with a few adjustments for australian differences.

Cheers…. Ive been playing with MoneyBrilliant today, promising so far ????

I like the fact it can link into my Broker SelfWealth too and track all that in NetWorth

Cheers Mark. I think your comment on revisiting things is spot on Mark – I’m guilty of thinking about things in a permanent way, when that doesn’t make a whole lot of sense. I think it’s the brain’s need for certainty so it likes to ‘lock things in’. That’s the excuse anyway!

Not very long to go till you hit your goals then, very nice!

I’ve just started debt recycling so the thought of dividends reducing hurts the strategy a little bit. I could just sell shares down as you say Dave – but does this mean I can still use the interest from the split loan as a deduction like I can with dividends?

Hey Luke. I think selling the shares and reducing your holdings will affect the deductibility of the interest, since the borrowed money was used to buy an asset that was partly sold. Don’t quote me on that though as I’m not familiar with anyone doing that. I would probably continue on as planned.

Some interesting thoughts Dave and I’m a believer you need capital growth in your income portfolio and it cant be set and forget in these modern uncertain times. You need to have a percentage of stocks that grow capital as well as provide dividends that you can sell down for profit to either reinvest or live off .

I’m not suggesting we all go out and buy fanboy stocks like Afterpay, Appen etc or get cute and buy Tesla hoping for a quick buck but look at companies that are middle ground that give you a bit of growth as well as pay reasonable dividends. We bought Macquarie and Magellan a while back and then sold part of them precovid that gave us a handy amount of money and then bought back in again cheap when covid hit. You are getting growth, 4.5-5% yield and they are solid companies.

You still have your core LIC’s like Arg, MLT, AFIC, and index ETF’s like VAS etc but tough times showed they took a hit too and it was really only the essentials like the supermarkets and utilities that held up.

Marcus Padley wrote an article a while back stating that retirees these days should be looking at growth

companies as a source of income and not relying so much on banks, bond proxies and the like.

Thats a bit too risky for me so I prefer a more measured in the middle approach of a bit of everything including a bit of realestate(Mortgage Trusts) too.

Problem with overseas companies is the lack of yield, they just dont pay enough and I would prefer exposure through a company like Macquarie, Magellan , WAM global or a Vanguard product.

The USA market is being propped by the Wang dang Faang hi tech stocks, you take out the Apples, Microsoft, Alphabets etc and the rest are doing poorly IMO.

I’m also not a real fan of ultra small portfolios and being diversified across a few sectors isnt a bad idea IMO.

I dont buy Buffets ideas that you are incompetent if you diversify heavily either and that his advice isnt always right IMO. Anyway thats my rant and I must check out out your podcast, keep up the good work.

Cheers Mark. Totally agree, growth is important. Some people get lost chasing the highest yield possible and it hurts them in the end.

All depends how much one wants to play the stock picking game or not I guess. Getting too fancy with picking bits and pieces and excluding others isn’t really what I want to do with my time. I think we can all agree that both the ASX and global markets will each have growth and income over the long term, just in different amounts, and we’ll all feel comfortable with different portfolios.

Hey Dave. I’m sorry to be the one to ask but someone will – VGS – Higher fees versus VTS/VEU split. VGS preference just due to simplicity? I stupidly bought some VGS then 12 months later. Ive got a large amount of cash ready to deploy right now and need to decide which horse I pick. Sometimes I think VGS the simpler bet and hoping the fees reduce over time but everyone in the fire space screams about reducing fees. I’m sure you have an opinion on this. Cheers Mick

HI Michael,

Just my opinion.. happy to hear others or receive feedback.

VTS/VEU is great If you’re comfortable with completing the W-8BEN form every 3 years, and confident that the tax treaty will remain in place with no changes to US legislation in the foreseeable future.

If not, VGS is the best alternative being Aust domiciled investing directly into the companies whilst being Aust domiciled.

Cheers

Thanks for asking about the VGS vs. VTS/VEU split, as this was the first question that I was thinking reading this post. Similar situation, I’m going to start investing internationally but haven’t decided which is the best way to go.

One problem with VTS is that even with the W-8BEN form you still pay 15%(?) Tax.

If at any stage you find youself in the AU 0% tax bracket you are losing money! This is most prevalent for unworking partners or lean fire

Hey Michael. Simplicity is one reason. The grey area of estate tax issues is another reason (since VTS/VEU are domiciled in the US). However you look at it, the fees are ridiculously cheap and will continue to get cheaper over time, so that’s not something I’d worry about.

Fair call mate, I think it’s very reasonable.

I’ve been holding 30% in VGS as my target allocation (which is slightly underweight at the moment), the rest is a couple of LIC’s and VAS. The weightings could change in the future but I’m comfortable with this for the moment.. what’s been interesting to note during this downturn is VGS has acted as quite a significant cushion to the overall portfolio, so the diversification is working.

P.S: Enjoyed the recent podcast episodes, look forward to more.

