“Stage 3 tax cuts!”

You’d have to be living under a rock to not have heard about it.

The media has been having a field day with the pros and cons of the upcoming changes, with various talking heads giving their opinions.

It’s received a lot of attention. And fair enough I suppose, given there’s a lot of tax dollars at play.

The recent amendments to the initial proposed changes have heated the discussion further, and (annoyingly) forced me to re-write some of this article!

Honestly, I’m not interested in debating the merits of it, which you would’ve heard endlessly about by now. Instead, let’s just make sense of the tax cuts and flesh out what it all means.

Who will it affect most, and by how much? How does it affect your goal of FI? For those already retired, how will it impact you?

Alright, let me give you the simplified version.

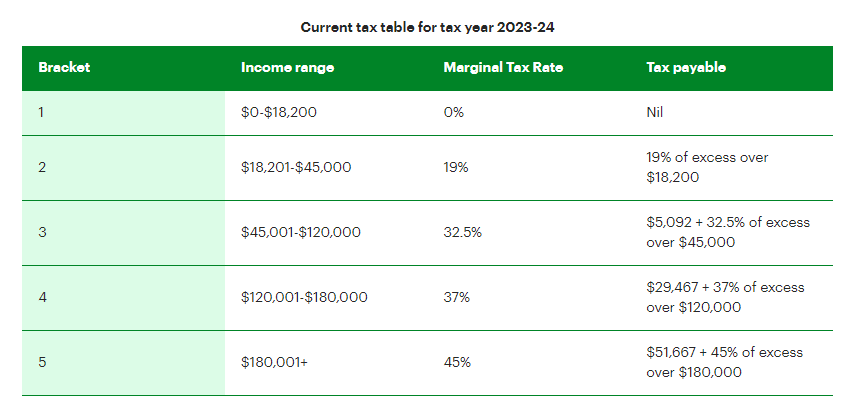

Our current tax rates look like this:

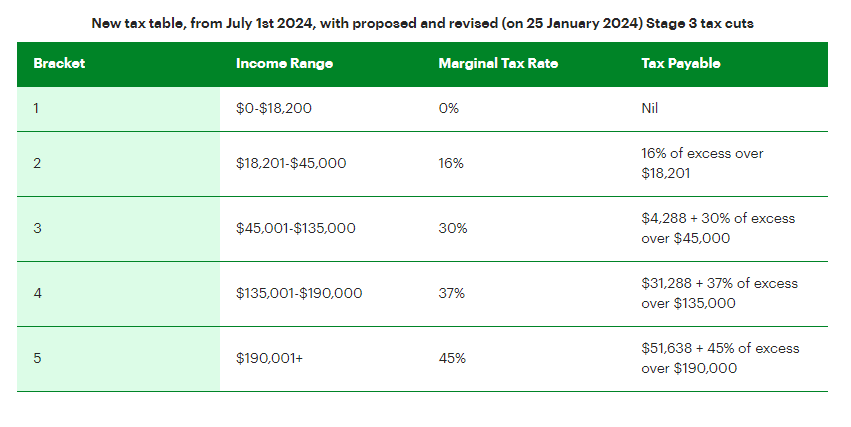

But now the government is dropping the 19c tax rate to 16c, the 32.5c rate to 30c, and widening some brackets a little bit.

The new tax rates for 2024-25 will look like this… unless it changes again 😉

These changes will come into effect in July 1, to begin the financial year.

Now, this doesn’t simplify the tax brackets as was originally proposed. But it does undo some ‘bracket creep’ that has occurred over the years.

For those unaware, bracket creep is where our incomes grow over time but the tax brackets stay the same. This results in a higher percentage of pay lost to tax over time, as society moves up the income scale.

