Many readers are well aware of the opportunity in front of us to reach FIRE (Financial Independence/Retire Early).

Hell, some of you are already there!

But maybe you’re new here. Maybe you’ve had a poke around, read my own journey to Financial Independence, checked out some saving or investing articles and decided, “OK, this is definitely for me, but where do I start?”

Or perhaps you’re sold on the idea, but the whole thing just confuses your spouse. Maybe they think it’s weird (or impossible) to save so much, or they dismiss the idea of never having to work again.

Well, today’s post is all about creating that starting point. That meeting ground if you will. So let’s lay the foundation of why and how we can jump on this FIRE train, take that journey together, and hop off at Freedomtown.

If you’re curious about this stuff, you probably already get this bit.

But the main reason to aim for Financial Independence is to get your life back. Here’s what I mean…

We spend a very large portion of our lives consumed by work. All day. All week. Almost all year.

And this goes on for a good 40-50 years.

Now, it wouldn’t be so bad if we all happen to drop into satisfying work that means something to us, with great conditions and co-workers, ample downtime to recharge and spend time on other things.

But for most of us, it’s just not like that. Even so, there’s much more to life than work, as this interesting article correctly concludes.

Thinking back to my late teens and early twenties, I noticed that, for the most part, work was something that people endured, not enjoyed. The need to make money to pay bills came before everything else.

And since we give up so much of our life and our energy for it, I struggled to accept that. In fact, I couldn’t. So I decided there had to be another way.

And lo and behold, there is! (if you’re keen, you can read my entire journey here or listen to my podcast with Aussie Firebug here)

The solution is to create your own freedom. You’ll do this by sensible living, saving and building wealth. Your freedom will be fully funded by creating an investment income stream.

And by doing this, you remove the power that money has over you, for the rest of your life.

You can still work, and you probably will. But it’ll be work that’s important to you. Work with meaning. Work that you want to get out of bed for. And work that is worth trading some of your precious time on this earth for!

Along my journey, I learned a lot and made a few mistakes too. But reaching FIRE has been the best thing I’ve ever done.

So to help spread the joy, I’ve broken down each important step into a simple plan, which you can read with your spouse, or pass on to a friend.

Forget everything else for a minute. Think about your life. Not your current life, but your life as a whole. From start to finish.

What do you want your life to be about?

How do you want to live?

How much time do you want to spend at work? And what type of work would you love to do, if you didn’t need the money?

What hobbies would you take up?

How much time would you dedicate to your health? What about being outside and doing physical activities?

Where does your family life fit in? Do you want to fit them in around work? Or would you rather place work after family time?

Spend time mapping out what your ideal life looks like for you. There’s no right answer. Whatever you feel is the most satisfying balance for your situation. You can always adjust it later, because we all learn as we go.

Hopefully you’ve just realised all the things you’d rather be doing other than working all the time. This is your motivation.

And if you’re still not sure, here’s a list of top 5 regrets people have at the end of their life. Wishing they worked more is not one of them!

Intuitively, we know this is true. The only difference is, some people take action and change their lives, but sadly, many don’t.

Hopefully you’re part of the first group. So let’s continue…

Take stock of your finances as they are today. Firstly, your net worth.

Add up your assets. Subtract any debt you owe. That’s your current net worth.

Don’t worry about what it is. The fact that you’re doing this means your future is brighter than your past.

I’ll even let you include car values in that calculation, provided you’re open to selling and switching to a more reasonable car choice to create some cash.

Next is your cashflow.

Write down your current household income, after tax. That’s pretty easy. Now the hard part. Figure out where it all goes!

The best way to do this is by checking over your bank transactions over the last few months, and guesstimating for the rest of the year.

You’ll soon have a good estimate of your household spending, and you can start tracking it from today. Here’s ours for comparison.

Or if you want to make it a little more fun and convenient, try the TrackMySpend app from MoneySmart.

The difference between your household income and your spending, is your savings rate. This number is very important. In fact, where early retirement is concerned, it’s the number one factor to focus on.

Basically, the higher your savings rate, the sooner you’ll reach FIRE!

Next, get a simple and possibly even automated savings habit in place. You can start small and build it up over time.

Whenever you get paid, setup an automatic transfer to divert some of your income to another account.

Think of your savings as non-negotiable payments into your freedom fund.

Your first job is to build yourself a cash cushion of at least $10,000-$20,000. Or whatever you’re comfortable with.

This will see you never have to go into debt for life’s little problems that crop up. Broken fridge. Vet bills. Car repairs (or replacement). Whatever it is, your cash cushion means you no longer have to worry.

If you’ve never experienced this, a cash cushion helps you sleep like a baby!

Even this basic level of financial strength makes life sweeter and your stress levels reduce dramatically. Financial security gives people a feeling of greater control over their lives, resulting in a boost to happiness.

