I recently became the owner of a brand new Tesla Model 3.

Not gonna lie, it feels very strange.

After not buying all that much (besides investments) for the last 15 years, I decided to indulge in some luxury.

While this might seem like a wildly out of character purchase (and let’s be honest, it is), when put into the correct context it might not be as crazy as it seems.

In this post I’ll explain…

— Why I bought it (and how)

— The experience so far (what I do/don’t like)

— How much it cost, and ongoing savings/expenses

— Charging options + EV basics

— Tax rebates + subsidies

— Whether you should get an EV

Alright, let’s get into it.

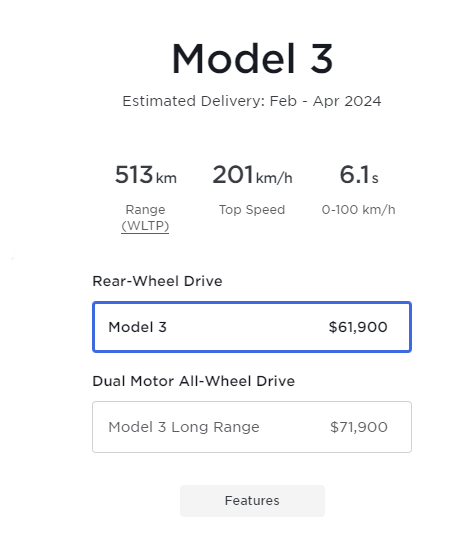

A relatively standard Model 3.

The only modification I made was blue paint. I was considering the larger, nicer wheels, but I’d read those can reduce the range a bit.

Why not the long range? It’s ten grand extra and only offers an extra 100km or so of range. That didn’t feel worth it to me.

Especially when most of our driving will be relatively short, plus where we road-trip (South West WA), there’s plenty of chargers along the way.

I had to draw the line somewhere! 😄 And since that’s not a real picture, here’s one after bringing it home:

After flirting with the idea for quite a while, I took a test drive back in November. The new model 3 hadn’t been released yet, so it was a 2023 version.

It was a strange test drive. No keys. No noise. No dials. No gearstick. But it was fun to drive, nice to be in, and felt futuristic. The novelty effect was in full swing.

After another few days of thinking about it, I ordered one!

The 2023 model had sold out for the year, so I had to wait for the 2024 version.

Anyway, you’re probably more interested in why we bought the damn thing rather than the actual details of the car!

Let me explain…

Here’s the story:

Before this, I’d been continuously exposed to the Model 3 for the previous 12 months.

My friend bought one to use for work as an Uber driver, replacing his trusty Corolla. Side note: his operating costs are now much lower (fuel and maintenance) making his driving more profitable per hour. He also qualifies for ‘luxury’ rides as a bonus.

Sitting inside, I found it pleasantly different from anything else I’d seen before. Granted, I don’t have a lot of car exposure, but I found it attractive yet minimalist, with thoughtful features, and cool technology.

But that’s why I liked it. Why did I actually buy one?

Well, because we can afford to without it having much of an impact on our finances. Importantly, the purchase has absolutely no impact on our freedom or lifestyle.

If that wasn’t the case, I simply wouldn’t do it. My personal motto is “freedom before fancy shit”, and that hasn’t changed.

Many of you are waiting to sink your teeth into this part!

How much did the car cost?

$63,400. Or $59,900 after the (incoming) WA rebate of $3,500.

Then of course there’s other fees and government charges (like stamp duty) which added another $6,000 or so. We also bought a wall charger and have that installed at home for another $1,800 (more on charging soon). Like having your very own 7/11 servo at home haha.

So yeah, it’s been an expensive exercise 😄

How did you pay for the car?

Cash. We held back from investing and let our money pile up a bit. The book has also continued doing much better than I could’ve ever imagined, so the car is kind of a reward for that I guess.

We did look at a novated lease (more on that later), but it didn’t make sense for our situation. The cost was going to be roughly the same overall to own the car outright, so we didn’t bother.

Will we actually save any money?

Absolutely not. The smart financial option is keeping our Hyundai i30 as long as possible, not sinking tens of thousands extra into a lump of metal on the driveway. This is a lifestyle purchase, not a financial one.

