WANT MORE PRACTICAL NO BS FINANCE CONTENT EVERY WEEK?

Join thousands of readers and subscribe to the Strong Money Newsletter below.

A while ago, I posted the following on my socials…

I thought this was a fairly mild and straightforward statement. But as it turns out, several people strongly disagreed with it.

Not only that, but they couldn’t even fathom how it could possibly be true.

Now, I’ll probably still write a fully updated Rent vs Buy post soon. But since my comment prompted such a mixed response, I thought it was worth unpacking.

If your initial reaction is, “Dave, how the hell can you say renting is more predictable for your finances?” then trust me, you’re not alone! But stick with me while I explain why it’s an accurate statement.

As you know, any discussion around property quickly becomes emotional and damn near religious. Reasoning and logic goes out the window as people begin furiously frothing at the mouth if you dare question their beliefs.

So, let me clear things up before I begin. Here’s what I’m NOT saying:

— Renting is better than owning

— Renting is easier and less stressful

— Owning is worse for your finances

— Owning doesn’t come with great benefits

— The current rental market is a breeze

— You should buy or rent based on one factor

— The most important metric to consider is cashflow

Again, I’m NOT saying any of these things.

My view is simply this: I believe renting makes your cashflow smoother and your personal finances more predictable, while owning makes your life smoother and more predictable.

In this post, I’ll show you exactly why. Hopefully we’re on the same page so far. As we continue, let’s try to put our personal preferences aside and just consider the specific points being discussed.

And the context here is the FIRE community. People who are saving and investing on their way to freedom. Not an everyday person or a struggling retiree. Yes, I understand those cases, hence the points above!

My focus here is the broader concepts which are largely true most of the time. I understand we’re in a more unusual market right now which makes renting trickier than is typically the case.

When we look back at this article in 5 or 10 years time, I believe these fundamentals will still hold, which is why I’m writing it. Let’s begin.

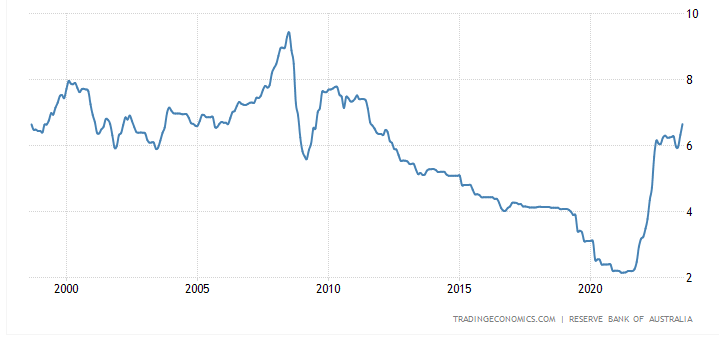

My first assertion is that rents are more stable than interest rates.

Rents may rise 10-30% in a few years, but interest costs can rise 50-100%. Both are rare, but the magnitude is different.