As you start saving, look for ways to increase your income. You can do this by:

— Working more hours,

— Switching to a better-paying employer.

— Switching to a better-paying industry.

— Negotiating a wage increase based on performance.

— Learning more valuable skills.

If you combine a couple of these, you’re looking at tens of thousands of dollars more hitting your bank account every year. Precious cash you can start piling up for the next step.

Once your cash cushion is built, it’s time for the fun part! Putting your money to work – also known as building wealth.

— The highest return will come from paying off any high interest debts you have. This includes credit cards, personal loans and car loans. Interest rates here are often well over 10% per annum, which is very destructive to your wealth.

As for things like Afterpay – just get rid of that nonsense and pay for things like a grown up. Because you’re better than that now! You’re not a broke millennial!

— Next, get comfortable with the sharemarket. I know, easier said than done. I used to think it was a casino too. But then I learned some important lessons, from some very knowledgeable people. So if I can do it, anyone can.

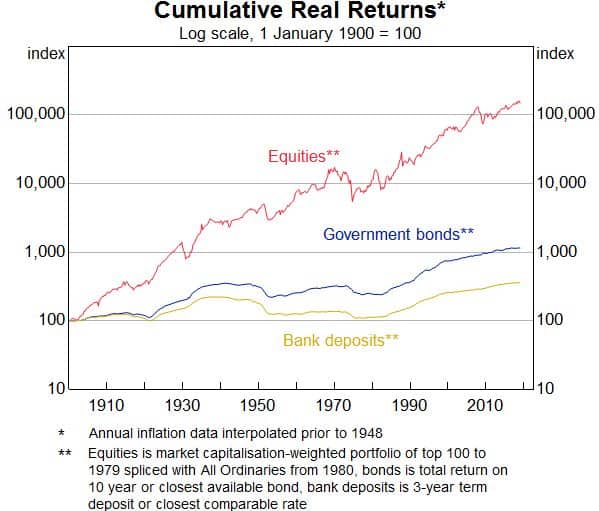

If you think the sharemarket is unpredictable and unreliable, look at this chart from the RBA (Reserve Bank of Australia)…

These are real returns, meaning after inflation. Australian shares have produced fantastic returns over the last few generations, producing a return of over 1,000 times your money in real terms.

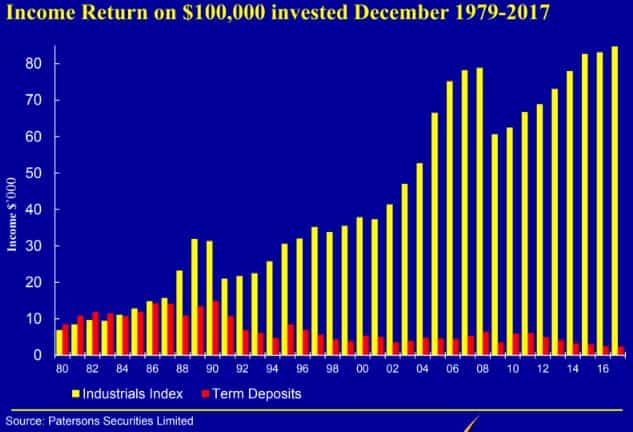

And in terms of income, it’s probably the best known cashflow generator available to investors. Here are the dividends paid from Australian shares since 1979, excluding resources (courtesy of Peter Thornhill).

No income has been reinvested. This is one purchase of $100,000 over almost 40 years. Just like the other graph, not a perfectly straight line, but a very predictable trend over time.

Looks pretty reliable to me!

We’re simply banking on the economy continuing to grow and Australian companies making more money over the long term. Betting against that hasn’t made much sense in the past and I don’t think it makes any sense now.

So benefit by becoming an owner of Australian business to get your share of the future profits and dividends!

— After learning about investing, choose your investments. You can see how I approach this here, here and here.

Because of our focus on easy passive income, most of our cash goes into a couple of low cost index funds. This offers us diversification and dividend income while keeping things relatively simple.

— Next, open an online brokerage account. I use Pearler because it’s low cost, designed for long term investing and has none of the other nonsense other trading-focused brokers have.

— Now start diverting some of your paycheck to your brokerage account automatically. Then, purchase your chosen investments every month or two, with a minimum of $1,000. Regular investing builds momentum and keeps your motivation high. Don’t worry about what the market is doing, just invest.

— You can reinvest your dividends for maximum automation. Set this up automatically by simply filling out the paperwork you get in the mail after buying your first parcel of shares.

— Use Sharesight to record your share purchases. This will keep track of all your dividend payments and franking credits for tax time. It’s completely free up to 10 holdings, sign up here (full disclosure: if you choose a paid plan, this blog receives a commission at no extra cost to you).

Now you’ve gotten started and are making progress, it’s time for the next phase.

