With the new year racing along, let’s take a step back for a moment.

As I’ve done for the last few years, I’m about to share how much we spent in 2023.

The aim behind this is to illustrate that a happy existence doesn’t have to cost a ton of money.

“$100k is barely making a living”

“Family scrapes by on $250k”

“(Insert ridiculous media story or statement here)”

The idea of life being expensive is so pervasive that it’s widely accepted as an unavoidable reality. But as most of you realise by now, that’s just not true.

We get to decide our own lifestyles and make our own decisions. ALL of them. Where we live, how we live, and what we do.

Anyway, let me share one example of a non-extravagant life, which doesn’t cost six figures. And yet, somehow we haven’t yet died from misery, resorted to eating roadkill or camping at the local park to keep costs down.

Lots of pictures too, so let’s get into it!

Before we get into the numbers, some context…

— We’re a semi-retired couple, who left our full-time jobs after becoming financially independent back in 2017. Up until a few months ago, we had a lovely dog, but no other dependents.

— In early 2022, we purchased an old house in Perth to live in and have since been renovating it (with some more works still to do).

— We enjoy our free time, lead a very comfortable yet relatively simple life. We like spending time in nature, going out for coffee, and catching up with friends.

— Mrs SMA works 2 days per week in government admin. I do writing stuff from home, like this blog, my book, and investing articles over at Pearler.

— We’re not really into fancy stuff. We buy whatever we need and anything else that seems worthwhile, without following any kind of budget.

Okay, with all that said, let’s get into the numbers.

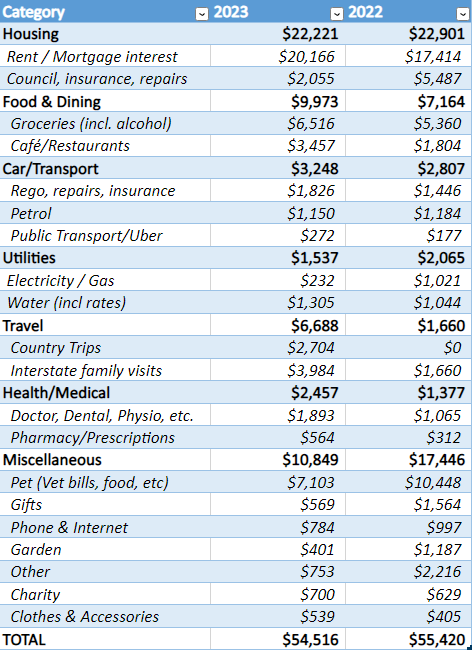

In our previous spending report, I revealed that our total for 2022 was $55,420. So how did we go in 2023?

OK, there’s a lot to go through there!

Even though the surface leave number is basically the same, there was quite a bit of fluctuation among the individual categories.

The mortgage figure is simply interest, so you could add another $8k or so for principal payments. That puts the out of pocket total closer to seventy five grand! So much for frugality, haha!

There’s some debate about whether to count principal an expense or a saving. In reality, it’s both. That money doesn’t disappear like an expense. But it also must be paid from cashflow. Those dollars simply morph from cash/savings to become home equity.

So you’ll have to choose your own method of measurement.

In addition to the above, we also spent $12k on home works as we continue to update our 50 year old house. In 2023, this meant a new front fence and big gate, and got the brick exterior repainted.

The old fence had huge cracks in multiple places with a tree about to push it over.

Now let’s get into some comments and explanations around specific categories to give you a better understanding of what’s going on.

Housing: Interest rates up from last year (full year effect hasn’t kicked in yet), but random repairs/maintenance costs down. By the way, this interest is all tax deductible as our home loan is now effectively an investment loan as outlined here. We debt recycled the whole lot!