In terms of ongoing expenses though, our ‘fuel’ bill will definitely be lower, despite the expected increase in driving. Maintenance will be lower too.

Here’s a summary of the main cost differences compared to our Hyundai i30 hatch.

We’ll be spending about $15 to ‘fill up’ the Tesla. That’ll probably get us about 450km of range on average.

For the same km, the i30 would cost about $60 in petrol. So the EV is much cheaper in that regard. Once our solar is installed in the next few months, our ‘fuel’ bill will be near-zero.

Insurance is pricier due to being a more expensive car and choosing comprehensive cover (see below). So that would be the case with any new car purchase vs keeping an older vehicle.

Servicing will be lower since there’s very little maintenance needed. The biggest cost likely will be the fancy tyres. My Uber-driving mate still had 2 original tyres after 80,000 kms! So, with our rate of driving – about 15,000 km/year – that won’t amount to much, maybe one full set every 5-7 years.

In short, the annual savings aren’t as good as some EV fanatics claim (it costs basically nothing!), but better than the naysayers claim (you save basically nothing!).

Overall, I expect the Tesla to be about $1,000 ‘cheaper’ to run in our particular scenario. But depreciation and the opportunity cost of having a more expensive car is multiples of that 😅

What’s the insurance like?

People have said insurance costs for EVs are insane. It’s true, there are certainly some very high premiums being quoted. But if you shop around, there are still insurers who are providing reasonable cost cover.

We went with RAC, $1,115 for comprehensive cover. AAMI quoted a similar figure. I’ve heard of other decent quotes coming from Allianz and NRMA, but it pays to shop around (as always).

Why did you choose comprehensive?

Long-time readers know I’m generally not a big fan of insurance. I only want to insure against massive out of pocket costs.

Two reasons why we went with comprehensive: to make the experience of owning an expensive car less stressful. And because I’d rather not fork out $60k for a new car if we get in a ‘write-off’ type accident.

We could technically afford to pay out of pocket for a full write-off or major smash. But the psychological benefits of not having to think about the ‘risk’ when driving and the convenience of having to pay very little if something happens, is worth it to me in this case.

I’ve always thought the worst part of owning an expensive car would be the stress of someone hitting it, or the frustration of getting it in an accident. So I see this as a deliberately irrational choice. Of course, I chose the highest excess available with RAC, which was $2k.

What I like about the car:

It’s fun, fast, smooth, and extremely comfortable. Very enjoyable to drive or just be in.

I like the minimalist interior and how heavenly quiet the car is. Driving is so incredibly peaceful, and they use ‘acoustic’ glass and special tyres to reduce noise even further. I tend not to drive with music on, so it’s even more noticeable. For someone who likes peace and quiet to relax and think, it’s bliss.

I like not having to use keys or a remote. It’s connected to my phone so I can just walk up, open the door, and start driving. That’s optional, but I like it. The car also closes the windows and locks the doors once you walk away. Little things like that.

Something unexpected too: air-con in the seats. I didn’t care about this at all when buying the car. But after turning it on one sweltering Perth day… holy shit it’s good!

It’s also pretty, haha. I’m honestly not a fan of many car designs. In fact, there’s very few cars I actually like (the older Chrysler 300c is another – like a poor man’s Rolls Royce Phantom). And while I’m not really a car person, luxury sedans are more my thing than sports cars, spacious SUVs, and obscenely large child-like monster trucks (RAM/F150, etc) 😉

What I don’t like:

It gets hot inside, thanks to the glass roof. Ironically, this makes the backseat passengers have the best view in the house. Also, if you’re taller your head will sit closer to the hot roof.

In cooler climates than Perth this wouldn’t really matter. Either way, we just got the car tinted to keep more heat out. This will probably reduce AC use and save battery. If it annoys me further I may get a cover for the glass roof. To be fair, it doesn’t take that long to cool down with the AC, and you can always ‘pre-condition’ the car to be cool when you get in.

The only other thing that has annoyed me so far is the automatic emergency lane assist. It’s come on a few times if I’m touching the outside of the lane (seems to be a safety feature I can’t turn off for now). The slight movement doesn’t worry me, but the beeping does. Apparently there’s no current way to permanently turn it off, other than de-selecting it before each drive (which I can’t be bothered doing).

