As this year is almost over, it’s time for another portfolio update.

The last update was back in July, and man, things have changed since then!

I’ll share how our investments are going and what we’ve been buying in the last few months, as we continue building our share portfolio and passive income.

Alright, let’s get stuck in, starting with the current breakdown of where our savings are stored.

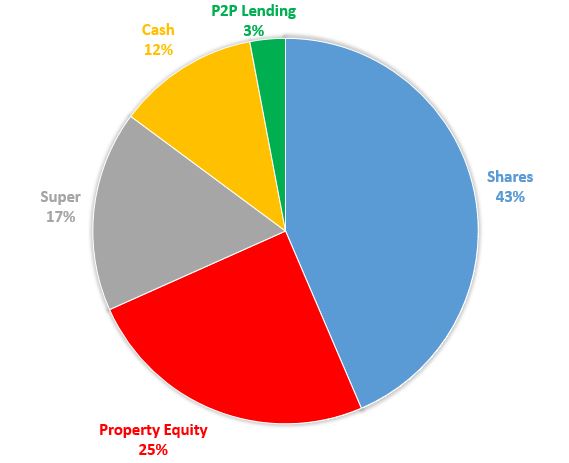

In the below chart you can see the basic breakdown of our net worth in percentage terms.

And for those that are curious, without super, the breakdown is: 52% shares. 30% property equity. 14% cash. 4% P2P lending.

Our super is still 100% international shares, while our personal portfolio is mostly Aussie shares and property.

Our share portfolio has become larger due to regular purchases and the market recovering. Plus, a couple of our properties I have adjusted higher (based on similar recent sales).

So super, cash and our peer-to-peer lending have become slightly smaller in comparison.

Speaking of which, our peer-to-peer lending investment with Plenti has actually been one of our best performing investments over the last 4 years, returning a reliable 8-9% income per year. Interest rates are lower now, unfortunately, but that’s true across the board.

If you were interested in trying out peer-to-peer lending, you can sign up using this link to get a $100 bonus when you invest $1,000 (or more) in the 3 or 5 year market. That’s like an instant 10% return.

The 3 year market rates are currently 5% per annum, and the 5 year market is paying 6.9% per annum. Read more about how Plenti works in my article here. They just reached $1 billion in loans funded, which is quite an achievement.

In what seemed unthinkable earlier this year, the US and Aussie sharemarkets have both had strong recoveries to date. The US market is now at all-time highs, and the ASX is getting close.

Unfortunately, when I wrote my article “My Thoughts on the Current Sharemarket Crash” back in March (days from the bottom), many people were sceptical the market would recover.

In fact, some suggested it was reckless to keep buying! Better to wait until the market was firmly in recovery mode and heading back up they said.

I urged readers to keep buying, and buy more if they could. Not because I knew the market would recover so fast. But because investing regularly is pretty much always the most sensible thing to do.

On the flipside, timing the market requires more effort, more stress, more time, and is unlikely to deliver a better outcome! Especially so when you have a goal like financial independence in mind.

In the last few months, property markets in most cities have started to improve. Here in Perth seems to be one of the strongest!

After being a laggard for the last half-decade, it’ll be good to see Perth have its time in the sun. And of course, owning multiple Perth properties, we have a huge financial bias swaying that opinion 😛

Jokes aside, it does look like our properties should fare reasonably well in the next couple of years. And we still have plenty of cash so we probably won’t sell another property until 2022.

All signs are pointing to rents increasing strongly here in Perth too. This will help our cashflow as we’re still forking out for principal & interest on each mortgage (which is fine since reducing debt is a form of saving).

Since the last update in July we’ve topped up all our holdings at various times. Quite often I look at which of our shares have lagged in the previous month and then buy that one. Recently that’s been our international index fund, VGS.

You might remember last year we owned some real estate investment trusts (REITs). I ended up selling these for large gains and reinvesting elsewhere as they became (in my view) vastly overpriced, trading well above the value of their property portfolios.

Well, this year the opposite has occurred. REITs were hammered during the market crash and some now look very attractive. And I’ve actually bought one for our portfolio. It’s a diversified office REIT if you’re curious. Yes, I’ve read “the office is dead” stories. I don’t buy it.

“Wait, what happened to keeping it simple?”