Food & Dining: Grocery costs are up a fair bit. We didn’t really do anything to combat this lol. Plus, we deliberately went out to eat more this year, and have been going out for coffee dates twice a week. Since we no longer have the dog, we don’t feel the same desire to stay home as much. There’s also spare time and what I’ll call an ‘enjoyment gap’ where he used to be

Transport: Car costs up a bit. Mrs SMA hit a curb so we needed a new tyre and a wheel alignment. If you follow me on socials, you’ll know that we’re about to collect a brand new Tesla Model 3. In fact, we may be getting it as you read this! I’ll write a post soon, but basically it’s just a gigantic splurge or retirement reward since things are going well financially.

Medical: Mrs SMA got a special heart stress test as recommended by a cardiologist due to having a higher than normal calcium score (artery related). It’s deemed to be genetic related so she’s on some specific cholesterol management tablets.

Utilities: Super low since we’ve still been using our electricity credit provided by WA government. Funny story, we actually had 3 power accounts in our name when the first round of credits were applied (rental, recent home purchase, IP being sold), so we totally lucked out there. When we closed the other accounts, they simply brought it across to our current one 🙂

Travel: Up quite a bit! Mrs SMA visited her family in Darwin three times last year, and I went to Victoria. This year we’ll be travelling together, so costs may go up. We also stayed in a fancy hotel in the city (Westin) for a few nights over the Christmas period. We hadn’t been to a hotel in over a decade (since we got the dog), so it was a really nice treat! We got a room with ‘club lounge’ access which includes drinks and food, plus we had buffet breakfast and ate wayy too much (well I did anyway!).

Miscellaneous: Pet bills were very high again as our dog was battling cancer before he passed away. The ‘gifts’ category is getting mixed up with ‘family trip’ spending since Mrs SMA tends to combine both and I can’t be bothered trying to figure out which was which 😂 Our hotel stay was kind of a gift to ourselves but I put this in travel… not really sure where it should go honestly! The ‘other’ category is often household items, random online purchases, getting cash out, and stuff that doesn’t really have a home.

If you have any questions about the categories or what we buy/don’t buy, feel free to ask.