Head back to your list of yearly expenses, and find a way to optimise every single one of them. Sure, it sounds as delicious as a Brussels sprout smoothie, but this is where the big progress is made.

Do it right, and you’ll bring your freedom forward by years! That was certainly true for us, and I bet it’ll be true for you.

For every $10 per week you spend, you need more than $10,000 of investments to cover it.

Don’t believe me?

$10 per week is $520 per year. To generate $520 per year in dividend income, you’ll need $13,000 of shares yielding 4%.

So yes, a few dollars here and there makes a difference of many thousands of dollars. Not only that, but lower spending means two things:

–1. You need less in investments to retire, so you can retire sooner.

–2. You now have a higher savings rate, meaning you’ll reach FIRE faster.

Here’s what else you can do…

Read as many peronal finance blogs as you can with a focus on saving. Like Mr Money Mustache for example. Or check out some of my posts on food, cars and insurance.

The factor that changed our thinking was realising how good we have it in modern-day Australia, and realising how little humans need to be happy. This is hard to accept at first but it’s undeniably true.

Further, we now spend more time being productive and less time on mindless consumption, doing activities which are enjoyable yet cost little or nothing – which also ends up being much more satisfying.

For those that think spending less means less happiness, we’re really talking about priorities here.

We’re choosing the wealth of freedom and time, instead of the unfulfilling void of ever higher spending.

At the start, many of us aspire to the wealthy, high-status and spendy lifestyle. But the problem is that luxury and comfort is a poor indicator for happiness and life satisfaction.

By now, you’ve got a solid savings rate and you’re adding money to your investments regularly. And it’s all relatively effortless at this point.

Here, the best use of your time is to learn more about happiness and start slowly building the life you want to live.

Because you’re essentially free anyway, it’s just a matter of time. So you can start thinking like someone who is already Financially Independent.

Start researching any places you want to go. Skills you want to learn. Volunteer work you’re interested in. Or a business you might want to start.

We’ve come full circle now. Back to Step 1 and creating your future life. But now you’re even closer to making it happen.

The only negative stories I’ve heard from people who have retired young and not initially enjoyed it, are those who had zero plans and ended up wasting their days away doing nothing productive, which led them to become depressed for a while.

So begin planning what you’ll do from your position of Financial Independence. How will you live your best life doing things that are important to you?

And a few years down the track you’ll reach FIRE! There’s little left to do now but enjoy your life and new adventures. But don’t forget to…

Share your newfound life philosophy with your friends and family. Bring them along for the ride as you improve your lives together.

But watch their disbelief as you explain you only need to work and save solidly for 10 or 15 years to fund a lifetime of freedom.

And if they don’t believe you?

Well, show them. Be the example that it’s possible. Teach others how it works, and be someone they can look up to and come to for help.

For now you can interact with the other great like-minded folks who visit Strong Money and the many other Financial Independence blogs around the place.

Really, you can do this anytime. But due to the likely scepticism, you’ll probably have a bit more sway with some people when you actually quit your job 😉

Like many good questions, it depends.

The basic goal here is to save and invest enough that your annual dividend income is higher than your spending.

Will a high income help? Sure. But only if you save it.

Is it necessary? No. Our own incomes were around the Australian median full-time wage.

Will being ultra frugal help? Yes.

Is it necessary? No. Provided you have a decent income and sensible living expenses, you should be able to save a healthy amount, without dumpster diving for dinner.

You get to decide on the right balance for you. But it’s very likely that most people can live happily on far less than they think.

Bringing this back to one factor that determines the outcome, it’s your savings rate. Want to speed up your FIRE journey? Simple. Just work out how to boost your savings rate. One little bit at a time.

This elegantly simple calculator will answer that.

Simply plug in your after-tax income, annual spending and how much your portfolio is going to spit out each year in retirement.

Play around with it and you’ll see for yourself how small changes in savings rate make a big difference in freedom!

Don’t get distracted by other ways to get rich. Often there’s can be a real urge to chase higher investment returns or other ways to speed up the process, like using leverage.

I know, because I felt it too. But the investment world is funny – especially the sharemarket. Larger amounts of effort and analysis doesn’t mean larger returns. Actually, the opposite is usually true!

So keep it simple and focus on what you can control. Keeping your living costs under control and sending your money off to work for you.

Your shares immediately start returning cash to you in the form of dividends, which you can use to buy more shares.

This income stream multiplies itself over time because you’re constantly adding new money to the pile. And that results in ever increasing dividends which you can use to grow your portfolio further.

It’s like a snowball rolling down a mountain, gaining momentum.

Sure, it starts off as a few tiny flakes. But those bring more flakes and it turns into a ball, which starts getting bigger. Eventually, the ball grows so large it’s an unstoppable force.

But instead of snow, it’s your investment income!

Firstly, what we’re really talking about here is building a strong financial foundation to live the best life you can. After that, whatever you do is completely optional.