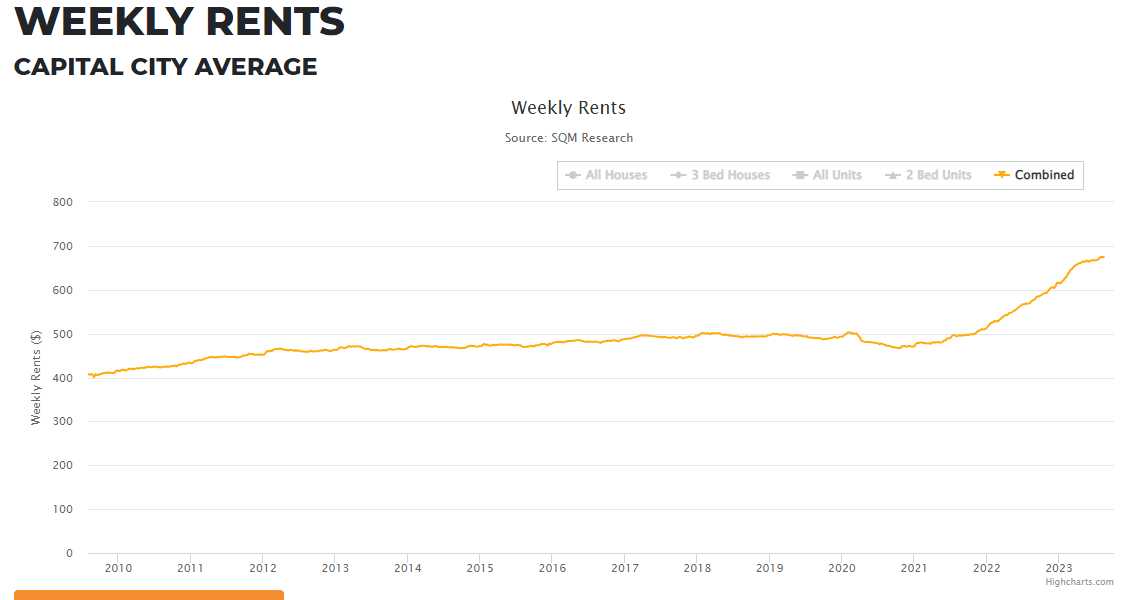

According to SQM Research, in September 2020 (the low point), average capital city asking rents were $470 per week for houses and units combined. Asking rents are now $685 per week as of September 2023.

That’s an increase of 45%. Some areas will be more than this, and some less (it’s an average). By the way, the data shows similar growth between houses and units in case you were wondering.

Not great. But as you can see, recent moves do seem to be more of an anomaly.

Most of the time, rents simply trickle upwards over the years in a much steadier fashion. Long term renters and property investors will know that’s the case.

How about interest rates?

Well, about two years ago, when the RBA cash rate was zero, a common mortgage rate was around the 2% mark. Today it’s over 6%. That’s an increase of 200%.

With a rate of 2%, mortgage debt of $600,000 would attract say $12,000 of interest. The annual interest on the same debt at 6% is now $36,000.

Now, this is also somewhat of an anomaly as interest rates don’t usually rise this fast. But as we can see below, interest rates (and therefore mortgage repayments) are more erratic and less stable than rents.

It’s worth noting that due to the amortisation feature of mortgages, repayments haven’t jumped as much as the interest rate.

According to the CBA loan repayment calculator, a new 30 year loan with a 2% interest rate would cost $2,220 per month. Change that rate to 6% and the repayment is now about $3,600 per month. A 62% increase.

So, rents will rise for a longer period than mortgage rates. But interest costs for a homeowner fluctuate more over a shorter period, especially from year to year, but also throughout the year.

Takeaway: monthly costs are typically less predictable for an owner than a renter.

Most often they do, yes. Though much of the time, it’s by relatively small percentages.

We can see that in the SQM chart from earlier. It also shows that rents can and do fall sometimes too, but less frequently.

This feature doesn’t mean renting is less predictable. In fact, it’s the opposite. Most renters would expect that rents will increase each year, bit by bit, most of the time. Again, let’s separate the current market environment (the exception) from the general rule.

As an owner, we also know our expenses will go up too. Water rates, council rates, insurance, strata fees, labour costs, etc. We expect to pay more for these each year, though most of the time it won’t be a lot more. Yet in recent times, insurance, building materials and tradies have also become a lot more expensive in a short period.

If the rents go up too much for your taste or budget, you have the option (in most scenarios) of moving to something a bit more affordable.

Ah yes, the never-ending rollercoaster of instability. This is why I said owning makes your life more predictable.

I’ve actually spoken to many people who’ve lived in rentals for a surprisingly long time (5-10+ years). So they may be lucky, or it could be that renting isn’t as much of a revolving door as many people believe.

I think it’s the emotional annoyance of having to move (not having the choice) that inflates this story in our minds. Which makes sense, but leads us to mistake what the most likely scenario is.

That said, renters DO have to move more often. And there are costs associated with that which owners don’t have to deal with.

Let’s assume a ‘forced move’ every 2 years. What’s the cost to move? Perhaps $1,000. Our two moves in the last 6 years have been less, but you could add more for outsourced cleaning.

This equates to $10 per week. Even paid as a lump sum vs budgeted for, it’s a tiny dent to cashflow, which can be covered with the laziest amount already sitting in a transaction account. Especially compared to moving as an owner, who’s up for selling agent’s fees and stamp duty on the next home.

These two costs typically equate to about 6-8% of the property’s value. Assuming a $700,000 home, we’re talking $40,000+. Now I know you don’t pay for that out of your own pocket, which is precisely why it’s such a trap people don’t even think about. But this ends up manifesting in a higher mortgage balance, which adds to mortgage repayments.

Effectively, one move as an owner costs more than a lifetime of moving as a renter. Every time an owner moves, a chunk of their net worth disappears.

How many people think of it like that? Very few. Regardless of how we slice it, this also affects an owner’s cashflow, so there’s no escaping it (unless you never move of course). Which brings us to the next point.

Absolutely, solid argument. And you’ll add value to your home in the process. Not that this helps your cashflow, but a fair benefit nonetheless.