That’s true, I’m kind of breaking my own rule. But this still feels simple. I was actually looking into unlisted real estate funds, after thinking more about having a long term allocation to commercial real estate as our portfolio gets bigger. That’s when I noticed some REITs are now much cheaper than before.

Also, it’s fair to say I’m not ready to be a 100% passive investor. I’ll likely continue with a mix of index funds and active choices in our portfolio.

The overall goal remains to steadily increase our investment income over time, while building a diversified portfolio of investments that are easy to understand and require little effort.

The only challenge will be deciding whether to keep REITs if they become stupidly overpriced again, or reinvest the cash elsewhere.

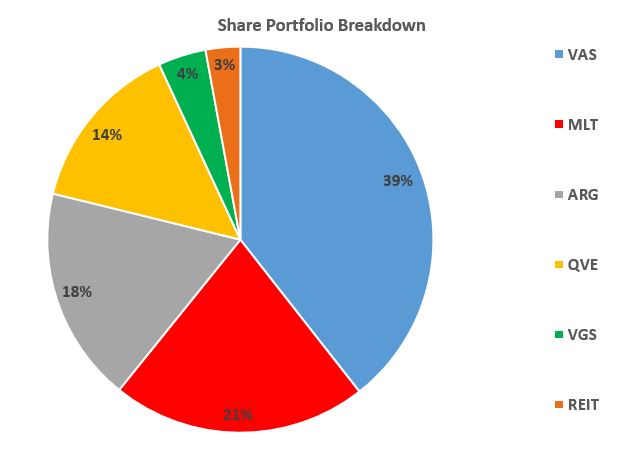

Here’s the latest breakdown of our share portfolio for H2 2020.

As you can see, still mostly Aussies shares with our LICs and index fund, VAS.

Our holding in VGS is bigger than last time, and will slowly continue to grow. And as mentioned, a real estate holding has been added.

Looking ahead, I can see us buying more international shares (VGS) and real estate to increase those parts of the pie over time.

That said, I do like to top up whatever seems good value at the time, relative to the others.

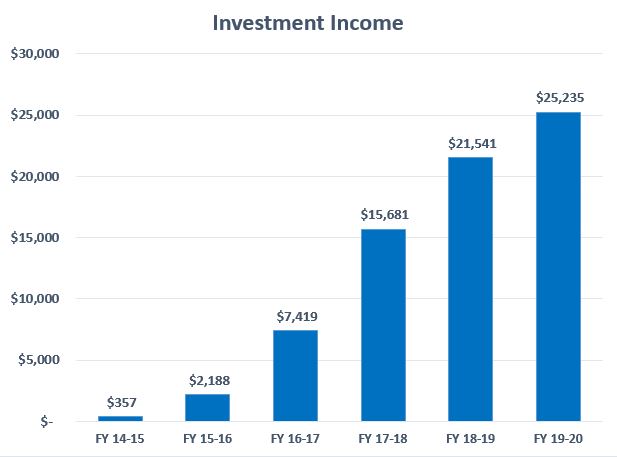

Yes, it’s now time to take a look at my favourite metric.

This chart shows our portfolio’s income from the 2019-20 financial year. The figure includes dividends, franking credits and interest from peer-to-peer lending.

If you’re interested in what I use to keep tabs on our Annual Investment Income, you can get it below…

Sadly, I do expect this pretty chart to lose its winning streak this year! There’s still a while to go for the current financial year, but dividends have definitely taken a hit. It’s difficult to make enough money to pay fat dividends when the economy shuts down I guess 😉

Income from our LICs have held up reasonably well so far. QVE hasn’t cut its dividend at all. Milton and Argo have both cut dividends by around 10%.

There may be more drops to come this year, but with the economy firmly in recovery mode, things should improve from then on.

For new readers: You might be wondering how we consider ourselves ‘retired’ if our passive income of $25k isn’t more than our household spending of $40k. I explain exactly how it works in this article.

You can also find a detailed article on how we’re turning our equity into income, using my property-to-shares transition strategy.