For those unfamiliar, there are essentially three speeds of charging.

1- Wall outlet (slow). This just requires a ‘mobile connector’ cable (these stupidly don’t come standard anymore). Charging speed is about 10-15 km/hour. While that is pretty slow, it would actually be enough for us (and many households). The average household drives 40 km/day. Plug it in after work, and by the morning, you’d have replenished well over 100km.

2- Wall charger (medium). These are far more convenient. Also known as destination chargers. Picture below. Charging speeds are 60-70km/hour with 3-phase power, or 25-50km/hr with single-phase (depending on being 16/32 amp). Often enough for a full charge in 5-8 hours, easily overnight. You’ll also see these in public spaces, like shopping centers, council buildings, hotels/restaurants, train stations, etc.

3- Supercharger (fast). Typically at shopping centers, Ampol service stations (they’re rolling these out), sometimes outside car dealerships or select major shops, and often in touristy towns on the way between major population hubs. These can charge up to 80% in 15 minutes.

How much does it cost to charge?

At home, a full charge would cost around $15 at current WA power prices., equal to about $60 for the same km in a small petrol car.

As mentioned, with solar the cost will end up being near-zero since we can charge during the day when solar is at its peak.

What about public chargers?

There are some free medium/fast public chargers around the place.

I recently tested one out at a nearby shopping center. Went in, did some shopping, had a coffee, came back with an extra 150km in the tank 🙂

Some places charge, so be mindful. I use the PlugShare app to find where they are, and whether they charge (very helpful). And sometimes you need to bring your own “type 2” cable.

Superchargers (in WA at least) often cost about double the rate of home electricity. Apparently, they’re very expensive to install so it makes sense they’d want to earn their money back. These are best used only on longer road trips when you can’t charge at home, or don’t have time for (or access to) a free public one.

In all likelihood, there’s no need to use a supercharger other than that. Most EV owners simply find a home charging routine that works for them and then never have to think about it.

Currently, we’ve just been charging overnight once a week or so.

Most state governments are promoting electric vehicles by offering subsidies or rebates for new EVs purchased.

There are certain price limits and caps that apply, so google it for your own state to see what the rules are. Or see a list of incentives here.

In WA, the current rebate is $3,500 for the first 10,000 vehicles with a value of up to $70,000 or less.

Do I need to tell you that it’s a terrible idea to buy a $60,000 car just to get a few thousand dollars back? I hope not!

People can be quite irrational when it comes to grants, rebates, bonuses, tax savings, and other forms of seemingly ‘free money’. But not you though, right?!

The idea of a car ‘lease’ is ridiculous to me for most situations. But novated leases are different, where you can buy the car outright at the end of your lease based on its depreciated value.

There are tax advantages to getting an EV through a novated lease. If your employer offers salary packaging, you’re able to make the payments using before-tax money. Depending on your tax rate, this can be a significant saving.

But there’s a catch. The novated lease companies charge you an interest rate in the background, which is built into the payments. This trips up many people who don’t run the numbers and just get excited about the tax savings (see previous point!).

We looked at novated lease, but it didn’t make sense in our situation. Mrs SMA’s job offers salary packaging. But her tax bracket is too low for the savings to add up.

If you go this route, be sure to triple check the total payments (including the final payout figure) to find out how much it’s really going to cost.

Beware, the NL companies are very sneaky with their marketing and make it look like an incredible deal. The reality is far less rosy. And be sure to get a few quotes, because prices can vary quite a bit between different novated lease providers.

Probably not.

If you’re still working towards financial independence, it likely only makes sense in a few cases:

— You already have an expensive vehicle, you drive a lot, and are looking at a simple switch. This way no ‘extra’ cash will be tipped into vehicle ownership.

— Your finances are going so well that you’re looking at upgrading your car, you want an EV, and you don’t care about the extra cost or foregone investment gains.

— You simply can’t resist buying one and it’s going to be your one and only major splurge along the way. You also accept it may not ‘save’ you money and delays your freedom.

— You’re on a high tax bracket, can access a decent novated lease, and drive a lot so the fuel and maintenance savings add up a fair bit.