Also, unless we want to live in a home that’s falling apart, renovating isn’t even optional. Just like property investors, we’re forced to update our properties over time or they become pretty crappy places to live.

Renters definitely don’t get this benefit. But given we’re discussing cashflow, how does that aspect compare?

A typical home reno, in place of moving, will run into the many tens of thousands of dollars. If this is paid with cash, it’ll mean forgoing investment income that money could be generating. If paid with debt, it’ll mean higher mortgage repayments.

What about the renter?

While they can’t always control when they move if they like a place, they can decide to move to a different property. One which suits their changing needs or tastes.

If one place is getting a little tired, they can move to something newer. All for the minimal outlay of moving costs and a modest bump in rent. In fact, the renter can end up in a renovated property without the hassle of managing the works, or forking out huge sums of cash.

At this point, it sounds like I’m 500% in favour of renting and I’m about to sell my house. Nope. I’m simply providing another way to look at things. We often become so enamoured with owning we can often miss the other side of the story, which can have just as sound reasoning.

Renters might also mention they don’t have to fork out for ongoing maintenance issues or problems with the property, which gives them greater predictability with their finances.

True. But having expensive items you need to budget for actually proves the point.

The very act of setting money aside for random expenses is a perfect indicator of a situation with less predictable cashflow.

Now, you could say renters need to budget for moving costs. But as we’ve covered, that number is so small it’s a nonsense argument. It’s absolutely peanuts in comparison to the owner’s lumpy expenses.

Side note: one thing a renter may decide to set money aside for is having savings to pay bulk rent in advance as a ‘one up’ in trying to secure a new property (which can be highly attractive to a landlord).

In truth, ownership costs are often random and lumpy. Roof tiles deteriorate. You get internal pipes leaking. Fence needs replaced. A large tree becomes problematic. Hot water system dies. And so on.

So unless you know the exact condition of every part of your house, visible and invisible, along with its predicted lifespan, budgeting isn’t always feasible. Don’t get me wrong, budgeting will smooth out your cashflow if you manage to account for all scenarios, but that often means setting aside (and not investing) a lot more additional cash than optimal.

Funnily enough, many people will point to the ease of budgeting for costs as an owner. While others are quick to point out the ‘sudden’ costs of having to move as a renter 🤷♂️

Here’s the thing: what starts as a repair can easily turn into a mini renovation. One thing leads to another, and little ‘improvement’ ideas pop into our mind. The truth is, many of us spend way more on our homes than we care to admit. There’s a reason Bunnings is one of the largest and most profitable companies in the country!

Of course, this is optional. But you’ll have to override your psychology to firmly resist. When you own a home, it’s far too easy to get caught up in, “Oh, imagine if we did this” or “You know what would be nice…”

Renters don’t struggle with the desire for constant refining or improvement of the home, because they aren’t as emotionally (or financially) attached to the space they occupy.

To renters, the details and small annoyances of a home doesn’t really matter to them nearly as much. It’s usually ‘good enough’.

True. But fixed rates usually come at a premium to standard interest rates (sometimes a substantial premium).

If you happen to lock in a great rate relative to where interest rates go, repayments will take a big jump after a few years, as is happening now to many people who locked in ’emergency low’ interest rates during the covid recession (as I did).

So while it’s possible to fix your rate and create stable repayments, it’s a less natural state within the Australian mortgage market. The US, however, is different. It’s extremely common there for people to have 30 year fixed rate mortgages.

What about refinancing? It’s totally possible to negotiate a lower rate in many cases, which is excellent and highly recommended!

Two things to note:

1. It basically means you were overpaying in the first place.

2. It’s not a controllable outcome, has tight limits, and is not a continually repeatable trick.

There are deals, sure. But we can’t control how competitive (or not) the market is. And the more we ‘save’ here, the more we were likely overpaying in the first place 😅

Here’s a little summary of what we’ve covered in this post:

— Rents are more stable over a multi-year period compared to mortgage rates.

— Renting is a single payment of the same amount every time, typically for 12 months. Owning has lots of additional lumpy expenses (council, water rates, insurance, possibly strata fees including special levies etc.) which amount to many thousands and come at various times of the year.

— Owning has the responsibility of paying for all repairs, damages, maintenance, and upgrades over time, which are all erratic expenses. More random multi-thousand-dollar expenses. A renter has no such obligation.

— A renter can more easily control the cost than an owner. If rents rise too much in one area, they can move to a lower cost place, by varying size or location for a minimal outlay. If interest rates or expenses become too high for an owner, they’re up for at least $30k-$50k+ to sell and downsize.