Sounds good Scott! Yes, VGS has helped up very well. And thanks for listening to the podcast 😀

Thanks for the honest and thoughtful post. Evidenced based research will always point to the superiority of a globally diversified basket of efficient ETFs from a number of different market sectors (e.g. large, small cap, bonds, international, commodities etc). Hence reading online you come across the ‘lazy portfolios’ of various combinations of the above, which will normally do better than a single country index, for example, and with less drawdowns. And as you say, dividend income may be lower, but you can sell at the end to make up for any shortfall in paying living expenses. However … for ourselves, while franking credits are in place I will stay with the (slightly less efficient) Thornhill approach. This is because ‘selling’ can be a problem if the market happens to be low when you need the funds. Additionally the LICs have proven in the past to have enough reserves to keep up dividends through even the GFC (e.g. WHF has 7 years in reserve, AFI 4 years etc). Finally, for people on low income that huge franking credit is too much to sacrifice for the sake of diversification. BUT I could revise my plans if franking is removed and that huge advantage for Australian dividend investors is lost. In which case I could probably see myself going for some overseas shares, and maybe some REITS etc. What does everyone else think?

Cheers Greg! Yeah it makes sense to leave the door open on that I think, since things can/do change. And it’ll be very interesting to see what the LICs do in the next 1-2 years.

Funny side note – I have a little bit of an issue with the term ‘evidence based’ as we can essentially find data these days to support any type of strategy (value, momentum, growth etc) and call ourselves an ‘evidence based investor’ which makes us feel all warm and fuzzy and intellectually superior. Not sure if that bothers anyone else or it’s just me! I have no issue with any of the strategies, just the way some people describe their approach lol.

Hi Dave – funny that you mentioned that, because the “evidence based” thing also annoys me to death! ????????

For the very same reason that you mentioned, you can basically find data, research that support any type of strategy or asset allocation, etc. It all depends on data selection, different timeframes, etc – I’m actually surprised that very few people seem to realise that.

It’s easy to get caught up on that stuff, but the hard reality is that when s***t hits the fan, you ain’t gonna have any professor telling you what to do or how to react, so you gotta be comfortable with your own strategy and have your own convictions, rather than relying on “academic evidence”

Also, I’ve never met any finance researcher or professor that became a great investor! Hahaha

Hahaha interesting – I’m not crazy then! Heard it the other day and I thought, “yuck – this person actually thinks he’s sophisticated and this wanky term ‘evidence based’ is somehow proof that his method/ideas are better than anyone else’s, who can also find data to prove theirs”

Right now, there are about 107 diets/nutrition plans and 324 investment strategies that could all claim to be ‘evidence based’. All that really means is, we have a study or some data that says these things might be a decent choice. *these estimates are not evidence based 😉

Actually I copied the term “evidenced based” from your blog partner(!) Pat the Shuffler (link below) when he discusses moving from LICs to something possibly more aligned with the US “Boglehead” style strategy. For myself personally I actually resonate with “Josh” above, as I do believe that behaviour will often trump any perceived advantage in investment strategy: It is important to be comfortable with your preferred strategy so as to be able to ‘hold on’ during the inevitable challenging times. In terms of arguing the advantages of the various strategies, I think some of the ‘evidenced based’ academic studies may work better for the US, and not take into account the enormous advantage that Franking gives to Australian investors? Thanks so much again for your blog Dave, your cheery and wise advice. (Link to Pat’s site follows)

https://lifelongshuffle.com/2018/10/28/pat-the-shufflers-lic-discount-estimator/

Haha I see. I’ll have to have a word to him about that 😉 Jokes aside, I have no issue with how Pat invests or writes – in fact we seem to have come to similar conclusions on certain things at different times. That term just rubs me the wrong way – I think it gets misused as it doesn’t mean all that much but sounds good.

Totally agree that behaviour is super important. And like I said in the article, no points following an approach just because others do. We should do it when it makes sense to us and we’re happy with it. Otherwise like you say we’ll really have trouble sticking with it. Thanks for reading mate.

G’day Dave, great post once again

Really enjoying your podcast with Pat and really pleased to see how well you have done in just your first week. Awesome!

I think you are bang on with your point about the need to be flexible as well as the reality that most of us will invariably tweak our portfolios as we develop our understanding and get clearer on our goals and strategies with the passing of time and investment in further self-education through blogs and podcasts such as yours!

We invest in 50/50 ASX/Intnl in super and I recently tweaked our after tax investments to tilt towards a 50/50 VAS/VGS split, after it was more 60/40 VAS/VGS tilting towards ASX for dividends and franking credits. I too feel more comfortable with broader diversification and a simpler 50/50 Intnl/Aus approach

We recently got soem independent financial advice to run over our FI numbers and our adviser suggested we consider having a little bit of international hedging to further add to the diversification of the portfolio. Made sense to me. We will be moving towards a 35% VGS and 15% VGAD allocation with future cash injections to our after tax portfolio. Agree that if our dollar depreciates, then we benefit from currency moves unhedged, but the opposite is also true when when our dollar is low, as it has been, and the potential for AUD to grow against the USD will work against returns from VGS. I do believe over the long term that currency fluctuations are likely to even out, so hedging is not absolutely needed, but I am comfortable to have a little bit in the mix for now.

Cheers

Thanks very much Craig 🙂

Sounds like an extremely simple yet effective portfolio mate – thanks for sharing.

Isn’t this almost like VDHG (except the bonds component)?

I am really torn about the investing approach for VAS/VGS vs VDHG, as I can’t fault VDHG in any way but my gut feel is that I would regret having VDHG, when I have 1 mil portfolio due to a higher MER.

Also, how do you top up your investments to achieve the 50/50 split? I am thinking of buying each month VAS then the next VGS, a round robin fashion rather than halving which end up pying brokerage fees twice a month.

