Big welcome to the 137 new readers who’ve joined us this month.

The Strong Money community is now 6,489 people passionate about financial independence. You can join us here:

It’s about time for another portfolio update.

There’s a fair bit to share today, with the main news being we’ve sold off another investment property as planned.

I’ll get into that, plus share our updated investment income chart for financial year 2020-21, and of course, chat about what shares we’ve been buying and how it’s all going.

Let’s get stuck in.

Below is the current breakdown of exactly where our savings are located. It’s a bit different to last time! You can read my last portfolio update here.

Cash has increased a lot due to the property sale, from 8% to 20%.

Shares are roughly the same. Property equity has reduced from 26% to 17%, with our remaining properties increasing in value in the last few months or so.

Peer-to-peer lending is also continuing to slowly get smaller as we spend the repayments elsewhere.

The interest rates on offer are just way too low for my liking these days at around 3-4%. Our cash was invested a few years back when rates were 8-10%!

Anyway, back to the big change…

The IP we chose to sell was a townhouse close to Brisbane. We decide which property to sell depending on which one has the most equity tied up in it.

It’s not really a bet on which market or property is going to do the best. It’s more about extracting the valuable equity so we can invest that into shares.

For example, a property with zero equity has essentially no opportunity cost, and there’s also little to gain financially by selling it. Unless it’s costing you money of course.

Anyway, the sale went smoothly and we got a pretty decent price – slightly more than I was expecting 🙂

Our cash will be used to cover repayments on the remaining mortgages as well as continually investing in shares every month. I usually try to work it so we exhaust the cash within a few years and then we sell the next property, continuing our steady transition from property to shares.

I explain roughly how we manage our cash during early retirement in this post.

How about those markets ey?

If you haven’t been paying attention, stocks in Australia and the US – the two markets most relevant to Aussies – have been really strong this year.

Both markets are up about another 10-15% in the last 6 months, after the huge recovery during the second half of last year.

I’m sure something will spook the markets at some point, but it’s an impressive run. But far more importantly, profits are now roaring back (and so are dividends) after a sharp drop.

Aussie property in most locations – when we’re not in lockdown – is also performing really well.

Prices are rising with huge demand from homebuyers and cheap mortgage rates. And rents are rising too, thanks to low vacancy rates and low demand from investors for the last few years.

We’ve been lucky to score some nice rental increases here in Perth.

As soon as that happens, of course, the media jumps all over it with hysterical articles about rental affordability. Yes, rents are up. But for context, rents are still lower than they were 7-8 years ago!

For example, we have a couple of villas which rented for $500 per week back in 2013. Those same properties today (after the recent increases) are achieving rent in the low $400s.

After speaking with our mortgage broker a little more about the idea of security substitution, it sounds like it would suit our situation.

This would involve selling a Perth investment property and us buying a home (to live in) at the same time.

Given we plan to buy at some point in this particular location, slowly offload our properties, and aren’t in the position to get a new loan, this should work out well. Especially since this won’t affect our ability to continue building our share portfolio.

In fact, pretty much everything would stay the same. We’d just have an owner occupied property instead of an investment property.

Our cashflow may even improve a little. So on the off chance something which fits our criteria comes up on this little strip, we’ll look to utilise this strategy.

It could take quite a while because we want a block with a fair bit of open space – not paved over with pool, shed, patio, and a huge sprawling house as seems to be the popular style.

I also want it to be in a good position relative to the lake, so we can continue doing our bit to help the local turtles 🙂

Since the last update, we’ve been topping up our holdings. Mainly our international index fund, and also the two REITs we own.

The real estate trusts have jumped in value recently, as I guess the market realised that offices aren’t going to disappear and we can see some light at the end of the tunnel with the vaccine rollout.

It was nice to buy up this commercial real estate at a 10-20% discount to the value of their portfolios, but that opportunity has now disappeared. So now we’ll kick back and enjoy the healthy income stream they spit out.