— A renter can more easily switch housing choices according to their income, work location, lifestyle desires, and space needs at the time. All at a miniscule cost compared to an owner, where transaction costs take a chunk out of their net worth and results in higher mortgage repayments even if the new home is of equal value.

— Renters are likely to make more logical financial decisions regarding their home since they aren’t as attached to the property. Owners are far more likely to overspend to try and personalise and refine their living space.

Bottom line: owners have many more ways their cashflow can be affected by various costs. Their monthly and yearly cashflow is beholden to many more forces outside their control (including government agencies, weather events, building issues, trade and material costs, and more).

Renters have one relatively predictable payment, which is more easily modified, flexible, and controllable, despite rents going up over time. All this results in smoother and more flexible finances for the renter, on average.

Much of the pushback on my social media post mentioned at the start of this article were along the lines of:

“But imagine renting when you’re 75 years old”

“But I have this relative who can’t find a place to live”

“But you’re completely at the whims of the landlord who can kick you out any time!”

“How can you possibly say that when we have an insane rental crisis!?”

The idea posed hurt their ears. Most of the pushback is simply emotional reactions to an emotional topic. Which is totally understandable!

It may have always been this way, but I’ve noticed something interesting lately: people tend to react to how a statement makes them feel, rather than whether the idea actually has merit or not. Just pure initial gut reaction.

So I don’t think people were logically arguing owning is more predictable for your personal cashflow than renting. I think they’re unwittingly just arguing how they feel about the bigger picture of renting, and that owning = maximum stability. When you combine that with a very tight rental market and some scary stories, you’ve got a recipe for the belief that renting = maximum fear and insecurity.

The emotionality of housing as a topic makes it hard to see the various angles through clear eyes. In general, many of us argue points simply because it fits with our own life decisions. We don’t want the mental discomfort that comes with acknowledging that the alternate choice could also be a good one. This conflict isn’t nice to sit with, because it causes us to question our decisions.

I hope this article helped shed some light on another angle to look at renting vs owning. I stand by my original comment:

Owning makes your life more predictable, renting makes your finances more predictable.

The seemingly high control of owning comes with many responsibilities. The seeming lack of control with renting comes with many freedoms.

I get that this is counterintuitive. From the outside, it looks as though renting generally comes with no control over your housing situation. But behind the scenes, most of the time renters have more control over their destiny than it appears, especially those who are financially savvy (which is who this post is for!).

Again, I’m not saying renting is better. Just playing devil’s advocate here and fleshing out these points for a more complete picture of my comment.

Now sure, there are exceptions to everything, but as a general rule these points are accurate. Before you send me a bunch of angry comments, go back up and read the caveats at the start of this post 😉

Don’t get me wrong. I agree with the pushback, to a point. There’s few things more stable than ending up with a paid off house. So even though it wasn’t the comparison here, it’s fair to say that owners eventually get the last laugh, with a unique level of predictability. But in most other scenarios, renting is far smoother from a cashflow perspective.

So, as much as renters are reminded how shaky and uncertain their future is (in fact, it’s rammed down their throat as part of the endless victimisation circus that is the media), I want to remind you of something very important…

While a house is a valuable asset that eventually saves you from paying rent, you definitely DO NOT need to own a house to become wealthy or retire early.

If you’re good with money, both options work just fine!

Here are some resources you may find useful on your wealth building journey:

Mortgage broker: My personal broker of 10 years is More Than Mortgages. Highly rated and award winning, Deanna and her team been super helpful over the years and can assist you with anything home loan related, including refinancing and debt recycling.

Sharesight: A great portfolio tracking tool for share investors, and free for up to 10 holdings. It tracks all dividends, franking credits and capital gains, which is incredibly helpful at tax time. Saves me a lot of time and headache!

My book: After 5 years and hundreds of articles and podcasts, I decided to distill everything down into an easy to follow book. Designed as a complete roadmap to achieving financial independence and retiring early in Australia. Available in paperback, ebook, and audio.

Just so you know, if you do use these resources, this blog may receive a financial benefit at no extra cost to you (thanks in advance). I only ever recommend things I genuinely believe in.

Why deliberate spending is my favourite money management style. What it really means and how you can use it as your situation and priorities change over time.

My thoughts on ‘The Great Taking’. An idea that the masses will lose untold amounts of wealth in the next financial crash, due to a deliberate plan by mysterious figures.

Get my latest content and thoughts straight to your inbox.

A fresh dose of financial motivation to power your journey.

I feel like the vast majority of articles on this topic – including this one – ignore the actual practicalities of renting into our older years.