Hi Dave,

As you said in the Opportunity section this approach of investing Globally diversified portfolio gives us the opportunity to invest in the market which has underperformed recently.

Going by that, isn’t it the better time to invest in ASX than US?

As of today VAS is down 23% and IVV is down only 12% from their recent all time highs.

What’s your view on this?

Going by that very simple idea, yes VAS would be the ‘opportunity’ more so than overseas markets, given Oz has fallen more, partly due to currency movements. I’ll probably be buying both from now on, as we start acting on our long term plan.

I went through a similar thought process, but being a very late starter, I realised that having enough amassed to entirely live off dividends was probably not ever going to happen. So this forced me into swapping across to indexing/draw-down and coupled with a thorough re-reading of the little red book (Bogle) put the entire subject to bed in favour of indexing and draw-down

Fortuitously, in the recent crash, our LIC’s did not drop anywhere near as dramatically as our Index funds, so this will allow me to sell these LIC’s with zero CGT impact and rebuy index funds (a lucky break me thinks!).

The other consideration is that as I age or if I drop off the perch or become incapacitated, my better half would be stressed with the concept of selling stocks (even index ETFs) and gathering all the paperwork and matching parcels bought to parcel sold for tax purposes – so I went with the Vanguard Wholesale Fund option which is infinitely easier to redeem and fill out tax returns compared to individual shares/ETFs (Vanguard will just set up a monthly draw-down similar to a Super pension).

For us, both the accumulation and draw-down process for Wholesale Index Funds has the same ‘ease’ factor of watching dividends drop in. You might want to think about the simplicity factor of Wholesale Funds later on in life for the future too.

We now have three investment buckets:

1. Directly held Vanguard Wholesale Fund (Australian).

2. Vanguard Wholesale Fund (Australian) held via Australian Unity 10 Invest Investment Bond (total costs structure of 0.46%) (This is as an alternative tax structure to Super that suits our current tax circumstances)

3. Vanguard Wholesale Funds in First State Super (50% Australian and 50% International with exclusions)

P.S. Sell spreads on many Vanguard ETFs and Funds have been hiked up during the latest stock market correction – will not affect you until you are in draw-down though.

Interesting Phil, appreciate your thoughtful comments! Haha that red book is a good one 😉

We also took advantage of large LIC premiums during the market fall, pretty handy.

I totally understand your point on making it so your partner can be comfortable handling it. A very under-appreciated aspect of all this. The tax returns are easier with wholesale?… I wasn’t aware of that. Mind explaining how that works?

It’s a good point to make and definitely something to consider, thanks again.

TL;DR – Worse case scenario – all I need is 2 documents each FY once drawing down from a managed fund.

Specifically in draw-down mode, with a Vanguard Wholesale Fund all I need is 2 documents:- 1. a Transaction History Statement and 2. an AMMA tax statement for that FY. That’s it. I can do this myself using MyGov or, I can just flick them to my accountant (personally I am happy to pay the accountant – I’ve got better things to do).

Compare that with Individual Shares, LICs or a portfolio of ETF’s – you personally need to keep a accurate record or every single purchase, event and sale – each event for each holding has a document (as you well know 🙂 ). If you are regularly buying ETF’s LIC’s or shares every month over many years then this amasses into a huge ‘pile’ of documents over the long haul. If I fall unwell, lose my marbles or pass away etc, then this pile of documentation is someone that I love and care for’s responsibility (heaven forbid they miss something)…..they will NOT be thanking me no matter how well organised/filed.

With Australian Unity 10 Invest, nothing needs to be lodged with ATO during accumulation. If we draw down on this fund in under 10 years then it is a single tax statement each FY (including 30% tax credits) that is supplied by Australian Unity. If we draw down after 10 years then nothing is required to be lodged with ATO.

(Compare that with Individual Shares, LICs or a portfolio of ETF’s – you personally need to keep a accurate record or every single purchase, event and sale – each event for each holding has a document (as you well know ???? ). If you are regularly buying ETF’s LIC’s or shares every month over many years then this amasses into a huge ‘pile’ of documents over the long haul. If I fall unwell, lose my marbles or pass away etc, then this pile of documentation is someone that I love and care for’s responsibility (heaven forbid they miss something)…..they will NOT be thanking me no matter how well organised/filed.)

Or Phil – just Use Sharesight to automatically monitor your portfolio, track your trades and generate a free year end tax report… But yes i agree simple is best

Thanks for the detailed reply mate, much appreciated. I guess that’s the thing – it gives Vanguard the task of keeping track of cost base and realised gains in a given year, which is pretty handy. As Mark said, I also use Sharesight, so it’s not much effort, but still the managed fund option is one step further!

Hi Dave,

Nice post. Made a similar decision about 12 months ago to increase our global allocation, but as we near retirement I haven’t been able to commit all the way to 50/50. I did advise our son to go 50/50 in his super though.

Would be interested to hear what made VGS your choice? Is it the comfort with Vanguard? I hold VGS, but have also been using IWLD lately, with its lower fees and slight tilt to small caps.