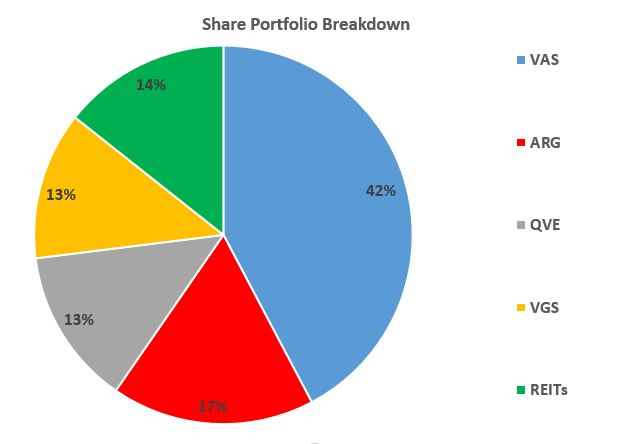

Here’s how our share portfolio looks at the moment.

Our international shares portion is slowly getting bigger as we add to it on a semi-regular basis.

Not much else is going on. Argo has been trading at a premium so I haven’t added much to it for a while.

Our value-focused fund QVE which focuses on small and medium sized companies continues to underperform while still paying a nice income.

I wonder if value investing will ever have its time in the sun again? I’ve seen logical arguments on both sides. Time will tell.

Here is a chart of our passive income from investments over the financial year ending in June.

This includes dividends, franking credits, and interest from peer-to-peer lending.

You might remember in my last update I flagged that our passive income growth streak wasn’t going to continue.

But this result is actually better than expected, given the last financial year was a pretty rough time for dividends.

Companies were rightly conserving cash to stay alive through the 2020 lockdowns. With light at the end of the tunnel and company profits coming back, many businesses now have a ton of extra cash.

This is likely to result in bigger dividends for shareholders over the next year or so. In fact, banks, miners, and a bunch of other companies have already announced some healthy dividend increases.

As someone who loves receiving income from investments, I’m looking forward to seeing those payments roll in!

For new readers: If you’re wondering how we consider ourselves ‘retired’ if our passive income isn’t higher than our household spending, I explain how that works in this article. Short answer: we use cash from offloading property.

It’s quite surprising how much our portfolio has increased since the corona crash last year.

If you’re a new investor, please understand that returns this strong are not normal! Markets don’t go up in a straight line forever.

We’ll experience another downturn at some point, and if you’re building your portfolio right now that’s exactly what you should hope for!

Now, I don’t recommend waiting because we don’t know when that’ll happen. But it’s definitely something to keep in mind, and even look forward to.

Anyway, that’s enough from me. How have your investments been going in 2021? Let me know in the comments below.

I share the findings from surveying my audience. See how wealthy the average Strong Money reader is, how much income they earn, and find out the most common money worries.

Why deliberate spending is my favourite money management style. What it really means and how you can use it as your situation and priorities change over time.

Get my latest content and thoughts straight to your inbox.

A fresh dose of financial motivation to power your journey.

Great update SMA!

It’s very sad to see those P2P allocations shrink from month to month isn’t it?

I am experiencing the same thing in my FI portfolio – there is just not the case for investing new capital at the current rates.

‘Good walkable proximity to turtles.’ It’s the real estate feature of our times! 🙂

Hahaha! Pretty sure no-one else is looking for property with that criteria in mind!

And yeah mate, totally – just can’t justify investing in peer-to-peer if the return has an upper limit of 3-4%.

Great update as usual Dave. I’d be curious to know if you and your readers have considered buying shares in Plenti/Ratesetter now that they are listed on the ASX. Wonder if we could make more money buying Plenti shares instead of via their P2P lending platform….??? ????

Thanks Jeff 🙂

I considered it in the very beginning but decided against it. I’m not really into individual stocks anymore. While the platform is a good innovation and I do like it, I’m not passionate enough to warrant becoming a shareholder… not worth the admin. At current rates, shareholders definitely have more upside potential, but also more downside due to unknown future profitability of the company/competition/etc. Are you thinking of buying some?