How many landlords are going to choose an 85 year old as their tenant? What about when it’s not longer possible for them to physically pack and move their own belongings? The moving costs quoted certainly aren’t a ‘full service’ moving company. What about the mental health toll of an 80 something unable to provide themselves a smooth home?

It’s easy enough to look at the numbers, or assume government or family support will be there as a backup etc: but that’s just not going to be the reality for a lot of people.

I’d love an article that actually interviewed people in their 80s and 90s who still rent and have actual lived experience, and get their perspectives on whether in average they’re happy with that lifestyle or they wish they’d had the opportunity to buy.

To say those who raise these things are just having an emotional reaction or that it ‘hurts their ears’ to consider different perspectives is pretty narrow minded.

Life isn’t black and white, and it’s about so much more than the numbers.

As a landlord, I couldn’t care less how old a tenant is, as long as I think they can pay the rent, have a good rental history and should keep the place in a decent condition.

There are always special considerations like the ones you’re pointing out, which I specifically flagged earlier in the article. You must have missed where I also specifically stated this article is for people on their FI journey. Which are precisely the people I was getting pushback from (not renters in their 80s). These are the same people who also have savings and investments and have the option to buy a home at some point during their lives if they don’t want to rent as they age for various reasons.

So you’re talking about an argument which I’m not actually making.

It’s such an emotional topic. I’m currently a happy renter who reached fire through a share portfolio, but plan to buy at some point in the future for security (as others have pointed out). We’re moving cities in early december, and it is soooo much less of a hassel then buying/selling. I went to 10 inspections over the weekend (and secured a rental) and what i noticed was that at the higher end of the rental market ($800/week) there was sparse attendance compared to rentals 750/ wk and under.. so the squeeze is definitely on for those without budget flexibility. The other thing this housing crisis has highlighted to me is what a financial privilege it is to be in a dual income household.

Definitely an emotional topic! Interesting point about the higher end of rentals… it often tends to work out better value at that end in terms of what you get for your money. By that I mean rental yields for expensive homes tend to be very low, meaning it becomes far cheaper to rent than own the higher up you go in cost.

I understand it may not have been the focus of the article but I think Christie has a point as age is a part of a risk assessment. How many weeks of rent will you miss out on if an elderly renter dies in your property? Will your agent now need to inform people that someone died in the property? Will people balk at renting or ask for a price reduction?

Similar to people not allowing pets, or unemployed or smokers, age can be seen as a risk.

I think you’d be in the minority of landlords there Dave for sure.

In a high demand area if presented with a list of applicants I don’t think it’s much of a stretch to say most landlords are choosing the employed couple over an older person. In my area it’s hard enough for anyone with kids, pets etc (and a retired person could have one or both of those as well!)

And I didn’t miss the point at all, I’m saying it’s a shortsighted one in my opinion. People on a FIRE journey have even more reason to consider the longevity of their strategy than others who aren’t.

The point I’m making (which perhaps you missed) was not that with the benefit of hindsight and lived experience, would those older renters still have made the same choices when they were in earlier phases of life. I think there’s something for younger people on the way to FIRE (like myself) to consider and reflect on in that.

To call these things a special consideration only underlines my initial point to be honest.

To echo Dave’s point below – I just turned 40 this year and we rent but I’m sat on a net worth of $2m currently yielding 10-14% YoY. It’s unlikely I’ll be wanting to rent in my 80s so as soon as I’m ready for pension age, I’ll liquidate some assets (looking at around $16m in by 62) and buy a house.

You may be missing the wood for the trees.

Where on earth are you getting 10% – 14% YoY?

My guess is long term dollar-cost averaging returns from a global-heavy share portfolio over the last 15 years… but could be wrong.

What if the idea of rentvesting? Rent the location that is more suitable for work during the younger years and enjoy a more stable cash flow. On the other hand purchase an investment property to move in at an older age. Any interest raises and other utility increases will be absorbed/protected by negative gear. If the investment is not negatively geared that means you’re doing well and the cash flow fluctuation is no longer an issue.

Yep that can work well and be the right fit in many cases. I guess the idea there and the key point being to make sure you’re investing while renting. One can definitely get the benefits of renting with the upside of property ownership without actually owning the place they live in. And as you say, the downside costs become tax deductible so it does provide some ‘shock absorption’ in that sense.