Just to be clear, If I was still on the path to FI, I definitely would not buy an EV (or a new car of any kind). I’d be ploughing everything into investments or smashing a mortgage.

But that’s me. Others take a more relaxed approach, and if they’re happy with the tradeoffs, that’s perfectly fine. This blog has always been about making clear and deliberate choices based on your priorities, as explained in the below posts.

— If the FIRE Journey Is Making You Miserable, You’re Doing It Wrong

— How to Beat FOMO and Create Your Own Path to Wealth

This post wasn’t to brag or encourage you to buy an EV. It’s simply to share what I’m doing, the thinking behind it, how the numbers work, and answer all the questions I’ve been getting.

This purchase seems to contradict my message of shunning consumerism, investing, and using money wisely. But those things are all in the context of wealth creation.

After you’ve built some wealth, you can focus a little less on wealth creation, and a little more on wealth enjoyment.

It’s also worth remembering something else…

If you engage in big spending consumer behaviour first, you’ll never have wealth. But if you build wealth first, you can also spend more later.

Not only do you get the life-changing benefits of having savings and assets, but you can also indulge in what I call CUPs (Completely Unnecessary Purchases).

To be perfectly frank, at a certain point, you can live however the hell you like. Eat fast food and sit around playing video games, I don’t care. You’ve earned the right to do whatever you want.

But I have a feeling you won’t want to do that. Life is far more satisfying spent in other ways. And after years of sensible spending, you’ll still manage your money wisely while also being sure to enjoy yourself along the way.

Thanks for reading!

Here are some resources you may find useful on your wealth building journey:

My book: After 5 years and hundreds of articles and podcasts, I’ve now distilled everything down into an easy to follow book. Designed as a complete roadmap to achieving financial independence and retiring early in Australia. Available in paperback, ebook, and audio.

Mortgage broker: My personal broker of 10 years is More Than Mortgages. If you’d like help refinancing or getting the right loan for your needs, get in touch with MTM. They have fantastic reviews for a reason. I’ve worked with them for 10 years and they’ve been excellent.

Sharesight: A great portfolio tracking tool for share investors, and free for up to 10 holdings. It tracks all dividends, franking credits and capital gains, which is incredibly helpful at tax time. Saves me a lot of time and headache!

Just so you know, if you choose to use these resources, this blog may receive a financial benefit at no extra cost to you. Thanks in advance if you do. And to be clear, I only ever recommend things I use myself and genuinely believe in.

Learn how our EV performed on our recent roadtrip and holiday in Southwest WA. What I learned from the experience, plus lots of pictures, recommended places to eat, and more 😉

The numbers behind our recent solar installation and how much we’ll save. A breakdown of solar FAQ, whether it’s a good investment and what to watch out for.

Get my latest content and thoughts straight to your inbox.

A fresh dose of financial motivation to power your journey.

What timing 😂 I also just bought a new Tesla Model 3. Took delivery a few weeks ago 😍. I went full upgraded LR model though so my OOP cost was a lot higher than yours. And sadly there are no EV rebates anymore in Victoria. But it’s already making me savings compared to my old petrol car so I’m good with it!

Congratulations, I’m sure you’re enjoying it just as much as I am 🙂

Great breakdown as always Dave. Thanks for sharing your perspective on this. CUPs is such a great acronym for these types of purchases – and precisely why it’s so satisfying when you can comfortably afford it. 😅

Cheers Kris! Haha absolutely, glad you like the CUPs concept.

I am not convinced on EVs. To me, it is like a battery surrounded by wheels and a steel cage with seats. Like batteries on phones and laptops, the battery will die over a few years, meaning the charge will not last long. This means that the EV cannot last ten years and will need replacement once the battery goes. I am waiting for better battery technology or some other form of power source to come along before ditching my 15 year old petrol toyota.

Fair enough Ken. For what it’s worth, stats are showing Tesla batteries to still be showing on average 85-90% capacity even after about 10+ years and many hundreds of thousands of km on the clock. So that argument simply isn’t reality. I think they’re holding up a lot better than many assume. And I’m no expert, but the battery tech in these vehicles is quite different from a phone battery.

Hi Dave, thanks for the sharing!