I’m still sitting on the fence Dave. I do think Plenti have a good management team in place but they have yet to report a profit let alone dividends! Their most recent annual report didn’t exactly blow out the lights. I may try a modest, speculative punt and see what happens, knowing full well, I could lose it all…

Haha I don’t think you’d be getting a dividend for a while with such a young company 😉 That’s a healthy way to approach such things though!

Another great post Dave! By the way, what’s your target allocation for international ETF e.g. VGS?

Good question mate. I actually don’t really have a specific target in mind. But as a range I’m thinking somewhere in the region of 30-50% and I’ll re-evaluate how I feel about it further down the track when it starts getting larger.

Hi Dave,

I usually try not to be opinionated about these things but i see you still have your pie chart seperating superannuation.

There is a narrative in Australia that super is not really your money, it’ seperate to your finances and it is a seperate asset class.

No one would look at holdings in a trust like one asset class on a pie chart and super should not be any different.

From memory you have a higher allocation to international shares in your super. This could mean if all your super was in international you now have pretty much the same allocation to Vas as you would VGS.

It’s harder to implement but its a better conversation for all Australians about super.

More than happy for you to tell me to bugger off and mind my own business as well 🙂

Thanks

Hi David. I hear what you’re saying. But you need to remember that given we’re living on our personal wealth we are noting down super separate just to give a picture of where our wealth is located from a broader point of view.

If we had a trust or something, that money is accessible to us, whereas super is not, so I think that’s an important distinction and why we do not include super in our ‘shares’ allocation. Yes, it’s in shares, but it’s still a different bucket of long term savings.

So I get the point, but I don’t think it’s really relevant to our particular situation, nor the picture I’m trying to share for clarity with other readers. I certainly think super is a valuable pool of money which is why it’s being included in the overall picture in the first place. But if I was to lump it in with shares etc. then I think it becomes a little confusing/misleading for people trying to follow along.

I’m not saying it’s a separate asset class, but in my mind, super is different, especially for people who are retiring on wealth a couple decades before they can even access that money. So accounting for it separately makes perfect sense to me.

I could also stipulate in every update where super is invested (I do sometimes) and remind people of the importance of it, but that quickly becomes boring to write and read 😉 Though I could probably mention we have X% now invested in international shares for the complete picture. And as we slowly end up with zero property, it should be easier to grasp the overall percentages in different investments.

Dave, with the AUD diving against the USD (to the lower end of the long term range) does that give you pause in putting money into VGS or do you think that it is a minor concern in the long term.

Keep up the great work and enjoy life 🙂

Thanks Jason! No pause at all. To me, it looks like anywhere in the 60-80 cent range is somewhat normal. Outside that, like 50 cents of $1 or something, I may consider doing something different, but in all likelihood probably not.

Important to remember that as the dollar falls like recently, it simply means VGS outperforms. This causes me to put slightly less in than I otherwise would, since my other holdings are cheaper, relatively speaking. And if the dollar goes up a lot, VGS would underperform and my AUD would stretch further, making it more attractive, meaning I would probably be buying more. So there is a natural balancing act happening on either side, whether I look at the AUD or not.

Hey mate. I’m also a suffering QVE holder. Serial underperformers. What keeps you in the stock?

A few things I guess. QVE is something different in my portfolio since it focuses on small/mid sized value companies. It pays a nice income stream. And the fact that people often give up on strategies and funds at the worst possible time. So I’d like to avoid doing that since I still feel fine about the manager’s strategy. But mostly, if it underperforms, it doesn’t really matter to me all that much. Something in a portfolio will always be underperforming.

I’m also in QVE, wouldn’t say i’m suffering. Invested in May’20, total return in a year is almost 30%. The quarterley dividends are a nice bonus and whilst some of the holdings within have underperformed its a nice complimentary holding to the LIC’s i’m in giving me some great diversification away from the usual LIC regulars.