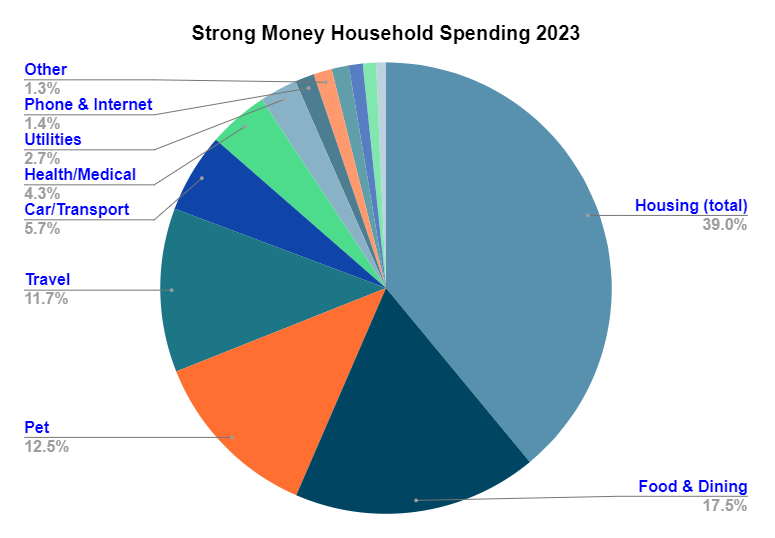

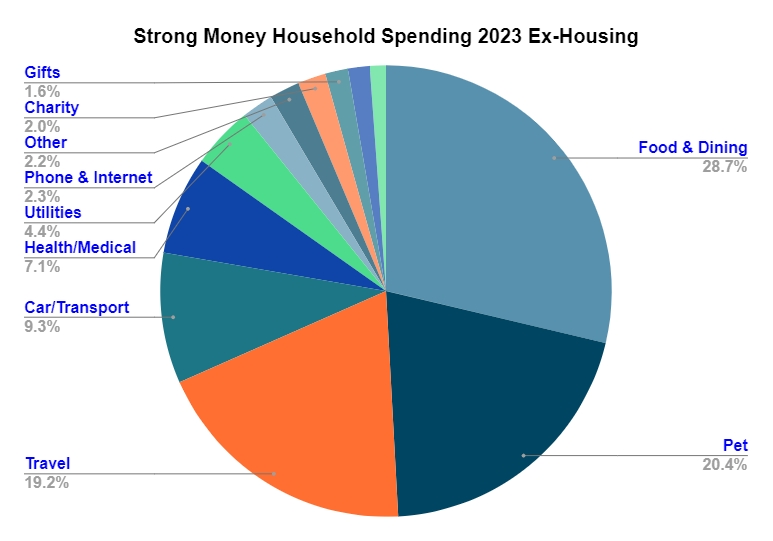

There it is broken down about as good as you can get it.

Outside of housing and our dog, we only spent about $25k for the two of us. And sure, we didn’t go on any international trips, but it’s not like we stayed home and did nothing.

It felt like a very free-spending year. Although when you don’t follow a budget, most years feel like that!

In fact, we’ve been deliberately engaging in what you could call lifestyle inflation. The idea being, our investments are going well (wealth effect in action), and our part-time incomes provide a generous surplus.

Importantly, I don’t deem any of this spending as crucial for my happiness. We could (and did) live very happily on less than what we spend now.

But at some point you just start doing whatever you feel like. Not like a child grabbing shit off every shelf. Like a mature adult who rationally acknowledges everything is fine and you can comfortably afford it.

As I’ve said before, you don’t want to get stuck in the mental trap I call relentless saver syndrome which seems to be common among FI people, even as their wealth compounds.

So I like to enjoy both frugality and a little bit of luxury so I can appreciate both. This gives you a full spectrum of experience and makes your life a little bit richer. Necessary? No. Interesting and enjoyable? Yes.

Our hotel stay…

Spending some time in Yanchep National Park…

Going out for quite a few coffees…

Hanging out with my boy…

And of course, continuing to help the local turtles, protecting their nests in our yard and releasing the hatchlings…

Lots more I could show you but that’ll do!

There’s more on my socials if you’re interested in random pictures and thoughts.

This wasn’t meant to be a ‘year in review’ type post, but it turned out a little bit that way didn’t it?

I may do another one of those soon since many of you seem to enjoy hearing about my early retirement activities. The last lifestyle post was Notes From The Other Side back in October.

A few predictions for 2024…

— Mortgage interest will probably be up

— Car costs will probably go up (won’t sell our old car straight away)… not to mention the $60k+ purchase itself 😅

— Electricity costs will definitely go up (no more credits)

— Travel costs will probably go up as we now travel together

— Pet bills will now be very low (but not zero), as we have a couple of re-homed chickens (silkies)

— Getting solar panels installed and other house works done

All in all it looks like our spending will be even higher in 2024!

I don’t want you to get the wrong idea here. This is not how much our life needs to cost AKA the cost of living. It’s the cost of all of our current decisions, which are all made in the context of our situation.

As I said in the post What If I Woke Up Broke, if we didn’t have freedom, there’s zero chance I’d be spending this much. The priorities would be different.

Most of these spending choices aren’t permanent ongoing costs (like the car and house works). And the other stuff could be unwound at a moment’s notice, which is pretty cool. I like maintaining a mindset of flexibility and adaptability.

Alright, time for a confession…

I’m actually getting a little sick of tracking our spending these days. I find the activity to be a little tedious and find myself delaying it longer and longer

I’m mostly just doing it for the sake of this blog, since I can keep a pretty accurate running estimate in my mind with less effort.

Maybe I’m just getting lazier (likely). But it could also be the fact that nailing down our exact expenses no longer matters very much.

Eventually you realise your default setting is to be relatively sensible. Meaning you’re just not going to start spraying money across every category, all the time, forever.

As I posted on Twitter recently:

There’s something magical about running your finances in such a way that there’s always a surplus. You end up with permanent peace of mind that you’ll always have enough.

Anyway, that’s how we spent our money in 2023. What about you? Have you found some new ways to save in 2024? Or maybe you engaged in some lifestyle inflation like us? 😄

Thanks for reading!