One should also consider the time and effort of owning a property, it can almost equal to a part time job at times. For example, every few years you might need to do a renovation… this will include but not limited to

1) look at the problem

2) getting quotes

3) evaluate quotes and doing your research on contractors, including reviews and materials

4) review plans

5) choosing contractor and review prices and make sure you don’t get ripped off

6) make your final decision and schedule time

7) make sure the contractors are actually doing their job properly and not a band aid job

8) get ready for scope changes and variations

9) if you are lucky then everything goes well, if not then prepare for more time and emotional consuming conflicts and emails and possible legal actions

I have know people they pursue legal actions again their contractors, with or without success…. It’s all very time consuming and drains your emotions and make you very stressed …..

Also, if you plan on travelling a rental will be worry free as you don’t care if there was a

Storm damage or burst pipe… if it’s your own home, you need to get someone to house sit and constantly check on your property ….

Fair points Jack, thanks for sharing. I’ve actually got another post planned on this topic after my experiences owning a home in the last couple of years.

Interesting article – but if you don’t buy a house with all your cash sitting in the bank / or invested at 65 when you retire and no longer have an income to pay said rent – you will not be entitled to any old age pension and with no income either ?

But you will have an income if you’ve invested the money… that’s the whole point of investing it. If someone follows this blog, saves their whole life… and retire with money in the bank earning nothing, no home, no other investment income, they’ve done it wrong.

Hi Dave – good read. I haven’t chatted to you in ages! We rent in Coogee and have taken a recent and sudden rental hit that will kick in around the end of December. Your characterisation of how rent moves is accurate in my situation.

When we moved in 10 years ago we were paying $530/week (that was considered a lot then), then it went to $555 and then $570 where it sat for years, and then last year it jumped to $600 and in December it’s going to hit $700! Yikes.

The other day an older guy I know (about 70) was gob-smacked that I was not interested in buying a house, not now anyway. I got the “but rent money is dead money” trope. I tried to tell him we were rent-vestors and my “asset” was building a share portfolio over all these years. What I didn’t tell him was that the portfolio is now worth $1.3M. Never would have happened if we were being sucked dry by a pile of bricks, glass and wires (aka a house).

Thanks for sharing Scott! Hope you’re well mate 🙂

When you look at that growth of rent over 10 years it’s actually relatively mild… like 2.5% pa. It’s just that it can shoot up at certain parts of the cycle, then be flat for others.

Ah yes, rent money is dead money… that’ll never die.

Similar boat to you Scott with $1.3m investment portfolio and happily renting, Renting in Ryde area for last couple of years after selling my Apartment and have no intention to buying a property in near future. I have this arguments with my friends all the time regarding “Rent money is dead money” lol and as Dave mentioned this argument get a bit emotional so Logic and facts often dont win the day but it is what it is.

P.S- Great article Dave, i might be sharing it with my friends next time we have this debate lol.

Thanks Loki – it’s not an easy discussion to have, but kinda fun, even though nobody ever changes their mind haha 🙂

Rent vs Buy has been an interesting discussion off and on for many years and I see the arguments for both and have considered both as a means to increase personal wealth. However, the last 2-3 years has really caused the rental side of the argument to drop off a cliff.

I would like to know Peter Thornhill take on the situation in recent years as he has always been a proponent of renting, albeit with the more long term style offered in Europe.

Fair enough Mango. Would you say your mind has changed due to the tight market, or simply the price increases? Because the cost increases for mortgage holders has been greater, so I’m guessing it’s something else, maybe more of a general uncertainty around renting.

Thornhill is an owner from memory, and he’s famous for having unwavering views on things, so I dare say he’d say the same thing as before – renting is ideal if there’s longer leases or you don’t mind it, but if not, then owning is the winner. I think his view was driven mostly by a desire to not own property and have every dollar possible in shares, rather than a strong view on renting vs owning.

Dave good one, thanks for taking on the tough topics. I agree for the most part with what you have written, but I think the discipline of the person plays a huge role in this debate.

I find that people who are reaching fire are more disciplined than the mainstream community with savings and investing. These people have the ability to set a target/goal and work away at this for a number of years. I am sure many people could rent and invest to reach fire. On paper for a lot of people, this makes sense. There are also owners who would be better off financially renting on paper. However, I don’t think most people are wired to rent and save/invest. They actually need the loan/debt of a house to make them save. I have heard this called forced savings.

When things get tough, It is so easy to put off investing if I am a renter, it is not easy with a loan and being a homeowner. Homeowners seem to step up things when times get tough. They pay the mortgage at all costs. This forced saving from a home loan is for many people the main source of their net worth.

