Welcome to a new round of Strong Money Q&A!

Think of this like you and me sitting down having a cuppa together and I share my thoughts on a bunch of different questions.

These posts are simply to provide more detail on certain topics where a whole article may not be necessary.

I take it everyone has perfectly optimised their personal finances, because this week we’ve got a bonanza of mostly investing questions! In particular…

Friendly Disclaimer: Remember, nothing on this blog is personal advice. I’m not an expert on tax, investments, or anything really. Please do your own research before making any financial decisions.

Hi Dave.

Just wondering… since LICs and managed funds often list their top 10 or 20 holdings, why not just mimic roughly what they do and directly build up your own share portfolio of 10-20 stocks?

That way you don’t pay any fund manager fees. By doing it yourself and playing more of an active role (assuming you’re sufficiently interested), wouldn’t you make more money?

Hmm, let’s think about this. You could try to replicate what a certain LIC or managed fund does, but it’d be a pretty crappy version of what they’re doing. And it’s more likely to result in lower returns rather than higher returns.

Here’s why: you’ll be much less diversified. And because returns tend to be driven by a small percentage of stocks, owning more companies often leads to a better long run outcome than owning less.

Now you could say, “I’ll just buy the good companies.” The problem is, a company’s quality (good or bad) is usually reflected in its price. So it’s not as simple as: good company = good return.

Plus, we won’t actually know which set of companies end up performing the best until its 2030 and we’re looking back!

There are other problems too. The top holdings of funds can change monthly. So which fund will you choose to follow? How often do you re-balance? What about taxes? What about certain sectors being overweight in the top 10 versus the top 100?

Think of the admin at tax time – more CGT events to fill in every year, dozens of dividend information (versus 1 LIC). Then you’ve got brokerage costs on buying and updating 10-20 holdings. How do you choose which one to buy each month? There’s no easy way to top up all your holdings.

Lastly, the fees on a low cost LIC are so small that all this effort still doesn’t make a whole lot of sense. In fact, it sounds like a nightmare, haha! For your sanity, keep it simple 🙂

I totally agree with your insurance post. However, smaller insurances like contents and car is different from Life, Trauma, and TPD. These are something that financial advisors really emphasise (I’m fully aware of their commissions etc.)

But I hope when you get some free time, you could write a post on these specific insurances.

Those bigger type insurances are different as you say. These are very specific to the individual.

In my mind, there are two good options. One is to hold those insurances inside super to allow maximum savings for investing and retiring early outside super.

The other option is to maintain low expenses and once some personal wealth is established, and ideally you’re financially independent, then you’re no longer reliant on work income etc. So, this becomes your big bucket of insurance in case of illness, disability, or one spouse passes away etc.

Of course, there are also safety nets in place in terms of Medicare and disability benefits. For people who are good at managing their finances, these are a very handy backup plan in themselves. We pay taxes for these things and that’s what they’re there for, as a safety net.

But it really depends on the person/household, their risk tolerance, and how many things they want to cover against. It’s not something I worry about, and while anything can happen, I’m just not interested in paying to insure against such risks. If the worst occurs, we’ll simply draw on our savings as needed.

Hi. My wife and I have a net worth of $800k, which is a combination of Aussie investment properties and super. We’re looking at investing overseas but worried about currency risk. Any info would be great.

Currency risk is a massive topic – hard to distil to a couple of sentences, and not something I know tons about either!

You might have noticed in my post on Dividends and Diversification, we plan to increase our global share investments over time. I could do this in two ways; hedged, or unhedged.

I’m choosing unhedged. This means currency movements will affect my investments. But this is also part of the diversification benefit, as explained in the post.

Choosing ‘hedged’ means your investment remains based in Aussie dollars. This sounds better in some ways. But usually it’s a little more expensive (as currency contracts are used and not free to implement), and is less tax efficient (as sometimes large gains are made on these contracts).

Unless investing a very large percentage of net worth overseas, unhedged tends to be the more diversified option. It’s not something I worry about. When one is investing steadily over time, as markets and currencies both fluctuate, the movements tend to have an averaging effect.

So I plan to keep it simple with unhedged shares given this increases our diversification since our savings are in mostly Aussie assets. That’s my novice opinion on it, but there’s lots of debate and everyone tends to feel different about it.

I’m a sprightly 53, and new to investing (March this year). I’m trying not to flounder in the sea of information surrounding stocks, portfolio management, diversification strategies etc.

All that coupled with the COVID crash has left me with a lot of questions, about how I can position myself as a late-comer, with zero experience of investing, and less time to maximise opportunities, compared to someone in their 20’s.

Interested to hear your thoughts for late investors, and how age vs exposure to risk informs (or should inform) investment decisions.

Quite a big topic you’re talking about! Generally, someone in their 50s who won’t be retiring ‘early’ is better off investing as much as they can into their (low cost) super fund.