Here are some resources you may find useful on your wealth building journey:

My book: After 5 years and hundreds of articles and podcasts, I’ve now distilled everything down into an easy to follow book. Designed as a complete roadmap to achieving financial independence and retiring early in Australia. Available in paperback, ebook, and audio.

Mortgage broker: My personal broker of 10 years is More Than Mortgages. If you’d like help refinancing or getting the right loan for your needs, get in touch with MTM. They have fantastic reviews for a reason. I’ve worked with them for 10 years and they’ve been excellent.

Sharesight: A great portfolio tracking tool for share investors, and free for up to 10 holdings. It tracks all dividends, franking credits and capital gains, which is incredibly helpful at tax time. Saves me a lot of time and headache!

Just so you know, if you choose to use these resources, this blog may receive a financial benefit at no extra cost to you. Thanks in advance if you do. And to be clear, I only ever recommend things I use myself and genuinely believe in.

Why deliberate spending is my favourite money management style. What it really means and how you can use it as your situation and priorities change over time.

My thoughts on ‘The Great Taking’. An idea that the masses will lose untold amounts of wealth in the next financial crash, due to a deliberate plan by mysterious figures.

Get my latest content and thoughts straight to your inbox.

A fresh dose of financial motivation to power your journey.

I haven’t (yet) totted up what my 2023 spend was, probably because I know it’ll be an exxy year. A 5 week holiday in England + Ireland; plantation shutters for the whole house; painting the house interiors: buying quite a bit of new furniture… the list goes on.

Still, most of those are ‘one-off’ expenses.

That’s what I tell myself, anyway!

This year? Alaska/Canada… plus I’m wondering if I should go on another trip as well…? I’m gaining to read 135 books this year, which is 5 more than 2023.

Financial Independence isn’t too bad.

Thanks Dave really find your thoughts and information helpful.

Glad to hear it Jamie, thanks for reading.

Loved this Dave, thank you for sharing this I find it really insightful and helpful to frame our ongoing spending.

I’m sorry to hear about your dog, I follow this blog very closely but missed his passing x

Happy it helps! And thanks 🙂

Did your passive income cover these costs?

I think our share dividends for the year were about 50k, so not quite. The rest of our money is tied up in property which we’ll be selling over the next few years to complete the share portfolio. I explain roughly how our cash management works here: https://strongmoneyaustralia.com/how-we-manage-our-money-each-month-explained/

Hey Dave,

Since you have debt recycled the entire mortgage, does that mean if you were to sell the house you wouldn’t have to pay any of it to the loan, since the loan is now tied to the shares?

So sorry to hear about your dog, they are such an integral part of the family.

regards

Sam

Cheers Sam.

Once you sell a property, you typically have to repay the entire mortgage before you receive the proceeds. The debt isn’t ‘tied’ to the shares, the loan is still attached to our home. It’s just that we used that debt to then invest elsewhere.

Hi Dave, Sorry to hear about your dog passing, Props to you for taking good care of your dog, we have a rescue German Shepherd that was in poor condition health wise when we first acquired him and cost us same for year and only good dog owners understand how expensive Vets bills are and not to mention the ongoing medication costs.

My Daughter has a new Tesla model 3 so I’ll be interested to see how you go with it, she has mixed opinions at this stage.

All the best for 2024.

PS…we like our coffees to but go easy on those cream donuts or you might be spending more on Cholesterol tablets too….😉

Cheers

Mark

Thanks for outlining these costs Dave, it’s very useful. Wondering how you’re keeping the council and insurance costs so low for your house? Council rates and insurances have skyrocketed here in NSW. Yours seem very reasonable!

Cheers – Nyomie

Council rates are quite low in my area as the suburb is not very fancy at all. I think about $1500 or so. Insurance is about $500 I think, it’s with Budget Direct and I chose the highest excess (6k or so) which makes a big difference, since I only really want it for huge problems (fire etc).