And that’s the point – the choice.

You can work as much or as little as you want. Have as much family time as you want. As much busyness as you want.

Instead of being forced into an inflexible and demanding routine, with high stress and little free time, just because there’s bills to pay. Quite simply, it’s another way to live. And in my opinion, a better way to live.

You can choose more interesting work, with people you like and hours that suit you. You no longer have to put up with any office politics, or management bullshit.

But it’s not about doing nothing. It’s about having control over what you do.

So even if you continue working the same hours in the same job (unlikely) because you’d do it for free, you’ll do it with a strong sense of freedom. Because every day you wake up and go to work, you know that it’s completely optional, and you’re choosing it because it’s what brings you satisfaction.

All the while, having the financial backing to step away at any time you like, if you no longer enjoy it or you decide something else is more important.

It’s the ability to live free from the worry and restrictions that go hand-in-hand with money problems and mandatory full-time work.

What a great feeling to have!

Hopefully this post serves as a useful starting point for both newbies and spouses. And it brings those who ‘get it’ and those who ‘don’t get it’, closer together.

The concept of FIRE is simple enough. But given people generally find it hard to think long term and easily succumb to peer pressure, accomplishing this goal is not as easy as it seems.

Reaching Financial Independence takes patience. It takes dedication. And it takes discipline.

But in my view, it’s the ultimate life goal, and the best thing I’ve ever done. The feeling of freedom is hard to describe. Actually, 2 5 years in and it still feels like a dream.

I’ll leave you with one last comment, which I feel sums up what money itself is all about. And I feel like I’ve heard this before, but I’m not sure where, so I’m sorry to whoever I’m borrowing this from.

Those little chunks of money you have, in your wallet, in your bank, in your investment account – they’re not money at all. They’re little freedom tokens, which you can keep and redeem at any point in the future.

By spending all your tokens, you’re left with zero future freedom. But start building them up, and eventually, you’ll have enough freedom tokens to last the rest of your life.

Thanks for reading!

Here are some resources you may find useful on your wealth building journey:

My book: After 5 years and hundreds of articles and podcasts, I’ve now distilled everything down into an easy to follow book. Designed as a complete roadmap to achieving financial independence and retiring early in Australia. Available in paperback, ebook, and audio.

Mortgage broker: My personal broker of 10 years is More Than Mortgages. If you’d like help refinancing or getting the right loan for your needs, get in touch with MTM. They have fantastic reviews for a reason. I’ve worked with them for 10 years and they’ve been excellent.

Sharesight: A great portfolio tracking tool for share investors, and free for up to 10 holdings. It tracks all dividends, franking credits and capital gains, which is incredibly helpful at tax time. Saves me a lot of time and headache!

Just so you know, if you choose to use these resources, this blog may receive a financial benefit at no extra cost to you. Thanks in advance if you do. And to be clear, I only ever recommend things I use myself and genuinely believe in.

Why deliberate spending is my favourite money management style. What it really means and how you can use it as your situation and priorities change over time.

My thoughts on ‘The Great Taking’. An idea that the masses will lose untold amounts of wealth in the next financial crash, due to a deliberate plan by mysterious figures.

Get my latest content and thoughts straight to your inbox.

A fresh dose of financial motivation to power your journey.

This is great Dave. I really enjoyed this article as it puts everything into perspective. The goal for us to reach FIRE but to not necessarily retire per say and sit on the beach drinking cocktails all day – I think we’d get bored! We just want the option to not have to work if we don’t have to. We love our jobs and are lucky that we work in a profession where we will always have work and will always be able to contribute to the profession. Ideally, I’d love to be spending all my days cycling and drinking coffee like a true MAMIL, however, the reality is that I actually do enjoy my chosen profession. FIRE for me looks completely different. At the age of 34 now, it means being able to work a few days a week if I choose to at 45, and then settling into MAMIL life on my bike and cycling around a few days a week too! We’ve also discussed volunteering and being able to give back to the community. We now just follow our strategy to a tee and smile looking at the spreadsheet we’ve created that details our growing stream of income from our investment LIC choices like ARGO and AFIC. I guess it is all about defining what FIRE looks like to you and what will bring you the most happiness if/when you do reach financial independence.

Also, if anyone else needs a SelfWealth referral to get 5 x free trades then my link is below. With a small family on the way we could use the free trades that we’d get as much as you could use the 5 x free trades that you’d get too!

https://secure.selfwealth.com.au/Registration/Plan/5/yG5oL

Great stuff Chris!

Haha I just learned a new acrynym (MAMIL), never heard that one before lol.

Your FIRE plan sounds like a good one – that’s the best part, we can tailor it exactly to fit our own needs. Look forward to hearing about your progress over the years 🙂

Great introductory post for people who are new to the concept Dave.