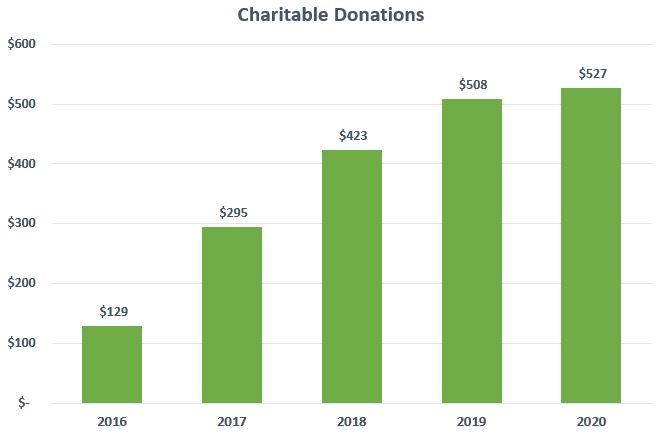

Just like the above, I’m aiming to increase the amount we donate to charity each year. In fact, I secretly hope it becomes our biggest household expense. Eventually!

We’ve only been going for a few years, but in 2020 we managed to increase our donations by almost 4%. Depending on how things go with our finances, we may ramp it up faster, but the main goal is to keep the streak going.

Granted, these aren’t huge numbers. But this is a long term focus and I’m happy with the direction it’s heading. And if you’re wondering where it goes – mostly animal welfare and environmental causes.

I’m aware of some people avoiding ETFs since the tax statements are, shall we say, a dog’s breakfast? The dividends (distributions) come with many different components and are not fun to read.

But this doesn’t really matter. Because Sharesight tracks all of it, with me only needing to casually check it during end of year tax preparation.

Sharesight gets the data directly from the share registries and fund managers and inputs all the complicated stuff. This article explains exactly how they do it. Of course, you should always double check it, but this is so freaking good.

I don’t want to sound like an advert, but if you’re not using Sharesight, then you should be. It costs nothing if you have 10 holdings or less. For larger portfolios, you do need to pay, but there are lots of extra features alongside.

You can connect your Sharesight account with most brokers, so that trades are automatically imported. It saves much wasted time and headaches, so you can focus on other things. That’s why you’ll see my affiliate link around this site, and on my recommendations page. It’s something I use, enjoy, and would recommend regardless.

So there’s no reason to avoid ETFs because of their complicated tax statements.

The more I talk to people about investing in shares, the more obvious it is that our psychology and emotions account for 90% of our results (because that determines our behaviour). Knowledge is really only about 10% of the equation.

With that in mind, if you (or someone you know) is struggling to get comfortable with long term sharemarket investing, because they’re a newbie or maybe a religious property investor, direct them to this post. It should calm many of their fears.

Well, that’s the latest peek into what’s happening with our investments. It’s hard to believe how strongly the sharemarket has recovered in recent months. And while I’m not waiting for it, there will be another wobble at some point.

Either way, I’ll be investing every single month – rain, hail or shine!

How have your investments fared in 2020? What have you been investing in? Let me know in the comments below…

Note: Since I use both, I’ve signed up this blog as an affiliate for Plenti and Sharesight. If you decide to sign up using the links provided, this blog may earn a referral fee. I never recommend anything I don’t use myself or genuinely approve of.

Learn how our EV performed on our recent roadtrip and holiday in Southwest WA. What I learned from the experience, plus lots of pictures, recommended places to eat, and more 😉

The numbers behind our recent solar installation and how much we’ll save. A breakdown of solar FAQ, whether it’s a good investment and what to watch out for.

Get my latest content and thoughts straight to your inbox.

A fresh dose of financial motivation to power your journey.

Long time reader, but I’ve never commented. So to break the habit, I just wanted to thank you for all your content so far, it’s been a pleasure to read. It’s great to have somewhere to go where someone else is just as interested in personal finance as I am. I haven’t found anyone keen enough on the topic in real life to talk about this, it always just feels like I’m lecturing them, instead of having a balanced conversation lol.

My investing this year has taken a halt, at my own fault. I’m 26, been investing in equities for over a year now and have about $250K in cash that I want to invest, but back in March, when prices suddenly became amazing, I wanted them to drop further, and so I hesitated and stopped buying. Waiting for the right moment to buy, instead of keeping to the monthly purchasing that I had in place, looking back, feels like a mistake. Especially since my goal is to produce income, growth is just a side benefit. Still, I feel like I’ve learnt a lesson; to not let opportunity pass you by. However, there is a part of me that wants to wait for another opportunity, even though I’ve read a million times that ‘time in the market, is better than timing the market’. Funny how even though I know this well, well before the march selloff, I never knew how l would act under those circumstances. I have no negative feelings to market fluctuations however, I couldn’t care less actually. I have/had no urge to sell, because I’m after income. Though, I wasn’t ready for how I would hesitate in buying.