I read this article a while back. In the US, the net worth of homeowners is 40 times greater than that of renters. I think this shows although renting is a viable path, most people on this path are not savers and investors.

https://www.cnbc.com/select/average-net-worth-homeowners-renters/

Excellent article Dave. An important factor in the discussion is a functional and viable rental market. I’m living in Ireland at the moment where there is no functional rental market unfortunately. There is virtually no rental stock available and what little comes up is vastly over-priced. Average mortgage repayments are far cheaper than average rent. €1200 vs €1800 per month on average. Many renters (and some owners) are technically in a state of poverty. Their rental costs are more than 50% of their household income. And they are trapped. It’s a dire situation, which hopefully will be resolved in the coming years through massive increases in housing construction.

Cheers Jeff. Sorry to hear about the situation in Ireland, I wonder how it got that bad. Possibly a hangover from their large property downturn and eventuating shortfall of building?

Hopefully it doesn’t get that bad here, though building does look to be woefully slow at the moment compared to population growth, so I don’t see it improving soon.

Hi Dave, another good insight into a real life scenario. I just want to add another take on your the topic and that is if you pay off your home. You now have security and smooth finances 🙂

We decided to buy a home and invest and keep investing small amounts. After 6 years of living pretty frugally we paid our home off just before the interest rates started going up. Our property has gone up around 50% after a recent valuation. That equates to around 8% p/a return on our money. I checked the ASX200 and for the same period has only returned 21%. We have no interest in renovating, and only fix what needs repairing which to date has been around $5k p/a. While we have forgone investing around $1m into the market to buy the house, we now don’t need that extra $5k p/m or more now to pour into the mortgage. We are very happy where we live and have no desire to move. The house is a huge asset that doesn’t give any return, but we are immune from interest rate hikes and the rental crisis. We have also managed to create a healthy portfolio which within a few years we should be able to start using the dividends toward living costs with some part time work thrown in.

Keep up the great articles Dave.

Cheers Matt

Absolutely true Matt, owners get the last laugh once they eventually have a paid off home in that sense.

Sounds like a mighty fine situation!

Speaking as an older FIRE person, I can categorically say that retiring in a paid-off house WHERE I WANT TO LIVE is absolutely wonderful. I pay $45/week in rates (and I make sure I read books from the library to cover this cost, so essentially I’m getting my rates for free), and life is pretty cruisy.

I put the ‘where I want to live’ in capitols because I’ve only bought 2 houses in my life – the first was where I brought up my sons in one of the best secondary school catchments in Melbourne; and the 2nd is by the beach living with my dogs. I only spent money on agents fees, repairs, renovations etc in places that I knew I was going to spend decades in. (First home two decades; second home… let’s see!)

I have a good friend in England who has bought and sold 3 houses in 12 years. He and his husband have bought, renovated, then sold these houses as his partner’s jobs changed. They have spent thousands on agents fees alone.

I think that when you’re pretty sure about where you want to live for the foreseeable future, then you can’t beat buying. The security is wonderful and if you’re happy with the location, then life is good.

But if you’re young, just starting out and life is pretty fluid, then renting is the way to go. Far better to pay rent for a few years than do what my friend in England did.

Anyway, that’s just my two cent’s worth!

Thanks for sharing, well reasoned take, and I agree!

Great article and food for future planning as I’m 24 and nowhere near being able to buy (especially in Sydney).

“people tend to react to how a statement makes them feel, rather than whether the idea actually has merit or not. Just pure initial gut reaction.” Judging from this quote you may be interested in the book ‘The Righteous Mind – Johnathan Haidt’.

It’s framed towards politics and religion but it basically discusses how people will form a quick snap judgement and then pull off a whole lot of mental gymnastics to fit ‘reason’ and ‘logic’ around their initial thoughts and justify them. In this case, I think people are very inclined to think that what they are familiar with is the better option. If they’ve always wanted to buy and bought then they want to justify that their years of hard work and costs that have been invested into buying a home and paying off a mortgage were worthwhile. A bit of motivated reasoning going on.

Similarly, my dad has had an investment property or two for a long time and has seen pretty good returns but is vary wary of any kind of shares. I think if he had actually tracked the numbers over time, that shares would be in front and all with a lot more liquidity, less hassle and stress depending on how you manage it. He also wouldn’t still be looking for a tenant on a recently renovated place…

Anyway, great read. Thanks Dave!

Yeah it’s a funny thing, because there’s almost no way to talk to someone who’d already made their mind up. And honestly, most of us hold pretty fixed views on things because it’s just mentally easier than leaving all these unclosed loops in our minds. An unclosed loop or ‘not yet decided’ opinion is a form of uncertainty, and our brains tend to hate that 😅

All fine in theory but explain that to the evicted tenants who are not able to secure another rental in the current market.