Any thoughts on people getting personal insurance in place particularly if they’re just starting on their journey? I wrote about it a while back https://aussiehifire.com/2018/10/02/fire-and-personal-insurance/ but I seem to recall you were less positive, although you’re at a very different point in your FIRE journey so it makes more sense from where you are.

Cheers mate.

Insurance is pretty personal, so other than my article about it, which details what I think has value, I have no specific advice. Hard to have blanket advice for that stuff. I still think much of it is unnecessary once people have a strong savings rate and some money behind them. Risk tolerances will differ though.

That interesting article you linked to was a fascinating read – I thought it was only disgruntled and dissatisfied individuals that pursued this freedom from work in full or in part. I didn’t realise that even the big thinkers like John Maynard Keynes predicted a 15-hour workweek in the 21st century!

I guess the moral of your story is you can choose your own future – not hope for someone else to change what the world considers ‘standard’…

Well said Frankie – I believe that forecast was based on increasing productivity and wages allowing us to only require a few days work to cover our expenses, which turned out to be absolutely correct. But what they failed to foresee was the rampant growth in consumerism and how we simply decided to use our increased wages to spend more, rather than work less.

And that’s basically what this all comes down to – realising how much real income we actually earn compared to history and that we can either choose to spend it all or use a good portion of it to create freedom for ourselves.

The timing of this post was perfect. Really useful to be able to share with people you want to bring on the FIRE journey with you or encourage to consider the path!

Thanks Jo, glad it’s helpful!

Great post! Often the first step is the hardest, but once you’re on the road you start enjoying the journey.

I was inspired in part by my father-in-law who retired at the age of 45. He’s 81 now, and spends his days with his grandkids, working on pet projects, and goes fishing. He’s never bored, and he reckons he’s one of the busiest retirees he knows!

The ability to choose how you spend your time without being dictated by necessity is one of the best types of freedom. I hope we’ll get there one day!

Wow that’s an incredible story – awesome stuff! Probably the best role model you could possibly ask for!

Stick to the path and you’ll get there 🙂

Excellent and very easy to read introduction to FIRE! I’m still not convinced dividends and the ASX returned those real results. If I look at real returns since 2008 (when I was meant to invest) I would be down still according to this graphic: https://topforeignstocks.com/wp-content/uploads/2017/06/All-Ordinaries-Accumulation-Index-returns-from-1900-to-2010.jpg. I chose to ignore the smart advice to invest in the stock market nor Australian property and save in cash to hit LeanFire in 2016. I invested in overseas property in Poland (family ties) instead. My investments there are lower taxes (around 9%) and capital gains (which I don’t count on in the short term) are much higher m, since it is a developing country. I also don’t believe the sharmarket will recover in the next few years due to the immense debt burden Australian has as well as it’s terrible industry diversification and lack of innovation. Just my 5 cents.

Glad you liked the article, thanks!

I totally agree that everyone has to decide for themselves what to invest in and whether it makes sense to them.

Sounds like you think the RBA data is wrong – what do they know, right? 😉

Picking one specific start date at the top of an inflated market peak is misleading for a number of reasons. Firstly that graph only goes to 2012, just a couple years after the crash so that misses 6 full years of returns. The next 6 years (start 2013 to end 2018) shows Australian shares returned 7.9% per annum, according to this interactive Vanguard chart.

Next, nobody invests 100% of their money at the top of the peak and never invests again. In reality if you invested in 2008 and continued to invest (as you would if you were building a portfolio for FI) you’d have achieved very attractive returns, because you’d continue buying each year afterwards and end up buying much more at much lower prices simply through regular purchasing.

In fact, anyone who is investing for FI is likely to achieve close to the long term average returns because of the effect dollar cost averaging has.

Moving the date a couple years earlier or a couple years later shows about average long term returns of 7-9% per annum, which is why the crazy spike in prices distorts the figures. The massive boom before the GFC where share prices, company profits and dividends were growing at 10-20% was simply not sustainable. So we have an inevitable correction and revert back to the long term trend again.

The chart you highlight again shows the relentless trend of real returns of 5-6% per annum over more than 100 years. Despite the booms and busts, the economy continues to grow and company profits continue to increase. If people want to invest in Polish property rather than dividend paying shares, then that’s fine with me.

Dave, Thanks for your detailed reply. I do think trusting RBA data fully is not the greatest idea, yes. I even question the Central Banking System‘s value.

In the same years you mentioned after the GFC bust we had inflation going even as high as over 4% so real rerurns were quite poor. The Aussie dollar tanked after the mining boom in addition. Both of these ‚things’ are meant to be carefully balanced and managed by the RBA. The RBA is in part responsible for the housing boom and ongoing crash by flooding the market with cheap money and turning a blind eye to its consequence. In global comparison Aussies lost a ton and will loose even more. It is hard to notice if you don’t travel internationally, or understand monetary policy and history.