In super, investments are taxed at 15% which is less than most people’s personal tax rate. Plus you can get a tax deduction for diverting extra money there too, so it’s really a double-win.

With a timeframe of about 10 years to traditional retirement, I’d probably focus on getting my living expenses down (by paying off the mortgage if applicable), then saving as much as I could over the remaining years by adding to super.

Retiring at 65 can often still mean a good couple of decades worth of spending to cover, so investing in long term risk assets like shares (inside super) still makes sense.

Keep in mind, if you fall short on the savings side, you’ll probably get help from the pension etc. So just do your best, but don’t stress over it. There’s no need to worry about picking stocks or designing a portfolio (your super fund will already have decent diversification). Just focus on the big things I’ve mentioned that will move the needle.

Seeking your wisdom on something and I don’t want to pay an accountant. I own VAS which I’ve purchased for an average price of around $83 per share. (At the time of this email) it’s $70 per share.

I’m thinking of selling it and immediately buying A200 with the proceeds. That way I realise a capital loss that I can one day use to offset a future capital gain, and the keep same exposure to the ASX. I do not think this is against ATO guidelines as VAS and A200 are not the same thing.

The ruling could go either way on this one. Even though these funds are not EXACTLY the same thing, it would be pretty hard to argue that you didn’t just make this transaction for the tax benefit – which tends to be how the ATO would decide whether this is acceptable or not.

There’s no way to be 100% sure until you’re audited or you ring and ask them. But my guess is, this would be frowned upon and not allowed. These two funds are not different enough to justify it, and there’s no other clear reason for doing this except for a tax benefit.

I understand the positives of index investing, but how do I reconcile this with the fact that two thirds of ASX companies doesn’t make a profit or are losing money? We’re also buying that two thirds of the market when investing in the index.

Yes I know the index is weighted according to market capitalisation, but still those companies are a massive drag. I have tried searching for this topic on the internet but found little to no studies on this. Any ideas? Would the ASX200 be better than ASX300 then?

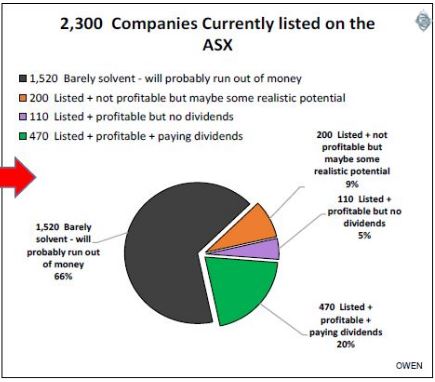

I’m not sure where you got that stat from? Would it be the following pie chart by any chance?

Indeed, this shows that about two-thirds of companies listed on the ASX are ‘barely solvent’ and therefore, are probably pretty crappy investments.

BUT, we’re not investing in the entire pie of 2000 companies (most of which are tiny, speculative and near-broke).

Instead, we’re investing in the largest companies – the ASX 200 or ASX 300 index, nearly all of which are profitable and pay dividends.

On that chart, we’re mostly playing in the green section. We’re not buying the pile of crap at the bottom. So, if someone owns index funds, this chart should be more of a comfort than source of worry.

There is basically zero difference between the 200/300 in terms of return over time, so I wouldn’t overthink that part of the equation.

The main idea behind indexing is that it’s largely unpredictable which companies are going to deliver the huge outsized returns that push the market higher. And where it does seem obvious, it’s usually priced in (see Question #1).

There is no doubt that some of the ASX 300 companies are currently unprofitable. Some will never make a profit and won’t survive. Others will flourish and are simply spending all their cash on expanding (like Amazon did for 10-15 years before making profits).

I have a few questions that I hope you could cover in the next round of Q&As.

1. Is there a general rule of thumb about ratios of ETFs to LICs in a portfolio? Right now I’m about 50/50 and only just started.

2. I’m planning on getting married in 1-2 years and have $15k set aside on top of my emergency fund for those expenses. Thoughts on using some of that money in a P2P lending like RateSetter in the meantime?

1. Definitely no rule of thumb. I know people who invest solely in LICs, and I know others invest solely in ETFs. And I know plenty who invest in both. Choose whichever investments you prefer, just try and make sure they’re diversified and low cost.

2. Smart idea setting those funds aside. Given you’ve only got a short timeframe, a high interest savings or offset account is likely the best home.

You could invest some into Ratesetter in the 1 month market if you wanted to. Unfortunately, they don’t have the 1 year market anymore, which might’ve been a decent fit. It’s not risk-free remember, so don’t use all of it just in case.

I’ve been asked about this recently so it’s worth mentioning here – yes, the $100 Ratesetter signup bonus is still available to readers of this blog who invest in the 3 year market (or longer). More info on peer-to-peer lending and Ratesetter here.