As a retired rental manager I am currently trying to assist several excellent tenants who have been issued notices to vacate but there are not enough suitable local rentals. If you could secure long term tenancy (say 10years) it would be a different scenario.

Robert, this wasn’t a ‘renting is better’ post, it was simply fleshing out one of the key variables that I found people were struggling to comprehend. Obviously, there are many other factors at play, which I’ve spoken about elsewhere and will do so again in the future.

Great article Dave!

We rented for 5+ years, then built a house to live for 12 years before selling that to find a trip around Australia. We are now looking to rent again next year when our trip finishes and love the flexibility on where and what type of place to rent knowing that if it do any suit us we can move again without significant costs.

I work for a global company and while we had the house watched many promotions interstate and overseas go by without being able to put my hand up. It was just too hard to sell the house on shortish notice – we never wanted to rent it out due to several friends having terrible, stressful and costly experiences with bad tenants (especially if interstate and unable to do an occasional drive by).

In our travels we have enjoyed large houses, small and cosy ones, views of the beach or of the mountains, space and large yards, pool or not and built up areas with convenience options. All had their pros and cons. We are still not sure what our ideal would be and we cannot afford the pros of all of them. Knowing that we can rent something, somewhere that we believe is right for us at this moment in time but up and move if it isn’t is a comfort. Being flexible for work opportunities or moving as our kids grow and need different things is also helpful.

We plan to buy or maybe build again one day, but not anytime soon. There are so many hidden costs with owning that I didn’t realise when I was renting and thought it as ‘dead money’ but now I know it isn’t.

I don’t know what the property market is going to do in the next 5-10 years but I doubt it will double as it has previously done just purely on the maths. Not enough people will be able to get the loan unless there is a large pay spike.

What if the market goes sideways for 10 years? That is a lot of interest payments, maintenance, council rates, water rates and building insurance. What is the opportunity cost on that? What if your forced to sell and move somewhere in that time for work or lifestyle changes? Now you’re really going backwards.

Thanks for sharing, lots of great considerations and lessons in there.

As you say, lots of tradeoffs and benefits with both options, so it’s good to have had such a variety of experience with renting and owning. Puts you in a far better position to give a balance viewpoint and make the right decision when the time comes.

I’m especially enjoying the comments from long-time renters saying they’ve enjoyed the experience overall. We only ever seem to be told about the downsides, the nightmare scenarios and how it can all go wrong, so this is a refreshing change 😉

As a single person in her late 40s I have been grappling with owning vs renting argument for years. I’ve owned investment properties (all now sold) and rented my whole adult life. The amount of social judgement renting attracts (especially in your 40s) is astounding.

Yes,renters can get kicked out. First 3 properties I rented were sold after the lease expired. But I’ve also lived in 2 properties (London & Melbourne) that have overseas investment only landlords and I’ve lived in both over 5 years. No fear I’ll be kicked out.

During 2020-2021 Covid years, I negotiated rental reductions due to the large vacancy rates in inner Melbourne. That extra $$$ went into savings/investments. Now as the tide has turned, it’s shot up again, but as Dave mentioned, not as bad as interest rates and cost of property maintenance fees that landlords incur.

As a former owner/landlord I understand first hand the costs of ownership. Don’t miss it.

But as a renter who needs to consider retirement sooner than I want to, the fear of not owning a home when pension age arrives is a little scary.

As for opinions about challenging rental conditions at age 70-80, I wonder if people have considered, at that age, you’re more likely to want/need aged cared facilities or move to a smaller town/community.

I could put all my hard earned $$ into buying a home in Melbourne today. It would be a squeeze, but I could do it if needed. Buy small. If I buy now, I’ll still have a big debt at retirement. But when I turn 65-70, I’ll probably want to move to Queensland, NSW coastal areas or live in Spain. Maybe sell shares to purchase a nice little retirement cottage.

Just food for thought for those (like my parents) who believe they can continue to live in a big family home well into their 70s/80s, who have security in ownership but health challenges with maintaining a home they can no longer manage and are too attached to let go off.

Thanks so much Dave for sparking the (very emotional) conversation. I love having example facts and figures laid out so clearly.

Thanks for offering such a balanced opinion, based on your experience of both sides of the coin!

As you point out, the amount of social judgement and assumptions about renting is mindblowing. I’ve noticed it a lot over the years on this blog (and in forums), so even though I own, I really find it valuable to provide other angles to the argument, since it’s so routinely dismissed by most of the population, even in the FI community. We only seem capable of amplifying one side in our minds, largely due to the emotion and ‘security’ aspect involved. Understandable, but doesn’t mean we shouldn’t strive to zoom out to form a broader understanding as you have.