You mentioned to look at the long term Trend and I fully agree with you here. Over the long term Australian Shares are doing worse. Returns are getting smaller, busts are getting bigger and taking longer to recover, real returns are getting smaller.

Your graph shows that it took 1900-1970ish to grow the index 100x but in the next 50‘ish years the value grew only about 10x. If I look at the last ten or so years since the crisis, it hasn’t even doubled – far from it. The trend is clear to me. Just like the hyper indebted housing market the indebted corporate sector will yield less and less is my view.

It is not about time in the market, it‘s about timing market and asset class cycles (also to comment on Michael‘s reply. That is what differentiates top investors from the average Joe. Looks at the famous ones: Dalio, Beffet, etc. They periodically rebalance portfolio and asset classes because they understand asset class cycles.

I‘m not saying everybody should invest in Polish Realestate. Rather I’m suggesting there is better and safer options out there for most people if they look a little harder on how to invest there hard earned dollars. I for one prefer to be in control of my savings, rather then releasing control over them and betting on a diminuishing long term trend associated with a currency not backed by any collateral. If you ask me it is way too much risk for a real 2-3% return.

Hmm okay. I’m no Central Bank Conspiracy Theorist, so I won’t go into that.

You still seem fixated on the peak of the boom for some reason, not sure why. Choosing the peak of the boom is about as fair as me choosing the bottom of the crash, which I haven’t done. If I did, it would show something like 12% returns including franking credits. But I didn’t use that, because that’s misleading (just like your cherry-picked date) when thinking about LONG term returns which is what we’re all focused on here.

The Aussie dollar dropping isn’t a bad thing for our economy – it helps it to rebalance and boost certain industries. It’s one of the reasons we haven’t had a recession in almost 30 years.

The RBA had no choice but to cut rates after the mining boom ended – something had to plug the gap. We’ve had high levels of construction which has helped since but at the same time has fuelled further debt growth which is a concern, though is now reducing (as people switch to P&I mortgages and credit growth slows). Many, many countries are in a similar position of high debt, whether household or government – that’s the outcome (and in a sense, also the cause) of low interest rates.

We’re not in the best position, no, but a lot of countries would kill for our demographics, low govt debt, strong population growth and general stability.

Your own chart shows that real returns have been the highest since 1980 (7.1% pa) versus the longer term figures. I also chose to ignore that in my reply and instead focus on the more conservative lower long term real returns of 5-6%.

And since you point it out, in the last 10 years (Jan 09 – Jan 19) Aus shares have returned 9.1% pa according to the same Vanguard chart from earlier. According to the RBA’s inflation calcluator, inflation has been 2.2% during that time (but we can’t trust them can we?), so real returns have been near on 7%, which would be approximately double. So the statement ‘far from it’ is a bit off.

I’ll leave you to time the market and join the ranks of Buffett and Dalio. Many of us aren’t concerned by real total returns as far as capital growth is concerned (which again is measuring the irrational peak), but rather on whether our investment income increases by inflation over the long term. And following this dividend investing approach, it has thrown off real growing income for many many decades as shown by the dividend chart, and also from looking at the likes of low cost LICs like Milton which has grown its dividend faster than inflation for 60 years.

It’s not magic, and I’m not promising a perfect world of consistently high returns here – companies as a whole generally increase their earnings and dividends a bit ahead of inflation over the long term for many reasons which I’ve gone into previously. And although there is plenty to be negative about globally (and locally), that’s always the case, and the pessimists are proven wrong over time.

By the way, Buffett does not rebalance his portfolio in different asset classes, he simply continues to accumulate ownership of businesses over time (listed and unlisted), and simply makes an effort to buy more when they’re cheaper. Buffett correctly acknowledges he has no idea where the stockmarket is going in the short term, he simply buys companies over time at attractive prices for the underlying earnings stream – capital growth is a sideshow.

At this point it’s pretty clear we have different views and this is quickly becoming a circular conversation, so I think it’s best we agree to disagree and leave it at that 🙂

Thanks, Dave, for another insightful and detailed response. Let’s agree to disagree on our views. Nothing wrong with this. There is opportunity coming from either outcome. With both our varying mindsets we achieved FI in our own ways. Let’s treasure that because it is an amazing thing to achieve. Let’s use it to make this World a better place. I keep following and reading, and I love a good and deep discussion. Thanks for sharing your thoughts.

Following on what Dave has said in his detailed reply, you should check this article out which is my go-to send when people ask the question ‘but if I invested at X time, I’d still be down’: https://www.afr.com/personal-finance/shares/as-a-financial-planner-i-watch-smart-people-repeat-the-same-investing-mistake-20181005-h16976

It’s not timing the market that counts, it’s time IN the market.

Another excellent article Dave. Wish I had read something like this years ago…. Still, better late than never!