I hope you enjoyed this Q&A session. I’ve got another two posts worth of questions lined up already!

Do you have any thoughts on these topics? Let me know how you’d answer these questions in the comments below!

And if you have a question you’d like me to answer, you can get in touch through my Contact page and I’ll do my best to get back to you. Keep in mind, it’s reached the stage where I can no longer reply to everyone, unfortunately.

Thanks for reading, as always! 😀

Video of the week: To continue today’s investing theme… in a recent podcast episode, Pat and I discuss our favourite aspects of investing in the sharemarket…

Why deliberate spending is my favourite money management style. What it really means and how you can use it as your situation and priorities change over time.

My thoughts on ‘The Great Taking’. An idea that the masses will lose untold amounts of wealth in the next financial crash, due to a deliberate plan by mysterious figures.

Get my latest content and thoughts straight to your inbox.

A fresh dose of financial motivation to power your journey.

With question 5. You could also simply take advantage of dolar cost averaging.

Instead of selling VAS to buy A200. Just buy more of VAS to reduce your cost base and average price.

Yep 100%. Most ppl are continuing to buy anyway so that’s likely to be the case. But it was pretty clear, our reader was really only doing it for the tax perk. And given they’re basically the same exposure, it doesn’t matter which one of those he tops up, his investment would achieve roughly the same exposure and returns over time.

I don’t agree with your question 5 answer – they are different so the ATO won’t mind. The real question is if there is a tax benefit by taking a capital loss now on VAS to offset a gain on A200 in the future. If you think the index will get back to previous levels then so will VAS and you will be back where you started with no loss or gain, whereas by selling and buying the index in a different way that is 2 lots of brokerage and some complication with tax for no difference.

It would only be worth doing if you actually think A200 is going to outperform VAS.

They are not sufficiently different for the ATO to just let it go. They are both broad based market cap weighted Aussie index funds, with near identical holdings. The only reason it is being done is for a tax benefit, and that is generally how they decide whether something is acceptable or not.

“In 2008, the Australian Tax Office (ATO) issued issued tax ruling TR 2008/1, which specifically outlaws arrangements where “…in substance there is no significant change in the taxpayer’s economic exposure to, or interest in, the asset…”

…This is known as a “wash sale” and the ATO will disallow the loss if the sole intention of the sale was to minimise tax. https://www.sharesight.com/blog/tax-loss-selling-for-australian-investors/

Totally with your answer for that person in their 50s. I’d imagine they’d feel so behind and could beat themselves up for not knowing about FI sooner. Pay down the mortgage, and take advantage of Super. It’s situations like those that makes you think how advantages it is to live in Australia!

Or read Nick Bruinings book Don’t Panic, combine around $280k in Super WITH the pension system and get $48k a year tax free.

If you can’t smash the super before you retire, then play the two systems together, there is a horrible horrible area I super between around $320k to $800k where you actually get penalised with the pension… aim high or aim low with your super but don’t be in the grey area.

> If you can’t smash the super before you retire, then play the two systems together, there is a horrible horrible area I super between around $320k to $800k where you actually get penalised with the pension… aim high or aim low with your super but don’t be in the grey area.

Actually I’m not sure that logic makes sense. For example, if you end up with $500k in super, surely you can just spend $180k over a couple years on extravagant living, and then you are back to the $320k sweet spot. That would be better off in my estimation.

Hi Leigh, yes that would be the go – but make sure your at that point close to 67 to get the full pension 🙂 after all paid enough tax into the system, time to get something out 😉

I began investing at 50, just after I paid off my house.

I think your advice to ‘sprightly 53’ is spot on.

Excellent, thanks for you feedback! It’s sometimes hard to know what I’d do in a similar situation. I can only imagine what that position is like, and there are a lot of factors at play.

Question 4 – sprightly 53 – totally agree with your answer. It is really hard to ignore the tax benefits of super, especially when preservation age is not that far away. I started in late 40s and want to retire at 55 so must have a bridge-the-gap fund from 55 to 60 which means investing outside of super. Otherwise, I would be happy just investing inside super.

Some people rely on growing their super balance then using a portion of that to pay off their mortgage at retirement. I’m more risk averse than that and prefer to pay off my mortgage without using super as super is subjected to share market returns. But, it really depends on your risk tolerance profile.

To the poster of Q5… why crystallise the loss now to offset against a Future CGT event that hasn’t happened yet? hold for now… VAS May well recover, you’ll get dividends in the meantime… use the loss when you need it not in case of…

Just my thoughts

Mark

Hi Dave

I have been reading your stuff for years now and find it inspirational. I am curious about your answer to Q5 though. I have received alternative advice, that VAS and A200 are completely different companies. I was advised that VAS holds 300 different companies, 100 more than A200, so it a completely different investment, regardless of whether they share common holdings.