Hi Dave, I’m a big fan of yours mate. Your book is the best Aussie FIRE book by a country mile! Thank you for sharing your actual numbers, it is really illuminating to see your yearly spending.

One thing that really caught my eye is your total grocery spending. That is really incredible especially considering it is for two people👍

Thanks very much!

Yeah a lot of people seem impressed with the groceries. A few things which probably help: we aren’t large people (55-65kg), we eat vegan mostly + we don’t really buy ‘treats’ or small portioned random packaged stuff which seems to add up a lot. I wrote a bit about it here: https://strongmoneyaustralia.com/frugality-and-food-the-grocery-strategy/

It’s interesting to compare your spending to ours Dave. Despite the different household size and stage of life our overall spending is actually pretty similar, but there are some areas like personal and health insurance where we are spending huge amounts of money compared to yourself, and then others where we’re not spending anything like the amount you are like mortgage/rent or pets and travel.

That’s what’s cool about seeing people’s personal finances – it’s often a good reflection of what each person finds valuable. And it also morphs and changes quite a bit over time which is also interesting. Hope you’re doing well mate!

Hi Dave,

Great update and thanks again for a peek behind the curtain. I have been grappling with the idea of early retirement and maybe it’s just fear, but I’m finding it difficult to make the final leap due to the society we live in. None of us live in a vacuum and while as individuals, we can choose to remove ourselves from the rat race, most won’t and will continue to push for more, more, more.

The very fact that the vast majority of our peers will always push for more means that we as an individual can get caught out and left behind in a way. Once you remove yourself from the crap – that’s it – you have a finite source of money and that’s it. I don’t know, maybe I’m overthinking this, but I’m really lacking the social proof. My job puts me in contact with literally thousands of people all over the country and I’ve never met an individual retire before 55. Not a single one.

Curious to get your thoughts on the above?

Also, RIP Boss.

Cheers mate.

You’re right, it’s definitely fear. I think we’ve spoken about this before. You need to remove your own measurements from that of those around you. What somebody else does, and their own benchmark of success, why the hell does that matter to you?

You’re also assuming there’s no way to make money after leaving a job. Come on, you know that’s complete nonsense. It’s fear creating all these limitations and ‘problems’ in your mind, but if you sat down and addressed them one by one, and all the counteracting points, you would see you have nothing to worry about. The main thing is this: deciding what you want your life to be like, and then doing that. Instead of looking around at how other people are living theirs. But that’s not easy, it requires some soul searching and the bravery to figure it out.

Nobody retires because everyone thinks in the same limited way. Barely anybody knew about this stuff until 10-15 years ago, but those who’ve stayed at work the last 30 years simply can’t imagine it. Their minds and spirits have been dampened so much they cannot conceive of another way of living. So they stick with the same old, despite many being able to afford to do whatever they want, partly because they don’t see anyone else doing it. More fear again, and watching everyone else, rather than independently deciding what they really want. I genuinely find it sad to see.

Will you die one day with the regret of what you could have done with those extra 10-15 years you worked when you didn’t have to? Or would you regret leaving work, trying a whole bunch of things with your time, and then maybe going back to work in some capacity because it’s not for you (which you can still do anyway with the first option)? Those ‘risks’ look very lopsided to me.

Hi Dave,

I am impressed. What are your secrets to spending so little for groceries. A bit more than $60 per person per week. I am scratching my head in disblief. I have been trying to get our grocery bill down for a while shopping at Aldi, going to the local fruit and veg stores etc. But I am not getting below $200 for the both of us per week. 🤔 what are your secrets? Any tips? Cheers Seb

Hey Sebby, I wrote an article about groceries a while back which you can find here: https://strongmoneyaustralia.com/frugality-and-food-the-grocery-strategy/

That should give you quite a few ideas. A few other points which may not be obvious: we aren’t big people, at 55-65kg, so that would have an impact. But in short, a lot of it comes down to questioning each item, avoiding packaged junk/snacks/treats, and figuring out a way to get the same item/meal/taste for less, using cheaper ingredients if possible. We also don’t really eat meat, so that would have a fairly sizeable impact too.