By the way I don’t think your “home charger figures are correct.

The “home charger” in single phase mode charges at 1.8KWh (230v x 8A) or 2.6KWh (230v x 12A (15A wall plug)).

The new Tesla model 3 consumes about 130Wh/km

So it’s more like 14km per hour for the 8a and 20km per hour for the 12a.

https://ev-database.org/car/1991/Tesla-Model-3

We too have invested for the future and purchased a Tesla but we were able to purchase a less than 3 year old Long Range for about 55% of the new price with 68k km.

We would not get the QLD EV $6000 rebate for the LR anyway as it’s over the the $68K limit and we were keen on the LR 4wd because of a steep driveway as well as the performance! 😉

We do have a 8KW solar array in QLD so plenty of power to charge it for free during the day as well as most shopping centres provide free charging.

We are paying just over $600 a year for the LR in QLD with Australia Post insurance, about the same as my old van!

Both solar and an EV have made major savings in our regular household costs and the Tesla is just the best car to drive!

Nice setup, and sounds like you got a good deal on the LR.

Interesting, is that for third party insurance?

It says on that linked page, Type 2 chargers (wall charger) take 6 hours to charge, which is roughly in line with what I said. I’ve been able to add about 60-70km or so charge per hour which again lines up with this. We have three phase power so I would guess that makes a difference with the speed? So home switchboard would perhaps be the limiting factor here, even if the charger + car are able to charge at said speeds. I’ll update the post to be more clear.

Hi Dave

The insurance is comprehensive.

Australia Post Insurance (QBE)

Agreed value: $60,930

Full glass no excess cover

Excess $1800

Annual Premium: $598.46

Might have been a Dec 2023 special to get more customers.

Yes the “home charger” three phase 11kWh max is about 84km hour max, more than most people will need.

Teslas are limited to 11kW AC because they need to convert to DC for the battery.

Wow that’s unreal insurance! Thanks for the clarification re power, I’m not the brightest spark with the technicals 😉

I would definitely be considering a hard-wired 7kw charger for home if it was me. To many stories around the stock GPO connections failing when you are using often and under max load.

7kw is around 30-40km per hour charge I believe

Nice.

My wife is an accountant, agrees that lease isn’t really worth it these days.

Can’t beat a good car owned outright and held onto in good condition for as many years as you can.

Absolutely, buy-and-hold for the long term 🙂

Hi Dave,

Great article. Thank you.

My wife and I are considering an EV. Keen for any tips and things to watch for when working out novated leasing costs. We understand the NL firms paint a pretty picture.

The NL companies will push “look how much tax you’re saving” and give you their own comparison, which is garbage. Just look at the total expected of pocket costs over 5 years (or whatever period you choose), compared to your current net pay. Then add the payout figure. Then compare to paying cash if that’s your alternative (remembering to include what returns that cash could’ve earned).

Novated lease will likely work out better than getting a car loan (even a green loan), which is obviously not recommended. Just go over the numbers a few times, because it’s deliberately confusing.

Great article Dave. Don’t forget to mention the ATO have brought a new rule in which states you pay zero FBT on EVs – https://www.ato.gov.au/businesses-and-organisations/hiring-and-paying-your-workers/fringe-benefits-tax/types-of-fringe-benefits/fbt-on-cars-other-vehicles-parking-and-tolls/electric-cars-exemption?=Redirected_URL – this is a great benefit to people who own companies as well and want to save tax.

Thanks Glenn. Yeah I saw that, but as it’s all rolled into the novated lease payments, I didn’t bother mentioning. But you’re right to point it out as some readers may be looking at purchasing a car with their company, where this benefit applies even without using a novated lease. Appreciate the tip!

I find the entire Novated Leasing industry full of inflated prices and fancy marketing. Tax payers subsidies the whole industry and the highly mark up all expenses and loan rates. Years ago I asked if I can do a Novated lease with my own finance and they say no! 🙂

I agree. As we were getting the ‘quotes’ I was just imagining how many people are going to just look at the “$X tax saved” and ignore everything else. But then again, those people are the most likely to have just got a car loan anyway. Still, the marketing and often misleading numbers were annoying to sift through.