So, my last investment was back in February. I’m not too proud of it, but, I think there are valuable lessons to learn from most happenings in life. My plan now is to DCA again, but have significant cash reserves so when there is another opportunity, I can make the most of it. Best of both worlds.

Anyways, that’s my year in investing. I still have so much more to learn, and mostly to experience for myself. Thanks again for everything you do on this blog. I appreciate the significant amount of time that you invest into this.

Harry.

Hey Harry, thanks for the comment! Great to have you here where you feel at home with like-minded people 😀

Thanks for being so open about your struggles this year, it’s interesting to read and more common than you would think. I think you’ve come to the right conclusion – hopefully you can make it a habit and stick with it, knowing you have plenty of cash and won’t miss out on buying at attractive prices if they do come along. All the best! Make 2021 the year where you create your rock solid investment habit – every month no mater what!

Sorry I’m a little late to share thoughts on this Harry but couple of points.

1 – you have amassed an impressive amount of cash for your age and you really cannot go wrong from here, maybe focus on where you are rather than ‘where you could have been’ as it isn’t helpful.

2 – picture a scenario 3 years from now where the market has gone up 30% and your still sitting on the sidelines. No idea if it actually will but if it hasn’t that just means you can keep buying more knowing it is cheaper than expected! Like planting a tree, 20 years ago was best but next best is now.

3 – put an actual investment plan on paper or spreadsheet or maybe there is an app for it these days… I.e. what index’s are you going to buy and what % of each do you them to have and when are you going to buy (DCA into them), an actual date like 1st Monday of the month. Then just do it, don’t look at the price, just buy the amount you commited to, in the index that is under weight at the time AND on the day you commited. Not a couple of days later because ‘it might drop’.

This might help make it an actual habit and short circuit the little man in your brain that keeps over analysing you into paralysis!

Hey Adam, sorry I didn’t reply sooner. Thanks heaps for the advice!

I just recently formed an investment plan actually, hopefully I can stay disciplined enough to follow through with it. I’m aiming to strictly invest the same amount on every first Thursday of the month, with added flexibility to allow myself to invest more if prices look attractive. That way I can regularly invest, but also be on the lookout for value.

I’m trying to keep it simple as I’m prone to analysis paralysis haha.

Why don’t you publish your net worth?

Why don’t you publish yours?

Anyways, another person’s net worth is completely irrelevant. It isn’t a “mine is bigger than yours” competition.

Not really… I find it really helpful to have know a target number that someone who has fired has and what I should kind of be aiming for (like AFB and millennium revolution). Yes I know everyone circumstances are different but it’s good to have a rough idea specially if they are in a similar situation (living in Australia…etc). Don’t get me wrong, I love SMA content so far and would love it so much more if he did share his net worth (even just a ball park figure say roughly 1 or 2 mill) but also understand why he doesn’t.

I get it but as I have said in a different place when there was a mention of books to read, the lot can be summarised in a few words which are “Invest as much as you can for as long as you can and be content with the outcome whatever it may be.”

Sort of fits with my general investment philosophy of “I don’t give a stuff. It’s all about me”

Sometimes it’s best to create your own disaster.

Hey Aly. Just to clarify – I’m not anonymous for one thing like many other bloggers (Firebug for example). Constantly sharing my exact net worth was something that I decided from the start of this blog that I’m not comfortable with and I don’t think it really adds any value to readers. I’ve shared the ballpark range numerous times (it’s a little more than $1m). That’s more than enough information for those that simply have to know!

Importantly, your target will be 100% based on your own living expenses. So my target or anyone else’s doesn’t really affect your own goals. The easy target is simply 25 times your annual spending. So the real goal is perhaps to get your living expenses similar to other people’s if that was your way of comparing yourself – because that tells you what your net worth goal should be. Hope that makes sense 🙂

Thanks SMA.

I didn’t realise you shared a ballpark figure but that is very helpful. Thank you for that.

I understand it’s strange especially as you said, you not annoymous – I didn’t properly think about that. It would be very strange if family members, friends , neighbours…etc knew my net worth.

That’s a great way to frame it actually – like declaring it to your friends on a semi-regular basis… when you’re just trying to provide them the odd bit of useful advice 🙂

Haha yes well said. The guy won’t even publish his email address! What does that tell you?