Cheers Jeff, at least you’re reading now, and thanks for doing so 🙂

This: “For every $10 per week you spend, you need more than $10,000 of investments to cover it.”

This is paradigm shifting.

Whilst this is nothing new, I have never heard it stated exactly in this way. That is powerful.

Thanks very much Phil!

Definitely sounds like a big deal when we start thinking in those terms, so hopefully it opens a few eyes.

Hands up who wants that daily Starbucks habit now… if you’re saving $20k per year, that’s one more year in the office to pay for it. Forty $10-per-week habits and you’re stuck in the office forever. But for every one you ditch you work one year less.

Paradigm shifting indeed!

I agree. The maths is simple and I could do it in my head. But the fact is, I hadn’t done it. Seeing it written out is a clarify moment.

Thanks Dave.

Always interesting.

Cheers Bradley – glad you found it helpful!

Hi Dave,

Thanks for another wonderful and insightful post. I’ve been reading your blog for years now (as well as a few others) but have yet to actually invest in the share market. I wouldn’t say I’m overly risk averse, more lazy than anything. 2019 is the year though! I think part of the reason why I haven’t gone further is because I don’t know enough about the process of withdrawing funds down the track. What if I want a larger some to invest in property? Are there any great posts or articles you can point me to on the other end of the journey?

Thanks heaps mate.

Thanks for being such a loyal reader Hamish!

Interesting scenario – the process of getting money out is extremely simple. You put in an order to sell as much or as little shares as you want, it gets filled usually within seconds and the funds can be back to your bank account within a couple of days.

If you really want to invest in property later on, I’d say don’t put money into shares that you want to pull out in the next 5 years. The long term returns are fairly reliable but the market can go anywhere in the short term (0-10 years). So with a shorter term focus I’d simply use a high interest savings account, or possibly peer to peer lending, which you’ve probably seen me write about before here. Hope that helps.

Hi Dave, another excellent article. Your blog is definitely a must to read one and once we started reading the blog we can’t leave without spending at least an hour by reading different articles.

Now I have a query, I just a started investing and bought some units of A200. Now I am looking to add another one, bit confused about VTS, VEU or ASIA or even LICs like AFIC,MLT etc.

Any thoughts? Thanks in advance.

I’m really humbled you spend so much time here George, thank you!

Hard question. Given A200 will pretty much give you good exposure to Aussie shares, the question is really do you want to balance that with some overseas exposure? Or are you happy to stay within Oz and buy an LIC for their own attributes? That’s for you to decide.

But from the overseas funds, I’d probably go with VGS instead of VTS/VEU – similar but doesn’t include small caps or emerging markets. Basically it gives good international exposure in one holding, and it’s domiciled in Australia so there are no overseas tax concerns like with the other funds. More info here. But as always take a look for yourself and think about what’s right for you – general thoughts only 🙂

Thanks for the reply Dave. I understand whatever you mention in the blog is just a general views. Nothing specific to anyone except you 🙂

Will definitely consider VGS..!

Hi Dave,

Great article, I’ve just landed on your site and delighted to find Aussie material. I’m a fan of Mr Money Mustache, love his attitude and yours seems to be similar. I sadly am in the very early stages of this plan due to a motorbike accident just under two years ago. At age 52, I want to try to retire slightly earlier! After having a lot of time off with my rehab, I’ve grown to appreciate the freedom not working can give.

At present, I’m all about paying down my last debt, then, I’ll set my next goal. Thanks for the inspiration!!

Kaz

Thanks Kaz, and welcome!

I’m indebted to Mustache – he definitely influenced my decision to retire earlier and with less than many people would think is ‘enough’ and be perfectly comfortable with it. We do share the same attitude on a lot of things, like optimising and deciding to simply make this FI stuff work whatever happens, rather than wanting more and more cushion and security.

Sorry to hear about your accident. At least it’s helped you have a mindset shift, that’s pretty powerful. Congrats on smashing your debt and all the best with your next goals!

Great steps for those getting started and also for those further along who get stuck and need to go back to their why/dream to reconnect.

I love the $10 now = $10,000 needed in investments. I’ll keep that in the back on my mind and may even use it when tempted with going out just one extra time.

Thanks for that Miss B! Haha seems to be a good reminder of seemingly small habits being expensive to cover!

Been getting some questions from readers on how to explain all this FI stuff to friends/spouses so tried to create an all-in-one post to cover it. Doesn’t hurt to have a ‘start here’ type post. Hopefully it’s what they’re looking for 🙂

Hi Dave,

I just wanted to thank you for sharing the Sharesight link. I signed up and it is really good in giving me the overall picture of my portfolio. So easy. Thank you. 🙂

The feelings of being financially free is very important for mental health and clear thinking. When struggling to make ends meet, one becomes tired and stressed and the whole situation then quickly turns into a vicious cycle downhill. I have recently given much thought to choosing a lower paying job over a higher paying one. I’m thinking the lower paying ones usually comes with less stress so less risk of loss of income from quitting due to stress (ie it is more sustainable in the long run). Its a slow burn but it burns much longer, and not as painful. What’s the point of having high income when one is unhappy most of the time? People say money cannot buy time and happiness.