It probably makes sense to automatically index the tax brackets to inflation, but you can see why the government doesn’t do that. Sneakily and quietly taking more tax without doing it overtly… then they get to look generous by offering tax cuts. A stoke of evil genius when you think about it 😉

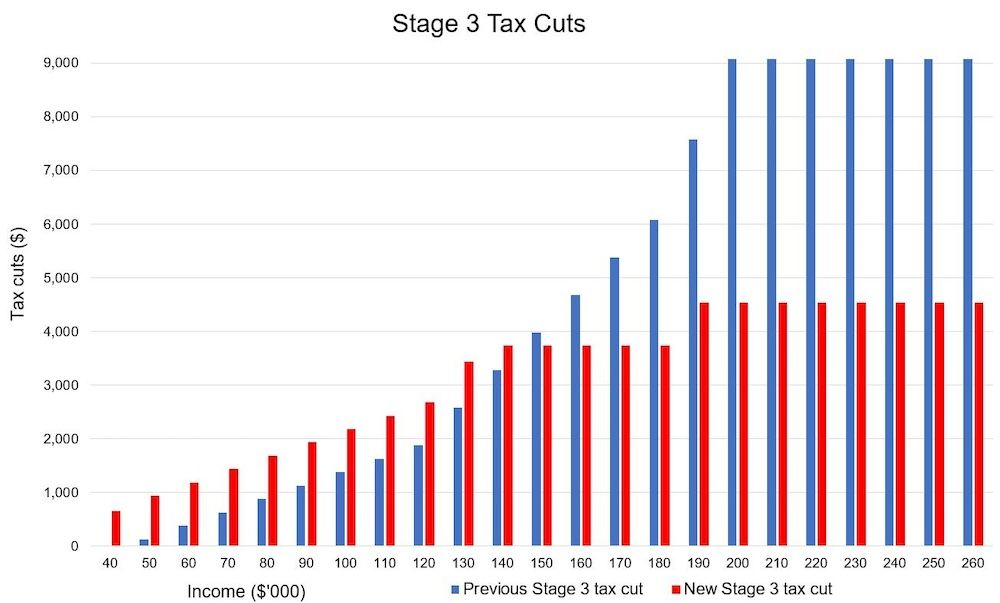

Because it saves me a bunch of time (and frankly, I dislike fluffing around with tables), here’s a nice table made by Pete Wargent. It’s the clearest one I’ve seen. Have a look at the income scale to see how it’ll impact you…

The main differences between the initial proposal and the new amended tax rates are the shifting of benefits from higher income earners to lower earners.

Basically, lower and middle income earners will take home an extra $1,000 to $3,000 in most cases. While higher earners will have their taxes reduced by about $4,500.

The median full time worker – a decent proxy for a reader of this blog – will receive about $2,000 extra per year. Like an extra pay rise really.

Now, many will say that’s unfair because people on the lower end should get more dollar-benefit than bigger earners. “People earning high incomes don’t need it.”

That might technically be true. But they’re also the people who pay the vast majority of the income taxes which fund so much of what the government provides in the first place.

Middle earners who’ve worked their way up and now find themselves earning solid incomes are getting frustrated with bracket creep.

What used to be a high income 15 years ago would now be considered a middle income. The tax brackets should move over time to reflect that, so I can see their point in wanting what was promised.

The below is a section I wrote before the amendments. I’ve left it in should you want to know my thoughts on franking credits and a hypothetical 30% tax rate, read on. Otherwise, feel free to skip to the next section 🙂

What does a 30% tax rate mean for dividends and franking?

You might be wondering, if my tax rate is 30% and a fully franked dividend represents 30% tax paid, what does that mean exactly? Does that make franking irrelevant?

No. It’s better than that.

Firstly, remember that franking credits are based on company tax rates. These tax cuts are for personal tax rates only. Under all circumstances (and all franking percentages) you’ll pay less tax overall (yay!).

Currently, anyone paying more than 30% in tax has to pay some out of pocket tax to cover the difference between franking and their personal tax rate (assuming a fully franked dividend).

But with a 30% personal tax rate, franking credits will cover the entirety of the tax owing = no out of pocket tax to pay (yay!).

This also has a nice flow-on effect for people living off their investments. But it’s not just dividends – any sort of investment income will end up getting taxed at a lower rate with these tax bracket changes.

Free Resource: I created a spreadsheet to keep a running estimate of my dividend income and wealth breakdown. I’ve used it for years as a way to help plan my finances and watch my progress over the years. You can get it below.

Here’s a stat that might just blow your mind (I found it very surprising).

If I received $115,000 in fully franked dividends (which comes with about $50,000 of franking credits), my taxable income is $165,000. Using the 2023-24 tax brackets, tax owing would be $50,000, so I’d be left with $115,000 after tax. No out of pocket tax was paid, franking covered it.