Cheers

Cheers mate. IWLD is a fine choice too, but I don’t like it being a fund of funds, rather than holding the stocks directly like Vanguard does. This makes it less tax efficient and a bit less clean in a way. Plus I do prefer Vanguard. Good comparison article on VGS vs IWLD here – https://www.etfstream.com/feature/10047_australias-best-global-shares-etf-vanguards-vgs-or-ishares-iwld/

Hi SMA,

Thanks for sharing your strategy change. It is a big mindset change to go from dividend investing to be comfortable with sale of stocks for investing. But post covid we too think that dividend yields will go down even for Aussie companies which will need to/should focus more on R&D and investing back in the business.

But due to the expectations of majority of the shareholders, it will not be easy for the companies. We did see how the discussion around franking credits went during the election.

In any case, diversification is always good.

All the best with the new strategy and thanks again for sharing your thoughts.

TwoToFIRE

Hi Dave,

Have you considered VTS and VEU for more diversity and lower fees? Yes, they are not domiciled in Australia (yet). VTS management fee = 0.03%.

I did consider it but decided on VGS as it’s simpler. May reconsider later if they do become Oz based. Fees will come down across the board so gap will reduce – wasn’t a huge factor for me.

I had a thought regarding investment discipline and behavioural control (i.e. controlling self behaviour and our tendency to sell at the bottom and other such traps). One of the Thornhill recommendations is to avoid stress by not looking at market valuations and instead keep focussed on the growing income stream. So Peter would show his ‘mother ship slide’ of dividends steadily increasing over many years, despite the mad fluctuations of the share market. Actually he qualified himself once speaking about the GFC and said you’d ‘have to be dead’ to not notice those kinds of losses in your account…. Having said that, his advice was to just ‘buy more’ during such downturns and to ride it out, keeping your eye on the steadily increasing dividend stream. (Which Grandfather LICs can provide for between a 4 to 7 year recession, depending on the LIC and their respective level of reserves). However if we are to move into ETFs (no dividend smoothing) and International Shares (relying on growth more than dividends, not to mention no franking) – then we lose this very valuable advantage of being able to focus on the income stream alone. If my retirement depends on my income stream, I can relax – clearly income is growing yearly (or very near to it). So what if the market crashes? If my retirement depends on something I’m going to have to sell down in the future, then suddenly I am more price focussed and all those old fears return… For me now in my 50s the Thornhill approach is like a breath of fresh air, not having to bother about market prices. By family connections (relative worked with Jack Bogle in Vanguard in the US) I’ve seen the alternatives first hand, and thoroughly respect the approach from an objective, efficiency point of view. But for me… because of the ease of better behaviour with Thornhill’s approach – I’m never going back! But respect and sincere best wishes for Dave and everyone trying the huge universe of wonderful available approaches out there!

The other aspect to consider is that the more one moves towards a capital sell down approach, the more volatility becomes an issue, that then needs to be managed (as people are exposed to the variability of capital values), therefore, at some stage, one would have to consider adding the most horrible long term investment there is on planet earth – bonds! Don’t believe me? Who would invest in an asset with an average P/E ratio of 50x, paying a static, no growing income stream, with a principal that is voraciously corroded by inflation, with diversification benefits that has been non-existent in this pandemic and that has had a 30+ year bull run?

Just something for people to keep in mind when considering their options…… always have to think about both stages, accumulation and withdrawal, when making these decisions

(Apologies if I’ve over-stated things in the above comment. On a re-reading I realise Dave’s article only mentioned adding international shares to complement and add diversification, not necessarily replace a dividend-focussed approach altogether. Can definitely see the appeal in this. E.g. over 5 years the LIC AFI has gained 4% p/a, VGS shows an 8% p/a gain! Who wouldn’t want that?)

Nice post Gregory, and definately my thoughts too at this stage. I think one advantage with LIC’s is the fact to a degree they are managed. They can get in and out of companies where the dividends shrink if they wanted to and focus on better dividend payers.

I hold FMG shares as the only individual company purely as I get them if I get a bonus at work, now there’s a good dividend payer, LIC’s could just go find the better dividend payers surely??

“They can get in and out of companies where the dividends shrink if they wanted to and focus on better dividend payers.”

Can they? The pent up capital gains might prevent them dumping some or all of the banks and moving elsewhere.

Do they? I’ve not seen any evidence that their portfolios change all that much. My expectation is that the larger LICs will just sit it out.

Fair call, I think the key is the could if they wanted to…. didn’t AFIC reduce bank exposure a bit at the end of last year? Thought I read somewhere they had, I may be wrong…

Still I’m happy with the dividend smoothing they can offer…

If you go the other route of diversifying your portfolio towards more of a capital gain strategy, at some stage in the future when you come to sell down some capital for income purposes you’ll get a CGT event

Whatever way you look at it the taxman has you by the short and curlies ????

Unless you look for your capital growth strategy within super until preservation age and have your dividend strategy to get you to preservation age…. (I’m hoping I’m right on this as pretty new to FI strategies)

Hi Dave,

Firstly, just want to let you know that I’ve really been enjoying reading your posts over the past year, and am pleased that there will be a good regular postcast. Well done on finding interesting content to write about every week.

On the topic of diversification, Mad Fientist wrote an interesting post about investing in bonds, and, being in the middle of an economic downturn, I was wondering if this is also an area that you are looking into investing in or if you plan to still invest your money solely in shares?