I also recently bought a Tesla which made no sense in my spreadsheet analysis (no matter how I hard I tried). This article could not have been more relevant to me at this point and seems to articulate my own thoughts. Well done.

Haha, it’s hard to get the numbers to line up when making such a big purchase that’s for sure 😉

Hey Dave, it’s Wes here. We met at one of the meetups before (the guy with the white dog ha!). Excellent article and I agree with everything that you have said!.

Just letting you know that there’s always the option to go the EV plan on Synergy ($5c per kwh during off peak), making the charging even cheaper! But obviously, it depends on your personal circumstances whether its worth going for it (its a lot more expensive from 3-9pm). Having said all that, solar might offset everything and you might charge the car for free from now on!

Ah yes I remember you!

Good point on Synergy plans (here in WA for others wondering). I did look at that briefly but since we’re getting solar I didn’t crunch the numbers on that, but could definitely work out in certain cases. Good reminder!

Hi Dave

Great article, I have been bold and just bought a second hand MG ZS ev.

The Chinese EVs have crazy depreciation. I got a 2021 MG ZS. I picked it up for $25k. It had 28,000kms on the clock and the owner wanted something new with more range. I get around 220kms per charge.

Many will think this is nuts to buy used but the MG came with a 7 year warranty which covers the battery to 160K or 7 years. Note older models only had 5 years. The balance I got as used buyer. So in Feb this year, I paid $25k for an Ev with 4 years of warrany left. It is not as nice as the telsa for sure but if you are on the road to fire, consider the poor mans chinese EVs. You may find the sums work like I did.

I am a tight wad and the sums were just to good to pass up

Thanks for sharing your experience. Wow I didn’t realise the MG’s had lower range like that. They are a lot cheaper so that’d make sense. And to be fair, that’s perfectly sufficient for a lot of people (including us!).

Nicely done, hope you’re enjoying it! There’s always a way to get similar benefits for a lower price, just like everything else.

Thanks for the article Dave. I’m sure my next car will be an EV but for the moment I can’t justify it to myself even on a “splurge” basis (and I’m not adverse to the odd splurge).

My thinking is that as I’m on a legacy FiT of 44c for my solar until 2028 and there are no longevity issues with my current car, it makes the most sense to keep getting as much of that high FiT as I can until I lose it. When that time comes, EVs are likely to be better and cheaper and I can pair one with a home battery array.

Yep that makes sense to me Steve, sounds optimal 🙂 (FIT = feed in tariff for those wondering)

It would be useful if you used some figures to back up your comments of novated leasing. The FBT concession makes it very compelling.

I appreciate your partner may be on a low tax bracket, but for anyone on the top bracket it is a no brainer (even with the high interest rates).

I could but the quotes + comparisons are all quite convoluted and complicated, plus this post was long enough. People need to do their own research, as it’s not a yes/no discussion. It can work out in many cases, which is why I said: “Depending on your tax rate, this can be a significant saving.”

But I’ve also read from a few ppl on Reddit that the deals simply aren’t as good as they used to be in the NL space due to the high demand. I’d still say triple check the numbers because what they’ll tell you is often misleading.

I’m also surprised you did not go with the NL option. I’m doing a similar calculation and taking into account the investment opportunity cost of the $60k to buy the car out right. The NL option comes out on top at the highest marginal tax rate. The FBT concession definitely makes NL a very attractive option for EVs.

It’s not surprising when you consider my partner’s part-time income is like 40-45k. On the top tax rate I have no doubt it would come out ahead! If that was our situation it’s very likely we would’ve gone with that.

Why do people assume opportunity cost only goes one way? You can lose in an investment, too. True story – I sold some of my shares to buy myself a new toy car. The shares that I sold slid to about 50% of the value I sold them for and then were subject to a takeover, meaning even if I held onto my shares, I would have lost. Depreciation on the car? Lol! I bought a used Porsche sports car. It’s actually gone up in value in the second hand market! Crazy, but true.

It’s a fair point to make Chris, even if those are outlier cases. Just for clarity, when I think about opportunity cost I’m talking about basically an index fund forever type holding period, same for the car, where those types of exceptions aren’t really plausible.

Congratulations on your new purchase – Hope you enjoy your new well deserved toy.

Thanks Robert!