Under the initially proposed 2024 -25 income tax changes, tax owing on $165,000 would amount to $41,000, so I’d actually get a $9,000 franking credit refund. Result: $124,000 income after tax, or $9,000 more than before.

Interestingly, the point where franking credits would once again equal the tax owing would be an incredible $250,000. Here’s the math…

Fully franked dividends of $175,000 amount to $250,000 with franking included. Tax owing would be $75,000, same as the franking credits. By the way, I used the 2024 tax calculator on Noel Whittaker’s site and this one from talent.com for the current year’s tax rates. (I’m sure Noel’s calculator will get changed at some point to reflect the amended tax changes so if you’re reading this later it might not show what I’m saying).

Basically, the level of fully franked dividend income achievable before any out of pocket tax is payable increases by about 50%!

Now, that’s not a common situation, but it’s definitely interesting. As a side note, I expect franking credits to be looked at again sometime in the next 5-10 years, along with negative gearing.

There’ll probably be an effort to reign in some of the benefits or increase taxes for those with money and investments. I just think that’s where society is headed next. There’s a shitload of pent up rage against the current state of affairs. Some of it is justified, some is just envy and entitlement.

You can twist and tweak the numbers however you like, using rental income, global shares, whatever. The end result is less tax paid on income generated from any activity.

In terms of your progress to financial independence, these tax cuts are a useful chunk of extra cash.

Not huge, but not nothing either! A middle income couple is looking at $4,000 extra in their pocket, to build their cash buffer, invest, or pay down their mortgage.

Over ten years, that will easily amount to $50,000, a very nice amount indeed!

In any case, I hope that your finances and savings rate is already so sharp that the extra few thousand per year is just a nice bonus, rather than a needle-moving event.

Importantly, from July, you’ll now lose less money to tax as you build up your investments over time. This means you’ll be able to compound your investments and wealth at a slightly faster rate, which is pretty exciting.

Just like fees, a dollar less in taxes is a dollar more to grow and compound for you. Now, I’m not a tax optimiser like some out there, but it’s worth keeping in mind and appreciating the positive slant these changes can have on your wealth.

The tax bracket changes may also change how couples want to allocate investments between each spouse. There may now be slightly wider gap between spouses than before.

I’m not the biggest fan of tinkering with this kind of stuff, having done it in the past. Situations change over the years, sometimes by a lot. So what’s ‘optimal’ today can change in 5 years. And when you leave full-time work it will be different again. I’d rather keep it simple.

That said, if your circumstances seem predictable for the next 10+ years, then sure, optimising can makes sense. OK, what about those who are about to retire or already living off their wealth?

The new tax brackets mean a higher level of Aussie dividend income can be earned in retirement before out of pocket tax will be payable.

And even if you aren’t in the tax free zone, any franking credits received will stretch a bit further than before.

Of course, it will also result in greater franking credit refunds in some cases. There’ll be more franking credits ‘left over’ depending on one’s income, so tax time may get a little juicier for some of you 🙂

For moderately wealthy retirees or semi-retired Aussies living on $40,000-$100,000 from investments and/or part time income, there is a modest benefit from the tax cuts.

I’m sure we’re all pleased about the changes overall. It means a little more spending money or cushion in the early retirement plans.

The 2024-25 tax changes won’t have a huge effect on most people, whether working or retired. But it does result in extra cashflow and undo some of the bracket creep which has occurred over time.

Overall, I think lower tax rates on personal income are a good thing. We probably should find other ways to generate taxes which don’t disincentivise career ambition and ladder-climbing.

One way is to tax consumption more. Another is to tax assets (or inheritances) more. I don’t have a strong view either way (I just roll with the punches), but I think targeting the wealthy will be the FAR more popular option!

The idea will be to make the ‘wealthy’ pay more tax, as they often make their money in ways other than personal income. Defining ‘wealthy’ and types of wealth to tax is another ongoing debate!

Of course, we should also look at how those tax dollars can be better spent – I have no doubt there’s a lot of room for improvement.

If you’ve read my blog for a while, you’ll know I’m more interested in working with the rules we have, rather than debating what they should be.

Basically, vote for what you believe in, but don’t let external factors eat at your mental state.

What I do feel strongly about is the fact that you’re far better off focusing your time, energy and attention on ways you can improve your own situation rather than hoping for the rules to change.