Hi Emma, thanks for following along, glad you’re enjoying it 🙂

Bonds isn’t something I’m looking at, given we have a large cash holding due to our situation (transitioning out of property and dollar-cost averaging into shares over time). Long term we’ll prob just keep a small amount in cash 5% of portfolio or so, and live off dividends and any part time income. The cash will sit in an offset account (as it does now) and likely earn more than bonds would. Hope that helps.

The other aspect to consider is that the more one moves towards a capital sell down approach, the more volatility becomes an issue, that then needs to be managed (as people are exposed to the variability of capital values), therefore, at some stage, one would have to consider adding the most horrible long term investment there is on planet earth – bonds! Don’t believe me? Who would invest in an asset with an average P/E ratio of 50x, paying a static, no growing income stream, with a principal that is voraciously corroded by inflation, with diversification benefits that has been non-existent in this pandemic and that has had a 30+ year bull run?

Just something for people to keep in mind when considering their options…… always have to think about both stages, accumulation and withdrawal, when making these decisions

Great to see you aiming towards a more diversified portfolio outside of super mate, welcome to the club!

And congratulations to you and Pat on the podcast!

Haha thanks very much mate. I’m definitely slower than most to join 😉

One significant problem with International Diversification is currency. The long term average AUD to USD price is around 75c and so if you are purchasing now at around 65c you are effectively giving yourself a potential -20% anchor on day 1.

***Yes, previous currency values are only a guide and possibly wont represent the future but it is still a valuable guide as to the relative value of the AUD vs the USD over the last 30 odd years depending on the world events etc.***

If the AUD was 75c+ plus then it would be an easier choice as you are buying the ‘high side’ of the long term average and the odds are that at any particular point in the future where you might want to sell you will at least be at parity or have gained through a lower AU currency.

Is VGAD (hedged VGS) a better option?

Should we ignore past currency ratios and just go for VGS?

These are questions for the individual and their own risk appetites but the thought of starting an investment with a potential -20% anchor to the long term currency average doesn’t fill me with joy 🙂

LOL lots of unknowns as you say. I’m just not sure, so it’s not a game I’ll bother playing. 75 v 65 isn’t meaningful enough to me to worry about. Currencies don’t compound, so if it moves back to 75c over 10-20 years, the effect will barely be noticed.

As you’ve said, nobody knows what the next 30 year average will be, so the potential anchor may not be an anchor at all. Maybe just slightly more probable than being a non-event or a tailwind. Each is possible.

Also, it’s not a one day decision, it’s a slow and steady increase in an allocation, which will be at different prices and different currency points. So any dramatic negative effect is likely to be negated through the effects of averaging. No right answer for everyone at the end of the day. And unless some strange situation is staring me in the face, I prefer to keep it simple where possible.

Have you read Ray Dalio share portfolio, he has changed or updated his share portfolio lately. He changed to 40% bond (bond yield is so low at the moment). Equity only 35% I think, anyway, it’s way lower than previously. He might think the coming year equity performance won’t be as good as before.

I owned VGS and NDQ, thought VGS would do better than NDQ but it was opposite, NDQ went up over 10% since I bought it in early this year but VGS went down. NDQ charge fee is higher than VGS.

According to Ray Dalio research, Asian country fintech, AI will catch up with or better than US in the coming 15 years. Have you thought about VGE (It’s down at the moment)? It paid dividends as well.

ASIA is the asian (obvious) mirror etf of NDQ. At approximately 1/3 of NDQ price, if you support that theory, then it may be worth a look.

Hey Jessica. Sounds like you’re into making specific bets and market calls, which I’m not.

I don’t follow how Dalio invests but have read some stuff by him over time. He’s got a very different set of circumstances to someone who is trying to build a portfolio to sustain them for 50+ years. I have no interest in making short-term bets or having large allocation to bonds for whatever reason – both of those things are going to be detrimental my long term returns.

I’m not interested in betting on tech or Asia specifically, regardless of whether they’re up or down. I’m happy with my long term Aussie allocation and a basket of international shares for diversification and VGS is a simple way to achieve that. Whether it’s optimal or perfect or something else will perform better, I don’t know, and doesn’t really matter. Emerging markets (VGE) is something I could add, but I’m just not that comfortable with them and feel VGS is ‘enough’ diversification. Australia has a fair bit of exposure already to emerging countries as it is.

I think you have made many good points here Dave and have a good strategy laid out. I am not sure if I have met many investors at all that come up with a detailed strategy in their 20s and never tinkered with at all for the next decade or two. So the kind of changes you are talking about are certainly not extreme. I also think your points on tax policy are well worth thinking about for investors. I happened to write a little bit about the same point myself yesterday. The issue has gone a bit quiet after the last election, and obviously the general news media have had other things to discuss of late. It may not be long though until franking becomes a hot topic again. Not to mention all sorts of other tax policies, meaning diversification from that perspective makes sense. Difficult to know what might happen.

I liked the podcast by the way, very impressive already seemed like you have done a heap of them before even though it was just the first few episodes.

Really appreciate that Steve, thanks a lot! And great to hear your feedback on the podcast – definitely feels like we’re very much in ‘beginner-land’ to be honest! Pat is a good editor I think 😉

Yes I think you’re right – both sides of govt may start looking for ways to repair the budget after the current situation is behind us. Franking credits are an obvious choice, and maybe negative gearing, who knows. Will be difficult to remove either of those but maybe putting a cap on them would be acceptable?