Hey SatayKing! Like Dave, you also contribute great advice also. Thanks Mate

It’s Dave’s blog.

Anything I may post in response to some other posts are just the ramblings of an old has-been who has been burnt one or three times and finally realised I am an average, as well as a lazy, investor.

I find it interesting that in your comment you’ve entered your email address as ‘thisisntreallymyaddress@…’ So you won’t even share your email address with me but you feel entitled to see the exact details of my net worth.

Sorry, that came out harsher than I intended. Now that you’ve explained it, it makes sense. I just enjoy following the growth of Aussie firebug’s portfolio and was hoping to see the same in yours, but as you alluded to I totally understand the desire for privacy online. Speaking of which, that actually that is my address, I chose the name as a joke.

Thanks for clarifying George. All good mate, appreciate your understanding.

Great write up Dave.

We have been tossing and turning over VGS v VTS/VEU split for a couple months, but have decided to add VGS into our portfolio starting next month (January 21). After all, one of our key elements to the FIRE journey is to keep it simple.

Can’t wait until the end of December to do a full recap of the years results, the market has shown us a bit of everything and somehow is going to provide a great return!

Stay Well.

Cheers Sneak! Nice work coming to a decision, sometimes that’s the hardest part. It’s certainly been a crazy year for markets, and another lesson of how unpredictable these things can be.

Good post! You’ve inspired me to work out current proportions myself (I take a ‘snapshot’ of my holdings every fortnight, but I’ve never bothered to graph them before). Current spread is:

– super 52%

– Aust shares 20%

– cash 12%

– index fund (Aust shares) 7%

– P2P lending 5%

– index fund (int shares) 3%

– US shares (OK, it’s just BRKB) 1%

I had withdrawn some funds from my index funds at the end of 2019 both to cash in on record prices at the time, and with a view to funding a property purchase. Fortunately, as it turns out, I decided not to go through with the purchase, and found myself with lots of cash when Covid hit, so I quietly bought quite a few shares when the prices were good. I didn’t expect the market to recover so quickly, so the proportion in shares is now quite large thanks to some really strong bounces. While it’s tempting to realise some of the gains, I really don’t know what I’d do with them – and the strongest performers still have reliable dividends.

Cash is earning very little (measly 1.25%) but I’m carrying about 2 years worth of living expenses with a view to switching to part time work, doing some study, and changing careers. Most of my current income from work is flowing into index funds to boost them up in the hope that the returns will be strong in the next couple of years. I keep considering buying a small apartment initially to live in then rent out, but the thought of ongoing costs does not spark joy.

Appreciate you sharing Matthew. Sounds like you also had a bit of good fortune there to be able to buy lots when the market was down – that’s fantastic!

Seems like you’re in a pretty good position to switch to part time work for a while and pivot to a different career, very nice. And yes, the apartment is likely going to be more costly to keep than ideal 😉

Honestly, my favourite part is the fact that you track your donations and aim to give a little more each year. I rate that highly. I think we may do the same thing!

Awesome, thanks! I get a bit nervous with things like that, don’t want it to appear like ‘hey look how great I am donating this money’ lol. It’s just part of my long term financial goals that I get excited about so I feel like sharing it.

Hi Dave, Great write up. I am interested in your share portfolio.

Is REIT the Van Eck Vectors FTSE International Property ETF (This has the ASX code of REIT) or is this something else?

Nat

Hey Nat. Nah it’s not a REIT index (not really a fan of the ones I’ve seen). It’s an office REIT which I like and have owned in the past (and is mentioned in my REIT article). There’s another REIT which looks pretty attractive to me as a long term hold which I may also add. Not necessary of course I just like them 🙂

“It’s an office REIT”

There is a sadness in my heart.

Haha! What can I say, still a sucker for a juicy income stream. You can dunk on me later if offices turn into ghost buildings 😉

Sorry, that came out harsher than I intended. Now that you’ve explained it, it makes sense. I just enjoy following the growth of Aussie firebug’s portfolio and was hoping to see the same in yours, but as you alluded to I totally understand the desire for privacy online. Speaking of which, that actually that is my address, I chose the name as a joke.

So ….. you’re not ready to be 100% passive investor hey? I’ll sit back and watch where that goes.