You also feel a lot happier, more at peace, more motivated and more empowered when you’re proactively making your own life better.

After all, there’s a shitload of ways you can improve your situation by many, many multiples of these tax benefits if you haven’t done so already.

And if you have, then any tax savings are more like a tasty dessert after dinner, rather than your main source of nourishment.

Thanks for reading!

Here are some resources you may find useful on your wealth building journey:

My book: After 5 years and hundreds of articles and podcasts, I’ve now distilled everything down into an easy to follow book. Designed as a complete roadmap to achieving financial independence and retiring early in Australia. Available in paperback, ebook, and audio.

Mortgage broker: My personal broker of 10 years is More Than Mortgages. If you’d like help refinancing or getting the right loan for your needs, get in touch with MTM. They have fantastic reviews for a reason. I’ve worked with them for 10 years and they’ve been excellent.

Sharesight: A great portfolio tracking tool for share investors, and free for up to 10 holdings. It tracks all dividends, franking credits and capital gains, which is incredibly helpful at tax time. Saves me a lot of time and headache!

Just so you know, if you choose to use these resources, this blog may receive a financial benefit at no extra cost to you. Thanks in advance if you do. And to be clear, I only ever recommend things I use myself and genuinely believe in.

Why deliberate spending is my favourite money management style. What it really means and how you can use it as your situation and priorities change over time.

My thoughts on ‘The Great Taking’. An idea that the masses will lose untold amounts of wealth in the next financial crash, due to a deliberate plan by mysterious figures.

Get my latest content and thoughts straight to your inbox.

A fresh dose of financial motivation to power your journey.

Does the Medicare Levy mean that people in the 30 cent bracket will still pay a (small) amount of net tax on dividend income after franking?

Good question. I’d say yes probably, if income is over $90k per person.

Yes Alex, but low income earners pay no MC levy.

https://www.ato.gov.au/individuals-and-families/medicare-and-private-health-insurance/medicare-levy/medicare-levy-reduction/medicare-levy-reduction-for-low-income-earners

Thanks for this one. I have been interested in this topic for a while now.

It’s certainly been spoken about a lot in recent months!

Including 2% Medicare levy, you will be able to earn about $140K in fully franked dividends and pay no tax ie. 140K dividends + $60K franking credits = $200K taxable income. Tax on $200K = $59774 – $60000 franking credit = $226 tax refund!

love this dave. thanks for the rundown!

nic

As you point out, the stage 2 revised tax cuts effectively ensure that individuals who dividend income exclusively will be tax neutral on amounts up to $175k. However, I cannot imagine many middle class Australians earn $175k in dividends. The other side of the story does not get as much coverage: that is, investors who rely on negative gearing tax concessions to augment their return lose every time the personal tax rates are cut. Governments of all persuasions have worked out that the way to make negative gearing less appealing to middle class Australians is to simply lower personal taxes. The percentage of middle class Australians who own multiple investment properties on a negatively geared basis has been rising for years. Stage 3 tax cuts will further erode the perceived value of negative gearing. As a public relations exercise, easier for Governments to sell a tax cut than abolishing a tax concession.

Great point Steve. Love the explanation.

Good point Steve, any tax deductions are now slightly less impactful at lower tax rates. I would say that the actual focus was the tax cut, and that the negative gearing dilution is just a happy side effect for govt.

Thanks for the breakdown! That helped !

No problem Rahul, thanks for reading.

Hi Dave.. Good morning.. I believe you are the right person for me to ask this. What are your thoughts on using super to buy investment property/shares. There are people urging me to do this. I have 120K worth in super and my husband has 140K.

Is there a tax accountant/financial advisor who understands FIRE concept that you can suggest? II live in regional Victoria.

Thankyou in advance.

I would be very careful about using super to buy property. A lot of people have vested interests pushing that idea, including advisors/accountants/buyer’s agents etc. Loans are more expensive for SMSF, leverage is less, and tax benefits are lower. So I probably wouldn’t bother with it honestly. Super already will compound effortlessly over time without adding more costs and complications to it.

As for shares, your super is likely already invested in shares. Check your fund’s details to find out what it’s invested in. You may wish to increase the exposure to shares inside super if you want to invest more aggressively for long term gains (10-20 years).