All this talk of investing internationally (Australia only 2% of the market etc) made me look around a bit. CTY (on the London stock exchange – ‘City of London Investment Trust’) is quite interesting for classic LIC lovers. I think this one is owned by Peter Thornhill. Established 1891, has never failed to increase the annual dividend since 1966, paid quarterly. The yield is currently just shy of 6%. Australian LICs can get 6% with franking but what if franking were removed? Australian dollar currently very strong against the pound (due to Brexit). Just a $20 share-trade away on Comsec or NAB trade… Does this sound interesting to anyone else? The advantage of a steadily increasing income stream and some international exposure (London is the second largest exchange in the world).

Not a bad investment IMO, considering the FTSE 100 is cheaper than it was 20 years ago.

Two things I’m not sure of though:

– Is the 6% dividend yield sustainable, or is it based on pre-covid dividends?

– Do you get franking credits for this investment? I thought that was only for Australian based companies…

Hi Dave, no of course no franking for the UK investment. What I meant was that the UK investment was 6% without franking. I’m thinking ahead to when maybe franking is removed in Australia and then we only get 3% or 4% max for most companies. In which case this 6% from the UK would look pretty good. The dividend currently is proposed to be paid throughout the Covid period out of reserves (typical closed-end fund dividend smoothing). I’ve read that there are 50 million pounds of reserves. The fund has not had to reduced dividends since 1966, which obviously includes lots of other challenging times when eg bank dividends were cut. Nb the fund increases dividends each year but I don’t think it does quite as well as the Australian LICs in outpacing inflation. Greg

Hi Dave,

Interesting developments here re international diversification! 🙂 But I agree with you and am currently looking to add either IWLD or VGS to my portfolio. Anyway, one thing I have always struggled to understand when it comes to selling down the magic 3.5-4% p.a. in retirement is this: Even if the value of those shares increased by more than what I’m selling for annually, I’d still be selling nominal shares and that means that at some point I will have sold the last share (even though that last share might be worth a lot). This conundrum has always had me leaning towards a dividend approach, or am I missing something?!

Keep up the good work and best of luck for the podcast as well!

Hey Matt. It’s a good question. In theory, perhaps, but depends how long we live lol. What we need to remember is that because the value of the shares is increasing over time, we end up selling fewer shares to create the same amount of dollars. On average, this would continue and even accelerate over time due to compounding, resulting in fewer and fewer shares sold, so is unlikely to be a problem. As mentioned, dividends alone are going to be over 3%, so you the amount of selling is likely to be fairly small. Hope that makes sense.

Hi Dave

Congrats on your success with the blog and the podcast – that is fantastic that the podcast is at #1!

I think it comes down to the relatability of the work you put out, it resonates with the lay person. You guys talk using understandable language and don’t come across like dickheads in suits with slick haircuts haha.

You mentioned that you are from country Victoria originally, people seem very down to Earth out that way. I’ve got a good mate from Orbost, they are all really good people out that way who can smell BS from a mile away.

On a personal note, it is good to see you are getting out of your comfort zone and doing things like the FIRE premiere and now this podcast. Good to see you went along to that premiere even though you said you were shitting yourself beforehand haha, many of us have been there before – thanks for sharing that.

Anyway it is really impressive that you are beating shows like The Property Couch and Low Rates, High Returns – I am an avid listener of both of those.

It is good to see you are adjusting your strategy going forward too, I have adjusted my strategy over the years as well. As you say, you can’t be too rigid in your thinking, but at the same time you can’t be constantly changing strategies over the years as you will not see the long term benefits.

For what it’s worth (and for posterity) my share strategy is as follows:

~70% in a global ETF strategy, buying countries cheap on the CAPE ratio. Cash v shares % is contingent on whether the US is high or low according to the CAPE ratio. I am about 95% in cash at the moment because of the general market conditions caused by the pandemic, and the US is very expensive per the CAPE ratio. (This is basically the strategy that Pete Wargent and Steve Moriarty recommend)

~30% in a trend following strategy. The returns of the last month have shown me that the stock market is basically removed from reality, not sure how we can be in a bull market when we have the worst financial conditions in the last 100 years essentially. You may as well follow the trend when the market is going higher and leave your logical thinking at the door.

Anyway mate keep up the good work, it is great to see you are doing so well.

Cheers

Dave

Thanks very much Dave 🙂

Appreciate your support and kind words. Haha yes, relatable is certainly what we aim for – there’s no need for fancy language here. FI is very doable for many people, by learning to save properly (none of this wussy 10% stuff) and investing simply… why complicate it? Not sure I could even fake being an intellectual/academic style person anyway!

That’s interesting, thanks for sharing. I’m somewhat aware of their approach. It’s definitely not for me, but interesting nonetheless. I hope it works out, and feel free to let us know how it’s going over time.

Dave – can you promise to come back here and let all of us know when it is time to get back into the market, please?

I mean, seriously…. that’s the problem with people – they all think they can outsmart markets, it is time and time again!

For low long have people been saying the CAPE ratio was high? I hear that since 2016/17, and guess what happened with the market? It kept going up, and up, and up! Had you been in cash all that time, your returns would have suffered tremendously. You miss those top 10-20 days when the market shoots up, and your long term returns are permanently damaged (have a look at Dalbar studies to see what returns individual investors usually get because of market timing strategies like the one proposed).