Good point Mark. I probably should have mentioned that it has actually done quite well for us since I was buying in the 70c range during the crash. So it matters when someone bought and the timeframe they’re looking at.

Also hold QVE. Have always found the strategy sound and the diversification away from the usual holdings in most lics & etfs makes it more interesting.

Appreciate the update, it helps us all on our own financial journeys

Cheers Justin!

Great post SMA, Thanks for sharing your insight and knowledge 🙂

Thanks for reading!

Hi Dave – I’m curious to know what your cost base per share is for VAS at the moment given you have been using the DCA approach over the past couple of years or so. Hope you don’t mind sharing that. Thanks mate. Scott

I don’t even look at such things Scott, but went to check it out just for you 😉 Sharesight shows it as $74.80 per share. As we’ve had this convo in the past, a ‘cost base’ is pretty much irrelevant as a long term investor aside from calculating tax etc.

Thanks Dave — good to see your in the mid $70 range — of course an overall lower cost base per share does mean the dividend yield is higher and why people like buying more in the dips or why we look forward to a correction/crash so that we can buy stocks on sale (and lower our cost base), so I think it is relevant. If this was not relevant for you, why not buy VAS in one big lump sum instead of spreading it out over the months as you do? Pretty sure you prefer to DCA for this very reason in case the market does tank. It would suck to buy a pile of VAS shares at $95 only to have it hit $65 a month later from some black swan event. Having said that, the evidence shows that 2/3 of the time we are better off going in with a lump sum.

I hear what you’re saying mate, but I think you’re still not quite seeing my point. As we’ve discussed before Scott, looking at cost per share is interesting, but it’s also looking backwards. If I own 10 shares of VAS and you own 10 shares of VAS, the return on our current dollars invested from today onwards will be identical. Yes we’ve paid different prices in the past, but this is irrelevant to VAS as an investment for us today and for the next 40 years. It’s also irrelevant for whether we should buy VAS today or not.

The benefit of dollar cost averaging is separate to the issue of anchoring to past prices. By your thinking, the highest returning investments are simply the ones bought the longest time ago. Following this further, this is why some people blindly hang on to bank shares they bought decades ago because they think their return is higher than buying something else today, when really, they’re looking at the price they paid decades ago and their ‘yield on cost’.

If someone right now has $1m invested in CBA, but it only cost them $50k a long time ago, every single day they should be considering the tradeoff of having this $1m in CBA vs another investment. If their CBA holding pays them $50k in annual income, they could think “oh great, 100% return per year” I’m never selling. But this is quite clearly ridiculous!

They do not have $50k invested – they have $1m invested right now. This means the yield is actually 5%. Yes it’s been a great investment and the cost basis matters for tax, but focusing on this distorts the decision-making process today. I hope that explains the issue of ‘anchoring’ a bit more.

Hmmm, that’s an odd way of characterising it to me and yes, I know we have touched on it before, but I would hope there is no problem discussing it further. We’re all here to keep learning after all. Here’s a real world example from a person I know:

The person purchased 5,000 shares of CBA when it floated and the purchase price was $27,000. As of this week, that holding is now worth approximately $505,000. The $2 per share dividend in a few weeks will pay $10,000 plus franking credits.

In this example, the CBA CAGR has a 10.25% pa capital gain and a 10.27% pa dividend return — over the 30 years the numbers were lower at the start but as the share price has appreciated and the dividends increased, the returns are compounding.

Personally, I would love a holding that did that every year for 30 years!

In my own case, I spent $53K buying MLT. That is money I earned. I then invested that money. My MLT holding is now worth approximately $87K. By your logic, I have invested $87K; my logic is I have invested $53K and have a capital gain of $34K.

Of course. I’m not saying performance doesn’t matter. What I’m saying is… you have $87k invested today. This means the yield should be measured against the amount of money you have invested in the fund right now. Because you could take that money and invest elsewhere so you need to compare the current income from both investments (if that’s your metric). Not the yield on a price paid years ago.