BTW, keep a keen eye on the $A fluctuations with your US and global ETFs, I note the hedged versions of VGS et al have faired much better than unhedged in recent times. With the $A sitting pretty much smack bang in the middle of its historical range against the $US, thus holding 50/50 split of hedged unhedged might be wise ( that’s for the tiny unpassive part of your mind to dwell on ???? )

Nope. You’re sceptical of that? 😉 Semi-passive I guess. I like simple long term investments but I will make active decisions from time to time.

Yeah hedged has been going pretty good as the Aussie dollar has drifted up. But not interested in hedged. Doesn’t fit out needs since we’re mostly invested in AUD assets already. Rather get the extra diversification of currency and countries. I’ll just keep buying VGS, and will do so unless the dollar goes falls significantly when hedged might make more sense. But 95% of the time I’ll spend zero time thinking about that as it’s bound to fluctuate within a pretty wide range 🙂

Thanks for your helpful and informative posts. Well done also on prioritising charitable spending. With your contributions to charity, do you set aside an amount from your everyday budget or have you set up an investment for this and donate the dividends? Thanks!

Thanks Kim. The charity stuff is actually pretty random. We have a few charities which we like and donate to every so often. Nothing is direct debit or on a schedule, it’s very much just when we feel like it. And it’s just cash from our offset account, with the goal just to make it a little bigger each year. I keep an eye on the ‘year to date’ donations by checking our spending spreadsheet, so I can donate more at the end of the year to hit our goal.

I haven’t setup an investment for it, because I want to control it. So if our investments don’t do that well, I’ll still aim to increase our donations regardless.

Wowzers, an article and podcast in the same week!

Chrissy has come early! Cheers Dave!

I find it interesting looking at Fire bloggers portfolio’s, just proof that there is no ‘perfect’ fire portfolio allocation. Even though that exact question seems to be asked on every single FIRE/financial page I’ve ever been on.

On that note, what made you go QVE? A bit of diversification from the Banking/Materials heavy ASX Top20? I have done something along the same line in Investing in WMI is all. Sorry if you have answered this question somewhere before.

Haha thanks mate. Yeah it’s true, everyone is different and gravitates towards different styles of investing, even though we value the same principles – low cost portfolio, diversification, regular investing, long term focus, etc.

On QVE: I like the manager and their style, and it was a way to diversify away from the top-heavy nature of the ASX while still getting a decent income stream. Some of the other small/mid cap funds are too short-term focused (trade too much) or charge performance fees which I don’t like. These days I’ve also added VGS which is probably a more thorough way to diversify.

Nice work with your donations to animal welfare, thank you for your blog and podcast. I am in the 55+ group , though I always find useful info in your blog.

Thanks Leisa, great to have you here 🙂

Hi Dave,

Thanks again for great update, I am at the start of the journey and my first target is to create an investment plan during this Christmas break and start journey early next year. Do you include equity in your PPOR portfolio?

Hey Lionel. Great to hear you’re getting into it! If you have home equity, I would include it in my ‘net worth’ numbers for tracking purposes, but would not include it in my ‘investment portfolio’ numbers. Does that answer your question?

Hi Dave,

I was wondering if VAS was necessary for a dividend growth profile in AU?

VGS I understand for international exposure but if you already have LICs, do we really need VAS?

I’d like to hear your thoughts on this.

Hey Anorat. If owns some old LICs, then no VAS isn’t necessary. I own it because I came to appreciate some of the other benefits of index funds which I wrote about here. That and I didn’t want to buy LICs if they’re trading at a premium. So these days I have both, which isn’t necessary, but doesn’t bother me.

Hi Dave, excellent site with lots of good information! Will take me some time to go through all this useful information :)

I have a quick question in relation to choice of share investment. In my understanding based on what I’ve read so far, the preference seems to be low fee ETFs that provide reasonable return and dividends such as VAS and VHDG. I’m curious as to how these compare to some of the popular investment apps like Spaceship and Raiz that have been providing pretty good returns and low fees too.

Keen to get your thoughts. Thanks!

Hey Kelvin. Thanks for stopping by, glad you’re enjoying the site so far!

Those apps are usually just a different way of investing in a very similar basket of ETFs – nothing special there. I find that using a proper low cost broker is better as there is no restrictions on what you can invest in. Some of those apps are quite limited and the percentage fees are sometimes quite high also. Hope that makes sense.