And with due respect, Dave, I consider myself someone with an open mind when it comes to researching, reading and discussing about different investment strategies, but I must admit, in all these years, I don’t think I’ve ever come across such a rubbish as what is proposed by those guys (Pete Wargent and Steve Moriarty) – it is shocking!

It’s a mix of market timing, passive but active investing (i.e. placing specific bets on certain countries, industries – how is that different to picking companies?!?), the ‘old’ buy low sell high mentality (but these guys took it to another level, requiring the individual punter to be able to time a whole sector/country – good luck with that!), with misplaced quotations from Ben Graham and Warren Buffett thrown here and there (all employed in the wrong context by the way!), a bit of Ray Dalio action as well, etc, etc, etc – a total mess!

Full of non-sense and really damaging to the individual investor – really interested to hear what other smart people who frequently visit this forum thought about it; open to other thoughts.

Dear Peter, excited and grateful to have your added input to Dave’s amazing blog. I think Ray Dalio himself said that ‘more money has been lost by people trying to avoid a crash than they would have lost in a crash itself’. (i.e. in terms of years of lost opportunity when markets are climbing). But – what if you’re using borrowed funds (e.g. modest use of a mortgage offset account to purchase LICs)? It it more valid then to wait for pullbacks? I thought I’d read in a blog somewhere that you commonly collected dividends into your offset account, and then applied them when there were bargains? But please forgive if that is a complete misquote!

Greg, I put the question back to you: what is a bargain? That’s the problem: conceptually, it makes sense to wait and “buy low and sell high”, who wouldn’t wanna do that? Where is the bottom? We can only see that in hindsight unfortunately. I encourage you to listen to Peter Thornhill’s recent podcast with Aussie Firebug where he answers a similar question (on people looking for market “bottoms” / bargains).

Also bear in mind that most people investing in index funds, should be, by definition, a believer that markets are efficient (not always rational or right, but sufficiently efficient), so an “apparent bargain” could easily be a value trap – e.g: cruise companies, airlines, etc – are these bargains? Why don’t you borrow funds and buy them (makes sense, right – some are -80% off!) – anyone buying them is basically doing 1 of 3 things:

1. betting against what the market believe they are worth TODAY (based on the available information we all have at this point in time about their future prospects), or

2. is inadvertently claiming they have an edge over the market (i.e. they know something the market don’t know) and therefore believe they are worth way more than their quoted prices, or

3. are gambling and taking on substantial more risk than the market

Re: your question on parking LIC dividends into an offset account, same principle applies – it is essentially market timing, as you are betting on the fact you can park that cash there and then buy dividends cheaply at a future date, this might or might not happen. This is money that could be buying more shares, earning more dividends, more returns, compounding, etc that is basically sitting there “waiting” for a crash – there is an opportunity cost to that too (costs of omission are usually more expensive than cost of commission)

By the way, it was Peter Lynch that said that famous phrase on losing more money preparing for a crash.

Ray Dalio’s advice exposes individual investors to one of the greatest risks they face: longevity risk (with his excessive obsession with controlling volatility and substantial allocation to bonds! See my comments above on this “great” asset)

Cheers

Peter

I am not one of the “smart investors” but I am a follower of Jack Bogle’s preaching that traders are not investors, they are gamblers. As such, 95% of them will suffer reversion to the mean which, at best will leave them with the market average, less trading fees and taxes. I may be old and dumb,but low cost index funds suit me fine.

Hi Peter

Thanks for sharing your forthright views on the matter.

Keen readers would have noted that I am putting 30% of my money to a trend following strategy, so I won’t be entirely missing out on any gains that may accrue from share market rallies.

Regarding your critique of the strategy, I think it is a case of “each to their own” with investing. I think it is worth noting that Pete Wargent’s blog has been going since 2012 and he has been pretty consistent with his message; he hasn’t really strayed from the fundamentals and would have a self-made share/property portfolio north of 10 million – he definitely walks the talk in that regard.

It would be great if you can share your strategy, is it to stay 100% invested 100% of the time?

I am not entirely sold on that idea, especially in the current environment. I believe it was Warren Buffet who said, “Rule #1: Don’t lose money” (and I hope that quote is not misplaced/out of context).

It seems to me that there are times in the market that are riskier than others, and it pays to place your bets accordingly and preserve capital at times of greater risk. The CAPE ratio is not perfect, but I think it has some predictive power (Norbert Keimling has put out a good paper on this).

Look forward to hearing back from you, and it is good to see some spirited debate in the comments section.

Cheers

Dave

Dave, I’ll stay out of the strategy debate lol. Not sure if you’re aware, but Pete has largely been a buy-and-hold style investor until about 12 months ago. I’ve been a follower of his since the start, so this strategy is maybe a little bit out of character – nothing wrong with that, just pointing out he hasn’t followed this strategy for very long (publicly, at least) and it’s not been the source of his success/wealth to date.

I understand why he’s doing it, have no doubt he’s researched it thoroughly, and that his intentions are sincere/honest. But it’s definitely different to what he has written about for most of his books/blog history.

That rule 1 Buffett quote I think is misused all the time and can be justified to do almost anything. I take it to mean do your research and don’t buy into an investment where PERMANENT loss of capital is likely. With indexing, permanent loss won’t occur as the index won’t go to zero. If he took this rule to mean avoid short term losses, he wouldn’t invest in the sharemarket at all. Berkshire has lost 50% of its value many times over its history – so have most of their investments. That is not WB breaking his own rule, that’s just the nature of markets.