Often the issue is people look at what they paid to determine what they should do today. Like with my CBA example, that person is not actually receiving 100% return per year. Their capital is now worth $1m (which is fantastic) but they’re getting 5% income on this. So they need to compare what they could be doing with this $1m elsewhere and whether this is still a good investment. Price paid doesn’t matter aside from tax at this point. The shares we own today are in no way affected by our previous purchases. Performance is dictated by today’s numbers and what happens from here.

The problem is, and your main point from the beginning, you’re measuring the dividend yield based on the price you paid… which is backwards looking. The dividend yield we both achieve today is exactly the same for the same holding, it doesn’t matter when we bought. So whether I bought all my VAS yesterday, or 10 years ago, we get exactly the same performance from here onwards. So yes it’s a reflection of past performance, but it should not at all affect our decision making today.

I can’t really explain it any differently than that. I appreciate it’s not very intuitive! This page explains it a little about this ‘anchoring’ stuff also – https://www.investopedia.com/terms/a/anchoring.asp

I live in Perth near the Canning river and love spotting the turtles down here on our walks. Best start to the day!

That’s awesome, they’re the best!

Hi Dave,

Hoping you could provide more detail as to why new investors should welcome a downturn?

All the best with your new turtle family!

Hey Matt 🙂 Well, say you’re investing and building your portfolio over the next 15 years. If the market keeps going up year after year you’ll be paying higher and higher prices – your money doesn’t buy as many shares.

But if the market falls early in your investing, your savings will buy a greater number of shares for the same dollars. Since you get to buy lots and lots of shares when prices are low, when prices eventually recover it has a magnified effect on your wealth since most of your portfolio was bought at cheaper prices. Hope that makes sense.

Hi Matt,

I like to think of a downturn in the sharemarket as the investors’ equivalent of the Boxing Day Sales…. Good value companies are on sale for a good price. Get ’em while you can. This is Warren Buffet’s classic mantra of ‘Be greedy when others are fearful’. Good luck!

Hi Dave, thanks for your column and the great podcasts. In terms of a long term lifestyle choice, is the decision to live off some of the capital generated by selling investment properties slowly eroding your capital base? I know that you are also funnelling some of the sale proceeds into shares, so are you hoping that the capital gain in shares will compensate to some extent for the capital you are spending on living expenses? This model seems also to depend quite strongly on equity residing in the investment properties, which in turn depends on either significant capital gain or significant pay down of mortgage capital – which risks becoming a vicious circle. Thanks for your thoughts on these questions.

Thanks for following along Robyn 🙂

No that’s not necessarily the case. In one sense, yes, if our remaining properties fall in value, we no longer have the equity to take out to reinvest into shares. But using some capital to live off does not mean you are eroding your wealth, provided the total return from your investments is higher than what you are spending.

The equity is already sitting in the properties… so it’s not requiring strong future gains or lots of debt repayment at all. We could sell them now, get the equity out and dump it into shares to create more income, but we’re deciding to slowly sell them off over time for a more slow-and-steady transition. Hope that makes sense.

Cheers for the update Dave.

I also saw a dip in dividend income for the past financial year.. we all knew it would happen, though it wasn’t as bad as I expected which I think for me was in part due to AFI maintaining it’s dividend.

Looking forward to seeing how the 2021-2022 goes.

G day Dave

Cheers for another great update!

On your house sale, was my prediction of it selling quicker then a takes you to read said comment correct?

Cheers

Ococ

Haha well it was actually the tenant who bought it. When the agent went thru to size up the property they expressed a keen interest in buying it, so you could say it was pretty quick/easy 🙂

Hi Dave I am new to investing and FIRE and your content has helped loads!

What I seem to understand from the reading I have done (ATO and ETF tax guides), Is that ETFs can distribute you less money than they attribute to you but you have to pay income tax on the amount they attributed to you. So you are paying income tax on money you didn’t receive.

So say the grossed distribution amount is $120 but you only get $100 but you have to pay tax on the $120, they give you $20 as an increase to your cost base so you save tax on CGT if and when you sell.