Just like growth stocks over dividend stocks. Howard Coleman from Team Invest warns of growth based on “story” rather than earnings (dividends). Basically those into growth gets pretty much nothing for the period of time invested until they sold and realised the profit (or worse, a loss, and is so often the case with retail investors) and then have to pay a huge chunk to the taxman. He said usually growth is a cover-up for no earnings/money. Otherwise they would have focused on the return side rather than the growth story. So he basically said those people are buying stories rather than real returns. This then leads to the herd mentality and the greater fools scenario. It might be due to ageing but nowadays I weigh everything in terms of risks. Basically the growth strategy is very risky. I can see a similar analogy in my backyard. I can plant a plum tree. It grows and after a long time it starts to produce many many small fruit. I then wait patiently for the fruit to ripen. Everything tends to go very smoothly until ripening time when suddenly a drought or fungus or insect/bird attack could wipe out the whole crop. If nothing happens, they then all ripen at the same time, causing a glut and many go to waste, or forced to give away (like profit to the taxman). Compare that to planting a tree that gives me little but constant supply of fruit throughout the whole year. Much less risky and more efficient.

People also say high risk high return. It reminds me of an incident. During Christmas, my colleague gave me a present. It was a lottery ticket. She spent about $13 on it. She said if I won, I’d be rich, and that one’s got to be in it to win it. I was never a gambler and thought why not just get me a gift card of $10 or even $5. In the end, the lottery ticket ended up in the bin. Didn’t win anything.

Thanks Michael. And no problem – Sharesight is definitely user friendly and makes tax time super easy.

Great thoughts you’ve shared here on a range of topics! Totally agree on the mental aspect of becoming FI. Even just a family being in complete control of their finances, whether high wealth or not – it’s been shown (can’t remember where) that those people are happier overall, so there’s definitely some intangible benefits that go with this whole financial independence game.

Interesting fruit tree analogy. I’m also generally cautious towards investing in high growth scenarios. Some growth is necessary, but high growth isn’t. I usually prefer at least half the total return to come from income.

Appreciate you sharing your thoughts!

The book “The Richest Man in Babylon” by George S Clason lists 7 rules of money. One of the rules is:

“Make of thy dwelling a profitable investment: own your home.”

I “retired early” almost 16 years ago. I could have done so a few years earlier, but one of my priorities before retirement was to own my home. I was brought up with the idea that home ownership is important. Indeed it is in this country; it provides security. In Australia, tenants are not usually given long-term leases, and can be booted out of their home with only 60 days notice. I don’t really want to own a house, but I don’t like the alternative.

Thanks for the comment Rob. Great old book that one! I do think the message about home ownership has gone a bit far in Australia. While it’s great in principle for lifestyle, security etc, all common sense seems to get thrown out the window when discussing it, and home ownership is turned into another purchase for status.

Hi Dave

My next move is investing in ETFs. My worry now is that I am hearing chat in regards to the sharemarket being over valued. Can it really just continue ever higher (albeit with some bumps along the way).

As the market is so uncertain now, would you suggest waiting, or to start dollar cost averaging in from now?

Thank you

These articles might help…

https://strongmoneyaustralia.com/short-termism-and-market-madness/

https://strongmoneyaustralia.com/is-the-sharemarket-dangerously-overvalued/

https://strongmoneyaustralia.com/timing-the-market/

The chatter is endless and things are never certain. But we need to invest anyway.

Hi Dave! I can’t find the Trackmyspend app in Apple store anymore. Are there any other (free) apps to track your expenses that you would recommend? Ideally without too many annoying ads.

Hi Olga. I can’t recommend any spending apps in particular as I don’t use them myself (I just use a very simple spreadsheet with a list of categories which takes all of about 5 minutes a week).

Hi Dave

Just wanted to say thanks for all of your articles. I’ve read several this morning and it’s great for reminding me of what and why I’m doing this. I’ve made all the initial steps – no debt, automated investments in ETFs, bills are optimised and I have a savings rate I’m happy with. However, now I’m a bit bored and completely impatient! Despite all of these good things in place it takes a long while and a lot of patience to get there. Reading this stuff in the meantime helps keep me focused, so thanks again.

Haha sounds like you’re in the boring middle part! I wrote about that with a couple of possible solutions here if you haven’t seen it already: https://strongmoneyaustralia.com/how-to-get-through-the-boring-middle-part-of-the-fi-journey/

Thanks for reading 🙂 Great to hear you’re in a fantastic spot on your personal journey!