People can debate whether cheap markets will outperform, but for what it’s worth, cheap markets can and still do experience large losses. They do not exclude you from experiencing losses, therefore wouldn’t they also be breaking Buffett’s rule #1? The answer is, the rule has been butchered to death and people can use it to justify any decision, so it’s almost meaningless in that regard.

p.s. note to self: so much for staying out of the debate lol.

Hi Dave

Yes I am aware that Pete has only started writing about this strategy recently. It is a bit different to the buy and hold, set and forget strategy. It requires you to be a bit more active, and removes some concentration risk.

I think a lot of people have changed their thinking post-covid. Investors are becoming more aware of risks like companies halting dividends, simultaneous global demand and supply shocks and governments changing policy in response (i.e. possibly removing franking credits as you mentioned). It makes sense to diversify a bit because having 100% of your capital in the ASX is a very concentrated portfolio, and the future has become a lot more uncertain.

Agree with your sentiments re Buffett quotes, people run into trouble if they get too dogmatic in their thinking.

Looking forward to the next blog post 🙂

Cheers

Dave

Dave – agree that each one of us have to adopt a strategy that feels right to us, no question there. But having consistent arguments and a strategy based on conviction is key for any successful investor. My critique of their “strategy” is the complete mix up of concepts and financial theories that sounds good in principle, but are unrealistic and hard to implement. They mix up index investing, with value investing, with market timing, etc. I’ve never met a “total market/sector/country” value investor – they might be the first! They even use words like “betting” all the time in their podcast – even you now are using these words (“placing bets”, as per your comment below) – is this really a strategy or gambling? Something to reflect on.

Also, the way they describe it, gives the false impression that it is easy to recognize where we are in a cycle IN ADVANCE (and that is the key word here!) – and being able to do this consistently over 10, 20, 30 years, which is another challenge, and then paying all those capital gains taxes, spreads, market impact costs, brokerage fees every time you dance in and out of the market – sounds easy, hum?!? Be careful with the market geniuses or gurus that have been claiming markets are expensive and “there will be a crash” for 5-6 years – they will eventually be right if they claim that every January!

Again, I’ve been hearing that we are at the end of a cycle since 2016/17, the CAPE ratio was already high back then, so was that really a successful “sell signal”? I doubt – look at the charts to see where we were back then and where we are today (and that is not even counting the dividends you would have left on the table during all these years!).

Now on Warren Buffett, again, classical case of manipulating his words and another usual case of putting his wisdom out of context: first of, he doesn’t give a damn where the market is, or cycles, or whatever – he is a stock picker, who has a tremendous talent and ability to establish the intrinsic value of companies and buying them when he believes their price is below that intrinsic value he calculated – period. No market timing tactics, no cycles, no nothing – otherwise he would have sold his entire share portfolio now, correct (as you quoted below, “Rule #1: don’t lose money”, right)? As far as I can see, he is not selling his Coke, Apple or whatever other stocks he holds because CAPE ratio is high, is he? And before anyone mentions it, Airlines were sold because they lost their fundamentals (the STOCK itself, not the MARKET, or not because of “the end of an economic cycle” or a high CAPE ratio!) – very important distinction and my whole point in this thread.

And as a matter of fact, Buffett himself advise no-nothing investors (which I consider myself one of them, together with probably 99% of the population), to BUY AND HOLD index funds for the long-term, not trying to time the market and being in and out of markets all the time; in fact, his instructions in his will is for a simple buy and hold strategy with 90% in an S&P 500 index fund and 10% in short term US government bonds – that’s it, as simple as that. And a lot of people that like to quote him here and there, conveniently choose to ignore or even mention that advice.

The fact that Pete Wargent has $10 million and has been around since whatever date has little relevance; I could easily argue that Thornhill has been around for a lot longer and is an old school buy and hold investor with a 100% share portfolio of a similar size – so what? how is that relevant to this discussion?

Again, my point here is the fact that these guys casually describe their strategy AS IF it was that easy to establish when a market is high or low based on a single ratio – just take a moment to appreciate the mammoth size of such a task when even experienced and successful investors struggle to find the intrinsic value of a SINGLE stock – how is that for a whole country, economy or sector – brave task indeed! Case in point: Japan has been “cheap” for ages now, how is that for an opportunity for you? Great tip, huh!

I’ll leave you with a brilliant quote from Jack Boggle (not misplaced, and appropriate for this discussion, I hope):

“The idea that a bell rings to signal when investors should get into or out of the market is simply not credible. After nearly 50 years in this business, I do not know of anybody who has done it successfully and consistently. I don’t even know anybody who knows anybody who has done it successfully and consistently.”

Poor Jack, it is a shame he passed way without having a chance to meet the Great Pete Wargent….

Hi Peter

Thanks for taking the time to write all that, hard to disagree with anything there.

I agree that the future can’t be predicted and you risk having your money eaten up by fees, brokerage, cgt etc. if you are constantly in and out of the market and chopping and changing strategies. I can’t remember where I read it but someone said ‘money is like soap, the more you handle it the less of it you end up with’.

At the same time it takes a lot of conviction to be fully invested through the cycle and live through 50% drawdowns, something I am not emotionally comfortable with.