They say they give you the money you didn’t receive to you as AMIT increased cost base which reduces your CGT tax if you were to sell. I just can’t see how that works.

So effectively if you are holding ETFs for long term, you can be paying tax on money you have not received because AMIT ETFs are not required to distribute all their income anymore. I don’t see this talked about anywhere in the fire community? What are your thoughts on it?

Hey Whit. Thanks for reading, that’s great to hear!

AMIT is a pretty confusing topic, a lot of which honestly goes over my head. My understanding of the idea is it was brought in to make ETFs more tax efficient, so I’m not sure how it could be that the opposite is true. I would possibly post this on the FI Australia Reddit page and you might get an answer from someone clever there.

My thoughts are: the cost base increases and decreases are so small relative to the size of one’s shareholding that over the long term it’s likely going to amount to a rounding error. So I don’t give it any thought. What’s the alternative? The managed fund versions of the index are far less tax efficient than the ETFs.

Yeah I am not sure what the cost bases adjustments would be on a large portfolio to be significant or not. I just noticed it when I went to do my tax. That I have to pay tax on income I don’t receive, and you don’t get it back until I sell my shares, even then I can’t see it working out neutral. Plus if you dont plan to sell your shares you are worse off. I did post it over on FI Australia Reddit, no one seems to be across it.

https://www.reddit.com/r/fiaustralia/comments/pygnnq/how_does_etf_amit_cost_base_adjustment_effect_tax/

The other thing I find interesting, is that now that EFTs are AMITs they can hold onto income similar to LICs if they choose to, as they are not required to distribute it anymore, but you have to pay tax on it if they do it (but you dont get the income).

So then, is the only other difference between LICs and ETFS the fact that LICs are managed and ETFs track and index?

But wouldn’t this cut both ways as there are (I believe) both cost base increase/decreases? Meaning it won’t always work the same way. It could also be the case that your taxable income is lower and the cost base decreases rather than other way round, making it beneficial and the opposite to your example. It also depends on one’s tax rate at the time which obviously goes from high at the start of a FI journey to low or zero later on.

LICs and ETFs are different in regards to strategy, which is quite significant in itself. The difference in performance can vary markedly, to the tune of 0-3% per annum, far more impactful than any of these tax intricacies. LICs are also taxed internally at a rate of 30% – because they’re companies. So their taxation is also very different from an ETF which does not pay tax itself.

What if we considered these tax issues to be an added cost of ETFs (not sure yet if that’d be accurate but let’s run with it). It might add a few basis points to costs each year, in which case ETFs would still be the cheapest and most efficient option available (for index performance and tax effectiveness).

Nothing is perfect but I fail to see a better idea unless you’d like to change strategies or the uncertainty of this tax issue is a dealbreaker for you.

Hi Dave,

I’ve been listening to your podcast for some time but haven’t been a regular follower of your blog so interesting to see what actually makes up your share portfolio.

I’ve been looking for something similar to QVE. I have my 25% Aussie share allocation completely filled by A200 but I don’t like how concentrated it is in the top 20 companies. I’ve been thinking of replacing a smallish portion of my Aussie allocation with ex20 (MER 0.25%). QVE looks interesting but I was surprised to see the MER is 0.90%. I know there is research to suggest that active management in the small cap/value space could do better than the index but that is a pretty significant fee. From listening to your podcasts, I’m surprised you would go for a LIC with a fee this high.

If you were starting again now do you think you’d still buy QVE?

Hi Scott. You’re right, QVE is a high fee LIC, which I’ve held for several years. It’s really tough to say whether I’d invest in it from day one… it would depend how simple I wanted my portfolio to be.

Keeping it ultra simple, no, I wouldn’t. But that said, I still like it as something which is active and focused on value/quality/smaller companies as I’m not religious about indexing. I’m also a sucker for a nice income stream which QVE provides 😉 I guess the answer is maybe! But I do think ex20 is a good option… I also don’t mind the equal-weight Aussie fund too.